DNB - Dun & Bradstreet: High Debt And Private Equity Overhang Keep Us On Sidelines

2023-11-09 20:31:18 ET

Summary

- Dun & Bradstreet has a Neutral rating due to limited margin upside, significant leverage, and continued selling by its PE owners.

- Q3 results showed resilient growth driven by North American and international segments, with slight decline in margins.

- We believe the company has made significant progress under its new management, however, current value fully captures the risk-reward.

Investment Thesis

We ascribe Dun & Bradstreet ( DNB ) with a Neutral rating as a result of 1) limited margin upside drivers in the near term 2) significant leverage and limited cash generation which would necessitate a refinancing at unfavorable terms and 3) continued overhang as a result of selling by its PE owners who still own about 26% in the company and had been aggressively selling over time at lower prices despite improving visibility on the company's ability to drive mid-single digit organic growth and stable operating margins.

Company Overview

Dun & Bradstreet has a long heritage dating back to 1841 and has been a leading provider of business decisioning data and analytics focused on US commercial credit data. The data is based on the aggregation of key accounts receivable data from its contributors with each having a unique DUNS number allowing its clients to have a holistic view on the 500 mn companies within its database serving a wide range of use cases from financial services, telecom and retail to government, transportation and manufacturing. It has diversified revenue base serving more than 240,000 across the globe with Top 50 clients contributing only 25% of the revenue. North America forms the biggest market which contributes over 70% of the total revenue with the rest of the contribution from international markets. The company was taken private in Feb 2019 by an Investor Consortium and was subsequently listed again in 2020.

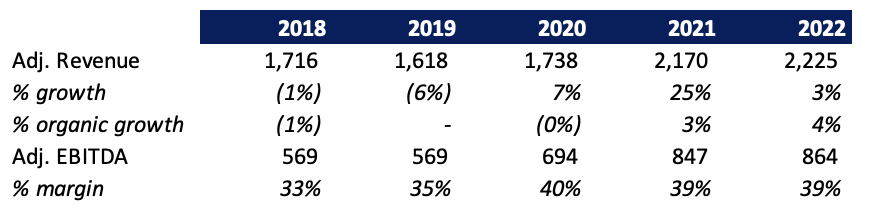

Historical Financials

The company posted over a 6% revenue CAGR during the period of 2018-2022 with organic growth accelerating towards mid-single digit growth in 2022.

{kind=link}

Note: Adj. Revenue and Adj. EBITDA excludes purchase accounting deferred revenue adjustment which was done by the Investor Consortium post take-private transaction.

Under the previous management before the take-private transaction, it had a bloated expense and a less efficient product offering leading to significant underperformance in delivery. Post the take-out, the company had a new leadership under its new owners which streamlined cost operations and enhanced its delivery offering leading to a strong upside to the margins as well as returning back to positive organic growth. The company was also able to shift to long term multi-year contracts which comprises about 50% of the total compared to just 20% in 2019 driven by enhanced delivery. However, the acquisition of Bisnode, Eyeota and NetWise in 2021 and 2022 were margin dilutive which lead to a slight decline in margins.

Mixed Q3 Results

The company reported mixed Q3 results with revenues increasing 4.8% YoY on a constant current basis, slightly ahead of the consensus estimates. The resilient growth was driven by 4.5% cc growth in North American segment (which comprised about 72% of total Q3 revenue) along with a 5.8% cc growth in the International market segment. Growth in North America was driven by 4.9% growth in Finance & Risk segment on the back of a strong double digit growth in in Risk Solutions (third party risk and supply chain management products) along with a single digit growth in Finance Solutions while legacy credit segment focused on small business credit continue to decline. In addition, Sales & Marketing segment also grew 3.9% cc driven by MSD growth in Master Data Management partially offset by weakness in D&B Hoovers professional contact data as a result of macro pressures. Growth in international segment was driven by 3% growth in Europe along with high single digit growth in UK & Ireland, APAC and Worldwide Network.

Adj. EBITDA margins declined by 10 bps to 40.0% which came slightly below the consensus as a result of decline in both international and North American segment due to higher data acquisition and processing costs along with a jump in personnel costs offset by lower selling and marketing expenses and lower professional fees. It reported an Adj. EPS of $0.27 slightly ahead of the consensus estimates pegged at $0.26.

The company reiterated its full year guidance with total revenues expected to be $2.3 bn driven by 4% organic growth (vs 3.75% previously) and further tightening its EBITDA guidance to $880 - $910 mn from $875 - $915 previously, with the midpoint guidance intact. In addition, it raised the lower end of its EPS guidance to $0.95 - $1.00 from $0.92 - $1.01 demonstrating the continued follow through and in-line YTD results.

Debt Overhang

The company has sizeable leverage with total debt outstanding of $3.7 bn and cash balance of just $230 mn. This yields to a net leverage ratio of 3.9x implying a significantly high leverage. Following its recent debt and extend arrangement to its swap agreement, it now has 87% of its debt as fixed (including interest rate hedges) through 2025. Majority of the debt ($2.7 bn) has a scheduled repayment in Feb 2026 while the rest of the repayment is required to be made in 2029. The company has about 9-10% of capex as % of revenue historically and has about 30% - 40% of free cash flow conversion over the years.

Assuming a 4% organic growth driven by continued traction within its Finance & Risk segment as well as stable growth in International segment, we project Revenues to touch about $2.5 bn by 2025. We further assume stable EBITDA margins of 40% going forward as a result of limited upside potential currently amidst most of the cost efficiencies realized. This eventually leads to an FCF conversion of 45% projected in 2023 which is expected to improve to 54% by 2025. We assume the company necessarily has a status quo on dividends and likely make the dividend payments just as in 2023. However, even factoring a non-dividend payment event, the cash shortfall is likely to be elevated which would compel the company in refinancing which could be at unfavorable terms.

Author

Valuation

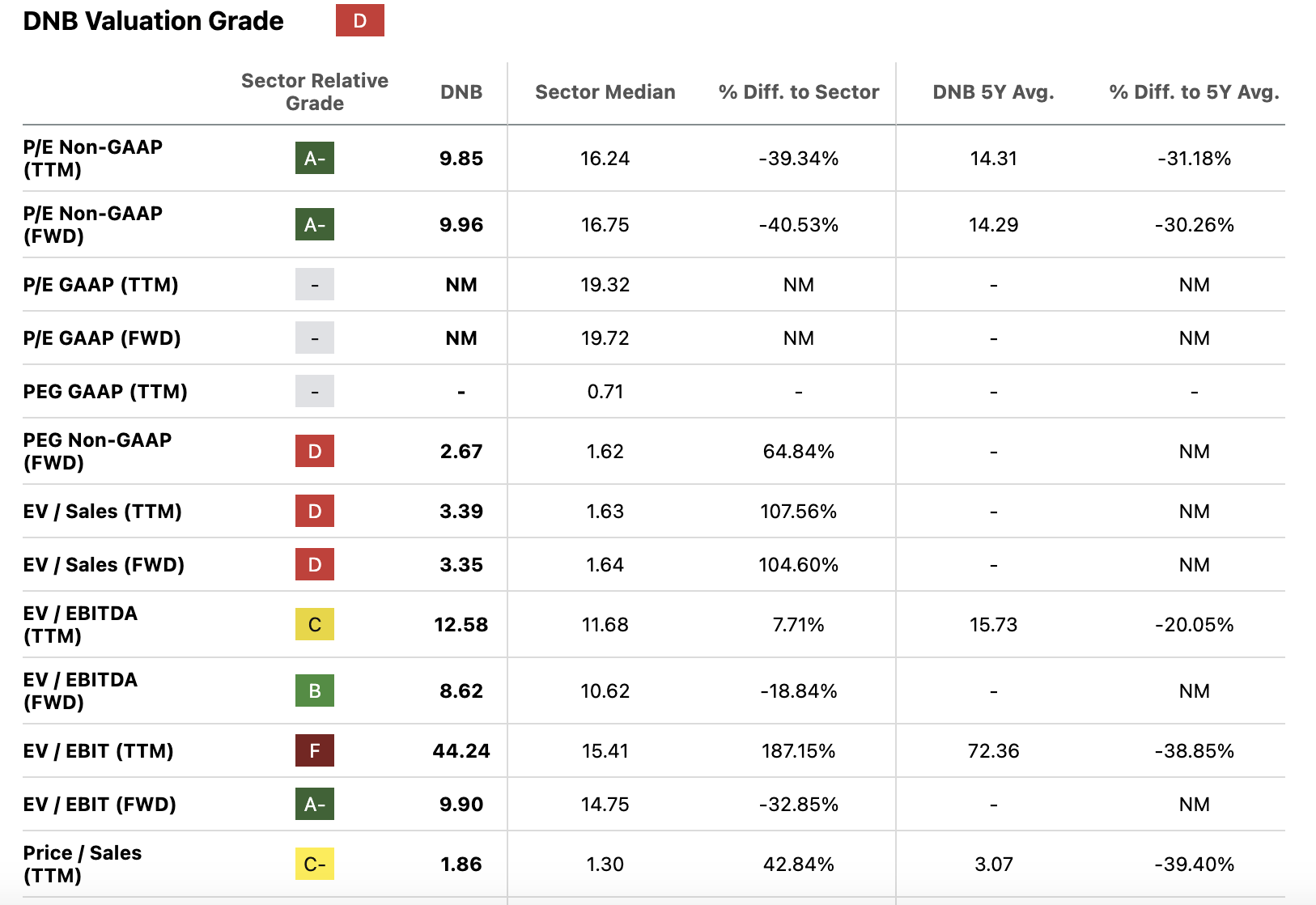

DNB trades at 8.5x EV/ Fwd EBITDA which appears to be at a discount to the sector median. On a P/Fwd EPS basis as well, the company trades at a significant discount to its peers (10x compared to sector median of ~17x). The company also trades at a significant discount compared to its long-term average as a result of the PE interest garnering a takeout premium. We believe despite the 'on paper' undervaluation, the current price fully reflects the mid-single digit organic growth and 40% EBITDA margin as echoed by the management during the investor day in February this year. Also, on PEG basis, the company appears to be at a significant premium reflecting the relatively weaker fundamental and operational outlook compared to its peers.

{kind=link}

In addition, the Private Equity firms Cannae Holdings and Thomas H. Lee partners still hold about 26% in the company and have been progressively selling the stock at continued lower prices. We believe despite the signs of a turnaround with mid-single digit organic growth and stable EBITDA margins, stretched balance sheet and selling by its PE owners continue to be an overhang. We initiate at Neutral as we believe the current valuation fairly reflects the risks and the volatility in the current environment.

Risks to Rating

Risks to rating include

1) High financial leverage and limited cash generation ability to invest in products and key growth areas such as AI can hamper future growth prospects

2) DNB faces significant competition from Experian, Transunion and Equifax in commercial credit data while LinkedIn and ZoomInfo competes with its Hoovers product. Any loss of market share as a result of increasing competitive intensity can dampen organic growth

3) Upside risks include growth in its risk/ trade segment along with international expansion and continued shareholder activity such as dividends and repurchases

Conclusion

DNB has made significant progress after several years of stagnant top line growth and bloated expenses suppressing margins. This could well be a new DNB 2.0 with a new management who has made significant changes in driving mid-single digit organic growth and margin expansion. However, we believe the balance sheet still remains a work in progress and would likely necessitate a refinancing while the current price fully captures the potential mid-single digit organic growth and stable margins. In addition, continued selling by the PE investors continue to remain an overhang which are likely to looking to exit over time. We initiate at Neutral.

For further details see:

Dun & Bradstreet: High Debt And Private Equity Overhang Keep Us On Sidelines