DNB - Dun & Bradstreet Holdings Q3: AI Initiatives Might Be A Key Growth Driver

2023-11-16 15:32:49 ET

Summary

- DNB is underperforming its peers in terms of growth outlook and net margins.

- They've taken initiatives to develop their own AI capabilities and partner with IBM, which could drive revenue growth.

- Revenue has been growing and its organic revenue growth is positive, but its net margin is negative compared to its peers.

Investment action

Based on my current outlook and analysis of Dun & Bradstreet Holdings ( DNB ), I recommend a hold rating as it is underperforming its peers in terms of growth outlook and net margins. Although DNB’s third quarter reported revenue growth, its growth outlook is in the mid-single digits, whereas its peers are expected to grow at double digits. In addition, DNB’s net margin is negative while its peers are positive. However, I do note that they have taken the initiative to develop their own AI capabilities and are also partnering with IBM. With the rapidly growing AI market, I believe these initiatives might be a key driver of revenue growth, but it's important to monitor the upcoming quarter’s performance to gauge the success of these initiatives.

Basic information

DNB offers commercial data, data analytics solutions, and data insights that support business decision-making processes. It also offers a wide range of products, such as risk management, finance solutions, sales and marketing, and supply chain management.

Over the last 5 years, its revenue CAGR has been around 5.3%. Revenue has been growing since 2018 from $1.7 billion to 2023’s $2.2 billion. Its gross margins have remained at a consistent rate of about 68% over the years. In terms of net margin, it has improved significantly. In 2018, it reported a negative net income margin of 41%, but by 2022, it had improved to negative 0.1%, almost breaking even. 2018’s high net loss is attributed to its high interest expense, which accounted for about 21% of revenue. But over the years, it has gradually improved to 8.6%. In addition, its total operating expenses as a percentage of sales have improved from 2018’s 66% to 2022’s 58%.

Review

For the third quarter of 2023 reported on November 1st, DNB’s revenue grew 6% year over year to $589 million. Adjusted EBITDA grew 6% year over year to $235 million. Therefore, the adjusted EBITDA margin is about 40%. When compared with the previous quarter’s results, it shows that DNB is growing both in revenue and adjusted EBITDA. In the previous quarter, the adjusted EBITDA margin was 37.2%, which represents an improvement of 2.8%. In terms of revenue growth, it accelerated from the previous quarter’s 3% growth to the current 6%.

DNB’s organic revenue growth has been trending positively. For the third quarter, it reported organic revenue growth of 4.8%. This is an improvement of 0.9% when compared with last quarter’s reported organic revenue growth of 3.9%. Increasing organic revenue growth shows that the demand for DNB’s products is strong. Not just organic growth and demand; another important metric I look out for is retention rate because it drives recurring revenue. It is important to capture market share, but equally important to retain it. In the third quarter, DNB reported a retention rate of 96% for North America and 93% for the international segment. A high retention rate is a signal of the overall popularity and stickiness of its solutions. So far, it has been trending in the high 90s, as the previous quarter’s international retention rate was 94%.

Currently, multiyear contracts account for 55% of North American revenues and 53% of overall revenues. Management expressed their goal of achieving 60% of overall revenue under multiyear contracts. While some might argue that locking in pricing with a multiyear contract might cause them to lose out in terms of pricing strategy, I believe otherwise, as locking in contracts improves long-term growth visibility and also allows them to make better investment decisions as they are able to forecast cash flow. This is important for DNB, as right now its third-quarter net income margin is very close to breaking even.

As mentioned by management, they are still seeing strong demand for AI-powered data analytics solutions due to the need to improve financial and operational performance. In response to this demand for AI-powered solutions, DNB has already embarked on its AI journey.

"North America and International continued to capitalize on the need for businesses to better leverage data and analytics in driving both financial and operational improvements, which is only being further magnified by the advancements of generative AI solutions." 3Q23 call

Firstly, DNB launched its D&B.AI labs back in June 2023. This platform allows co-development with its clients to create specific and tailored solutions for them. I believe such a co-development platform will further improve DNB’s branding and increase demands. Its off-the-shelf solutions have already won many clients hearts, as shown by its high retention rate. By offering a customized solution, I expect this product to drive up its demand even more, further bolstering its long-term growth.

Apart from internal AI development, DNB is also forming strategic partnerships. It has teamed up with IBM to create and introduce new innovative products into the market. As DNB’s solution mainly focuses on data analytics, I believe the integration of DNB’s data with IBM’s Watsonx will create significant value for DNB. IBM’s Watsonx is an AI platform that is built for enterprises. Thus, it empowers and allows DNB’s solutions to have AI abilities integrated into them, making them more sophisticated and intelligent and increasing their data analytics efficiency. Thus, it positions DNB well to create additional value for its existing clients, which will support retention. In addition, such a solution and partnership will attract more new clients, further increasing its organic growth momentum. Th e AI market size is expected to grow to $2.5 trillion by 2032 from the current $538 billion, and this represents a huge market opportunity for DN B. Together with IBM, I believe this partnership is going to drive DNB’s long-term growth outlook and allow them to tap into this fast-growing AI market.

Valuation

I believe DNB will grow at 4% in 2023 and 2024. Management guided 2023 full-year revenue to $2.3 billion, or about 4% growth. This growth rate is also in line with market estimates. I believe 4% is highly achievable given the robust revenue growth reported in the quarter. In addition, its multiyear contracts, which account for more than half of total revenue, will ensure long-term stable revenues. DNB's initiatives to develop and incorporate AI capabilities into its existing solution and its partnership with IBM further support its growth as the AI market is expanding at a rapid rate, and they are well positioned to capture that growth.

{kind=link}

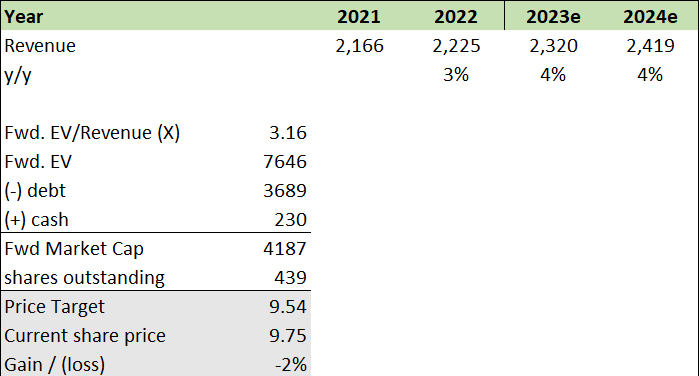

DNB is currently trading at 3.16x forward EV/Revenue. Its peers are trading at a median of 8.25x. Given that DNB’s negative 1.14% net margin is significantly lower than peers median of 17.36%, and its NTM growth rate of 4% is lower than peer’s median of 12%, it's fair for DNB to be trading lower. My price target is $9.54, which represents no gains. Given the fact that its net margin is negative and its NTM growth rate is 66% lower than peers’ median, I recommend a hold rating for DNB.

Author's work

Risk and final thoughts

With DNB’s consistent growth in revenue and EBITDA, combined with its high retention rate and investment in AI, if DNB were to report better than expected results for the next few quarters, I would expect to see its multiple moving closer to peer’s median if its growth outlook and net margin were to inch higher.

DNB’s third quarter results were robust, with revenue and adjusted EBITDA growing in the mid-single digits. Organic revenue growth has been consistently improving due to its strong branding and market positioning in the data analytics segment. With more than half of its revenue under multiyear contracts, its future revenue growth has become more certain, and with this visibility, management guided full-year revenue growth of mid-single digits. Currently, there is demand for AI-powered solutions, and DNB has already hopped onto the bandwagon by launching a new AI-powered product as well as partnering up with some of the largest names in the market. However, DNB underperform peers’ in terms of growth outlook and margin strength. Its share price is trading at my target price based on its current forward EV/revenue, which I argued to be fair. With this in mind, I am recommending a hold rating.

For further details see:

Dun & Bradstreet Holdings Q3: AI Initiatives Might Be A Key Growth Driver