DNB - Dun & Bradstreet: Lacks A Competitive Advantage While Having A Bloated Balance Sheet

2023-12-19 03:54:18 ET

Summary

- DNB’s revenue has mildly grown during the last decade, with a CAGR of +4%. This growth has been consistently low, although accelerated post-pandemic. EBITDA has lagged behind at +2%.

- We are unconvinced by DNB’s competitive position, with mediocre organic growth and significantly larger peers.

- The biggest issue with this stock is its balance sheet, with a substantial debt balance contributing to a loss on a NI basis.

- DNB’s performance relative to its peers is moderate, with superior margins but a lack of organic growth. The company’s focused business model allows this to occur, although the growth trend at its size is concerning.

- DNB may appear attractively priced but we are not convinced. A 11% NTM FCF yield cannot be enjoyed by investors and does not sufficiently reflect the risks faced and scope for underperformance.

Investment thesis

Our current investment thesis is:

- DNB is a good business that we struggle to see becoming great. The company faces significant competition, in an industry [DATA] which is going through a democratization trend. It is becoming easier to collect and analyze data, with AI accelerating this. DNB lacks the scale and network effect to sufficiently offset this, with its larger peers far better placed to innovate in an exploitative way.

- Compounding our negative assessment is the company’s balance sheet, which is bloated with debt and Management is seemingly in no rush to deleverage. This will restrict the cash flow potential of DNB for a substantial period of time, deterring new investors.

Company description

Dun & Bradstreet ( DNB ) is a leading global provider of business data and analytics, enabling companies around the world to improve their business performance through data-driven insights.

Share price

DNB’s share price development since it was listed has been disappointing, losing over 50% of its value. This corresponds with a difficult period for the markets as a whole, although likely reflects an inflated IPO price.

Financial analysis

{kind=link}

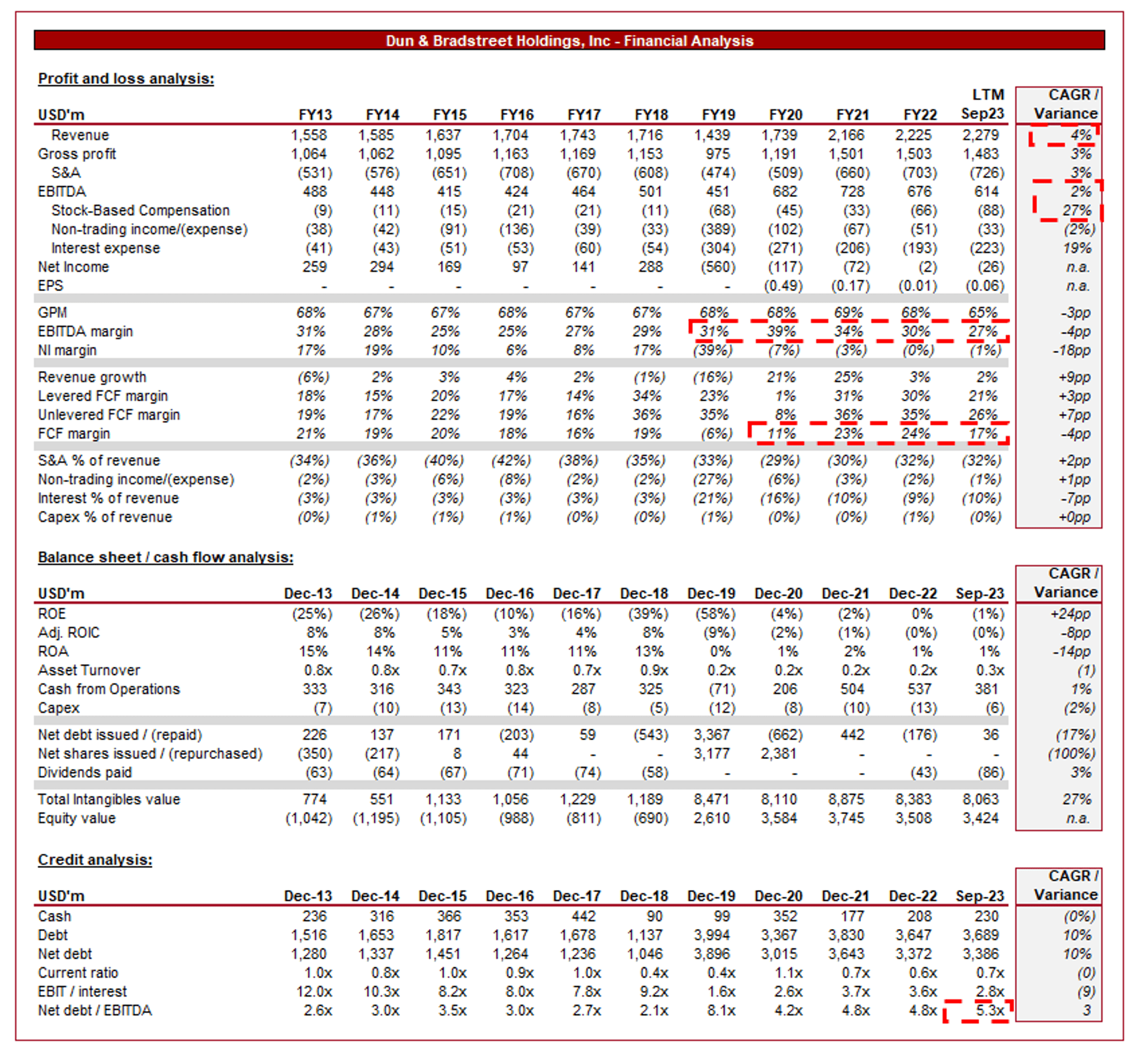

Presented above are DNB's financial results.

Revenue & Commercial Factors

DNB’s revenue has grown at a CAGR of +4% during the last decade, while EBITDA has lagged behind at +2%.

Business Model

DNB is a data business, having created a depository of proprietary data that can be utilized to make informed business decisions.

D&B collects vast amounts of business data from various sources, including public records, financial statements, trade references, and other proprietary sources. It adds value through compiling, organizing, and managing this data to create comprehensive business profiles and credit reports. DNB focuses heavily on data accuracy and quality. Its rigorous verification processes ensure that the information they provide is reliable.

DNB operates on a subscription-based model where businesses pay for access to their database and analytical tools. This is a lucrative monetization model as it allows for consistent cash returns and scope for up/cross-selling over time. Clients include banks, corporations, and government agencies.

In conjunction with these Finance services, DNB offers risk management solutions that help businesses assess the creditworthiness of potential clients and partners. These services include credit reports, business monitoring, and predictive analytics, assisting clients in mitigating financial risks associated with their business relationships.

In addition to Finance & Risk services, DNB provides sales and marketing solutions that enable businesses to identify and target potential customers. Their data-driven marketing services help clients optimize their marketing campaigns, with the objective of increasing their customer acquisition rates.

The primary reason DNB can earn the margins it does is by providing essential services for businesses, especially those engaged in B2B transactions. Its insight is critical to making quick decisions that are financially beneficial. The critical nature of its data and insights ensures consistent demand and high unit economics.

The complexity of data aggregation, verification processes, and the vast database DNB maintains creates reasonable barriers to entry for potential competitors. This said, the company’s low organic growth trajectory implies it has lagged behind the industry, during a period of rapid credit expansion and technological development (thus demand for technology). We attribute this to its competitive advantage not being sufficient.

DNB’s business model is solid. The company earns attractive unit economics for its services while benefiting heavily from the democratization of data to continually develop its data capabilities. With it providing essential services, the company is positioned well to achieve LSD/MSD growth long-term so long as it remains competitive. This said, we struggle to see what the unique value proposition is, which means there are greater risks associated with a decline in its competitive position or subpar growth.

DNB competes with numerous larger businesses, including Equifax ( EFX ), Experian ( EXPGF ), and TransUnion ( TRU ). Their expertise and scale will likely limit DNB’s ability to grow beyond a certain point. DNB’s willingness to support small businesses does mean it targets customers that the bigger players will likely avoid, but we nevertheless see this as a risk to its future trajectory. Data accumulation and analysis is not a unique trait, particularly as access improves through technology.

Secondly, the risk of AI should not be understated. This will allow for the collection, cleansing, and analysis of data rapidly, contributing to greater competition and alternative services for users. Again, we believe DNB lacks sufficient differentiation to offset this risk. The business does not have a material network effect like the leading credit agencies for example.

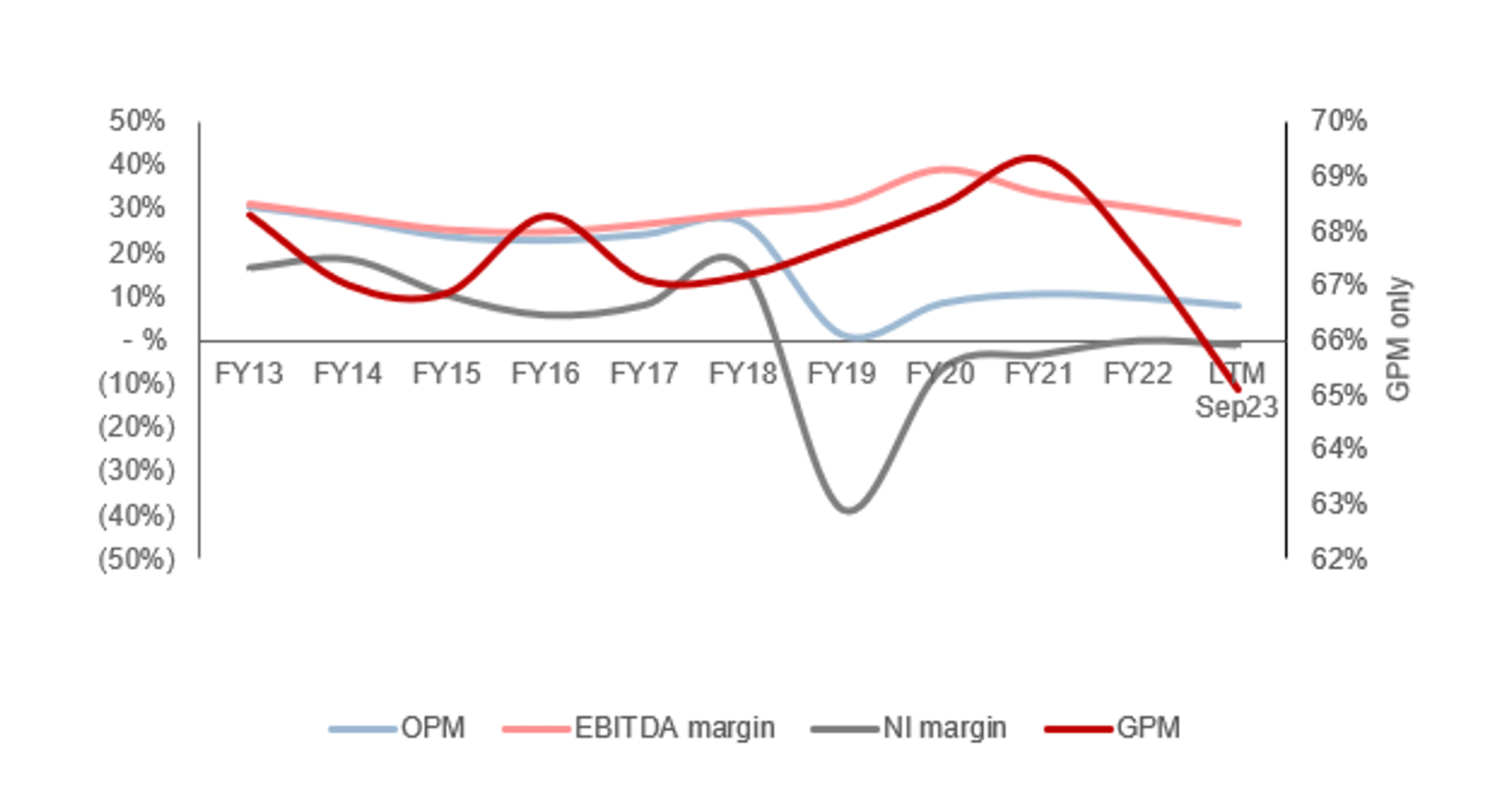

Margins

{kind=link}

DNB’s margins have been fairly volatile during the historical period, although the trend has been broadly flat. Its strong margins are a reflection of the nature of its services, with low incremental costs to provide its data services. In recent years, NIM has significantly declined, with substantial debt raised to fund its transaction in FY19. This has contributed to interest payments amounting to ~10% of revenue, a barely sustainable level. With interest rates expected to remain elevated into FY24, NIM will continue to remain deflated. This said, we should acknowledge that FCF is strong enough to service payments and reinvest within the business.

Quarterly results

DNB’s recent performance has slowed, with top-line revenue growth of (0.6)%, +0.8%, +3.2%, and +5.8% during the last four quarters. In conjunction with this, margins have declined, with an LTM EBITDA-M of 27%. Despite the slowdown, we broadly consider this a good quarter for the company.

The slowdown in revenue growth is principally attributable to reduced M&A activity, contributing to a reliance on organic growth. Further, the broader macroeconomic environment continues to weaken, contributing to a host of businesses seeking to cut back spending to protect margins, as well as reduced small-business growth. Further, the heightened interest rates are contributing to softening demand for credit services.

Key takeaways from its most recent quarter are:

- Finance and Risk segment is struggling more in North America than Internationally, while the opposite is the case for Sales and Marketing.

- Revenue from its Public Sector and Small Business Solutions sub-segments has materially softened, while Master Data Management and Digital Marketing solutions have performed well.

- Management believes they are seeing returns from its investment in service development. There has been a focus on enhancing and expanding its proprietary data sets, increasing its use cases. Further, investment has been made in modernizing its platforms and solutions and incorporating generative AI tools. Given the healthy organic growth during difficult conditions, we suspect this investment is paying off.

Balance sheet & Cash Flows

As touched on previously, DNB’s balance sheet is a mess. The company’s current ND/EBITDA ratio is 5.3x, with the majority of its debt serviced on a SOFR + CSA +325bps rate. Management is committed to deleveraging its balance sheet, although this does not appear to be occurring rapidly. Management is still acquiring assets consistently and even paying dividends, which we consider unusual given the cash cost to the business currently. We do not consider this an efficient allocation of resources.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a step-up in its growth from its organic trajectory, with a CAGR of +5% into FY27F. This appears reasonable when considering smaller, bolt-on acquisitions are likely in conjunction with organic growth.

Further, margins are expected to sequentially improve. This is reasonable in our view, given the scope for monetization from subscriptions (up/cross-selling), as well as operating cost leverage and dilution of SBC.

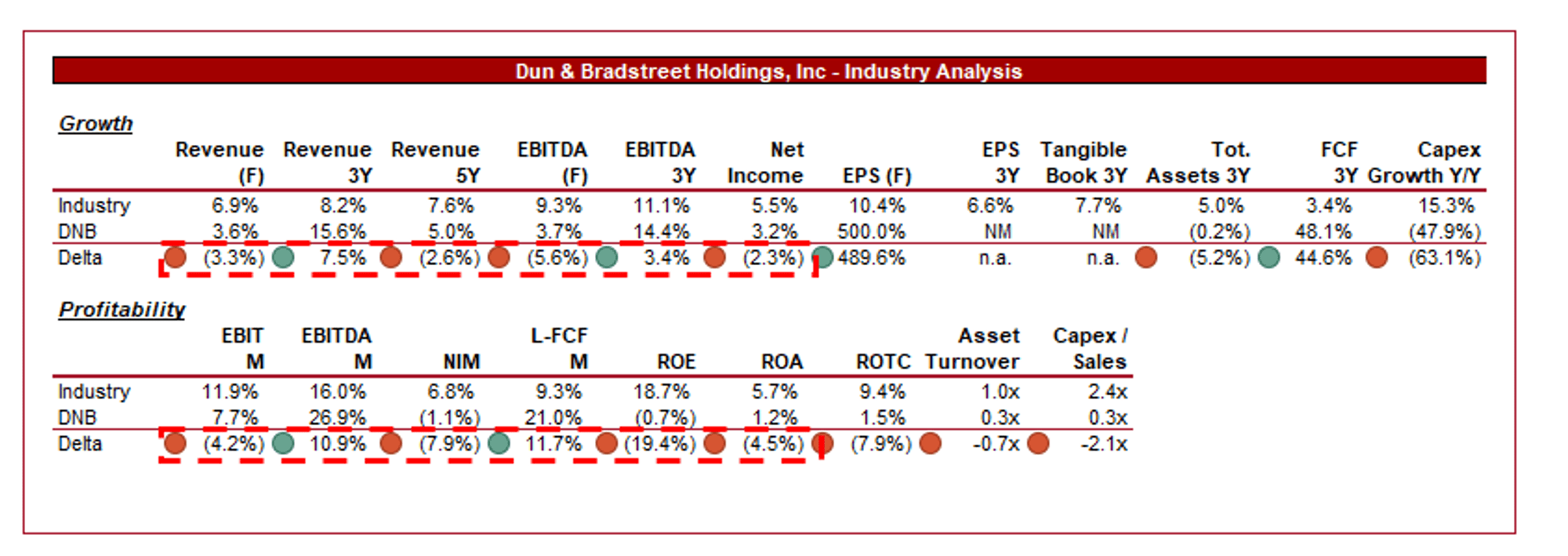

Industry analysis

{kind=link}

Presented above is a comparison of DNB's growth and profitability to the average of its industry, as defined by Seeking Alpha (29 companies).

DNB performs moderately relative to its peers, although does not stand out. The company’s growth has been strong on a 3Y basis, although this is heavily attributable to acquisitions. On a 5Y and forward basis, DNB is lacking and implies a diluting market share.

Further, DNB’s margins are its key strength, with a substantially higher EBITDA-M and LFCF-M. This is a reflection of its current business model, with a focus on data and subscription modernization allowing for minimal incremental costs.

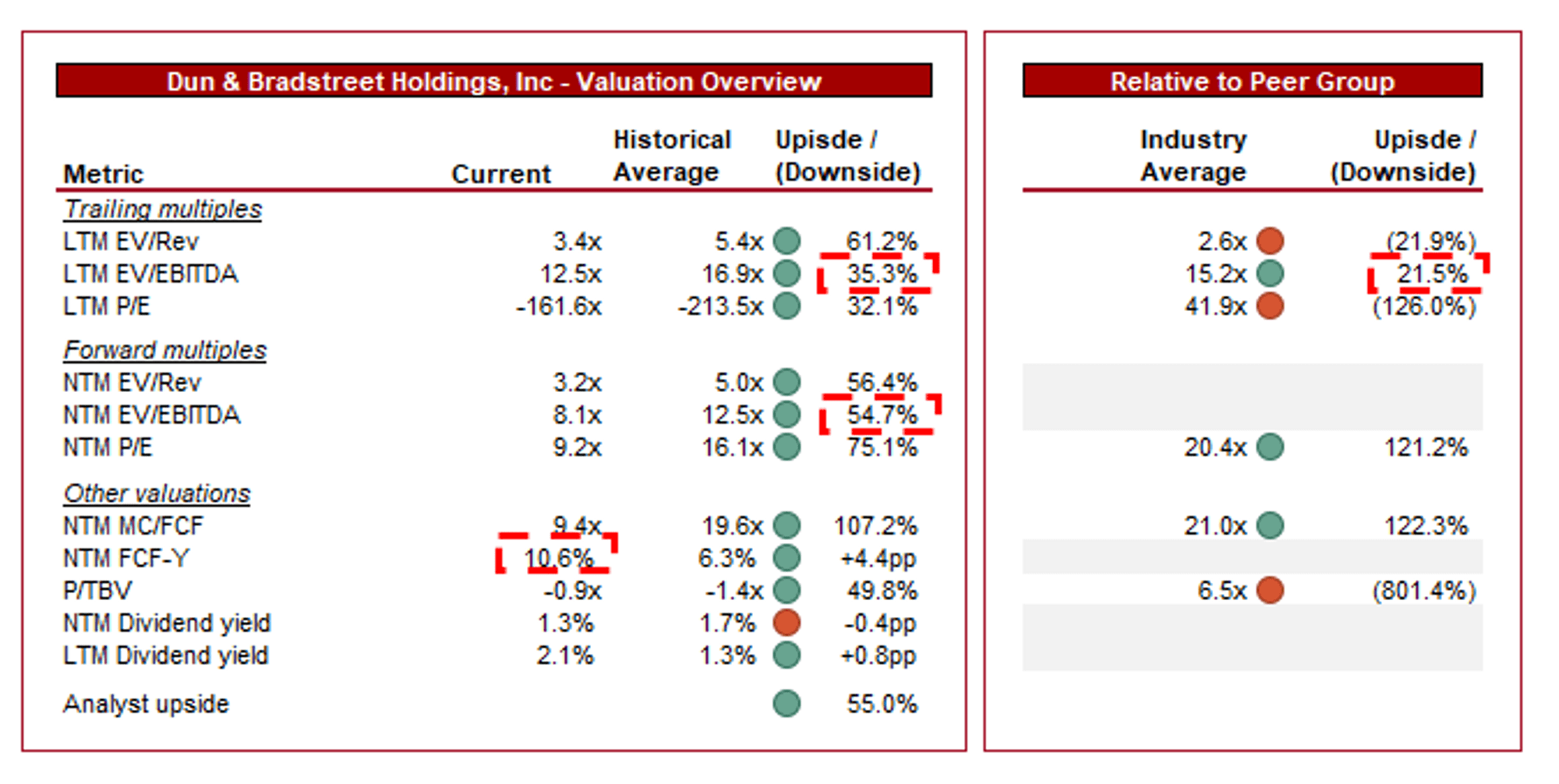

Valuation

{kind=link}

DNB is currently trading at 13x LTM EBITDA and 8x NTM EBITDA. This is a discount to its short historical average.

DNB’s valuation appears attractive from a fundamental basis, with its strong business model allowing for a NTM FCF yield of ~11%. This does not wholly reflect the risks associated with the business in our view, with its significant debt balance that requires reducing and competitive concerns.

DNB is currently trading at a discount to its peers, with a ~21% discount on a LTM EBITDA basis and ~122% on a NTM FCF basis. This is attractive in our view, given the company’s comparable financial performance with margins offsetting growth weakness.

Key risks with our thesis

The risks to our current thesis are:

- Utilizing AI to close the gap to its peers.

- Expanding product offering to diversify into less competitive segments.

- M&A accelerating growth.

Final thoughts

DNB is a solid business, with truly impressive margins and scope for reasonable growth. This said, we are not wholly sold. The company faces significant competition, with its position reasonable but likely to face challenges as DNB pushes for greater scale. We struggle to see what sufficiently differentiates the company that will allow it to exceed the growth rate of its mature peers.

Further, the company is heavily indebted, which will restrict its ability to distribute to shareholders. This means greater pressure on changing investor sentiment through outperformance, which does not look possible.

For further details see:

Dun & Bradstreet: Lacks A Competitive Advantage While Having A Bloated Balance Sheet