BFFAF - DuPont: Keep Dropping And I'll Keep 'BUY'ing

Summary

- We're revisiting DuPont de Nemours, Inc., now yielding over 2.5% with one of the more significant chemical companies in the world.

- We're now down 20% from my last article - and the undervaluation is starting to reach almost ridiculous levels for DuPont.

- DuPont is mostly valued at a premium - it has a BBB+ credit rating and some of the better other fundamentals out there.

Dear readers/followers,

DuPont de Nemours, Inc. ( DD ) is a company I keep writing about, and I'll keep pounding the table as the company drops lower. We've now reached multiples we've not seen for quite some time. As always, valuation is the key to investing, and certainly for investing in industrial companies like DuPont.

Let me show you why I'm even more positive about the company here.

Revisiting DuPont a few months later

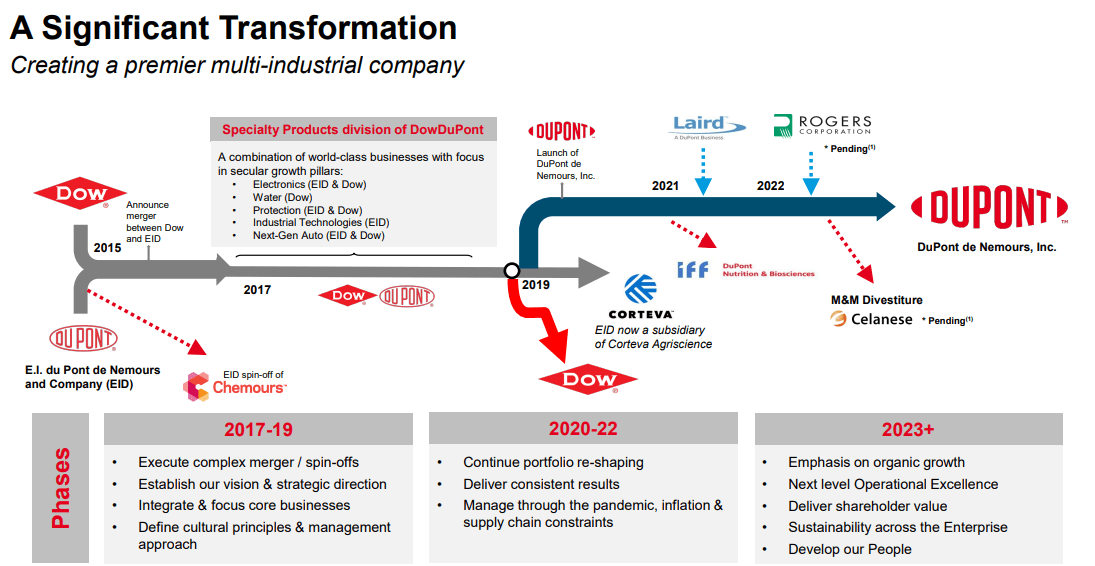

So, the company's results do not in any way justify the drop in valuation. DuPont is an industrial company - a world-leading one in key sectors, as a matter of fact. It's a company that's in the midst of a transformation.

{kind=link}

It's a transformation that's been ongoing since 2017, including some significant creations of spinoffs such as Corteva, Chemours ( CC ), and others. I own Chemours as well, by the way.

The industrial and commodities sector has been hit pretty hard over the past few months, but the company has a truly excellent overall sales mix that we can consider as we move in here.

{kind=link}

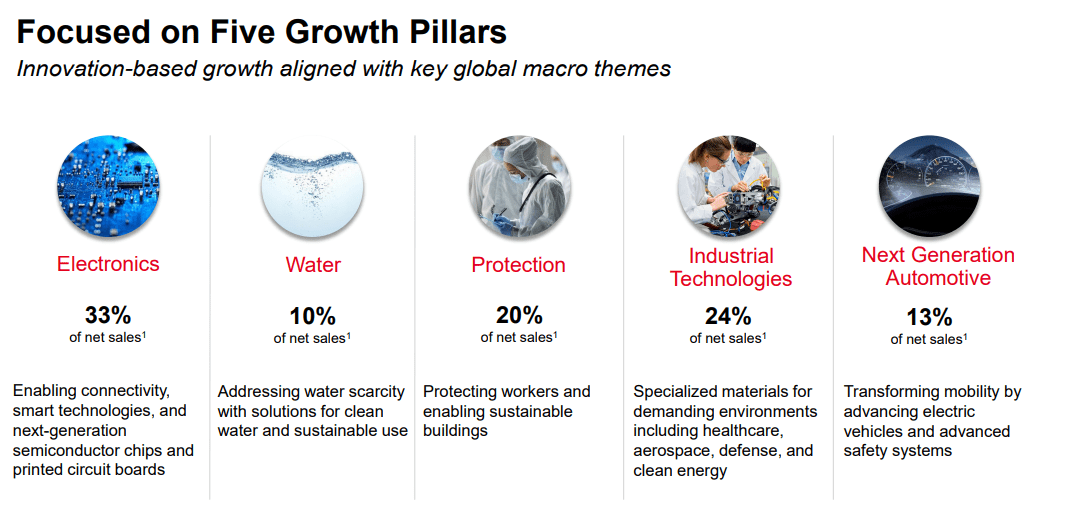

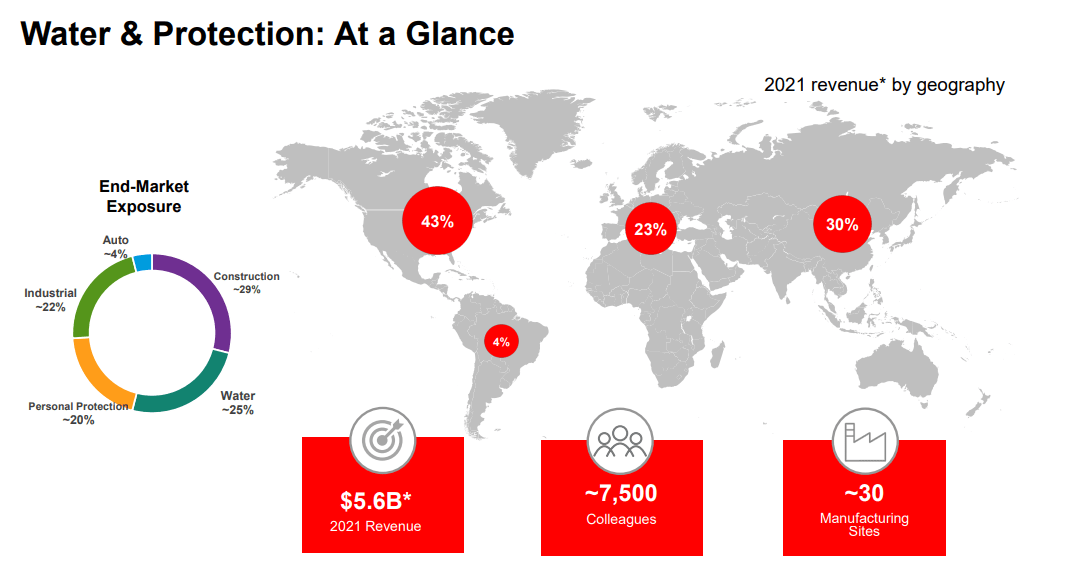

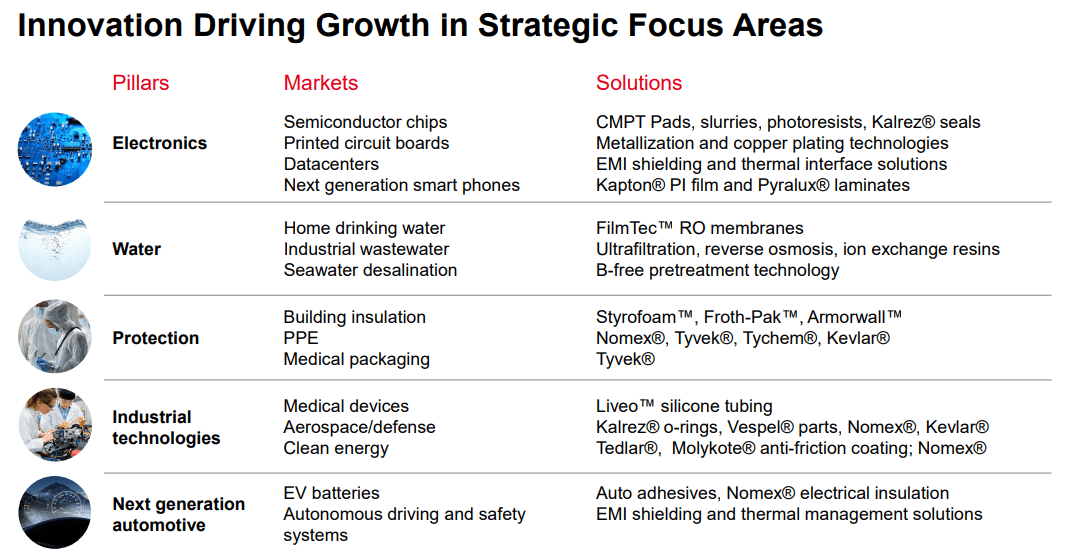

The company is, of course, also global. DuPont has most of its sales outside of the U.S., and nearly 50% of net comes from Asia. Its 90 manufacturing sites across the world generate $12.6B in net sales on an annual basis. DuPont no longer has a Mobility & Materials segment. This was a much better fit for Celanese. DuPont has been made into Water, Protection, and Industrial/Electronics, which have been turned into the main sales drivers. These are market-leading business segments that will become crucial going forward. This especially goes for Water & Protection, where every single sub-segment is attractive to the macro we're moving into - Safety Solutions, Shelter Solutions, and Water technology. All of these segments are and will become even more crucial going forward.

DD also has a very appealing customer mix - 18% of sales to industrials, 11% to Automotive, 12% to telcos, 15% to data processing, 18% to mobile, and 26% to consumers. Again, plenty of diversification in industrial here. Exposure in Water & Protection is even better, as I see it.

{kind=link}

Growth for DuPont comes from a few sources, as we move forward. The company, of course, can push prices through its market-leading position in key markets. It also has one of the leanest cost structures in the entire industry, coming in at less than <1% of annual revenues, and the management team that pushes DD is one of the best in the industrial sector.

it can't, of course, fight against macro trends in a way that essentially ignores or develops in opposition to these - but it can try to lessen the overall impacts, which I see DD doing. For each product segment, the company has plenty to work with and work on.

{kind=link}

Also, company fundamentals remain extremely solid. With debt of less than $12B and extremely well-laddered maturities (nothing much until after 2026, looking at company bonds), and over 80% in long-term debt, there's plenty to like about fundamentals here.

The company still has some clean-up work to do in terms of its portfolio. Non-core still comes to over $2B in overall proceeds once the final actions are complete. These include things like Sustainable Solutions., Hemlock JV, Semi Solutions, Solamet, Cleantech, and Biomaterials. The company also has a strong M&A trend, having bought ultrafiltration water membranes, MEMCOR, and many other things. The Rogers Corporation M&A is currently ongoing. Much of the company's future growth is not expected to be organic, but bolt-on.

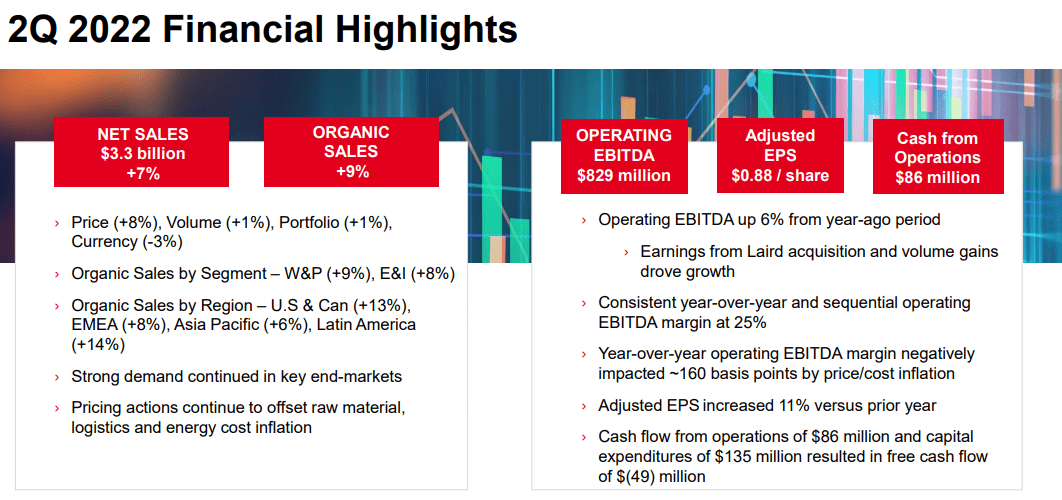

We have 2Q22 results to go through here. These results continue to not justify the current valuation drop, as the company delivered 9% top-line organic growth, strong demand, and full offsetting of raw material/logistic/input impacts through pricing actions.

{kind=link}

Top-line isn't the bottom line, but the company also sees increased EBITDA and increased EPS. Looking at the bridge, headwinds included a weaker product mix and start-up costs as well as input issues, but EPS was up from Laird performance, semi/tech, and share buybacks, reducing the company's overall share count. Both of the company's segments were up - Electronics and industrial more than Water & Protection, but still impressive numbers. The company also delivered some FY22 guidance and 1H22 forecasts. The current numbers do not correspond with most analyst forecasts here, as analysts expect at least 3-5% lower EPS than DuPont does, coming to a significant decline to 2021 YoY.

There's still a lack of clarity here regarding the intended M&A of Rogers Corporation, which DD is in the middle of working on. With a very strong sales trend, and good segment expectations (impacted somewhat by China problems), the company is set to deliver yet another decent fiscal in 2022, despite some of these ongoing issues.

2021 was high - but 2022 is expected to come in above 2020, and definitely above pre-pandemic 2018 results, with 2023E expected to be even stronger. The company seems to trade as though expectations are for the company to face significant problems or fundamental issues. This is not the case - not from company forecasts, and not from when I dissect earnings or current risks.

There are some considerations worth noting here.

The main ones are of course some market resilience considerations for the company's main segments, in particular, order rates. The company is currently seeing them at expected levels, but are expecting a drop-off/softness as we move forward. Demand is going down slightly as we move into 3Q22/2H22, but the foundational demanded drivers are still very much in place.

We're going into plenty of uncertainty. With inflation rising, macro and geopolitical factors at tensions not seen since the end of the era of the cold war, it's only natural that companies face significant valuation and other pressures that cause share prices to behave in such a manner. However, when it comes to DuPont, it's my firm stance that this has now actually gone a bit too far.

Or perhaps, it's better said that it's "going" a bit too far.

DuPont Valuation

So why do I say this?

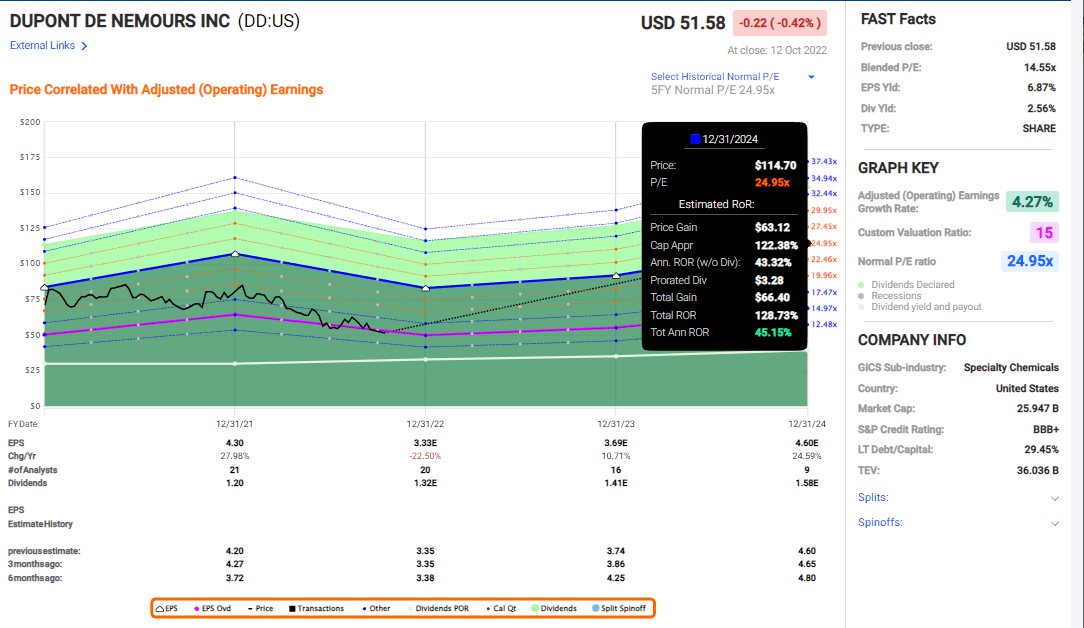

Well, because there are two ways to view DuPont. One is the valuation premium perspective, which actually has been pretty well-established for the past 5-10 years or so. Going by averages DuPont should trade closer to 20-25x P/E due to its massive quality, industry exposures and fundamentals. From this perspective, DuPont is one of the most undervalued industrials currently out there available for you to invest in.

The upside to a 24.9x P/E reversal is no less than 128% RoR in around 3 years.

DD Premium upside (F.A.S.T graphs)

{kind=link}

Is this likely? Based on what essentially amounts to slightly more than EPS reversal in 3 years, I would say no . The company isn't worth a 20-25x P/E here, especially not going into a double-digit 2022E EPS decline. Now, i don't think the EPS is going to come in quite as hard as forecasts are saying here, but I do think that we will see EPS decline - and that it will definitely be double-digit YoY percentage drops.

Beyond that, I say that reversal is likely based on the company's performance record. However, the second perspective we can use to view DD is a very conservative 15x P/E. Keep in mind, this is nearly 10x P/E below the company's typical premium. 2 years ago and suggesting this sort of discounting, it probably wouldn't have been taken all that seriously. Now on the other hand, we can do it and stay fairly realistic given where the market has been going.

The company is now trading at around 14-15x P/E normalized. That means that even on the basis of a 15x P/E forward valuation with estimates that, granted, have an abysmal forecast rate, I can still see an upside at such a discount valuation. The upside, in this case, is over 16%, coming to estimated 40% RoR from one of the world's more significant industrial companies out there.

The upside here is realistic , and it's market-beating - that's what makes this such a great deal.

The company is fundamental in a very fundamental sort of sector. It's a stalwart with a massive history, and despite recent significant reorgs, the company has a lot of that character left, as it seeks to streamline and focus the business on attractive segments.

The obvious solution to any multiple uncertainties in a thesis is to buy the intended investment at a discount - a massive one if you have to. To me, that's exactly what we're starting to see here for DuPont.

S&P Global gives the company an upside here and echoes the "BUY" stance I myself hold on the business. 15 analysts, 14 of which have either a "BUY" or "Outperform" rating, give the company an average of $72.24/share based on a range of $45-$100/share. Even the lowest of these targets is close to the current valuation that the market assigns to DuPont. The upside based on averages is around 40%.

This marks a convincing upside to me, and that's why I remain a "BUY."

Valuation

The company has proven quarter after quarter that positive sales momentum has continued - and I personally consider FactSet 2022E targets of $3.3/share to be on the lower end, and choose to forecast at a $3.5/share this year. The dividend is also expected to grow at a relatively rapid rate, increasing by more than 10% per year until 2024E - and based on payout, the company may certainly afford this.

Combine this with below 15x P/E, and you may understand why i go for "BUY" here.

Thesis

My thesis for DuPont is as follows:

- Chemicals/Industrials are still an investable segment, and I continue to invest major capital in businesses such as BASF ( BASFY ), Linde ( LIN ), Air Liquide ( OTCPK:AIQUY ), LyondellBasell ( LYB ), Covestro ( OTCPK:COVTY ), and others. DuPont is now becoming a greater and greater deal. And remember, companies tied to commodities tend to not perform at all badly in environments like this.

- The company combines the appeal of specialty chemicals with a great market position, excellent fundamentals, and a yield that could double in less than 5 years if the company's growth plan remains intact. I also like the pricing the market is giving some of the options for the company here, which is why I might go for some of them.

- I give Dupont a "BUY" with a PT of $85/share for the longer term, legitimizing some of the company's premium that we see here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

DuPont: Keep Dropping, And I'll Keep 'BUY'ing