BROS - Dutch Bros: Financial Prudence Or Growth Ambitions? At A Crossroads

2023-11-14 13:33:55 ET

Summary

- Dutch Bros Inc. Q3 results exceeded expectations, signaling continued growth and a bolstered balance sheet post-dilution.

- Management's caution regarding the likelihood of achieving self-funding or positive free cash flow in 2024 introduces an element of uncertainty.

- As I navigate its nuanced landscape of financial decisions and growth ambitions, I recommend caution.

Investment Thesis

Dutch Bros Inc. ( BROS ) delivered Q3 results that put a dent in the bear case. Succinctly put, its Q3 results demonstrate that Dutch Bros is evidently still in growth mode. It now appears highly likely that Dutch Bros will continue to grow in 2024 at approximately 30% CAGR.

Moreover, after its shareholder dilution in Q3, Dutch Bros' balance sheet is now in a much better position.

On the question of how long until this business is self-funding, or free cash flow positive, management implies that investors should not expect this to take place in 2024.

For now, I remain neutral on this name.

Quick Recap

In my previous neutral analysis , I said:

I've been following Dutch Bros closely, and I must admit, I have my doubts about its future. While it's been a growth story, things seem to be changing. The era of cheap money is behind us, and Dutch Bros' unwavering commitment to growth has created a disconnect.

Author's work on BROS

As you can see above, despite its alluring narrative, this stock's performance has not been a rewarding investment, unless you managed to time your entry at the exact bottom tick of this year, which is an unlikely feat.

Dutch Bros' Near-Term Prospects

I'll first describe Dutch Bros' bull case, followed by describing the bearish argument.

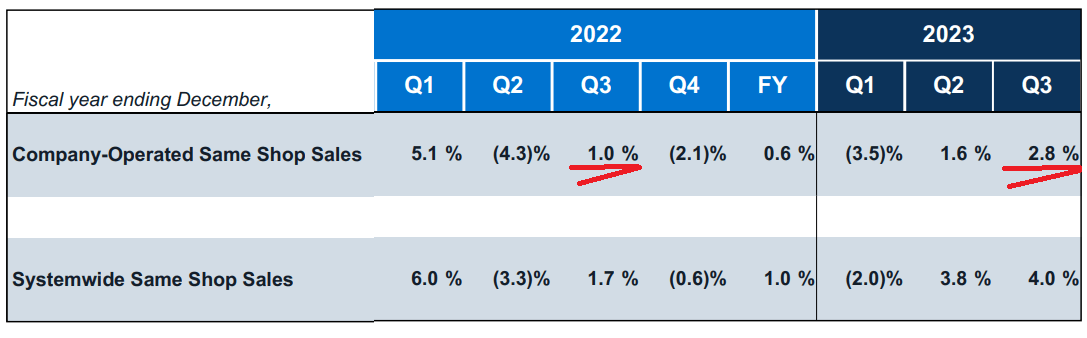

Dutch Bros' recent results exhibit promising prospects, notably demonstrated by its robust 4% increase in comparable sales during Q3 .

{kind=link}

What's more, its company-operated same-shop sales were also nicely positive with an increase of 2.8% y/y. When asked on the earnings call about the drivers, management openly noted that price increases were the main driver of this upswing.

Without turning too bearish too soon on Dutch Bros, I'll state that I'm not compelled toward companies that support their growth strategy through pricing increases. Those price hikes tend to be one-off and not supportive of long-term stable growth. It's better for the overall business to increase its customer base, rather than charging more for the same product.

Moving on, the company remains committed to opening more shops, for example in Texas, while maintaining a steady pace of development. Also, during the earnings call , there was a discussion around a change in shop manager roles and responsibilities, aligning incentives with revenue growth. Aligning employee incentives with more sales should translate into better growth over time.

All these indicators appear to reinforce the narrative that Dutch Bros is still in growth mode.

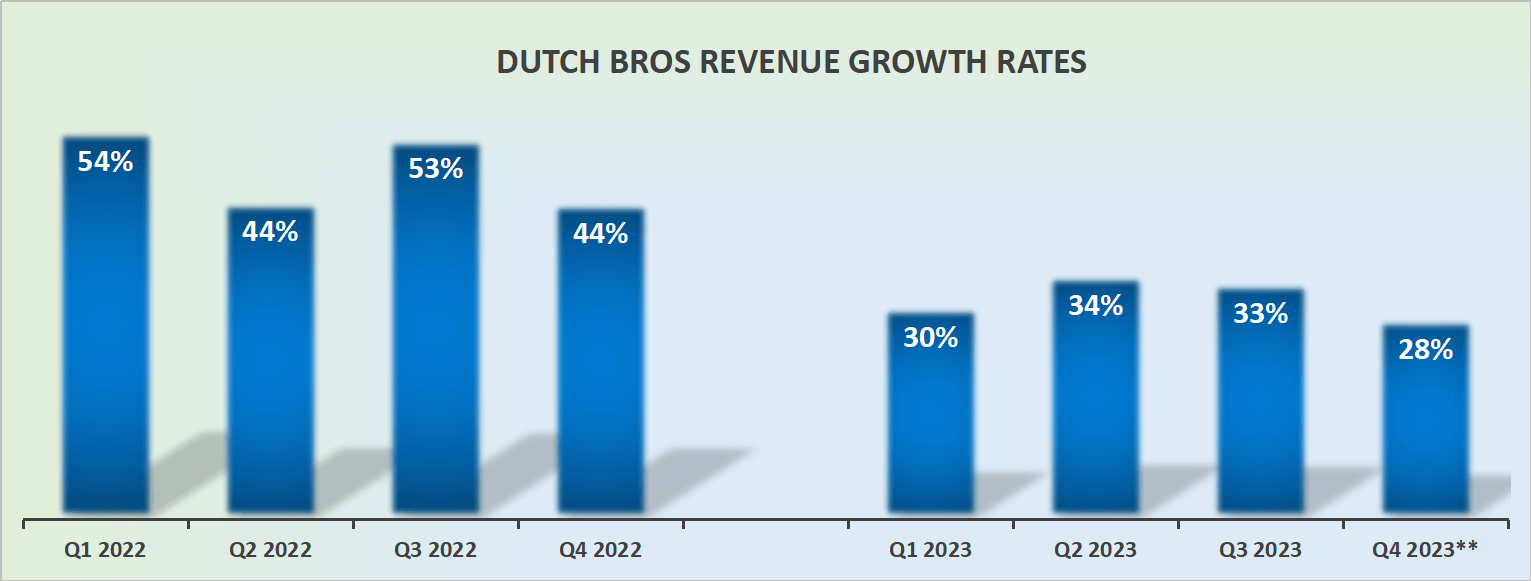

Revenue Growth Rates Are Stabilizing

{kind=link}

Dutch Bros doesn't have a history of massively sandbagging its results, as you can see below:

SA Premium

Consequently, assuming that Dutch Bros beats its own estimates by around 3% on the top line, this would see its revenue growth rates in Q4 reach 28% y/y.

That being said, its comparables in 2024 will ease up, which means that Dutch Bros is likely to continue growing at approximately 30%-35% CAGR in 2024. Once again supporting its narrative, that Dutch Bros is a growth company.

There are some minor pesky detractions worth considering. For example, Dutch Bros faces near-term challenges, particularly in managing labor costs. Despite impressive y/y gains in labor efficiency for five consecutive quarters, the company acknowledges upcoming challenges, including an investment in shop manager labor effective November 1 and the impending California wage increase as of April 1, 2024.

The latter poses a potential threat to margins, and while the company is evaluating productivity and other options before resorting to pricing, uncertainties in wage and incentive structures create a need for careful strategic planning.

Now, we'll turn our focus to the bearish arguments.

Balance Sheet in Focus

Dutch Bros holds $150 million of cash and equivalents. After successfully diluting shareholders in Q3, its balance sheet is in a much better position.

Last week during the earnings call, Dutch Bros noted how by diluting shareholders and shoring up its balance sheet, the company will be able to improve the interest payment on its debt.

I don't know what the updated interest payment will be going forward, but according to my rough estimates, I suspect that Dutch Bros will continue to pay at least $25 million per year as interest on its debt.

Put another way, 20% of its go-forward run-rate operating profits will be used to pay down its debt. And this is the absolute lowest estimate for its interest expense.

On top of that, when asked pointedly on the earnings call when the business would return to positive free cash flow, management gave the impression that it would not be free cash flow positive in 2024.

That being said, Dutch Bros has already diluted shareholders in 2023, therefore I can't imagine that management will be too eager to dilute shareholders further in the near term.

Consequently, I suspect that if necessary to choose between further capital raises and slowing down its growth ambitions, I believe that Dutch Bros will opt for a smaller business that can thrive, rather than a larger business that's striving to survive.

The Bottom Line

As I reflect on Dutch Bros' recent performance and the implications for its near-term trajectory, a sense of uncertainty lingers.

While Q3 results exceeded expectations, showcasing sustained growth and a strengthened balance sheet post-shareholder dilution, there's an air of caution.

Management's acknowledgment that the business might not achieve self-funding or positive free cash flow in 2024 introduces an element of unpredictability.

The recent Dutch Bros Inc. focus on improving the interest payment on debt, while enhancing financial resilience, raises questions about the potential trade-offs between debt servicing and sustaining growth momentum.

As an observer, I find myself in a neutral stance, grappling with doubts about Dutch Bros' ability to seamlessly navigate the evolving landscape and reconcile its growth aspirations with financial prudence.

For further details see:

Dutch Bros: Financial Prudence Or Growth Ambitions? At A Crossroads