BROS - Dutch Bros: High Growth High Price

2023-12-05 04:43:55 ET

Summary

- Dutch Bros’ total store count has grown 19.22% from the end of 2022 to 800 locations, which will continue to boost revenues.

- Increasing coffee prices and demand will continue to drive earnings growth.

- The company has regained profitability and has experienced rapid top and bottom-line growth.

- However, valuation is extremely expensive.

Overview

Dutch Bros (BROS) is a coffeehouse chain that sells hot and cold drinks, non-coffee options, and baked goods. The company primarily operates in the western region of the country, with a majority of its stores being located in California, Oregon, Washington, and Arizona. Dutch Bros also has a significant and rapidly expanding presence in Texas.

The company reported revenue of $265 million for Q3, and EPS of $0.14, a beat by $0.07. Even though Dutch Bros reported strong Q3 earnings, their stock price has dropped 29.56% YoY due to poor performance overall in the retail sector. While tailwinds such as new store openings, rising coffee demand, and improving financial health are set to boost the company’s earnings, we believe that valuation remains a key issue for Dutch Bros.

New Growth Opportunities

New Store Openings

Dutch Bros is opening new stores at an impressive rate, as demonstrated by the 39 new store openings in Q3 alone. In addition, the company has been rapidly expanding their presence in new markets. For instance, after entering the Texas market in 2021, Dutch Bros has already opened 131 stores in that state. This impressive rate of growth has driven the company’s total store count up 19.22% to 800 locations so far this year. The company has plans to continue this growth by opening 67 additional stores by the end of 2023.

Dutch Bros

These new stores have contributed significantly to Dutch Bros’ top-line, with a revenue increasing 33.15% YoY to $265M in Q3. Due to the consistency of the company’s expansion and the fact that it has already yielded significant results, we believe that Dutch Bros is well positioned to continue revenue growth through new store openings.

Rising Coffee Demand

Global coffee revenue for both instant and roast coffee has steadily increased at a CAGR of 2.8% from 2018-2023.

Statista

This rise is projected to accelerate in the next 5 years, with forecasts projecting a higher 4.6% CAGR from 2023-2028. Overall, global coffee revenue is expected to reach a whopping $110B by 2028. We believe that this increasing demand for coffee paired with Dutch Bros’ expanding location count will allow the company to rapidly increase its revenue.

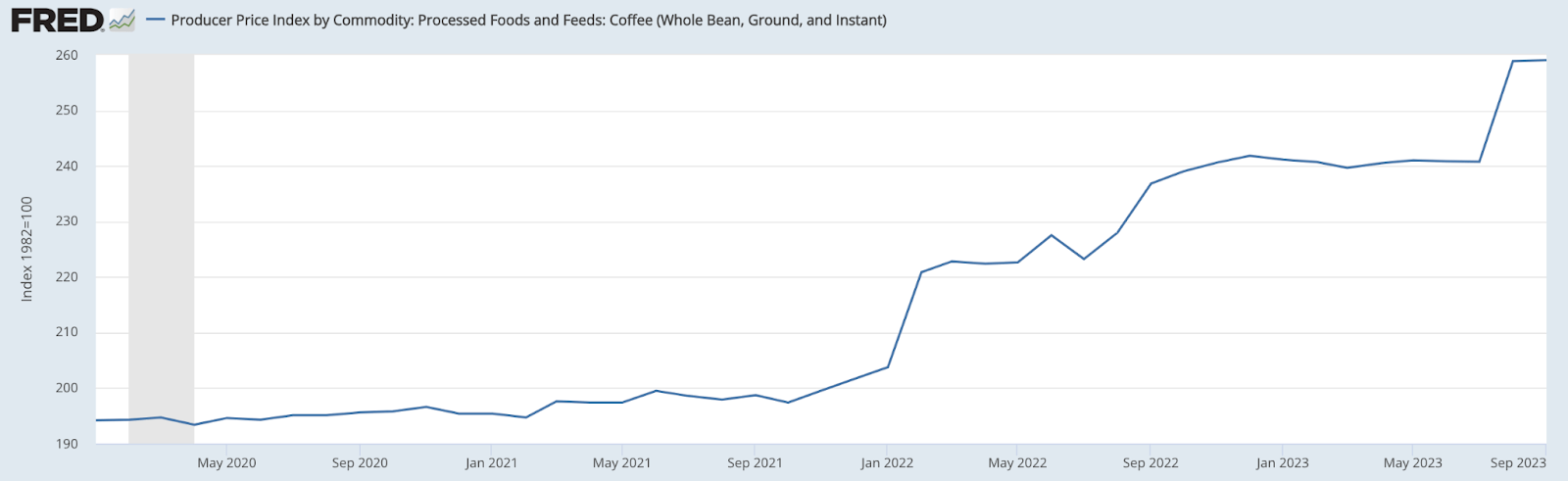

Increasing Coffee Prices

Due to strong demand and rising food prices, the price of coffee has been rapidly increasing over the past 3 years at 10.11% CAGR.

{kind=link}

The rise in coffee prices has enabled Dutch Bros to raise its prices, which has improved the company’s margins and allowed it to regain profitability. As such, Dutch Bros reported a net profit of $2.75M in Q2 2023, up drastically from a net loss of $0.91M over the same period last year. Since coffee demand has low elasticity , we believe that Dutch Bros’ price increases will have a minimal impact on its sales, which will allow the company to further improve its profitability without hindering revenue growth.

Improving Financials

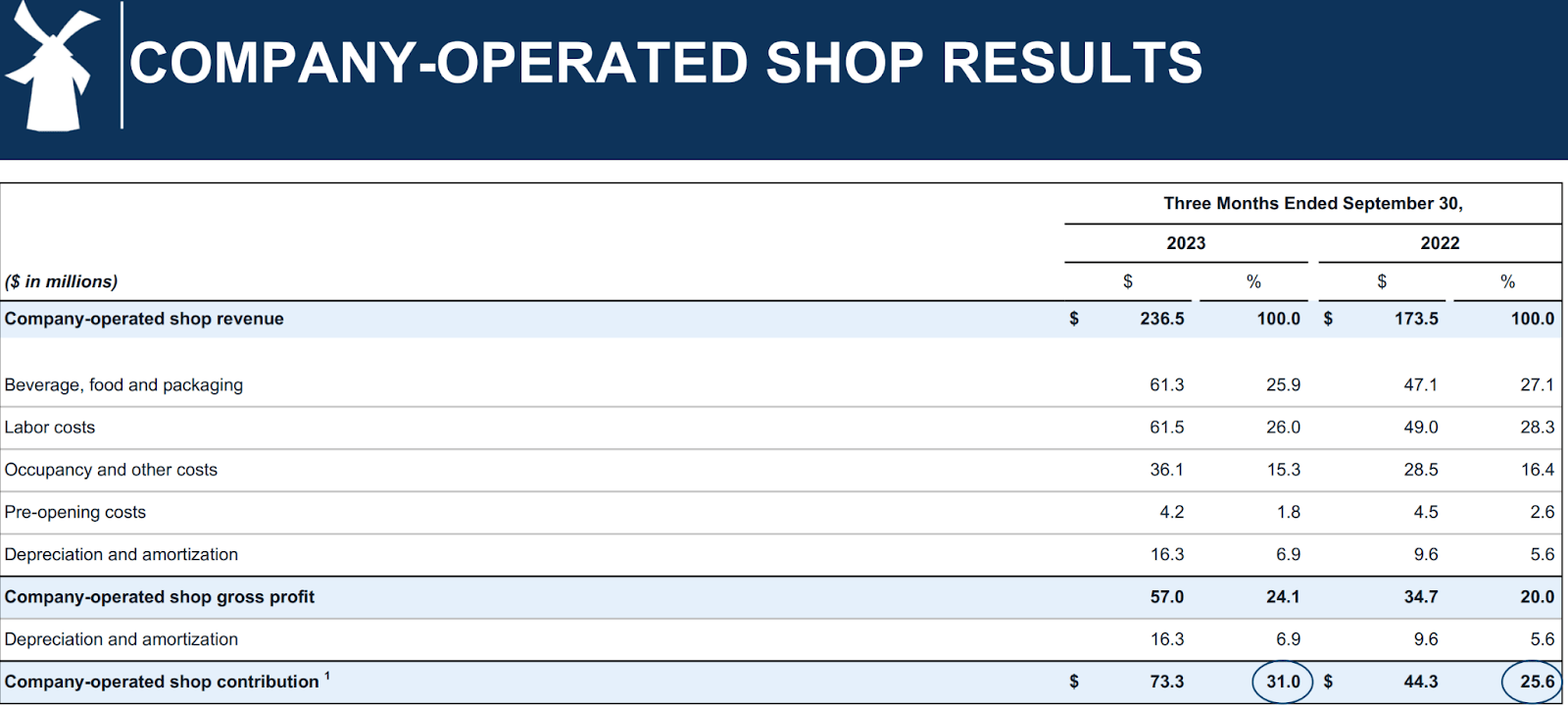

The company’s narrow margins has caused it to miss analysts’ expectations over the past year. However, Dutch Bros has been able to raise its prices at a faster pace than the rising cost of operating its business. Despite the cost of beverages, food, and packaging rising 25.9% YoY to $61.3M and labour costs rising 26% YoY to $61.5M in Q3 2023, the company’s revenue more than compensated for these costs by rising 33.15% YoY. As such, the company’s margins have improved substantially and the business is now far more profitable, as demonstrated by the total gross profit of Dutch Bro’s rising by 48% YoY 20 $75.2M in Q3.

{kind=link}

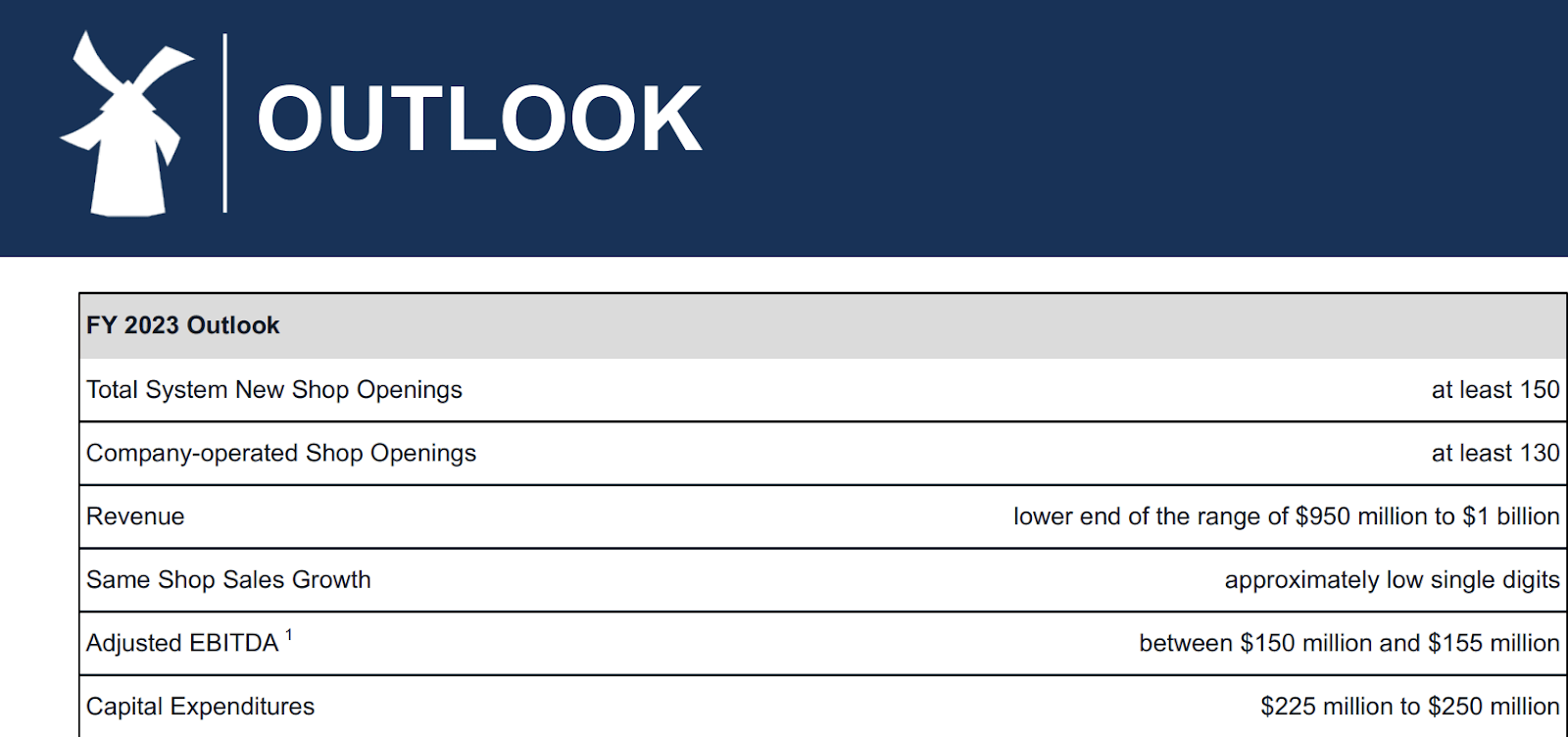

Due to increasing revenue, wider margins, and the opening of its new stores, Dutch Bros has significantly improved its outlook for FY 2023. Largely thanks to its new stores, the company’s revenue is forecasted to rise to between $950M and $1B for this fiscal year, which represents a substantial improvement from its revenue of $739.0M in FY 2022. Dutch Bros’ increasing revenue, alongside its improved margins, has made it such that the company is projected to achieve EBITDA of between $150M and $155M this year, demonstrating Dutch Bros’ rapid improvements in terms of profitability.

{kind=link}

We believe that Dutch Bros’ rapid revenue growth will be sustained by its rising number of stores, strong demand for its products, and the rising price of coffee. As such, it is likely that the company will be able to grow and maintain the profitability it has recently regained. Therefore, we believe that the company’s long-term outlook is fairly solid and that it will continue to enjoy rapid growth in the foreseeable future.

Valuation

Author

We used Graham’s Formula for Dutch Bros’ valuation. We assumed a 3Y forward EPS CAGR of 34.58% and a forward EPS of $0.18, which is based on Seeking Alpha’s earnings estimates . Even with this impressive growth, our model values Dutch Bros at just $6.43 per share, which implies a 77.28% downside from their current share price of $28.30. While earnings growth has been impressive over the past few years, we believe that their struggle with substantial profitability is still being reflected in this valuation model. For these reasons, we believe that Dutch Bros is overvalued at current prices.

New Store Risk

Since the Dutch Bros’ future growth and profitability are heavily reliant on the performance of its new stores, the company faces significant downsides if these new stores fail to be as profitable as the company hopes. The increases in average per-store revenue and comparable sales that the company has experienced may not be indicative of future results as these positive results have only been sustained for about two years. Although there is a serious risk for the company if the performance of its new stores turn out to be underwhelming, we believe that this risk will most likely have a low impact on the company since 35 of the 38 stores opened in Q2 have been profitable. As such, we believe that the company’s new stores will most likely be a net positive for the company, although the risk of these stores’ potential underperformance cannot be ignored.

Conclusion

Despite an underwhelming performance in FY 2022 and failure to meet analysts’ optimistic projections this year, Dutch Bros has been able to significantly improve its financial state by markedly increasing its revenue, improving its margins, and opening profitable new stores. As such, the company has been able to return to profitability and we believe it is likely to continue to grow over the next few years. Nevertheless, its lack of a substantial bottom-line has resulted in an extremely high valuation that cannot be justified. As such, we rate Dutch Bros stock a hold.

For further details see:

Dutch Bros: High Growth, High Price