BROS - Dutch Bros: High Growth Remains Possible

2023-12-17 08:02:37 ET

Summary

- Dutch Bros reported strong financial performance with revenue growth of over 30% and improved profitability.

- The company's growth outlook remains positive, and I believe it can achieve $1.5 billion in sales by FY25.

- Strategies to improve labor efficiency and the deployment of the Tap system and potential mobile ordering are expected to drive further growth and profitability.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy rating, as I believed Dutch Bros ( BROS ) could continue to grow at a very fast pace across the entire US. Especially when compared to bigger players like Starbucks ( SBUX ), the growth potential remained huge. I am reiterating my buy rating for BROS as the path for continuous high growth remains visible. Notably, the problem with the weak balance sheet is no longer a concern, which gives me confidence that BROS can continue to grow units as planned. A strategy to improve labor efficiency should also help to further improve sales growth potential.

Financials / Valuation

BROS reported another strong quarter , with revenue growing by more than 30% to $264.5 million. Notably, the strong growth was not at the expense of margin deterioration. Restaurant-level margin [RLM] improved to 32.8% from 28.2% in 3Q22, which drove profitability at the consolidated level up as well. Because of the small margin base in FY22, the strong revenue growth and improved RLM led to substantial operating leverage at the company level. At the consolidated level, the EBITDA margin improved by 11 percentage points to 16%. As a result, net income also saw significant growth, from $14 million to $22 million.

Based on author's own math

With the better-than-expected growth in 3Q23, I have an improved growth outlook for BROS (in line with consensus). I now expect BROS to achieve ~$1.5 billion in sales in FY25, driven by continued unit growth (which no longer faces a weak balance sheet hurdle) and same-store sales growth (driven by improving labor efficiency). I am not making any changes to my valuation multiple assumption as BROS continues to grow at a high rate, just as I expected. Hence, my view that it should continue to trade at a premium to other QSR peers (as defined previously: SBUX, Wendy’s, Shake Shack, and Sweetgreen) remains the same.

Comments

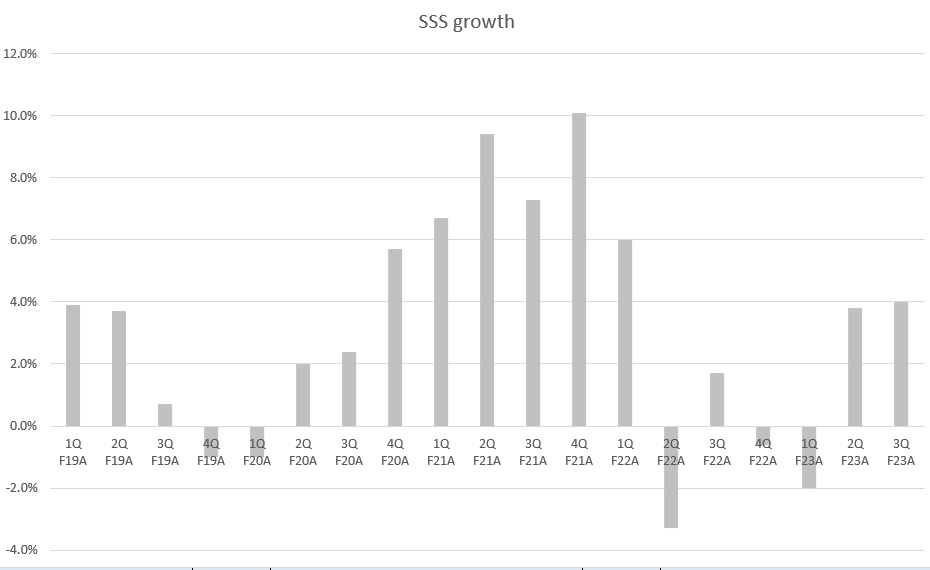

BROS 3Q23 performance showed great growth momentum that I expect to follow through in the coming quarters. Both growth drivers—same-store-sales [SSS] growth and unit growth pipeline—remain healthy with no signs of slowing down. For SSS growth, BROS should see an easier comp in 4Q23 given the weak 4Q22 quarter and as management continues their aggressive marketing strategy. As for unit growth, management has reiterated their expectation for more than 150 new stores in FY23, implying a 22% growth in FY23 units and 4Q23 to open another 27 stores. One of the key concerns with BROS was the weak balance (I discussed this previously), and this might impact the pace of unit growth if BROS runs into liquidity issues. That concern is now off the table as BROS has improved its balance sheet significantly with $150 million of cash, $350 million of undrawn revolvers, and $200 million of undrawn delayed draw term loans. Collectively, BROS has around $700 million of spare financial capacity. Using the last 12 months of FCF performance as the burn rate, this implies that BROS can last the next 5 years without the need to conduct capital raises via equity issuance. In fact, as profitability improves (as seen in the results), BROS could very well turn FCF positive over the next few years.

{kind=link}

With regards to profitability, I believe there is a visible path to improved margins as management continues to improve labor productivity and in-store operation efficiencies. Over the past year, BROS has restructured its labor strategy to be tied to the number of transactions (i.e., from labor hours/sales to labor hours/transaction). This makes more sense as volume (or traffic) is a better metric to understand how the store is performing, especially in the current inflationary environment where pricing is high. Also, this strategy enables BROS to better schedule labor to meet peak periods. Sales per hour will not accurately tell you how busy the store is, as pricing will distort the results. I believe the resulting impact is clear in the operating leverage.

BROS labor strategy ahead is to focus on hiring the right shop managers who are willing to pay more. While this will increase the wage expense in the near term, I believe this is a sensible move as how efficient the store is is ultimately dependent on the store operator, which is the manager. The shop manager is also a fulcrum in BROS growth plans, as the more units they open, the more competent shop managers they need. The long-term plan is to have more shop managers that are able to manage 7 shops instead of the current 3 to 4 shops. This is huge, as if effectively meant that BROS will need half the size of regional shop managers. The cost savings could then be reinvested in the business or shared with consumers.

Apart from labor productivity, I also expect to see positive results from the Tap system. BROS Tap system rollout is improving store efficiency at 16 of BROS stores currently, and I expect this management to roll this out to the entire cohort. The reason for the slow deployment was mainly due to logistics, as BROS needed to get permits before they could install it. Since this is a new system, I think there is a learning curve for BROS before it can quickly deploy to all other stores. I believe the deployment will get faster from here on. For reference, the long-term benefit is that this could save around 200 bps of cost, so it is huge.

At some point, I would also expect mobile ordering to be possible, which should drive massive improvements in store efficiency as it improves throughput. There will be less time spent taking and confirming orders, and the time saved could lead to a reduced number of staff or an increase in drink-making capacity. The latter translates to higher sales potential per store. There are sufficient precedents in the industry to show that mobile ordering is well received by consumers. For instance, SBUX launched mobile order and pay in 4Q15 and has grown it to ~29% of total transactions. Another benefit of mobile ordering is that it complements the BROS loyalty program strategy. It would increase the frequency of members opening the app, as they would need to look through the app and order. From there, BROS brand awareness should become more effective, as members are likely to pay more attention to promotions and other campaigns when they are in the app compared to a billboard ad, for instance. Essentially, the rollout of mobile ordering would improve store productivity and marketing dollar efficiency, both leading to an improvement in profit margins.

Risk & conclusion

The new labor strategy will target competent managers, which is a fundamental component of BROS's capacity to drive improvements in margin. Unit growth potential and RLM could be negatively affected if it doesn't work. Production and delivery delays, as well as declines in growth and profit margins, could result from problems with the coffee supply chain, flavoring syrups, milk, or other components and packaging.

To summarize, I am reiterating my buy rating for BROS as I see a visible path to sustained high growth. The concern over the weak balance sheet is now off the table, giving me confidence in BROS's ability to grow units. Strategies to improve labor productivity, including shifting to transaction-based labor metrics, also underpin profitability growth. Furthermore, enhancements like the Tap system deployment and future mobile ordering hold promise for improved store efficiency and increased sales potential.

For further details see:

Dutch Bros: High Growth Remains Possible