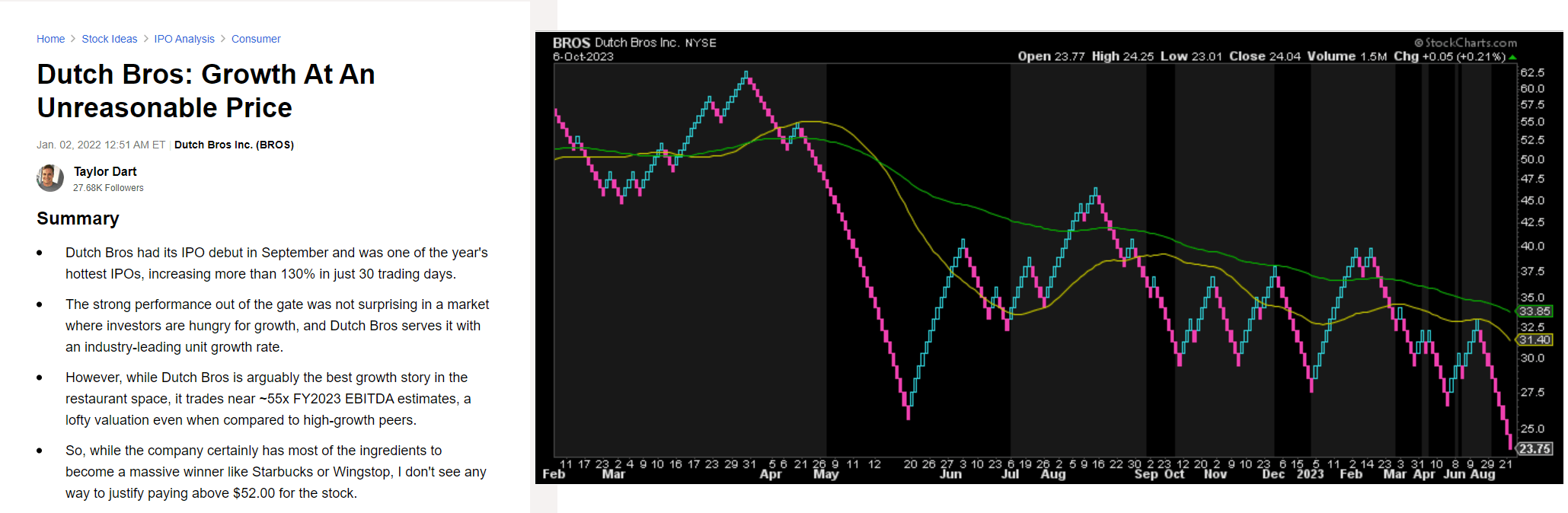

BROS - Dutch Bros: Still No Margin Of Safety

2023-10-09 05:23:11 ET

Summary

- Dutch Bros reported record revenue in Q2, driven by shop count growth and menu price increases, and got a bounce after a 60% plus decline post-IPO.

- However, BROS has since rolled over, industry traffic has plummeted & AUVs have come in below my expectations given the aggressive infill strategy, a negative combo with rising build costs.

- In this update, we'll look at industry-wide traffic trends, the stock's valuation after two years of massive underperformance vs. the QSR peer group & the stock's ideal buy zone.

Just over 12 months ago, I wrote on Dutch Bros ( BROS ) shortly after its IPO, noting that there was no way to justify chasing the stock above $52.00. This is because the stock was trading at over 55x two-year EBITDA, a figure that dwarfed the valuations of even some of the most successful restaurant concepts in their prime, like Chipotle ( CMG ) and Wingstop ( WING ). Since then, the stock has slid over 50% (not helping by its recent ~7% share dilution ), massively underperforming quick-service peers like Restaurant Brands International ( QSR ) and Wingstop which have enjoyed positive returns in the period. Unfortunately, while the stock is plumbing its IPO lows, it's still hard to make a case on valuation, and industry-wide traffic is not helping, with quick-service suffering one of its worst traffic declines in the past year in September. Let's take a look at Dutch Bros' recent results, industry-wide trends, and its valuation after its 50% haircut below:

Dutch Bros January 2022 Update, BROS Chart - Seeking Alpha PRO, StockCharts.com

{kind=link}

Recent Results

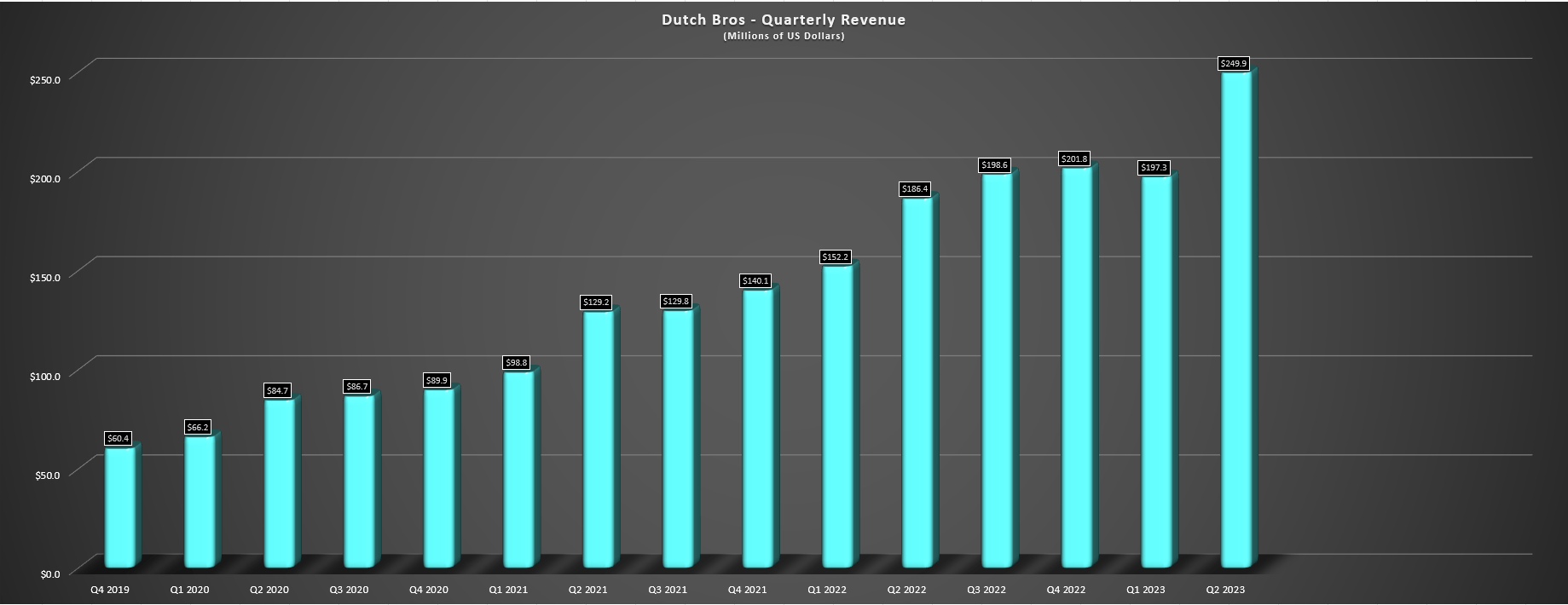

Dutch Bros released its Q2 results in August, reporting record revenue of $249.9 million, a 34% increase from the year-ago period. The strong performance was driven by 25% growth in its shop count to 754 stores at quarter-end (63% company-owned), and mid-single digit menu price increases in the period which helped to push same-shop sales back into positive territory. However, it's important to note that the company was lapping relatively easy comps with 3.3% same-shop sales in the year-ago period, with the 3.8% increase translating to below 1% two-year stacked same-shop sales on a system-wide basis, while company-operated same-shop sales were negative (two-year stack basis). This was below my estimates and given the heavy cash burn due to rapid unit growth and rising interest rates that contributed to ~$9.1 million in interest expense in Q2 (Q2 2022: $3.6 million), it's not overly surprising that the company elected to sell equity to pad its balance sheet with a $300 million offering at ~$26.00.

Dutch Bros - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

In addition, while the company noted in its FY2022 results that it did not intend to take additional menu pricing in 2023, it hasn't been able to follow through here, with the company choosing to raise menu prices again, with mid-single digit effective pricing in H2. This is below some of its restaurant peers, but in an environment where traffic pulled back sharply in Q3 on an industry-wide basis, the higher prices on an already pricy beverage could weigh on sentiment a little, especially with wallets getting due to rising gas prices. That said, menu pricing and some softening in commodity prices at least had a positive effect on profitability and margins, with food/beverage costs improving to 26.8% vs. 27.1% year-over-year, and labor down 280 basis points to 29.4%. The result was a 420 basis improvement in company shop gross profit to 23.6%, while adjusted EBITDA improved to $48.6 million helped by industry-leading unit growth, allowing the company to take up its guidance to "at least $140 million" on adjusted EBITDA vs. $125 million previously.

That said, revenue was guided for the lower end of the $950 million to $1.0 billion prior outlook, the company has stuck to guidance of low-single digit same-shop sales which implies traffic declines and heavy infilling in markets could continue to weigh on average unit volumes [AUVs] which haven't progressed nearly as well as I expected relative to IPO levels given the pricing actions taken. This isn't ideal when build costs are up significantly and while the company has made progress on driving traffic in Q2, the combination of higher build costs (higher capex), sticky/elevated labor costs, and choppy traffic industry-wide has created a difficult environment for meeting/beating estimates over the next few quarters.

So, while the company has certainly excelled when it comes to its expansion, on track for 800 shops at year-end and now has over 130 shops in Texas, placing this market next to its other big 2 markets (Oregon and California), other areas of the story have become less attractive since the stock's IPO debut, albeit largely out of Dutch Bros' control (weakening consumer, significantly higher construction costs, and higher rates that have significantly increased its interest expense). Let's dig into industry-wide trends below:

Industry-Wide Trends

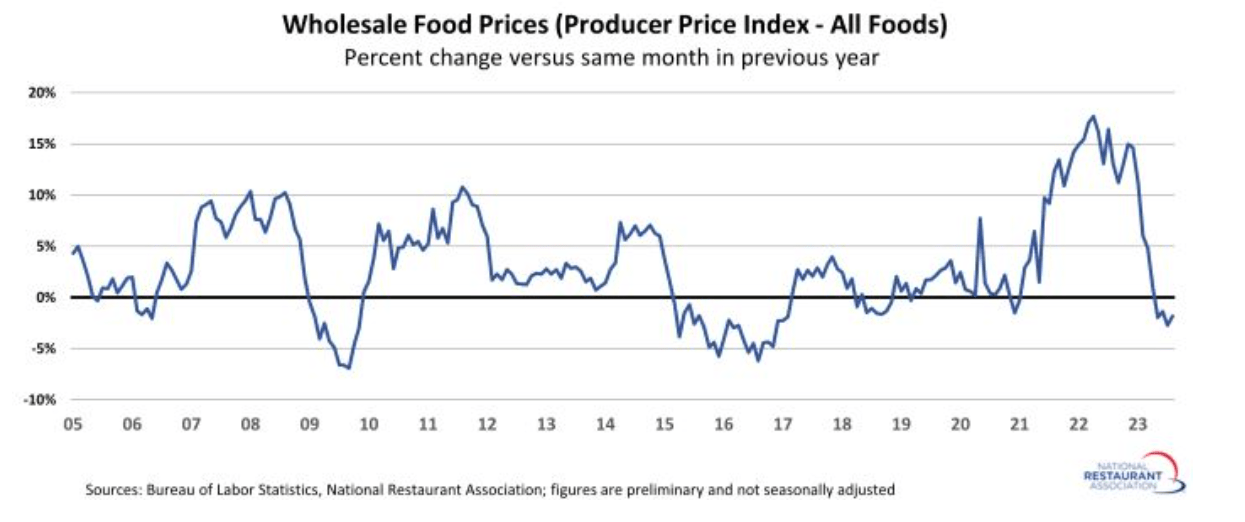

Starting with the positives, average wholesale food prices were down year-over-year in August, a positive departure from the double-digit commodity inflation that dented margins in H2 2022. However, while dairy has cooled off as has the commodity basket as a whole, to-go packaging, tea, coffee, and refined sugar remain elevated and were up 20.5%, 15.8%, 13.7%, and 13.3% in August, respectively. Meanwhile, labor isn't showing any real signs of pulling back, with minimum wage increases continuing across several states, investments needed in team members to maintain retention given other large brands continue to invest in wages to support their growth like Costco ( COST ) at $17.00/hour, and while it's nice to see some commodity deflation which is helping out the industry group as a whole on the bottom line, it's the top line where trouble could be brewing, with major operators like Darden ( DRI ) calling out some hints of check management, and it being a rough August and September for industry-wide traffic.

Wholesale Food Prices - National Restaurant Association, BLS

{kind=link}

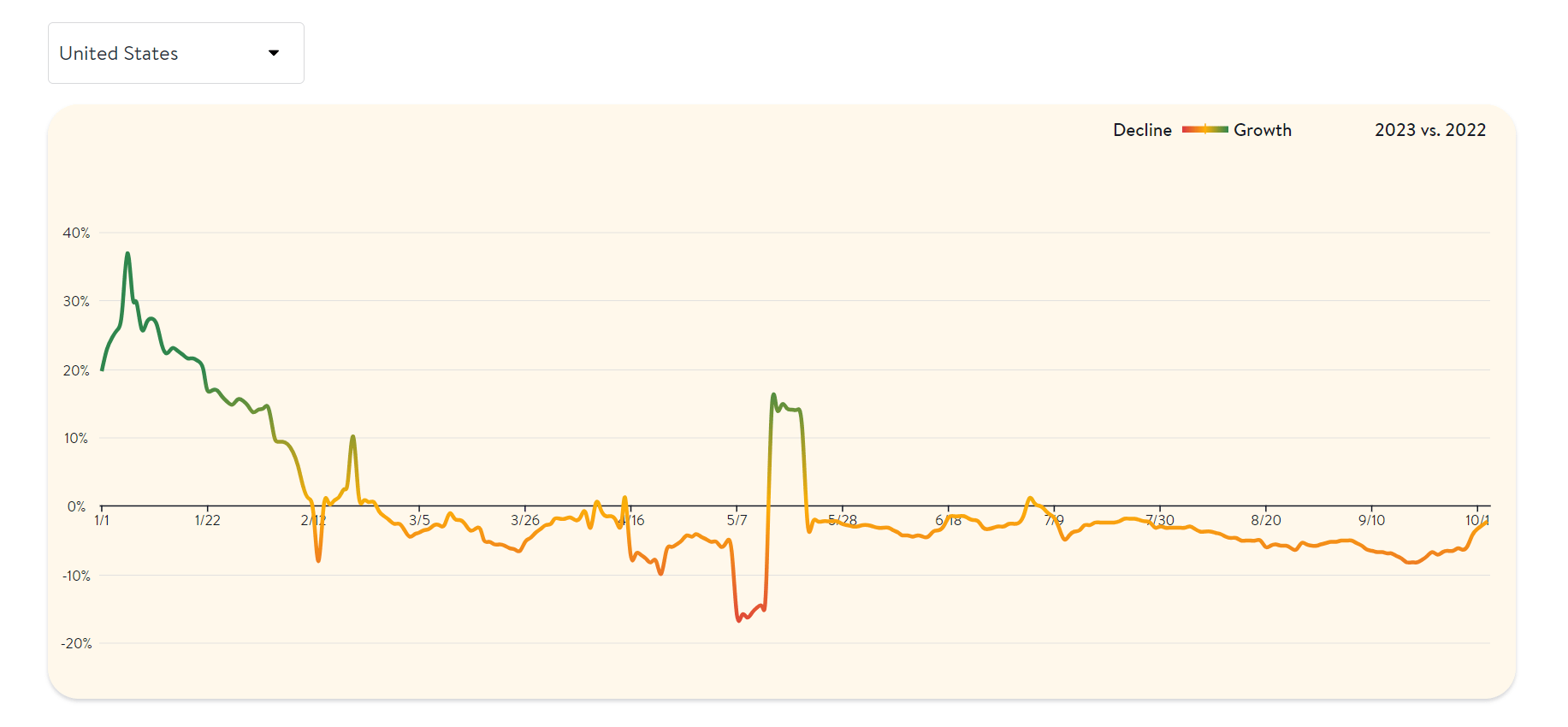

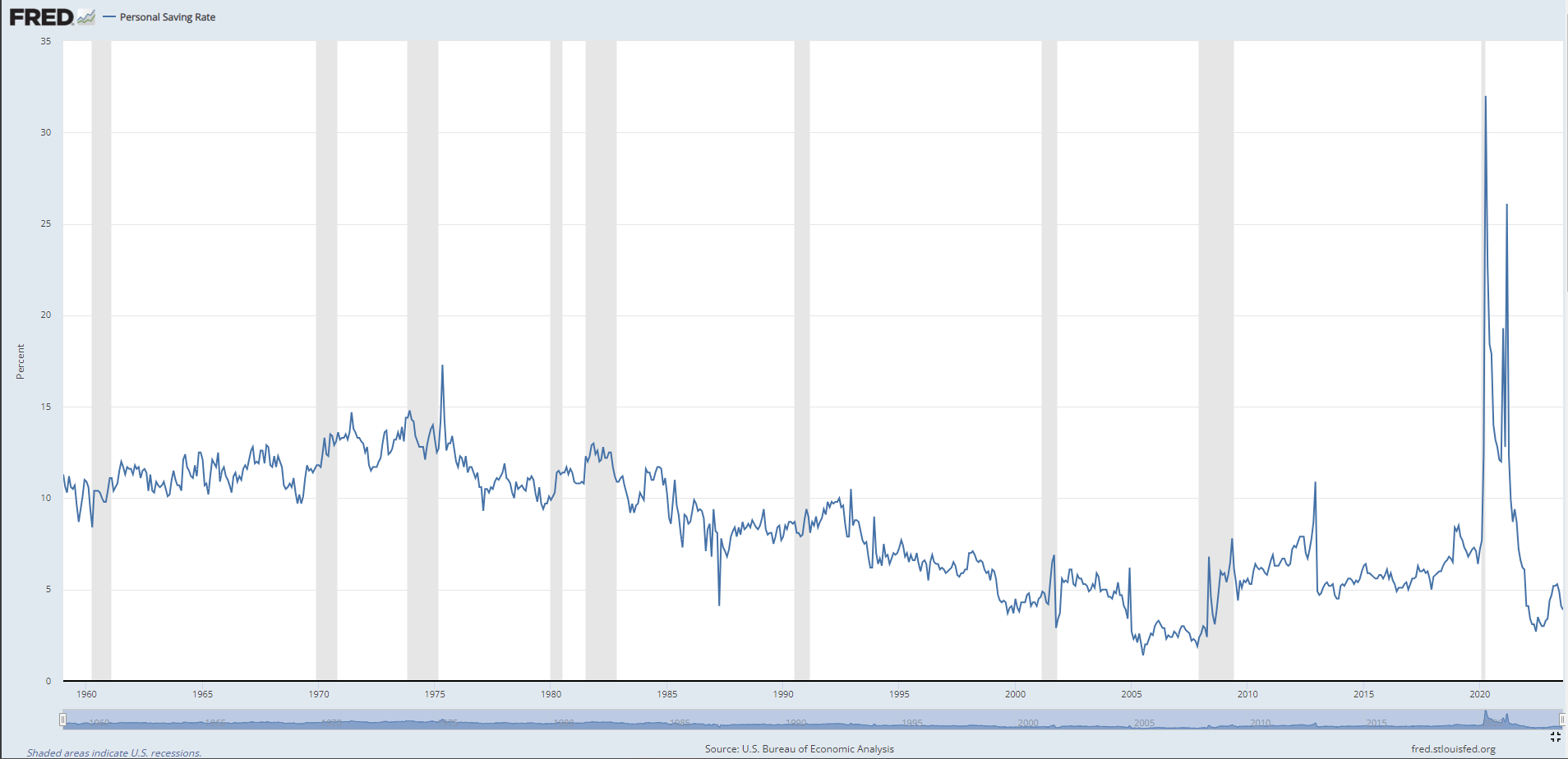

In fact, as shown below, seated diners in the United States according to OpenTable have continued to trend lower since late July, decelerating throughout Q3 and turning lower once again to start Q4 after a brief recovery in late September. This may not be reflective of Dutch Bros' traffic given that these are seated diners and more relevant to the casual dining category, but this pullback in traffic is not contained to casual dining. In fact, quick-service just came off its worst month of the year, with traffic down over 4% and it's been steadily declining since its double-digit traffic percentage gain in January off of easy Omicron comps vs. January 2022. So, while the declining traffic may not be as significant for quick-service as it is in casual dining, the trends look to be quite similar, with this trend being more judicious consumers when it comes to spending. And with personal savings rates plunging, rising gas prices and grocery, utilities, and mortgage/rent costs up, this inevitable pullback is not surprising.

{kind=link}

On a positive note, Dutch Bros benefits from being a commodity that is quite addictive, and even if the Ozempic fears are true, it's an occasion that isn't likely to suffer nearly as much. That said, the company's higher-priced drinks are arguably somewhat of a trade-up vs. much cheaper alternatives elsewhere, with the ability to get a caffeine fix at lower prices with Red Bull, Celsius ( CELH ), and Monster ( MNST ). And while its coffee offerings are undoubtedly premium, it's possible that tighter wallets could lead to some trading down or one less occasion per month, with there being much cheaper alternatives out there like Tim Hortons and Dunkin Donuts, not to mention the increasing competition in the space, with shops like The Human Bean that continues to expand outside of Oregon. So, while I don't think Dutch Bros is in as much trouble from a traffic standpoint as other higher average check casual dining brands, it's tough to be optimistic about a beat on the Q3 and Q4 results given the industry-wide traffic trends and the semi-tapped out average consumer.

Personal Saving Rate - FRED, BLS

{kind=link}

Valuation

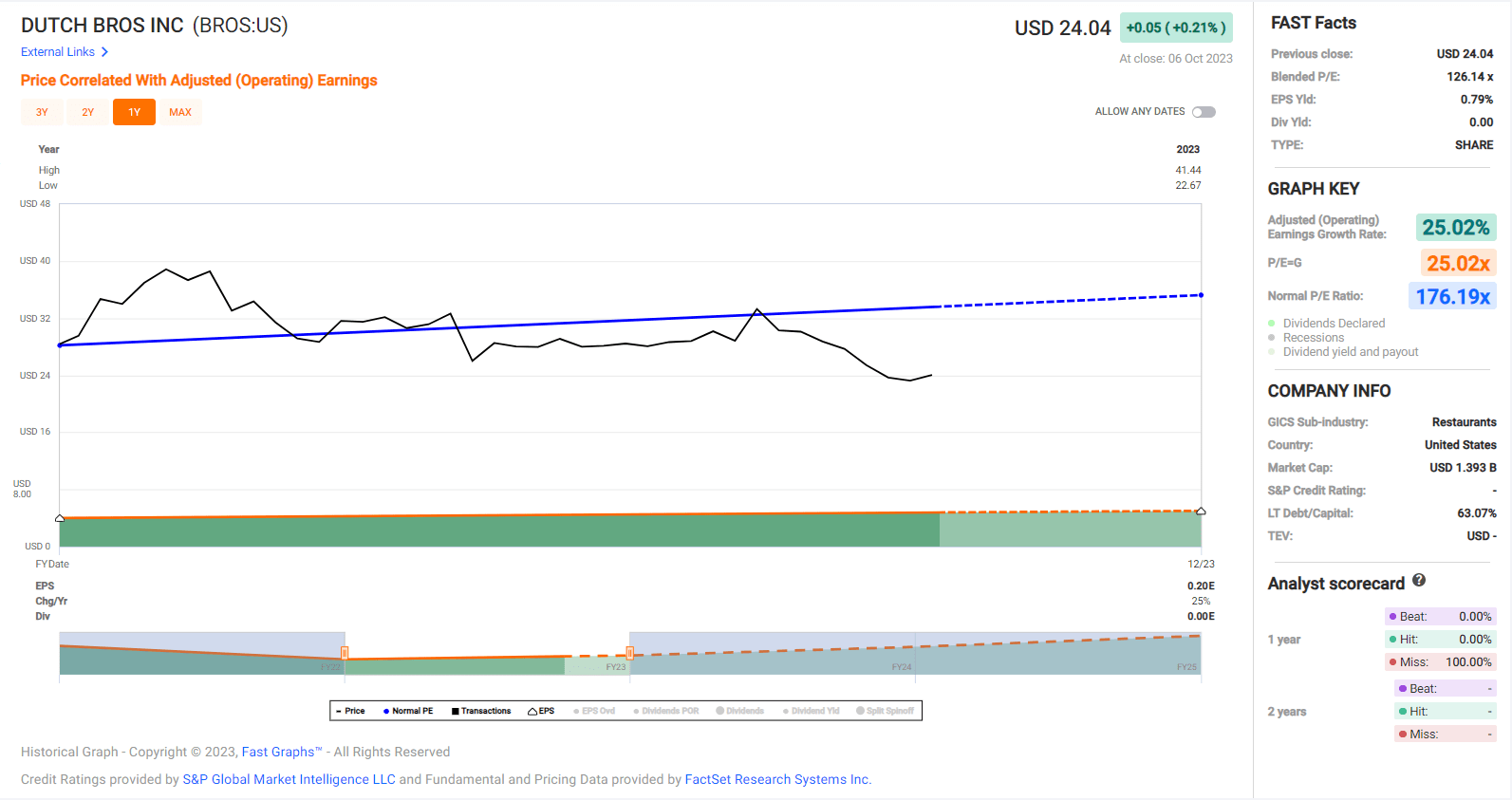

Based on ~178 million shares and a share price of $24.20, Dutch Bros trades at a market cap of ~$4.31 billion and an enterprise value of ~$4.65 billion, leaving it towering over several other restaurant brands from a capitalization standpoint. From a valuation standpoint, this leaves the stock still trading at a relatively high EV/EBITDA multiple of ~33.0x using FY2023 estimates, a figure that is double that of mature brands generating significant amounts of free cash flow like Restaurant Brands International, and nearly triple that of First Watch ( FWRG ), which is also growing its units rapidly and one of the more iconic up and comers in the casual dining space. In my view, this is still not cheap enough even if Dutch Bros is on a path to become a future behemoth in the QSR category, and this is especially true in an environment where the market is not paying up for future growth like it was in a low to zero interest rate environment shortly after Dutch Bros' IPO debut.

Dutch Bros - Earnings Multiple - FASTGraphs.com

{kind=link}

Using what I believe to be a more conservative multiple of 24.0x EV/EBITDA (FY2024 estimates) given that this is a differentiated and high-growth concept with the ingredients to become a long-term share gainer in the space (but offsetting for the higher-rate environment), I see a fair value for the stock of $23.00. This suggests that the stock is still fully valued using this more conservative multiple, and I prefer to buy at a minimum 20% discount to fair value when it comes to mid-cap growth stories to ensure a margin of safety ( implying a low-risk buy zone of $18.40 or lower ). So, although BROS could get a relief bounce after what's been a violent two-month correction (34% in 35 trading days), I continue to see far more attractive bets elsewhere in the market and would only start to get interested if BROS were to undercut its IPO lows at $20.05 at a bare minimum.

Dutch Bros Menu - Company Website

{kind=link}

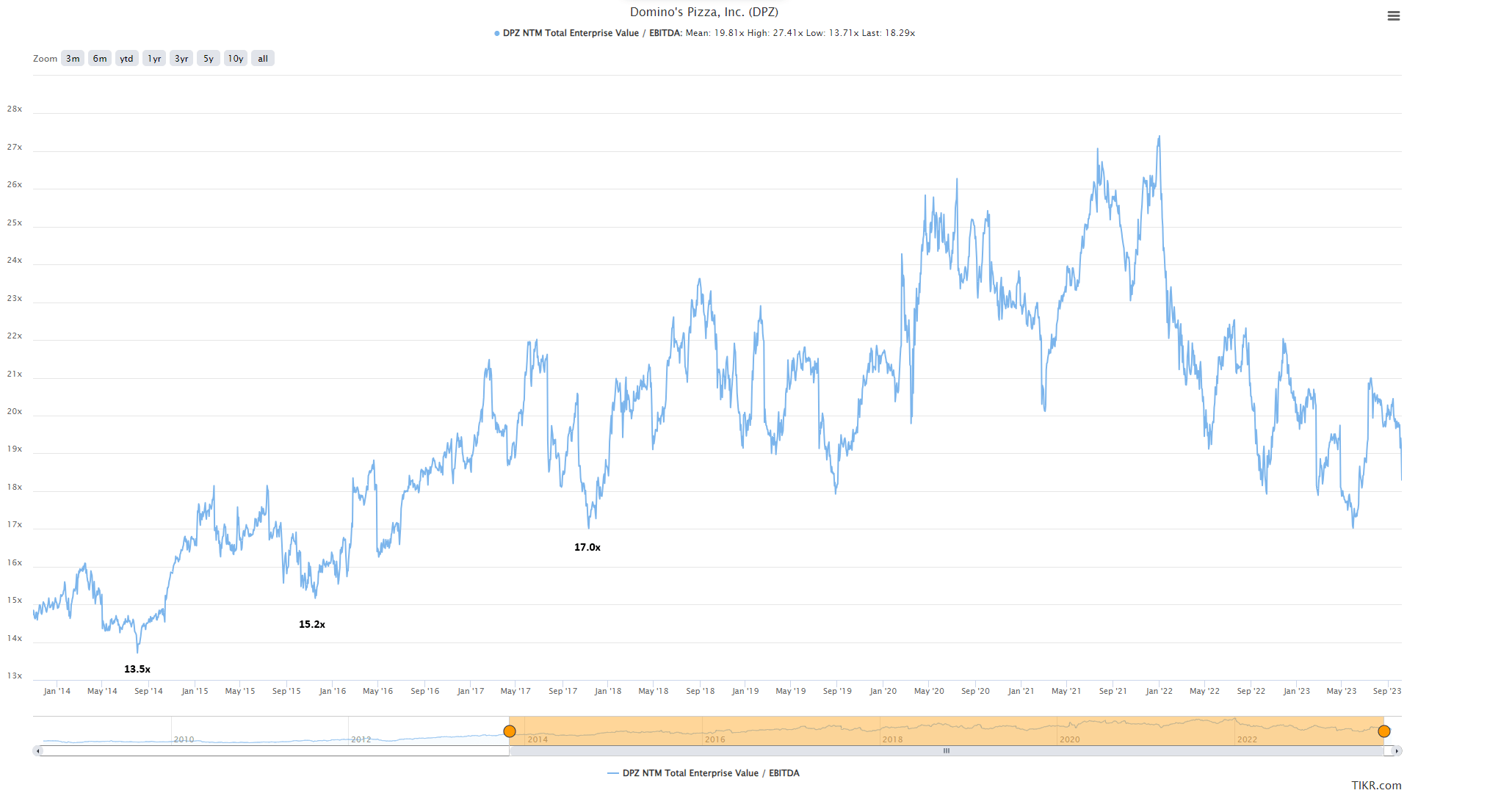

Obviously, I could be wrong here, and it's possible the stock will continue to command a rich valuation as it has over the past two years. However, in a market where one can find growth at much more attractive valuations in other sectors with similarly iconic brands, I don't see any reason to overpay for BROS. Plus, while the stock may be detested by some investors who have hung onto overpriced shares, I think there are more hated stories elsewhere in the market, and I prefer to buy on extreme pessimism when stocks are being given away or passed entirely. And as the chart above shows, patient investors were able to scoop up exceptional businesses like Domino's ( DPZ ) at very reasonable valuations if they were patient and during environments with a less aggressive Federal Reserve, suggesting that it's hard to rule out BROS trading at below 20.0x EV/EBITDA under a higher for longer scenario.

DPZ Historical EV/EBITDA Multiple - TIKR.com

{kind=link}

Summary

Dutch Bros may be one of the more iconic brands to have its IPO debut in the Retail Sector ( XRT ) over the past decade, in addition to names like Five Below ( FIVE ), Boot Barn ( BOOT ), Wingstop ( WING ), and Portillo's ( PTLO ). However, if there's anything investors can learn, it's that there's no investing without valuation even if these are great growth stories, with FIVE and BOOT suffering 50%+ corrections despite debuting in weaker market environments where they didn't trade up to insane valuations like ~8.0x sales at BROS' peak. And as stated by Joel Greenblatt, "there's no investing without valuation" . So, although it may be tempting to buy the dip on BROS and there could be a nice snapback rally, I would ultimately expect to see the stock re-test or undercut its IPO low at $20.00 before bottoming out for good. For this reason, and given that there are more attractive bets elsewhere in the market at double-digit free cash flow yields, I continue to focus elsewhere for the time being.

For further details see:

Dutch Bros: Still No Margin Of Safety