VLU - DVAL: Now An ETF This Top Performing Large Cap Value Fund Has My Attention

2023-04-18 05:43:22 ET

Summary

- DVAL is an actively-managed U.S. large-cap value fund that recently reorganized to an ETF from a mutual fund. Its expense ratio is 0.49% and DVAL has $160 million in assets.

- The strategy relies on a quantitative model to switch between deep value and broad value regimes as market conditions change. Changes typically occur between 2-7 years, but aren't scheduled.

- Using performance data from its predecessors, DVAL ranks near the top of my sample of 32 large-cap value ETFs over the last ten years. Risk is kept in check, too.

- DVAL won't always get it right, as its long-standing fund managers openly caution. However, if investors take a mid-to-long-term approach, I think they'll be rewarded.

- Normally I don't recommend high-fee funds, but DVAL has an exceptional track record and equally-impressive fundamentals that can complement passive ETFs like VTV. It's a buy.

Investment Thesis

Based on its measly 16 followers on Seeking Alpha, The BrandywineGLOBAL Dynamic U.S. Large Cap Value ETF ( DVAL ) is not a fund I expect readers to recognize. However, that's because DVAL reorganized into an ETF just last year. Formerly an open-ended mutual fund and a private fund before that, DVAL's model that rotates between broad and deep-value large-cap stocks is tried and tested. DVAL gained 179% over the last decade, second-best in my peer group, so it's clear its active managers have done something right.

This article evaluates DVAL's 1-10Y returns against well-known passive alternatives like the Vanguard Value ETF ( VTV ) and the Vanguard Russell 1000 Value ETF ( VONV ), DVAL's primary benchmark. This article also evaluates its fundamentals alongside these ETFs, ultimately selling me on the strategy and why I've rated DVAL as a "buy". While other value ETFs achieve a low valuation by sacrificing quality or accepting excessive risk, DVAL keeps both in check. Furthermore, managers target a much different market segment than these low-cost passive funds, making it an excellent complement for those wanting the benefits of active management. In short, I like what I've learned, and I look forward to taking you through my findings in more detail below.

DVAL Overview

Strategy Discussion

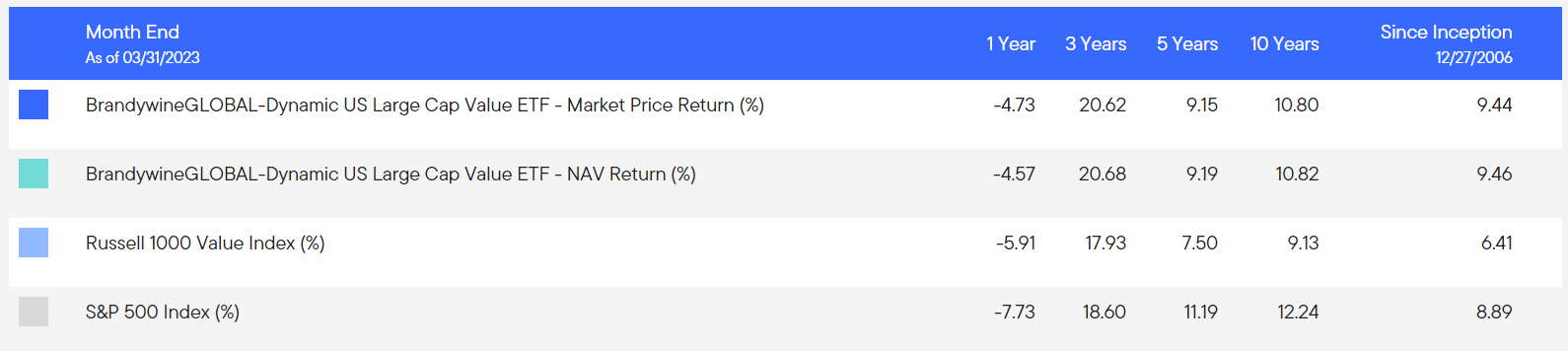

DVAL is an actively-managed ETF led by Brandywine Global, an independent investment manager of Franklin Templeton. DVAL reorganized into an ETF effective after the close of business on October 28, 2022. As such, "official" performance data on most websites, including Seeking Alpha, is limited. However, DVAL was permitted to retain the returns for its predecessor funds. DVAL operated as an open-ended mutual fund from October 2014 until October 2022 and a private fund since its inception in December 2006. As shown below, DVAL easily beat its primary and secondary benchmarks, the Russell 1000 Value Index and the S&P 500 Index.

{kind=link}

The outperformance is impressive considering DVAL's 0.49% net expense ratio (0.65% for its predecessors). Returns were less impressive over the last decade, but I still think the strategy is worth exploring further.

The same three portfolio managers have managed DVAL since its inception: Henry Otto, Steven Tonkovich, and Michael Fleisher. They form part of the Diversified Equity Team, comprising six portfolio managers and three analysts with an average of 25+ years of experience. Remarkably, only two members have departed the team since 1988. This low turnover rate is an essential feature described in the "Meet Your Manager" video on DVAL's fund page. In the video, Mr. Fleisher provides insight into the team's overall strategy, as does the fund's latest annual report . I've listed three takeaways below.

1. The team seeks to exploit behavioral biases and prefers simple models focused on a handful of quality, value, and sentiment-related factors.

2. Models are tested over 50-60 years of market cycles. DVAL's model was tested over at least 40 years and aims to outperform its primary benchmark over most three and five-year periods.

3. The model adapts to changing market conditions, alternating between broad and deep value portfolios. Managers expect the model to shift every two to seven years, typically driven by valuation spread changes.

I recently reviewed the Invesco Russell 1000 Dynamic Multifactor ETF ( OMFL ) and expressed some reservations. Despite an excellent track record, its model is between the business cycle's slowdown and expansion phases, resulting in two completely different portfolios and an excessive turnover rate. This is not a concern with DVAL. Instead, the Diversified Equity Team operates with high conviction, and it is reassuring that the team's general market outlook will remain for at least two years.

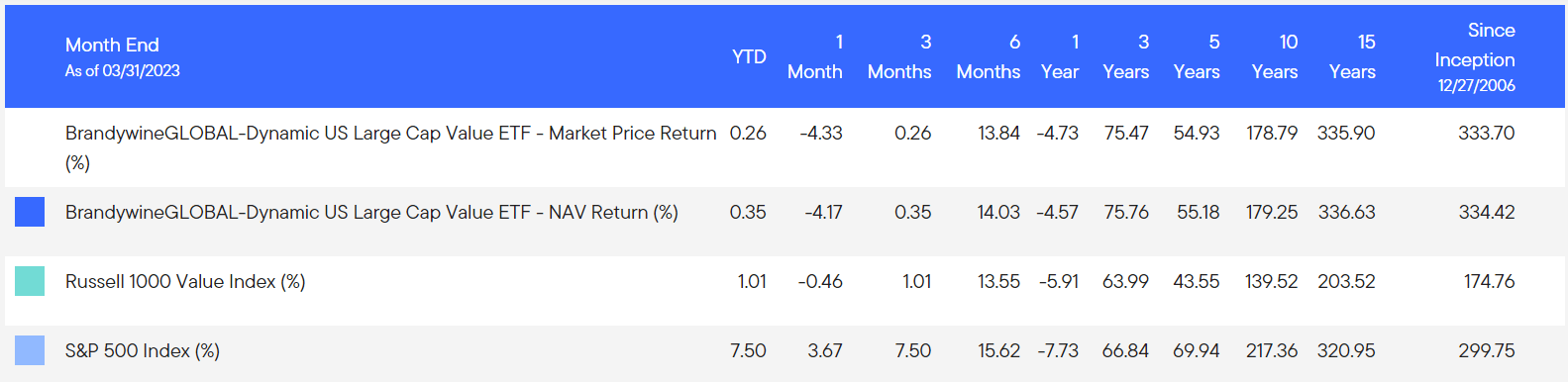

The aim to outperform over most three- and five-year periods is crucial. Since it's not a new fund and we have actual, non-backtested data available, we should avoid praising or criticizing DVAL for performance over a short period and instead consider any outliers that make the fund seem more "normal ."For example, DVAL outperformed the Vanguard Russell 1000 Value ETF ( VONV ) by 14% in 2023, which won't be counted in ten-year return comparisons next year. On the other hand, performance was closer to average over the last few years. Let's take a closer look at these historical returns next.

Performance Analysis

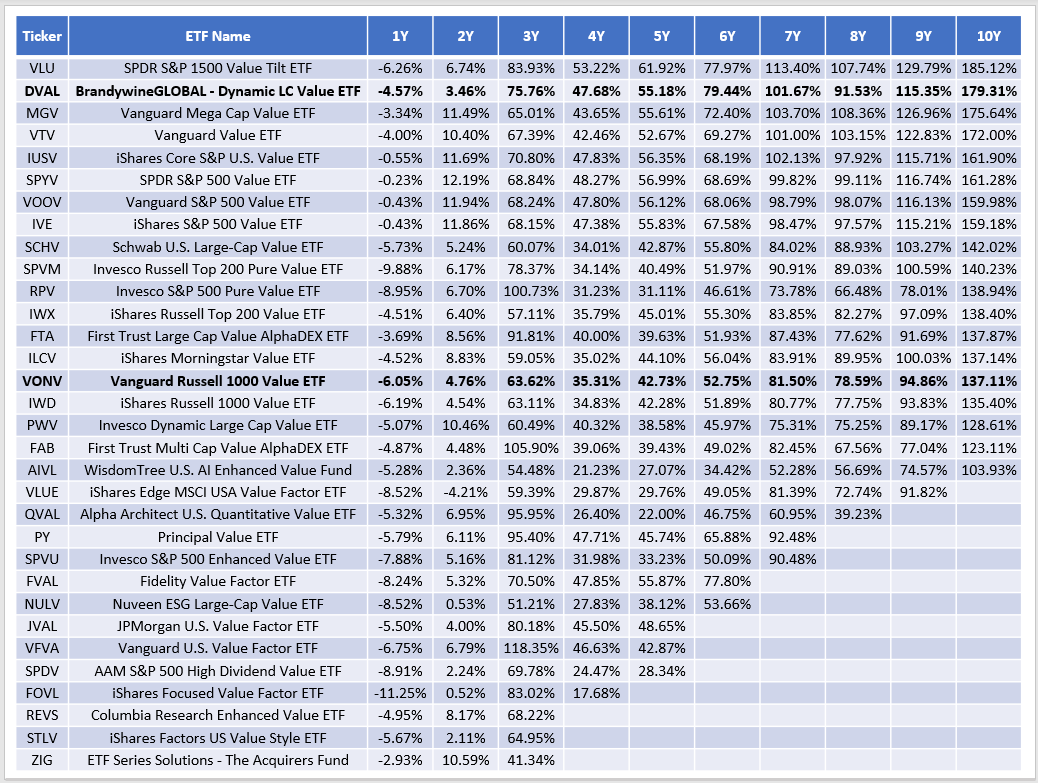

The first point I want to make is that VONV is not a top-performing large-cap value ETF. That's not to say it's an inappropriate benchmark for DVAL, but investors have choices. I've listed 32 in the table below, narrowed down from 43 in my ETF database. The only requirement was that each has either a Large or Total Market Value Focus/Niche, according to FactSet, and three years of performance history through March 2023. Note that this list doesn't include funds recently reorganized into ETFs like the Dimensional US Marketwide Value ETF ( DFUV ) or many dividend-focused funds like the Vanguard Dividend Appreciation ETF ( VIG ).

{kind=link}

DVAL's 179.31% ten-year total return is slightly off from the website's 179.25% figure due to rounding. I had to extract monthly returns manually using the "growth of 10K" charting tool on DVAL's website, as I couldn't find reliable monthly returns even on reputable sites like Morningstar.

{kind=link}

Only the SPDR S&P 1500 Value Tilt ETF ( VLU ) has a better ten-year track record, delivering a 185.12% ten-year return. Even Vanguard's MGV and VTV, two funds I like, fell short by 4-7%. You'll notice that many "pure" or "enhanced" value ETFs, like SPVM , RPV , and SPVU , lagged over the long run and are typically expensive to own. However, they might substantially outperform sometimes, and recognizing that in advance is why DVAL can potentially succeed.

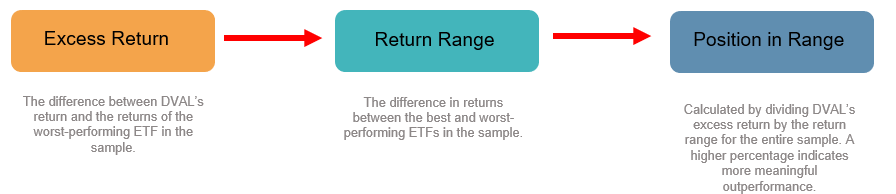

The following section ranks DVAL's performance against these peers in two ways. The first is a simple rank from best to worst for each period listed. The second measures the position in range for each set of returns. For example, a #2 ranking is less impressive if five other funds performed almost identically. The calculation is explained in the graphic below.

{kind=link}

- 1Y: #11/32 (60.62%)

- 2Y: #26/32 (46.67%)

- 3Y: #12/32 (44.70%)

- 4Y: #7/29 (84.41%)

- 5Y: #8/28 (83.12%)

- 6Y: #1/25 (100.00%)

- 7Y: #4/23 (80.81%)

- 8Y: #8/21 (75.65%)

- 9Y: #7/20 (73.85%)

- 10Y: #2/19 (92.84%)

Although DVAL was close to average over the last three years, its five-year 55.18% gain ranked #8/28 and is only 6.74% behind VLU, the top performer in the sample. These results paint a positive picture overall. If you take a five-year time horizon as the DVAL's managers suggested, you're likely to come out ahead.

Lastly, I want to touch on risk-adjusted returns. In the video mentioned earlier, Mr. Fleisher differentiates his team's strategy with the following quote:

Where others only see risk, we often unearth potential.

The statement is interesting because most value investors view risk negatively. However, rational investors are only concerned with downside risk, as volatility to the upside is not problematic. To add some color, I evaluated DVAL's rolling quarterly returns since inception with VTV and found the following:

- DVAL's annualized standard deviation is 16.65% vs. VTV's 16.01%

- DVAL had 133/193 positive rolling quarterly returns vs. 132/193 for VTV

- DVAL's averaged a 6.91% loss in down quarters vs. 6.69% for VTV

- DVAL averaged a 6.79% gain in up quarters vs. 6.22% for VTV

DVAL doesn't appear much riskier than a standard passive value fund. Its range of returns is slightly wider, but that should be beneficial in upward-moving markets. Even if the market moves downward, I doubt DVAL will substantially underperform.

DVAL Analysis

Sector Exposures and Top Ten Holdings

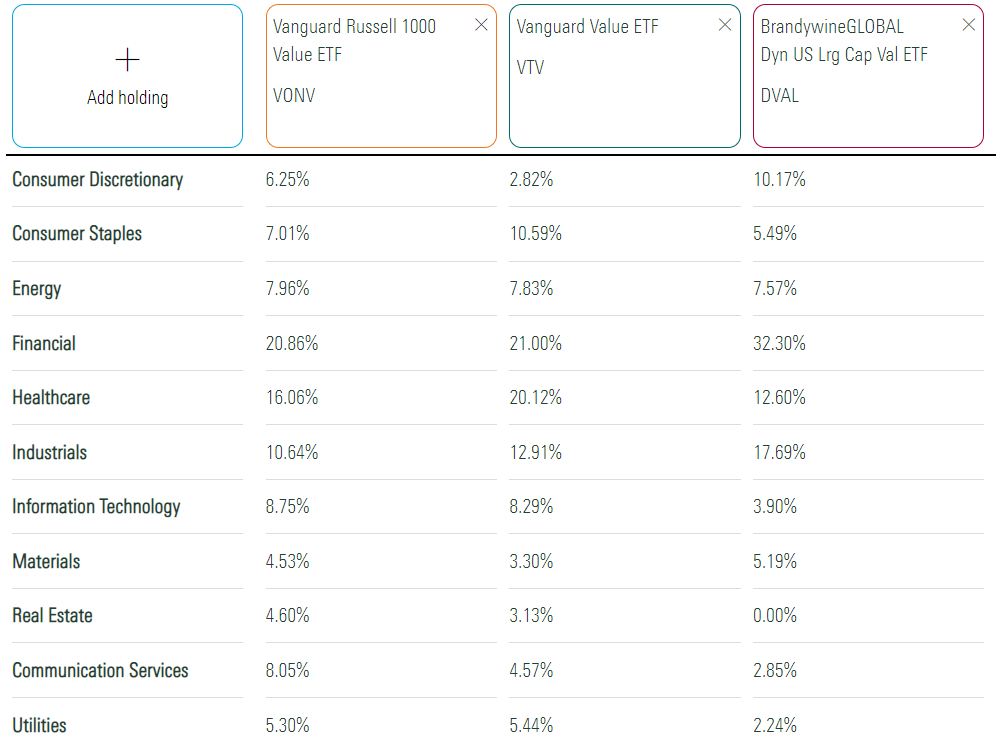

To my knowledge, DVAL's managers don't announce what strategy its model is following (broad or deep value). However, the annual report mentioned how the model shifted to broad value in July 2022. Given the estimated two-year minimum and how current sector exposures are similar to those in December 2022, I assume the broad value strategy remains. That might surprise some investors, given how DVAL is 1/3 Financials.

{kind=link}

Approximately 17% of the Financials sector exposure is in insurance stocks. Coincidentally, I just reviewed the SPDR S&P Insurance ETF ( KIE ) and concluded that the larger insurers are the better choice now. It's not mentioned in the fund documents, but managers evidently favor large-cap companies, which is appropriate in this case. The portfolio holds 17 insurance stocks, but only four (1.75%) have market capitalizations below $10 billion. Instead, Chubb ( CB ), Aflac ( AFL ), and Travelers ( TRV ) are most prominent with market capitalizations between $40 and $80 billion.

DVAL also has 10%+ exposure to Consumer Discretionary, Health Care, and Industrial stocks. Notably, it has only 4% exposure to Technology, mainly KLA ( KLAC ) and Cisco Systems ( CSCO ). It's also relatively light on Utilities, often used to drive down a portfolio's volatility.

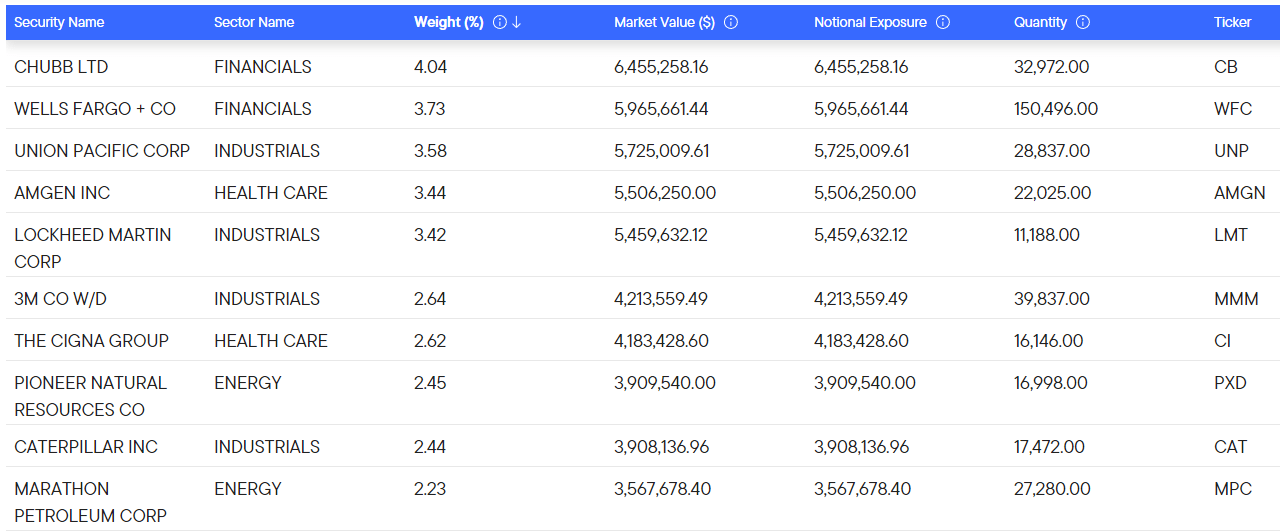

DVAL's top ten holdings are below, totaling 30.59%. There are 118 holdings, so it's more concentrated than VONV and MGV. I mentioned the preference for large-cap companies, and this list illustrates it well. Many constituents have market capitalizations above $100 billion, and while 46 have market capitalizations below $10 billion, they account for just 13% of the portfolio.

{kind=link}

DVAL Fundamentals By Company

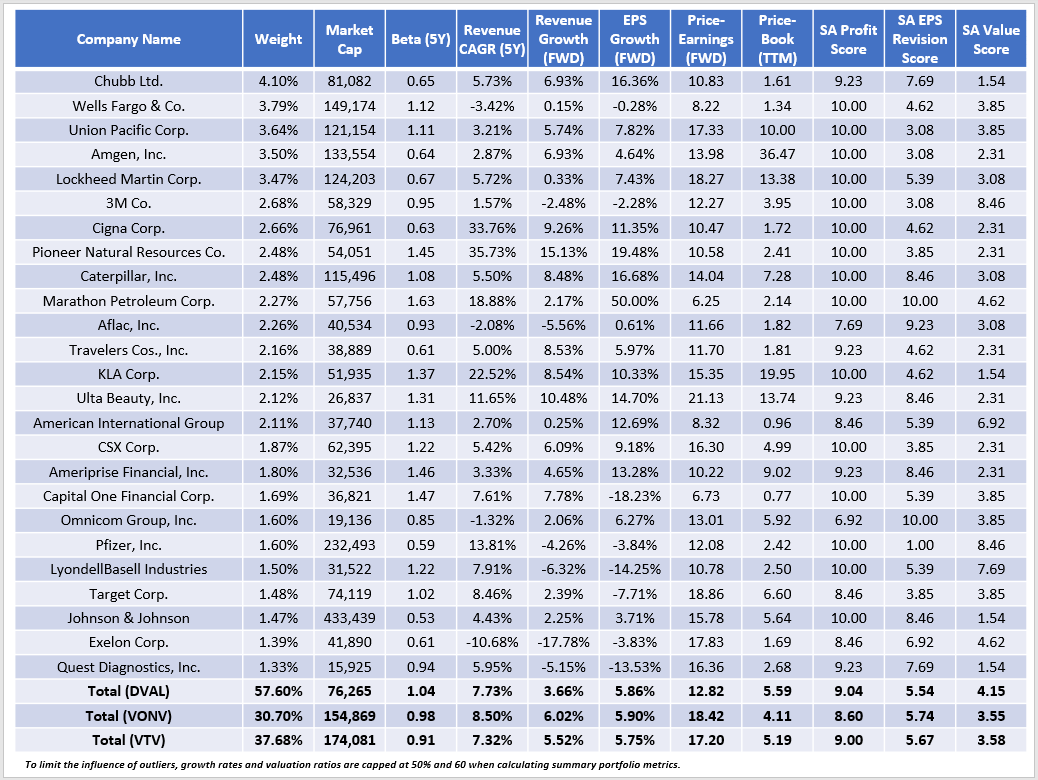

The following table highlights selected fundamental metrics for DVAL's top 25 holdings. This view covers 58% of the portfolio, and I've included summary metrics for DVAL, VONV, and VTV in the last rows.

{kind=link}

DVAL's five-year beta is 1.04, indicating higher volatility than VONV and VTV. I already discussed earlier how it's not burdensome. Still, VTV might be a better solution for those aiming to reduce risk because of its lower standard deviation than VONV. In addition, VTV's ten-year return-to-risk ratio (annualized returns divided by annualized standard deviation) is superior to DVAL's (0.73 vs. 0.66). We see similar results over three and five-year periods.

DVAL trades at 12.82x forward earnings, 5-6 points less than VONV and VTV. Much of this is due to high exposure to Financials stocks, which tend to have lower valuations. However, DVAL also has a 4.15/10 Value Score, calculated using individual Seeking Alpha Factor Grades that measure stocks against their sector peers. This score, while not great, easily beats VONV and VTV. Its 5.86% estimated earnings growth rate is on par, even if estimated sales growth is weak. That's one risk to the fund. If high-growth stocks, particularly those in the Technology and Energy sectors, lead markets, DVAL isn't in a great position, and its strategy will likely stay the same for a while.

Finally, I initially considered DVAL a possible substitute for a low-cost value fund like VTV. However, I now view them as complements, and the reason is quality. DVAL has a 9.04/10 profitability score, about the same as VTV, so you might think it holds no advantage. However, what's unique is that DVAL targets a much different value segment, evidenced by its smaller weighted average market capitalization ($76 billion vs. $174 billion). Market capitalization and profitability are highly correlated, so it's nice to see DVAL buck this trend.

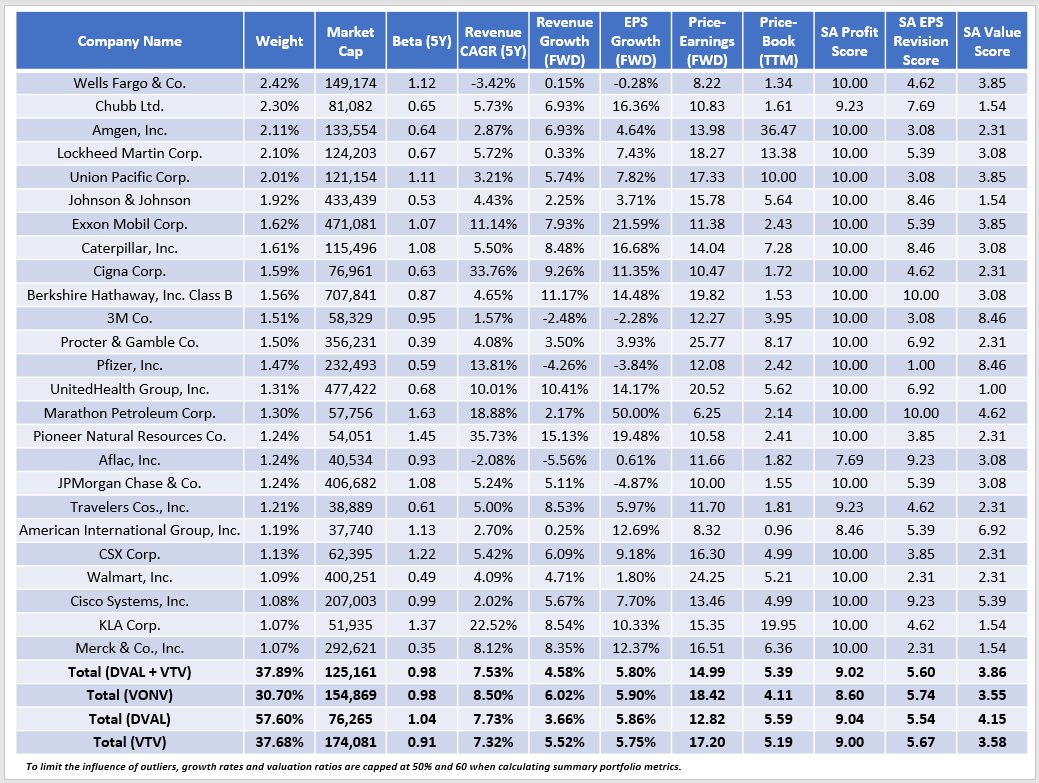

To further illustrate, VTV has only an 11.68% overlap with DVAL's top 25 holdings listed above (57.80% of the portfolio). On the opposite side, DVAL has only a 12.53% overlap with VTV's top 25 holdings. Combining the two in equal weight yields the following portfolio:

{kind=link}

This combined portfolio adds traditional value names like Berkshire Hathaway ( BRK.B ) and UnitedHealth Group ( UNH ), plus increases exposure to Energy giants Exxon Mobil (XOM) and Chevron ( CVX ). In the latest annual report, DVAL's managers cited a lack of exposure to this sector as a key reason for underperformance. This simple two-fund solution could be the answer for investors wanting to experience the benefits of active management but are nervous about essentially ignoring this critical sector.

Investment Recommendation

After evaluating DVAL's track record and current portfolio fundamentals, I believe it's a worthy large-cap value fund. The 0.49% expense ratio doesn't bother me if managers deliver on performance, and DVAL's Diversified Equity Team has done that for over 16 years. To be sure, DVAL's ten-year returns will look less impressive next year when 2013 returns rollover. However, don't let that detract you. At best, another one of these years will happen again. At worst, you'll get a return similar to a traditional large-cap value ETF like VONV. Based on my analysis of historical monthly returns, DVAL managers are unlikely to take on excessive risk to boost returns. They're part of a small, disciplined team with a reputation to protect that dates back 35 years.

My primary purpose on Seeking Alpha is to evaluate ETFs. I've studied the most popular strategies and formed my opinion about what works over the long run, especially with value-focused funds. In my view, DVAL is not a game changer but rather an arrow in your quiver. VTV and MGV are sufficient for passive investors, and I like how they are less volatile and also have solid track records. However, DVAL clearly has a system that works, too. By targeting a different segment of stocks than a traditional large-cap value ETF, you can efficiently diversify and capture the value factor without sacrificing quality or taking on excessive risk. For that reason, DVAL earns a "buy" recommendation, and I look forward to discussing this further in the comments section below.

For further details see:

DVAL: Now An ETF, This Top Performing Large Cap Value Fund Has My Attention