DLNG - Dynagas LNG Partners: Dirt Cheap But With A Potential Landmine

2023-04-17 11:02:27 ET

Summary

- The units of Dynagas LNG Partners presently trade with an insanely high circa 50% free cash flow yield that leaves them appearing dirt cheap on the surface.

- Although when looking further afield into the future and digging beneath the surface into their financial position, sadly there is a potential landmine, metaphorically speaking.

- Right now, they are benefitting from abnormally low interest rates that are actually even beneath the United States federal funds rate.

- This will change in the third quarter of 2024 when their hedges expire and they have to refinance almost the entirety of their debt.

- This could shave away half of their free cash flow and thus given the other associated risks, I only believe that a hold rating is appropriate.

Introduction

When it comes to investing, it is not too difficult to spot options that are cheap, such as Dynagas LNG Partners ( DLNG ) who presently trade with an insanely high circa 50% free cash flow yield. Although the real challenge is finding ones that are not a result of significant risks and thus, despite their units appearing dirt cheap on the surface, metaphorically speaking, I can see a potential landmine when digging beneath the surface that negates the appeal of their units.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

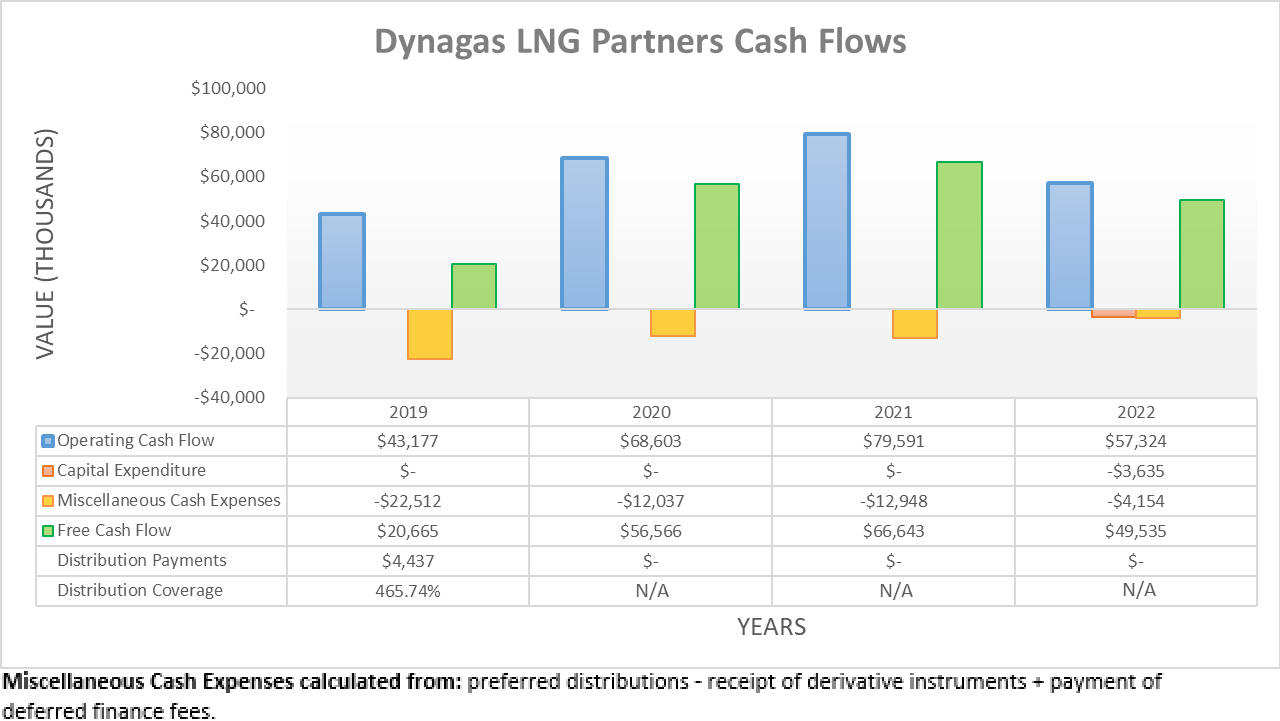

Despite the booming operating conditions for LNG during 2022 in the wake of the Russian invasion of Ukraine, alas it seems their cash flow performance was left behind. In fact, their operating cash flow of $57.3m was actually down circa 28% year-on-year versus their previous result of $79.6m during 2021. Thanks to their barebones capital expenditure during 2022, at least they were still able to translate most of this into free cash flow of $49.5m, which itself was also down by a similar extent year-on-year versus their previous result of $66.6m during 2021. Whilst not ideal, the shipping industry is inherently volatile and thus in this situation, the reason for this disappointing performance primarily stemmed from two reasons.

{kind=link}

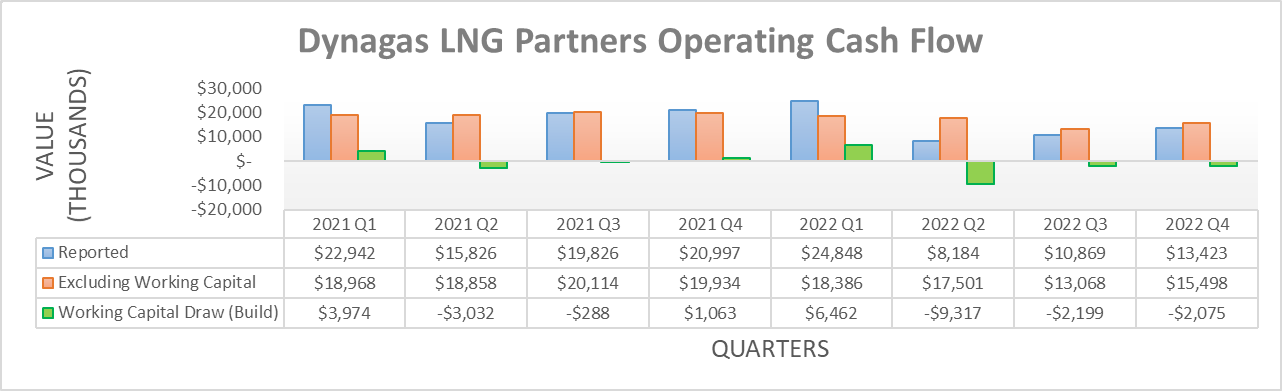

The first of which pertains to their working capital movements, which are more easily visible when viewing their operating cash flow on a quarterly basis. Routinely, they see various working capital builds and draws each quarter, which is normal for virtually every organization, although as 2022 saw a net build of $7.1m versus their previous net draw of $1.7m during 2021, it skewed the results in the favor of the latter. Even if excluded, their underlying result of $64.5m during 2022 was still down around 17% year-on-year versus their previous equivalent result of $77.9m during 2021 and thus more was at play. When examining their cash flow statement, this largely stems from 2022 incurring an additional cash outflow of $12.8m due to dry-dockings versus that of 2021, which are seemingly going to reoccur again during 2023, as per the commentary from management included below.

“We have three dry docks for 2023, which are expected in the third quarter of 2023.”

-Dynagas LNG Partners Q4 2022 Conference Call.

Since their fleet only contains six vessels, this is likely to create another headwind during 2023 but at least on the positive side, all of their vessels have charter contracts until the end of 2025, as per slide eight of their fourth quarter of 2022 results announcement . Even though these charter contracts ensure cash should keep flowing into the partnership, only time will tell where their free cash flow lands during 2023. That said, even if no better than 2022, their free cash flow of $49.5m still represents an insanely high free cash flow yield of almost 50% against their current market capitalization of approximately $103m. Even though this is seldom ever seen and leaves their units appearing dirt cheap on the surface, alas there is a potential landmine when digging beneath the surface into their financial position.

{kind=link}

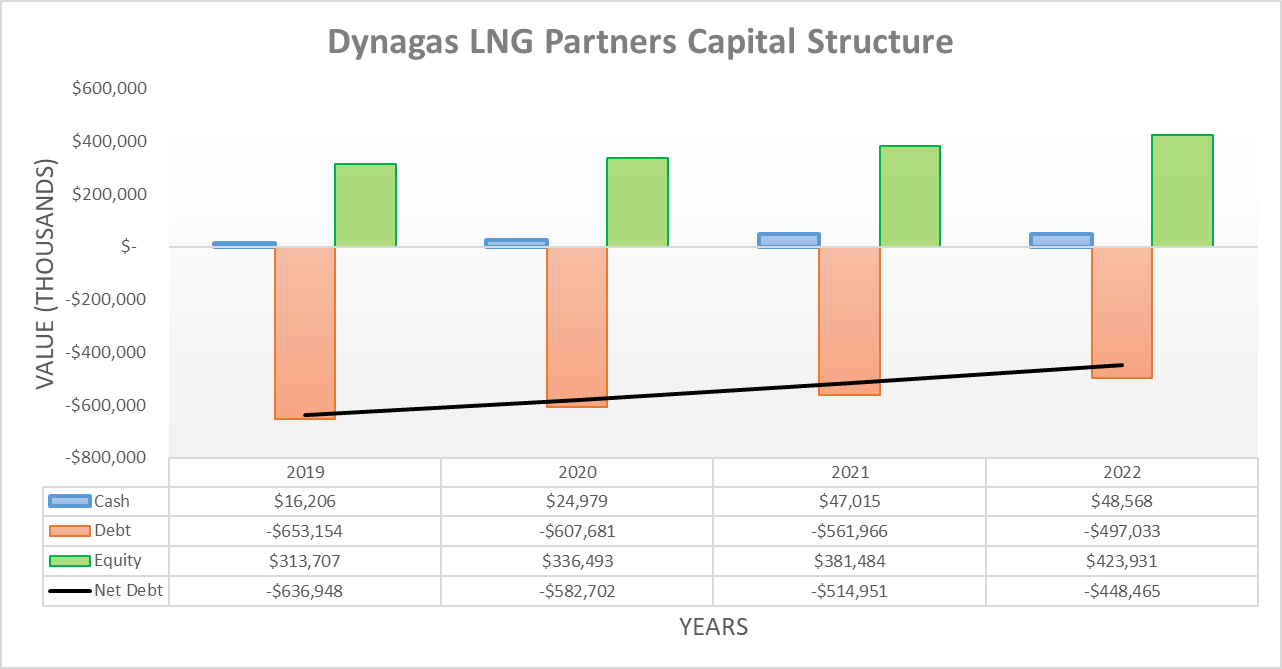

When first reviewing their capital structure, it is positive to see their net debt steadily decreasing every year at a decent pace with 2022 ending at $448.5m, which is down $66.5m or circa 13% year-on-year versus its previous level of $515m at the end of 2021. Going forwards into 2023 and I suspect, most likely into further years, they remain focused on decreasing net debt, as per the commentary from management included below.

“The partnership has remained committed to its strategy of reducing debt and has since September 2019 until Q4 2022 period…”

-Dynagas LNG Partners Q4 2022 Conference Call (previously linked) .

Due to the inherently volatile nature of the shipping industry, it remains to be seen how much their net debt continues decreasing during 2023. Although given their historical cash flow performance and aforementioned three dry dockings, I feel that a decrease of between circa $50m and $75m makes for a middle-of-the-road basis point. Whilst positive, it would still leave around circa $375m to $400m of net debt remaining at the end of the year and $325m to $375m remaining if continuing one year later at the end of 2024 that as subsequently discussed, sees a potential landmine.

{kind=link}

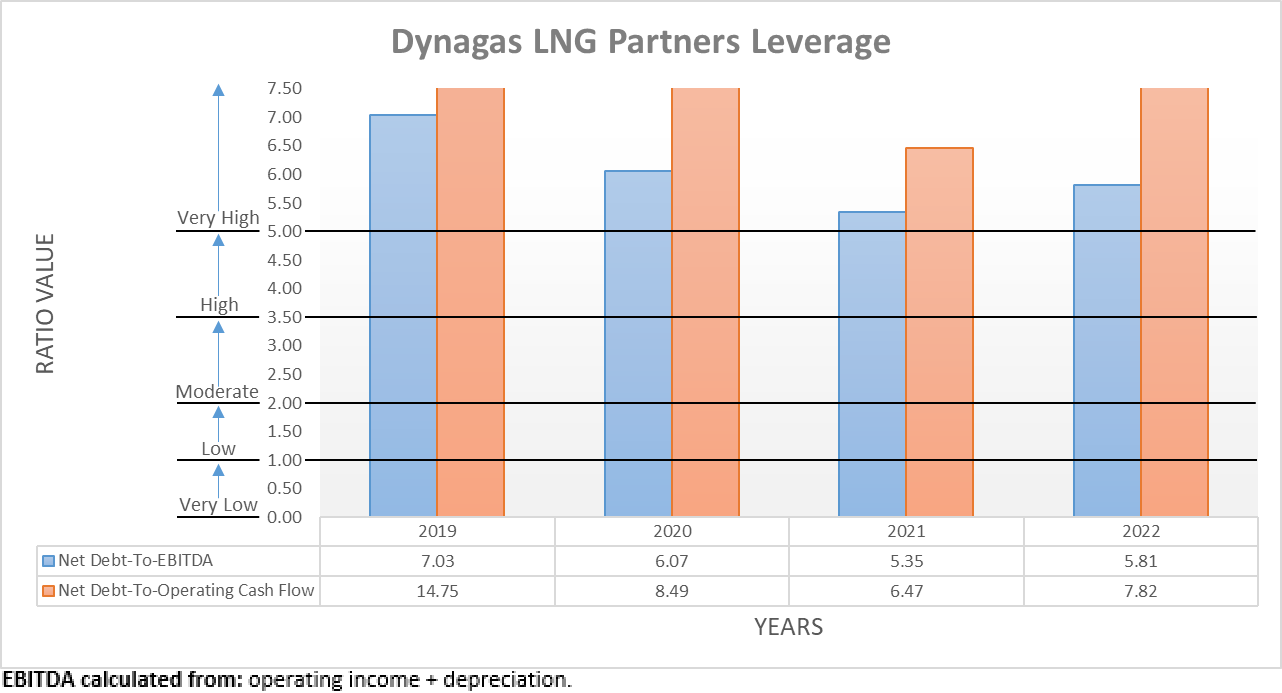

They have been steadily decreasing their net debt every year but unfortunately, their leverage is still very high, even at the end of 2022. To this point, their net debt-to-EBITDA is 5.81 that is accompanied by a far higher net debt-to-operating cash flow of 7.82, which are both materially above the threshold of 5.01 for the very high territory. Going forwards into 2023 and future years, their leverage should trend downwards in tandem with their aforementioned decreasing net debt, although this is obviously going to vary in line with their inherently volatile financial performance. Barring good fortunes, this will obviously take a number of years to rectify and whilst not ideal, the bigger issue pertaining to the potential landmine is still partially buried, metaphorically speaking.

{kind=link}

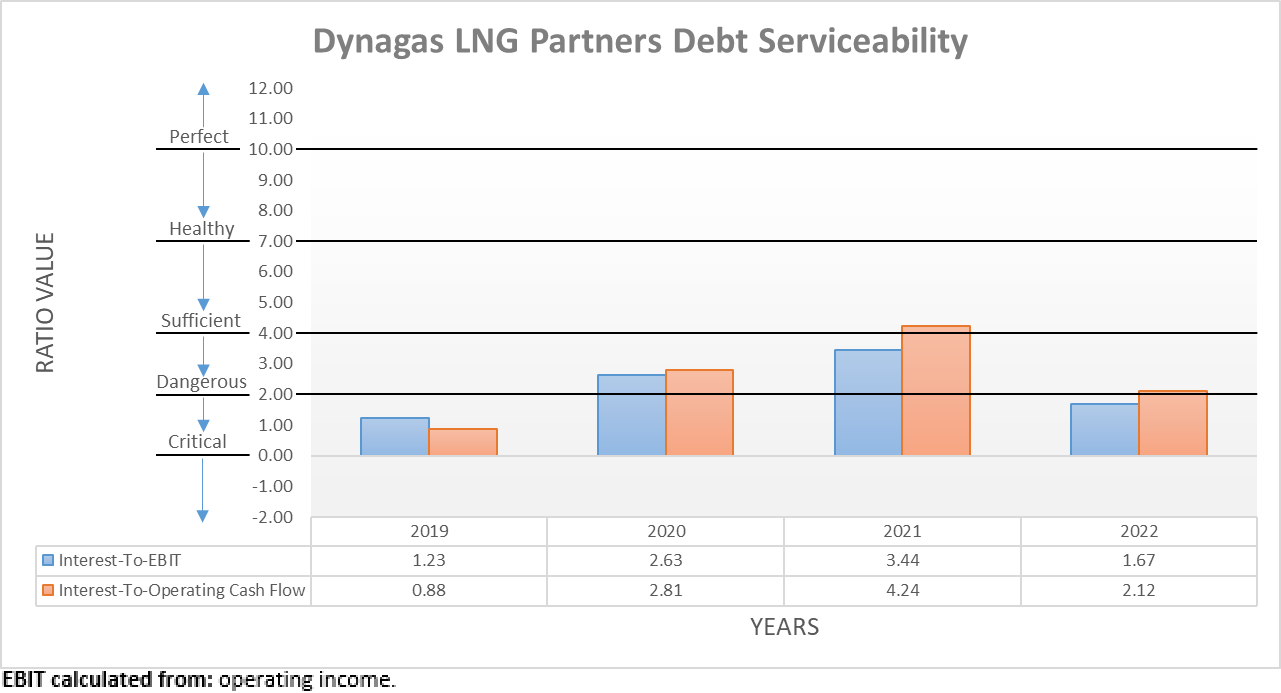

In light of their very high leverage, it should not come as a surprise to see their accompanying debt serviceability is dangerous, most notably when comparing their interest expense against their EBIT that produces interest coverage of only 1.67. Whilst comparing their interest expense against their operating cash flow yields modestly better interest coverage of 2.12 that is within the range I consider sufficient, I prefer to judge on the worse side.

This situation is already not ideal but to make it particularly concerning, their interest expense is actually abnormally low thanks to hedges that see an effective interest rate of only 3.41%, as per slide five of their previously linked fourth quarter of 2022 results announcement. Considering this is even beneath the present United States federal funds rate of 4.75% to 5.00%, there is no way that a small and inherently volatile shipping partnership with very high leverage could possibly borrow new debt anywhere near these rates within the foreseeable future.

Even though management deserves credit for hedging their interest rate exposure before monetary policy rapidly tightened, it still does not remove the risk of higher interest rates forever because unfortunately, these hedges expire during the third quarter of 2024 and thus expose the partnership to dramatically higher interest rates. Since their interest coverage is already dangerous despite these abnormally low interest rates, it threatens to significantly shave away their free cash flow in future years and thereby plants the metaphorically potential landmine.

Unless monetary policy suddenly loosens rapidly, I expect their interest expense to surge to circa 10% or at best, perhaps the high single-digits given the present United States federal funds rate. Even if their net debt continues decreasing to the circa $350m by late 2024 that I estimated earlier, adding another 5% to 7% to their interest expense equates to costs of $17.5m to $24.5m per annum that would shave away one-third to half of their free cash flow, if utilizing the $49.5m they generated during 2022 as a basis point. In turn, this risks bringing their insanely high free cash flow of yield of circa 50% down to circa 25% and whilst this is still massive, it is not nearly as appealing given the risks associated with their partnership, especially in light of their impending debt maturities. It also risks significantly slowing down their deleveraging by the same extent, thereby both further increasing and also, prolonging risks.

Following the analysis thus far, it is abundantly clear they cannot continue decreasing their net debt fast enough to have eliminated the majority by late 2024 when their hedges expire, which is also when almost the entirety of their debt matures. Whilst 2023 only sees a manageable $48m, alas September 2024 sees the rest of their debt maturing and therefore, north of $450m as it stands right now that creates a big hurdle to jump to avoid bankruptcy. Since they routinely generate free cash flow, it is realistic to avoid such a bad outcome but at the same time, they still have no choice but to enter the capital market asking for new debt, which is almost certainly not going to be offered beneath the United States federal funds rate like what they enjoy right now.

Generally speaking, debt is normally refinanced well in advance of maturity to minimise the risk of bankruptcy or being forced to accept onerous terms, such as suspending preferred distributions and so forth. In turn, this leaves much less room than otherwise apparent to wait for monetary policy to loosen, which itself remains a speculative notion right now given the Federal Reserve is still routinely increasing interest rates.

{kind=link}

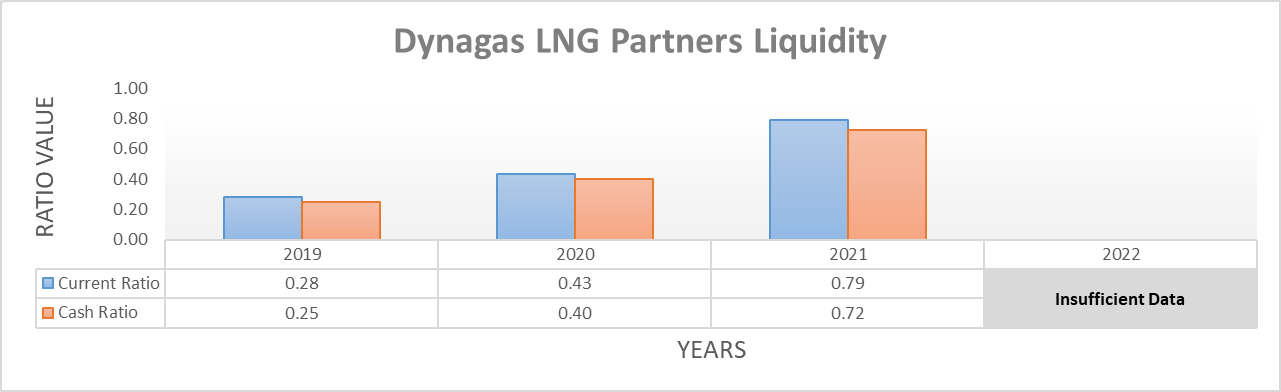

Despite already being halfway through April 2023, as of the time of writing they have unfortunately not provided a detailed balance sheet for the end of 2022 and whilst we know their cash, debt and equity, their current assets and liabilities are not completely known, which in turn leaves their latest current and cash ratios a mystery.

Thankfully, we can work around this small hindrance because at the end of 2021, their current and cash ratios saw respective results of 0.79 and 0.72, thereby meaning they had strong liquidity heading into 2022. Since their cash balance of $48.6m at the end of 2022 slightly increased versus its previous level of $47m at the end of 2021, it indicates their liquidity is not significantly different and by extension, they should not be reliant upon capital markets for anything, apart from refinancing their aforementioned debt maturities.

Conclusion

On the surface, their units are dirt cheap with an insanely high free cash flow yield of circa 50% that is seldom ever seen. Although when digging beneath the surface, alas there is a potential landmine waiting in the form of a massive debt maturity. Not only does this create a big hurdle to jump to avoid bankruptcy during a period of tight monetary policy but even worse, it exposes the partnership to the risk of dramatically higher interest rates that could shave away half of their free cash flow. When everything is said and done, I see the negatives negating the appeal of their units and therefore, I only believe that a hold rating is appropriate. In the event that monetary policy starts loosening rapidly or they somehow manage to strike a very desirable refinancing deal, this may be upgraded to a buy rating, depending upon other future events.

Notes: Unless specified otherwise, all figures in this article were taken from Dynagas LNG Partners’ SEC Filings , all calculated figures were performed by the author.

For further details see:

Dynagas LNG Partners: Dirt Cheap, But With A Potential Landmine