DLNG - Dynagas LNG Partners: I'm Sticking With The Almost 10% Yielding Preferred Shares

2023-05-09 10:30:00 ET

Summary

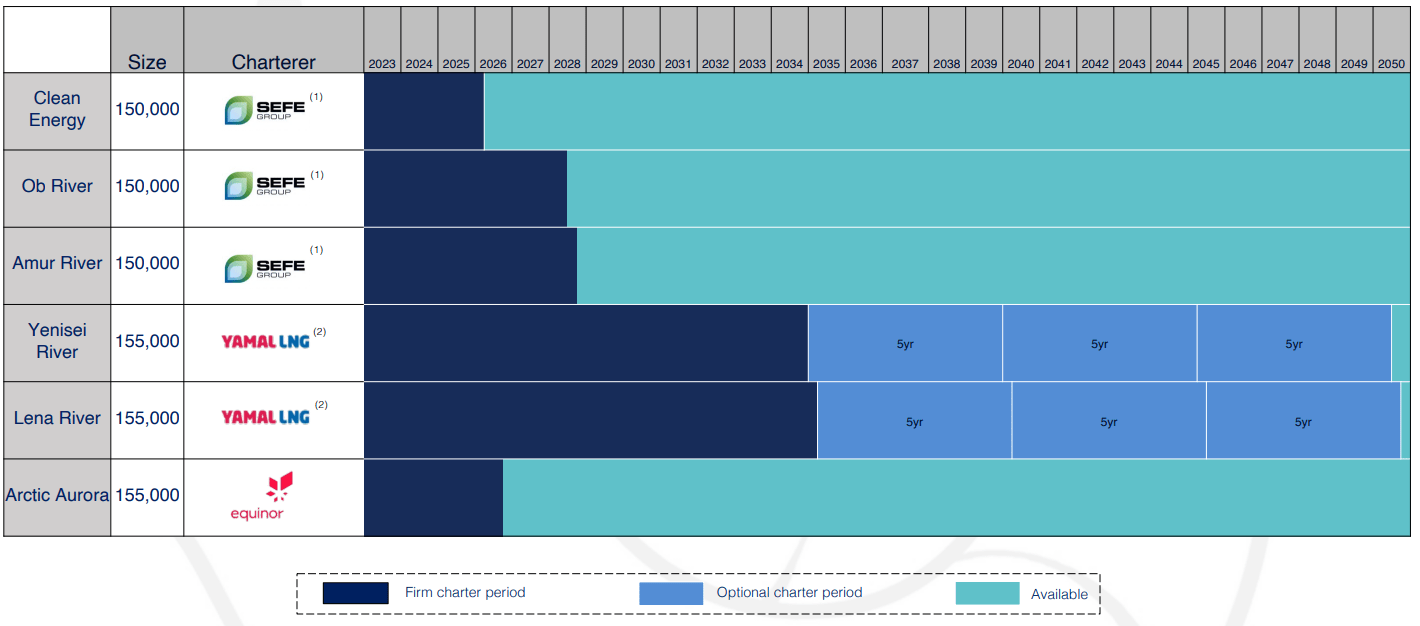

- Dynagas LNG Partners owns six LNG vessels, chartered to three different counterparties.

- Although two of the vessels have been chartered to a Russia-focused LNG operation, the partnership is not subject to sanctions.

- The cash flows are strong and predictable, but every available dollar is used to reduce the net debt.

- I don't want to be a common unitholder despite the discount to the book value. But I'm a satisfied preferred shareholder and may add to my position.

Introduction

Dynagas LNG Partners (DLNG) offers an interesting risk/reward trade-off but I'm mainly focusing on the preferred shares as I like the risk/reward of the preferred shares even more . The Series A of the preferred shares have a current dividend yield of almost 10% and as preferred equity obviously ranks more senior to the common equity. And as the partnership isn't paying any dividend or distribution on the common units, it's an easy choice for me to focus on the preferred shares for the income and from a safety net perspective.

The net debt continues to decrease

The common units of Dynagas have lost about 20% of their value in the past few months but even the preferred shares weren't immune as the higher interest rates on the financial markets make high-yielding assets less appealing.

That being said, Dynagas' financial performance is still pretty satisfying. Thanks to the longer term contracts, Dynagas' cash flows are pretty consistent. That doesn't mean it's risk-free as there still is some counterparty risk (the SEFE Group ('Securing Energy For Europe') which accounted for almost half of the revenue is the new name of Gazprom Singapore while the two vessels chartered by Yamal LNG are shipping Russian LNG to China). Additionally, Dynagas LNG Partners only owns six vessels which also reduces the diversification. And of course, the increasing interest rates will hurt the Partnership's bottom line once the interest rate hedges expire.

{kind=link}

As explained in my previous article and more recently by fellow author DT Analysis, Dynagas has hedged its interest rate risk until the third quarter of 2024 but that obviously also means that from Q4 2024 on, the partnership will be fully exposed to the market interest rates. DT Analysis calls it a landmine and that could very well be true for the common unitholders and is an additional reason why I like the preferred shares.

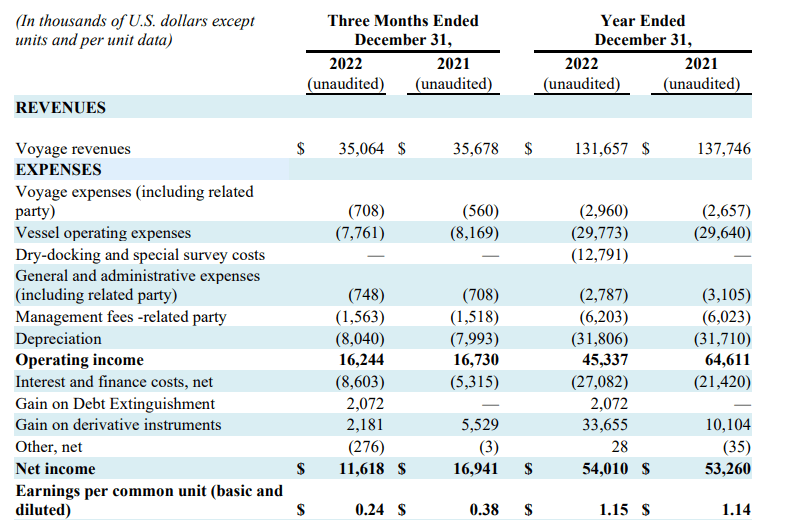

The income statement shows how important these hedges are. The partnership reported a $2.2M gain on derivative instruments during the final quarter of 2022 which went a long way to compensate for the $8.6M interest expenses.

{kind=link}

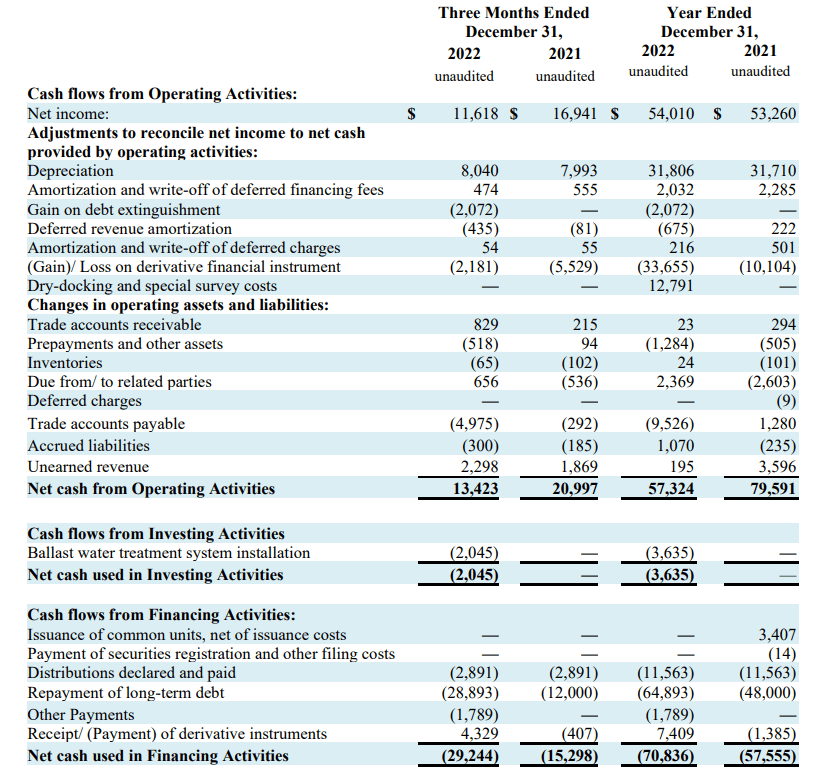

The cash flow statement actually shows the hedges are even more important on the cash flow level. Although there was an accounting gain of $2.2M on the interest rate hedges in the final quarter of the year, the cash flow statement shows the net cash inflow related to the hedges was approximately $4.3M. As you can see below, the cash flow remained strong and the operating cash flow adjusted for changes in the working capital position was approximately $15.5M and roughly $19.8M if you include the cash gains on the hedging book. The total capex was just $2M which means the underlying free cash flow was $17.8M including the impact of the interest rate hedges and $13.5M if you'd apply the normal market-based interest rates.

{kind=link}

The partnership tapped into its existing cash position and repaid almost $29M of its debt. It ended the quarter with $80M in cash and $497M in long-term debt for a net debt of $417M. Fortunately Dynagas still has a strong cash position and this, in combination with the incoming cash flow over the next six quarters, could go a long way to reduce the gross debt level to less than $400M which could soften the blow of higher interest expenses from Q4 2024 on. It will for sure not be sufficient to mitigate the impact, but it could soften the blow.

The preferred dividends are safe

As explained in a previous article, the preferred series A issued by Dynagas (trading with ( DLNG.PA ) as ticker symbol offer a fixed 9% preferred dividend ($2.25 per share, payable in four equal quarterly tranches of $0.5625 per share). The B-Series (trading with ( DLNG.PB ) as ticker symbol) were interesting but did not offer as much protection as those B-shares will soon offer a floating preferred dividend. From November 2023 on, the quarterly preferred dividend will be set at the 3M LIBOR + 5.593%. The LIBOR will no longer be in use, and the quarterly preferred dividend will likely use the 3M SOFR as benchmark.

At this moment, I'm more focusing on the A-series as I like the fixed payment and you know what you are getting. Last Friday, the A-series close at $23 per share which means the current dividend yield is approximately 9.8%. There is no foreign withholding tax on these dividends.

The preferred dividends are well-covered. The total amount of preferred dividends paid during Q4 of last year was just $2.9M which compares quite well to the $17.8M of free cash flow including the hedging gains and even if you'd use the underlying pre-hedge interest expenses of in excess of $8M for the quarter, the partnership still needs less than 25% of the free cash flow to cover the preferred dividends.

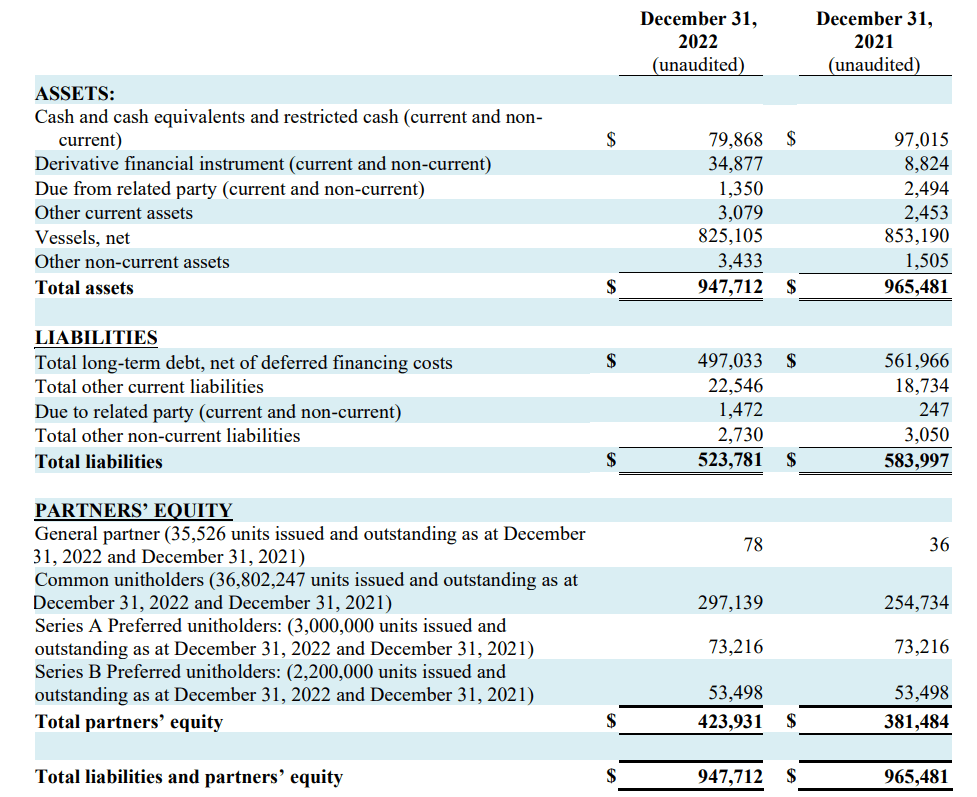

As you can see below, the total amount of equity on the balance sheet is $424M. There are 5.2M preferred shares outstanding for a total equity value of $130M. This means about $300M of the total equity ranks junior to the preferred shares. That is a very substantial increase from the $237M as of the end of Q3 2021 so the preferred shares are actually getting 'safer' as the company retains its earnings and spends its incoming cash flow on debt reduction.

{kind=link}

Investment thesis

I don't think I'd want to be an owner of the common units because although the partnership is making good progress at rapidly reducing its gross debt and net debt, there still is an awful amount of debt left on the balance sheet. While missing out on any potential double digit capital gains, I like the 'safety' (of course nothing is ever guaranteed) of the preferred dividends, so I am focusing on the additional layer of safety. Refinancing the existing debt in 2024 is the biggest risk but I expect the partnership's lenders to appreciate Dynagas' focus on debt reduction.

I currently have a small long position in the Series A preferred shares of Dynagas LNG Partners and as I'm having some cash available after Enbridge ( ENB ) called the subordinated baby bonds ( ENBA ), I may be looking to deploy a portion of it into Dynagas. At this moment, I am avoiding the common units of Dynagas despite the apparent deep discount to the book value of almost $8/share.

For further details see:

Dynagas LNG Partners: I'm Sticking With The Almost 10% Yielding Preferred Shares