DLNG - Dynagas LNG Partners: Parking Cash In The 9.4% Preferred Shares

2023-12-11 10:30:00 ET

Summary

- Dynagas LNG Partners has frustrated common unitholders by not paying dividends on its common units.

- The partnership's operating and financial performance remains strong, but all incoming cash is used to reduce debt, leaving common unitholders frustrated.

- The preferred shares of Dynagas offer a fixed 9% preferred dividend and currently yield 9.4% making them increasingly attractive to income investors.

Introduction

Dynagas LNG Partners (DLNG) has a lot of frustrated common unitholders as the partnership hasn't paid a dividend on its common units since 2019 . That's why I have been focusing on the partnership's preferred shares and the Series A preferred shares are currently offering a 9.4% yield. As the balance sheet gets safer on a quarterly basis as the partnership uses the free cash flow to reduce its debt, I think the preferred shares are getting increasingly attractive.

The partnership continues to print cash - but common unitholders don't see anything

Although the common unitholders haven't had any reason to be too happy with Dynagas LNG Partners, the partnership's operating and financial performance actually remain very strong. But instead of letting the common unitholders participate in the strong cash flow result, all incoming cash is used to reduce the total amount of debt on the balance sheet. While this makes the balance sheet stronger, common unitholders are getting very frustrated. And that's definitely understandable.

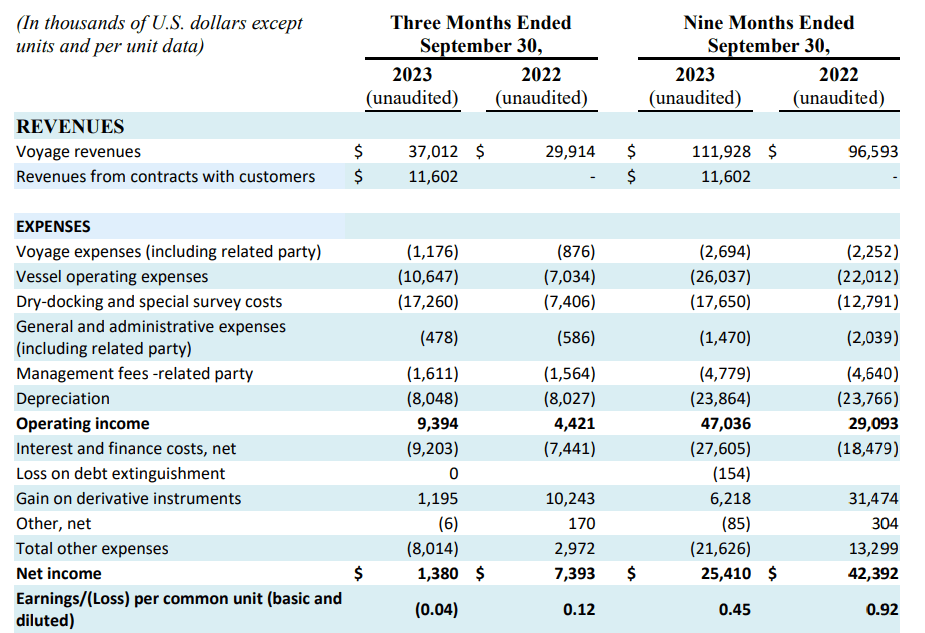

In the third quarter of this year, Dynagas LNG Partners reported a total revenue of $48.6M of which $37M was generated by the normal voyages (with the $11.6M generated from the contracts with customers representing the income from time charterers of its vessels for dry-docking and the special survey costs of those vessels). The total operating income was a disappointing $9.4M but this disappointing result was caused by the $17.3M in dry-docking and special survey costs. Excluding those expenses, the operating income would have been close to $27M.

{kind=link}

But those expenses definitely weighed on the result and the total net income was just $1.4M. This means the net income attributable to the common unitholders of Dynagas was negative as the partnership reported an EPS of negative 4 cents per share.

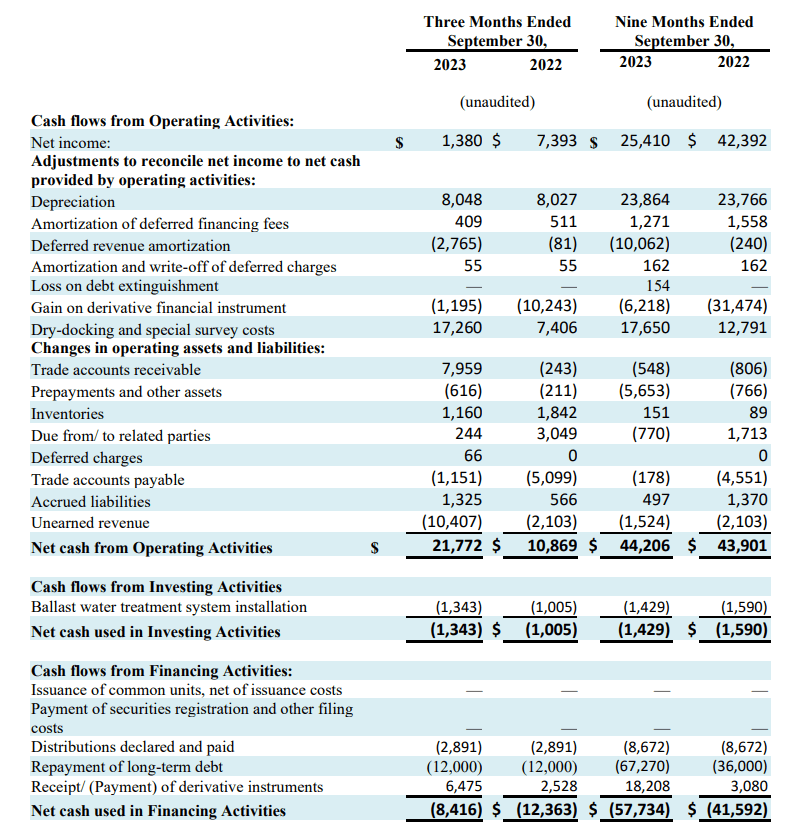

The total cash flow profile of the company was much stronger than that. The reported operating cash flow was $21.8M, but this includes a $1.4M investment in the working capital position and excludes the $6.5M in hedging gains (Dynagas was smart enough to hedge its interest rate exposure.

{kind=link}

So with a total cash flow of $23M and a capex of $1.3M (note: the drydocking expenses were not booked as capital expenditure), the underlying free cash flow result was almost $22M, and approximately $19M after making the $2.9M in preferred dividends.

Looking at the 9M 2023 results, we see a reported operating cash flow of $44.2M and an underlying operating cash flow of $52.2M with very minimal capital expenditures. And as the cash flow statement above shows, the partnership repaid $12M in debt in the third quarter, bringing the YTD debt repayment to $67.3M. That's good news, as this means the total interest expenses may remain relatively stable or will only increase by a manageable amount as hedges roll off and debt will have to be refinanced.

At the end of September, Dynagas had a net debt position of $366M compared to $417M at the end of last year. The total book value of the vessels was just over $805M at the end of September, which means the debt ratio (here defined as net financial debt versus the book value of the vessels) was 45.5% compared to 50.5% at the end of last year.

The preferred shares are a better idea for income investors

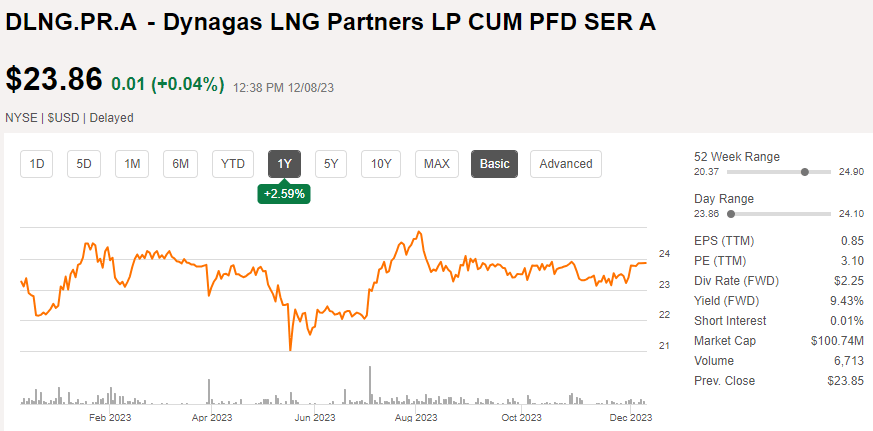

I already explained the details of the preferred shares in previous articles. The preferred series A issued by Dynagas (trading with ( DLNG.PR.A ) as ticker symbol offers a fixed 9% preferred dividend ($2.25 per share, payable in four equal quarterly tranches of $0.5625 per share). The B-Series (trading with ( DLNG.PR.B ) as a ticker symbol) was interesting but did not offer as much protection as those B-shares will soon offer a floating preferred dividend. From the next payment on, the quarterly preferred dividend will be set at the 3M LIBOR + 5.593%. The LIBOR will no longer be in use, and the quarterly preferred dividend will likely use the 3M SOFR as a benchmark. The recently announced quarterly dividend on the Series B preferred shares was $0.546875 per share (the last payment of the fixed 8.75% annual dividend) so it will be interesting to see the next quarterly dividend announcement for the Series B.

At this moment, I'm more focused on the A-series as I like the fixed payment, and you are not at the mercy of the short-term interest rates. At the time of writing this article, the Series A preferred shares are trading at $23.86, resulting in a preferred dividend yield of around 9.4%. There is no foreign withholding tax due on these preferred dividends.

{kind=link}

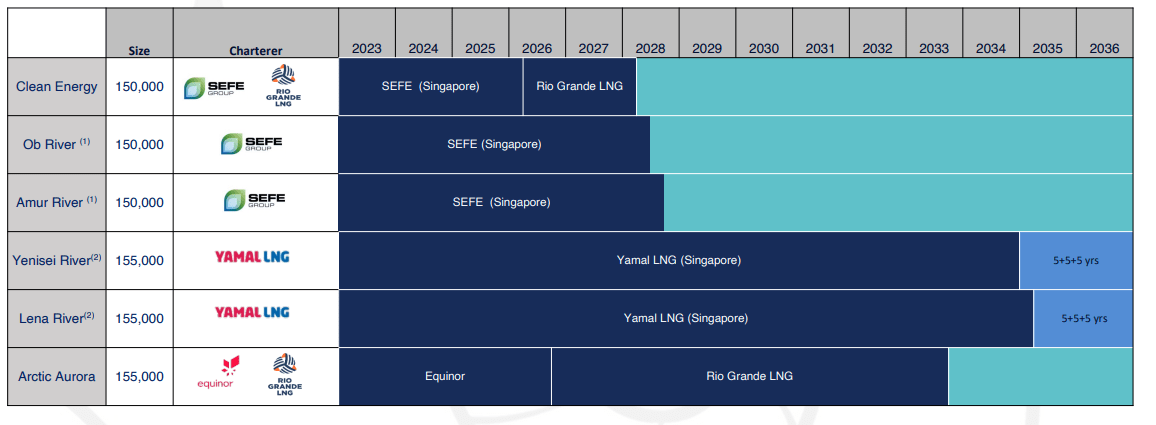

The ability of the partnership to cover the preferred dividend payments is very straightforward and as shown in the cash flow statement earlier in this article, I don't see any risk to the preferred dividend payments. As all the vessels are fully booked until well into 2028, I think the cash flow visibility is excellent as well. The total backlog exceeds $1B, with an average duration of 7.2 years. But more importantly, I anticipate Dynagas to generate at least $200M in free cash flow after making the preferred dividend payments in the 2024-2027 period.

{kind=link}

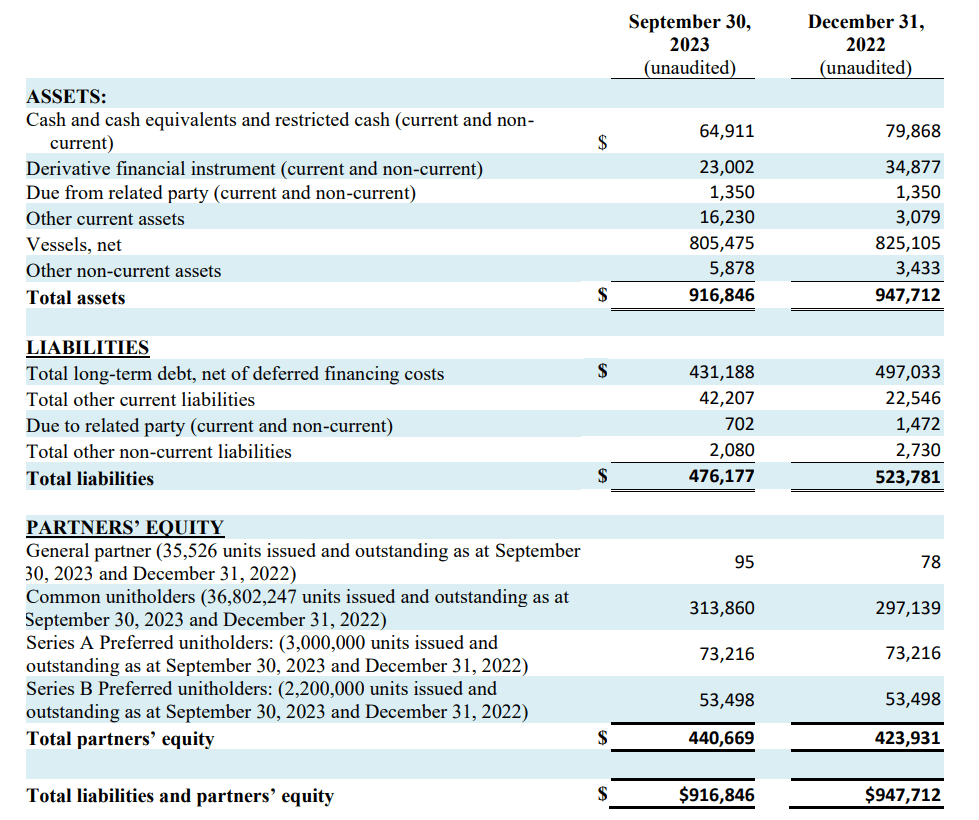

And while it is very unfortunate for the common unitholders to not get any dividend, the decision to use all free cash flow to reduce the net debt actually makes the preferred shares even safer. Let's pull up the balance sheet.

{kind=link}

As you can see above, the partnership had a total equity value of $441M. Not only is this an increase compared to the end of last year, but it is also an increase while the total size of the balance sheet decreased (as Dynagas has been repaying debt). There are currently 5.2M preferred shares outstanding with a total value of $130M. This means there is about $310M in equity ranked junior to the preferred shares. And even if the vessels were sold at a 35% discount to book value (which is close to impossible in the current LNG shipping environment) and if the partnership would be liquidated, the preferred shareholders would be made whole. And after every quarter of debt repayments, the balance sheet is getting safer with an even better coverage ratio for the preferred shares.

So what's holding back the share price then? I think it's the looming maturity date of the debt, as the entire $420M remaining gross debt will have to be refinanced in 2024.

DLNG Investor Relations

I think Dynagas will successfully refinance the debt, thanks to its recent efforts of sharply reducing the net debt, making refinancing more appealing for lenders. And given the strong performance in the LNG shipping markets, it's not unreasonable that upon a refinancing, there will be less strict covenants in place which could perhaps allow for the partnership to restart a (symbolic) dividend on the common units.

Investment thesis

I think the common units could be an interesting speculative bet on a refinancing agreement in 2024 which could allow the partnership to perhaps restart unitholder distributions, but I am mainly interested in the preferred shares and preferred dividends. My personal preference would be to focus on the Series A as I'm not willing to bet on the short-term interest rates. I think the 9.4% preferred dividend yield is a handsome compensation based on the risk profile.

I have a small long position in DLNG.PR.A but will likely increase this position as my fixed income portfolio will receive the proceeds from the Textainer ( TGH ) preferred shares being called in Q1 2024.

For further details see:

Dynagas LNG Partners: Parking Cash In The 9.4% Preferred Shares