DT - Dynatrace: High Growth In Cloud Infrastructure Observability And Security; Initiate With 'Buy'

2024-01-12 07:36:50 ET

Summary

- Dynatrace offers an observability and security platform for cloud-based infrastructure monitoring, driving revenue growth exceeding 20%.

- The company is making investments in research and development to expand its software intelligence platform and strengthen partnerships with consulting and service providers.

- Dynatrace's financial results show strong growth, with a high gross margin, strong free cash flow conversions, and a robust balance sheet. The company is projected to continue delivering around 20% growth in the next few years.

Dynatrace (DT) offers an observability and security platform that provides application and microservices monitoring, security, and infrastructure observations. The company has been experiencing revenue growth at a rate exceeding 20%, driven by the increasing demand for cloud-based infrastructure monitoring. It is a high-quality growth stock, and I am initiating coverage with a 'Buy' rating and a fair value of $65 per share.

Infrastructure Monitoring for Cloud

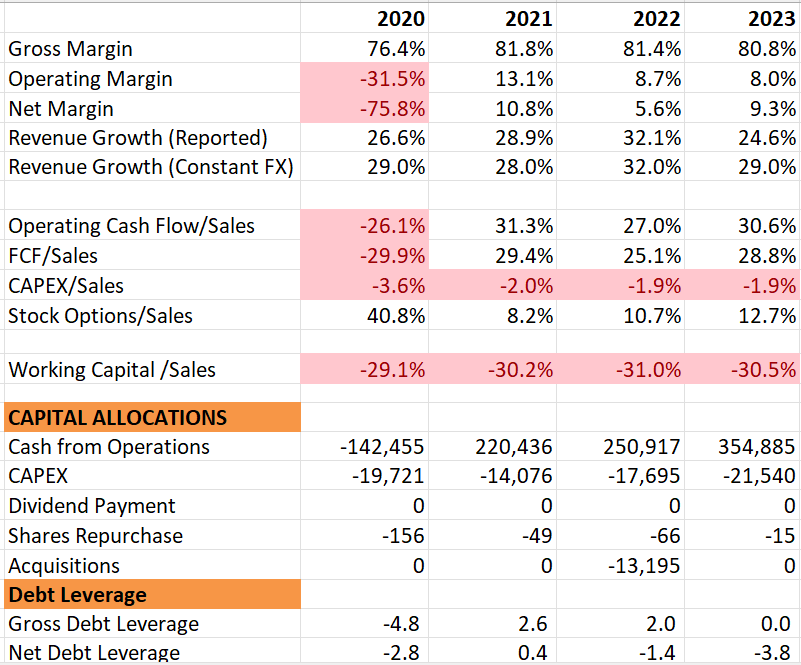

Dynatrace's platform empowers enterprises to achieve observability, security, intelligence, and automation for their cloud-based infrastructure. Dynatrace has showcased remarkable growth over the past few years, achieving close to 30% annual revenue growth and maintaining an adjusted operating margin above 25%.

{kind=link}

Their growth is driven by several factors. Firstly, their observability and security platform were developed in the cloud environment, making it uniquely suited for the digital transformation of enterprise workloads. As businesses migrate their workloads to the cloud, there's a growing need for a platform that can comprehensively monitor their entire IT infrastructure and security.

Secondly, Dynatrace is making substantial investments in research and development to expand the capabilities of their software intelligence platform. This includes modules for infrastructure monitoring, application and microservices, log management, cloud automation, and security. They allocate more than 18% of total revenue to R&D expenses, allowing these added modules to generate additional revenue and profits within the same platform.

Lastly, Dynatrace's solution offers automatic instrumentation, enabling the identification and resolution of technological issues before they lead to service outages. These infrastructure automation functions assist enterprises in saving costs and relieving their support teams.

Partnership with Consulting and Service Providers

Dynatrace is actively pursuing partnerships with key consulting and service providers, including Deloitte, DXC, Kyndryl (KD), Accenture (ACN), and Microsoft (MSFT). Through these partnerships, Dynatrace can leverage the global distribution and professional services capabilities of its partners.

In their Q2 FY24 earnings call , the company announced plans to accelerate their sales capacity in the second half of the year. While they are not currently capacity-constrained, the aim is to empower this incremental sales force to drive more growth for FY25 and beyond.

With the ongoing expansion of their sales capacity and the strengthening of partnerships, Dynatrace's solutions are becoming increasingly relevant to digital transformation. This strategic growth positions them to offer comprehensive cloud solutions for enterprise customers, encompassing both infrastructure and cloud monitoring, thereby enhancing their overall capabilities.

Financial Result and FY25 Outlook

As a typical high-growth software company, Dynatrace boasts a high gross margin, strong free cash flow conversions, and an asset-light business model. The company maintains a robust balance sheet with a net cash position. With a free cash flow margin approaching 30% and a subscription model driving substantial deferred revenue, Dynatrace exhibits a strong overall growth profile.

{kind=link}

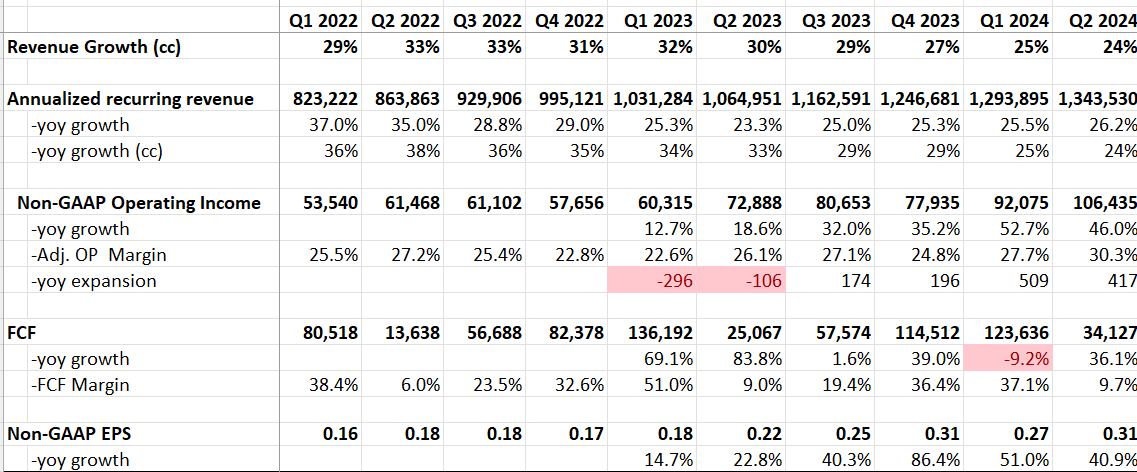

In Q2 FY24 , they delivered a remarkable 24% revenue growth on a constant currency basis, with adjusted operating profits experiencing a substantial 46% year-over-year increase. The quarter was exceptionally strong, leading to raised guidance across both topline and bottom line. Notably, subscription revenue witnessed a 26% year-over-year increase in constant currency, and annual recurring revenue grew by an impressive 25% year-over-year.

{kind=link}

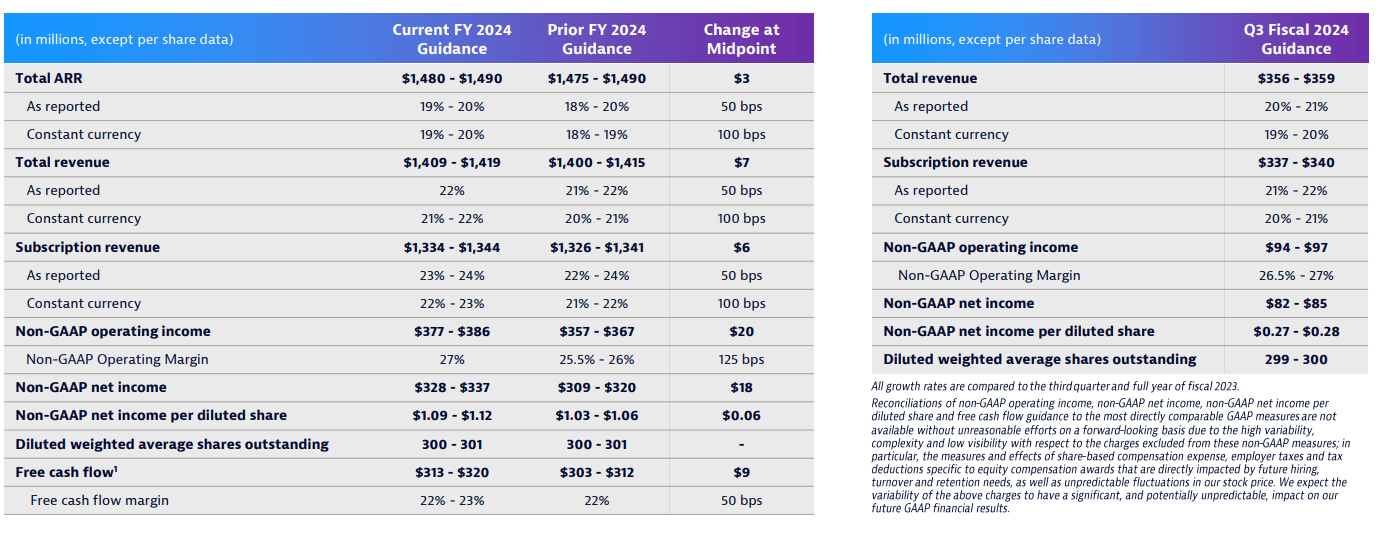

On the balance sheet, they ended with $702 million in cash and zero debt. Over the trailing twelve months, free cash flow amounted to $330 million, reflecting a solid 25% margin. The company raised its FY24 revenue guidance to 19-20% in constant currency, with a projected free cash flow margin of 22%-23%. This guidance is deemed quite reasonable.

Management has expressed confidence in their visibility and pipeline for the second half of FY24, anticipating an improvement in the macro environment during this period. During the earnings call, they conveyed a high level of confidence in meeting the FY24 results as planned.

{kind=link}

I anticipate their revenue to exceed a 20% growth rate in FY25 for several reasons. The announced plan to increase sales capacity in the second half of this year is expected to contribute to incremental growth in FY25. Furthermore, their robust growth in annual recurring revenue establishes a strong foundation for future expansion. I share the management's optimism regarding the gradual improvement in the macroeconomic environment in 2024, especially if the Fed initiates rate cuts.

In the post-pandemic era, many enterprises began optimizing their cloud spending, resulting in some slowdown in cloud expenditures. These optimization initiatives are likely to diminish in 2024, presenting a positive outlook for Dynatrace.

Valuations

The revenue growth assumption in FY24 aligns with their guidance, and the free cash flow in the model slightly exceeds their guidance range of $313 - $320 million. Historically, Dynatrace has tended to underpromise in their financial plans, and an upward revision of guidance in the second half of FY24 would not be surprising.

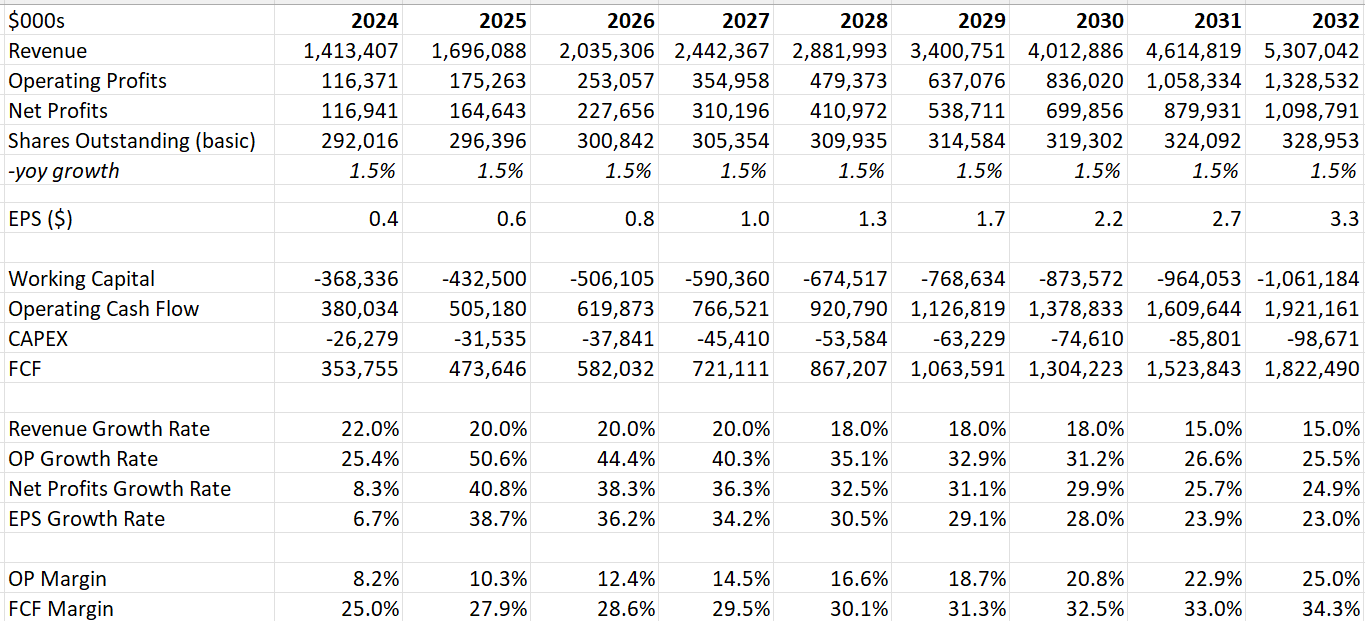

I project that Dynatrace will continue delivering around 20% growth in the next few years, tapering to a more moderate 15% growth from FY31 onward. Despite this high growth rate, the forecasted revenue is only expected to reach $5.3 billion in FY32, which is still relatively small compared to other established software companies. I believe their expansion into security could significantly expand their total addressable market, and their all-in-one platform could provide a holistic solution for digital transformations. In my opinion, these factors position their solutions to support exceptional growth over the next ten years.

{kind=link}

Their margin expansion is primarily driven by operating leverage, with operating expenses not needing to grow at the same rate as revenue. Currently, they allocate 18.8% of total revenue to R&D, and I project this ratio to decline to about 16% by FY32. Even at 16%, this figure remains relatively high compared to many growth-oriented software companies, in my view.

The model utilizes a 10% discount rate, 4% terminal growth, and a 19% tax rate, resulting in an estimated fair value of $65 per share.

Key Risks

High Stock Options : SBC represents more than 12% of total revenue. For a small growth company, utilizing stock options to attract superior technology engineers is a sensible strategy. It is anticipated that the SBC ratio will decline over time as the company scales and grows.

R&D in Europe : 65% of their employees are located outside of the United States, with a significant portion of their R&D operations based in Europe. Dynatrace requires a strong working culture to effectively manage their global R&D resources.

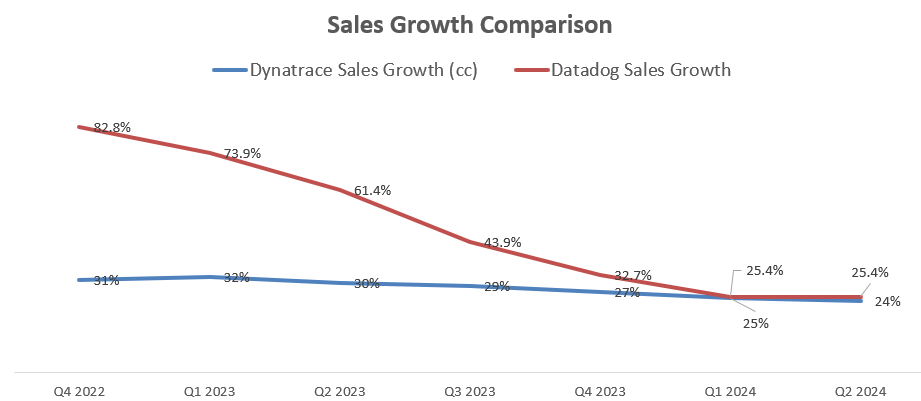

Competition from Datadog : Dynatrace is in direct competition with Datadog (DDOG), and both companies have demonstrated impressive revenue growth in the past. Dynatrace shareholders should actively monitor Datadog's performance as well. For more information on Datadog, please refer to my recent article on the subject.

{kind=link}

Takeaway

I believe the cloud infrastructure monitoring market is poised for structural growth over the next several years. Given Dynatrace's favorable positioning to capture this industry growth, I am initiating coverage with a 'Buy' rating and a fair value estimate of $65 per share.

For further details see:

Dynatrace: High Growth In Cloud Infrastructure Observability And Security; Initiate With 'Buy'