DT - Dynatrace Q2 Earnings: Preparing For Topline Growth Reacceleration

2023-11-06 07:41:40 ET

Summary

- Dynatrace's Q2 FY24 earnings report showed resilience in a fragile economic environment.

- Management is focused on reaccelerating topline growth through partnerships, investment in sales, and emerging product categories.

- The company's strong margin profile and stable revenues make it a less risky investment in the SaaS space.

Introduction and investment thesis

Dynatrace (DT) published its Q2 FY24 earnings report recently showing continued fundamental resilience in a fragile economic environment. After negatively surprising investors with its previous Q1 FY24 earnings release , shareholders could breathe a sigh of relief after the Q2 print. Back in the Q1 quarter the company suffered an unexpected ARR growth slowdown and provided quite conservative estimates for the financial year. In the aftermath, I argued that this won't last long as there are important growth drivers intact, which could reaccelerate topline growth soon. The Q2 earnings release and the accompanying earnings call showed that this could be the case indeed.

It has been confirmed that management still hasn't given up on reaccelerating topline growth, which could possibly happen sooner than later in light of current developments around the company. Besides strengthening partnerships with GSIs and hyperscalers, management decided to step up investment sales, another factor pointing towards a quicker turnaround. Meanwhile, emerging product categories are still performing well with ample room for further growth.

In light of these trends I believe, the shares of the company provide a good investment for the upcoming years at current valuation levels.

Not giving up on topline growth reacceleration

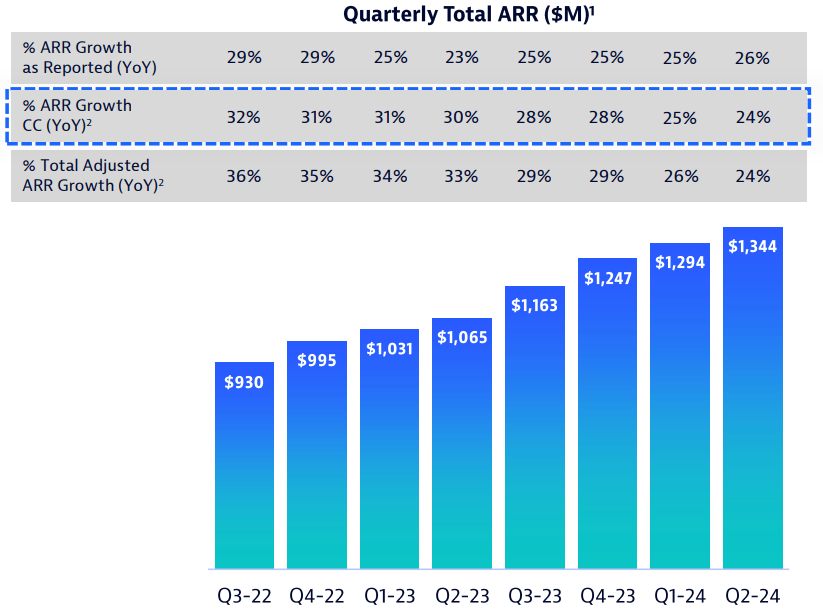

Dynatrace reported an ARR of $1,344 million for the Q2 FY24 quarter representing a YoY growth rate of 26%. This has been a slight acceleration compared to the previous quarters, however, after adjusting for FX effects topline growth slowdown still prevails:

Dynatrace Q2 FY24 earnings presentation

{kind=link}

The YoY ARR growth rate in constant currency reached 24% a further slight slowdown after 25% in Q1 FY24. Unlike after the Q1 quarter, when shares tanked 13% after the earnings release, investors didn't take this as a surprise. Management already guided for softer expansion trends resulting from IT spending cuts in an uncertain macro environment. This has materialized over the Q2 quarter indeed.

The big question is whether DT is ready to turn the tide, or if a few similar quarters could follow. Based on the optimistic comments from management on the Q2 earnings call , the strengthening ties with GSIs and hyperscalers, the success of emerging products, and the planned increase in sales capacity in the back half of the financial year I believe the reacceleration of topline growth is already on the corner.

Elaborating on the company's relation to hyperscalers and GSIs there have been important announcements made recently. First, DT announced a global alliance with Kyndryl, the world's largest IT infrastructure services provider. According to management, this partnership has already resulted in several six and seven-figure new deals. With this enhanced partnership with Kyndryl Dynatrace managed to set up strategic partnerships with all the top GSIs around the world.

Second, after announcing a go-to-market partnership with Microsoft (MSFT) back in July, Dynatrace shared with investors in October that several core innovations of the DT platform will be available on Microsoft Azure soon. The most important among these will be the native availability of Grail on Azure, which is the company's massively parallel processing data lake house.

Log management powered by Grail is one of the most important emerging product lines for the company (expected to reach $100 million ARR within a few quarters), so the general availability of Grail on Azure should be an important growth driver in the future. Besides logs on Grail, the application security solution of Dynatrace is also on track to achieve $100 million ARR by the end of FY25, so these emerging product lines could play an important role in the topline growth turnaround.

On top of this news, management decided to accelerate the addition of planned sales capacities in the back half of the financial year. They based their decision on good visibility and a strong pipeline for the second half, which suggests optimism going into the next quarters.

Although it is important to note that this optimism hasn't been reflected in management's topline guidance in my opinion, as it stayed approximately the same at an ARR of $1,475-1,490 million exiting FY24. I believe this means that current guidance is sufficiently de-risked, which could pave the way for further upside surprises over the coming quarters.

Finally, another important piece for potential ARR growth reacceleration is the new logo acquisition. With 160 new logos added over Q2, the metric came in flat yoy:

Created by author based on company fundamentals

For the first sight, this could have been a source of disappointment. However, taking into consideration that the average ARR per new logo land on a ttm basis increased to $140,000 in Q2 from $130,000 in Q1 I think it's also satisfying. This could be partly the reason that the company expects an increasing portion of net new ARR coming from new logo additions instead of expansion deals. This means that the historical mix of 1/3 new ARR growth coming from new logos and 2/3 from expansion deals could shift to 40% coming from new logos and 60% from expansion deals over the upcoming quarters.

All in all, I believe these trends suggest that Dynatrace will be able to get back to ~30% ARR growth rate over the course of FY25, and the first signs of this should be already visible in the upcoming quarters.

Maintaining a strong margin profile

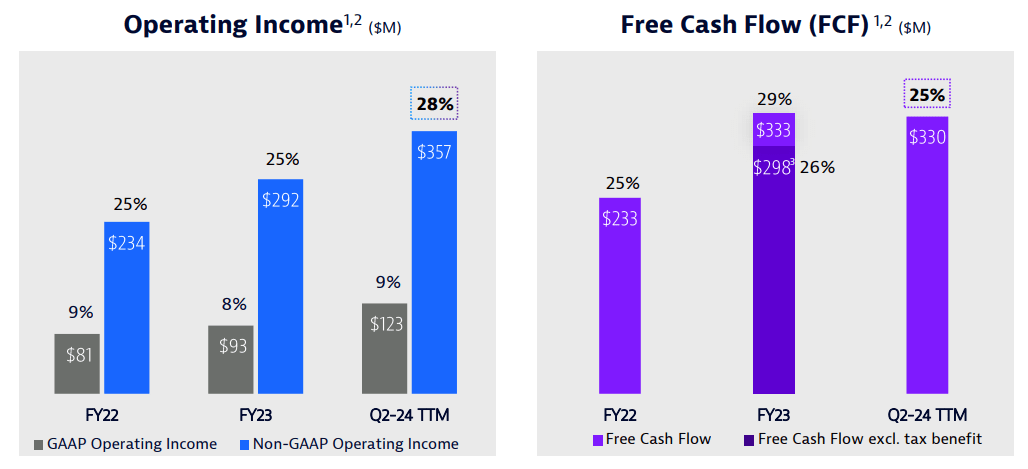

Taking a quick look at the company's margin profile investors can be still impressed:

Dynatrace Q2 FY24 earnings presentation

{kind=link}

Non-GAAP operating margin reached 28% in Q2 FY24 on a ttm basis, a 3%-point increase from the 25% reached in FY22 and FY23 as well. Meanwhile, FCF margin tracked at 25% in Q2 on a ttm basis, just like in the previous two financial years.

Dynatrace still belongs to those few SaaS companies that are profitable on a GAAP basis, which is good evidence for their prudent operating model. Thanks to the subscription-based pricing model revenues tend to be quite stable, which provides a good basis for a similarly stable and predictable bottom line. I believe this makes the shares of Dynatrace a good investment for those investors, who seek a somewhat less risky investment in the SaaS space.

Valuation and risk factors

Exactly like three months ago Dynatrace trades at a market cap of ~13.8 billion with FY24 sales expected to reach $1.41 billion. This results in a forward Price/Sales of ~10. If we assume that topline growth could accelerate back to ~30% for the upcoming 3 years and DT reaches a net margin of 25% shares would trade at a forward P/E of ~18 in three years' time. This compared to the P/E ratio of 19 of the S&P500 suggests to me that there is ample room for multiple expansion over this time horizon.

I believe as DT manages to stabilize its topline growth rate around 30%, its valuation multiple shouldn't compress meaningfully from current levels in the upcoming years. This means that in three years' time when revenues could approximately double from current levels (a CAGR of 27-28% satisfies this criterion) the share price should also double assuming no change in the valuation multiple. As a side note, this doesn't include stock-based compensation, which should shave off a few percentage points from the 'doubling share price in 3 years' assumption per year.

Finally, looking at the most important risk factors the company faces there is nothing new on the horizon. The cloud optimization cycle is still ongoing, and no one knows whether this is just temporary or possibly a new trend. Thanks to its subscription-based pricing model Dynatrace managed to escape a larger growth slowdown. However, if things would turn around the upside potential for the company would be more limited as well, at least compared to consumption-based players, like Datadog (DDOG).

Another important risk factor is competition in the observability space, especially from the side of large cloud providers. I believe Dynatrace mitigates this risk factor efficiently, as they constantly focus on building strong partnerships with these companies.

Conclusion

After a weaker Q1 quarter, Dynatrace managed to get back on track in Q2 and showed signs of optimism for the back half of FY24. I still envision the company as a leading player in observability, being able to grow revenues at ~30% on an annual basis for the upcoming several years. Further strengthening partnerships with GSIs and hyperscalers, the success of emerging products, and increased investment in sales could be an important driver behind this in the shorter run. I believe in light of this, shares provide a good entry point at current levels for the longer run.

For further details see:

Dynatrace Q2 Earnings: Preparing For Topline Growth Reacceleration