DZSI - DZS: 5G xHaul Technologies And M&A Could Trigger The Price

2023-04-07 00:08:09 ET

Summary

- DZS is a company that offers high-tech solutions through its different service channels.

- Successful development of new 5G mobile xHaul technologies, further creation of a network of partners, and internationalization could be quite beneficial for DZS.

- DZS may try to acquire emerging companies, like RIFT and Optelian, which may expand its portfolio of services besides generating alliances in the market ecosystem.

- Considering the contacts that DZS already has with leading Tier 1 carriers, the company already has the clients for its new solutions, which is quite convenient.

DZS Inc. ( DZSI ) is working on successful development of new 5G mobile xHaul technologies, and enjoys target markets that grow at the double digit. I believe that successful creation of new partnerships, internationalization, and new acquisitions of disruptive technologies could push the stock price up. There are some risks from failed introduction of new technologies or lack of liquidity, yet DZSI stock price is too low.

DZS

With a view to a hyper-connected world and supporting the transformation of technology provider businesses through a new generation of mobile connectivity, fiber optics, and online software, DZS is a company that offers high-tech solutions through its different service channels. These include broadband connectivity, home and business connectivity, antennas for mobile devices, and cloud-based software networks.

Its products to date have been used by more than 750 clients, including the Tier 1 internet protocol nationally in the USA and in business environments in more than 100 countries around the world. DZS develops, researches, tests, sells, and produces platforms in the areas of mobile connectivity and broadband connections, with 800 employees per day to date. In my view, the company is destined to create value for its customers and their products by offering innovative solutions that strengthen communication circuits globally .

{kind=link}

Source: Investor Presentation

The company reports a single segment of operations, which includes the sections named above. The broadband connection is provided for residential and commercial customers either by fiber services or by replacing the old copper connections of the network. In this way, service providers can offer their customers high-definition video playback as well as 10-gig voice and internet services. Something similar is the connectivity service for homes and businesses through its Helix platform by installing fiber optic networks to offer a high connection speed.

In addition, through Chronos, DZS offers a large-scale solution and manageability to mobile phone service providers, allowing them to upgrade the network to 5G connection, exchange IP protocols, and connect from different radio broadcast nodes.

{kind=link}

Source: Investor Presentation

Finally, its online storage allows providers to build a digital architecture that decreases the cost of operations and the risk of damage, which in turn increases the speed of communication and response.

I believe that one of the reasons to have a look at DZS is the growing target market of some of the technologies offered by DZS. Management expects that the target market for Cloud EDGE will likely grow at a CAGR of 35%. Besides, the global market, including Optical EDGE and Cloud EDGE, is expected to grow at a CAGR of close to 18%. With these figures in mind, I think that making a forecast of future FCF and net income growth for the next ten years appears appropriate.

Source: Investor Presentation

Besides, I think that having a look at the recent guidance given by management may generate certain interest from investors. DZS expects an Adjusted EBITDA close to $25-$40 million, which includes restructuring costs close to $6.5 million in 2023. Guidance also included growing adjusted operating margin close to 36%-38% and 2023 net income losses between -$8 million and -$23 million. Under my assumptions, DZS may report negative net income in 2023, but in the future, profitability will likely improve as economies of scale and the target markets grow .

Source: Quarterly Report

DZS Reports A Significant Amount Of M&A Activity

The balance sheet recently reported includes an impressive increase in total assets, mainly accounts receivables, inventories, goodwill, and intangible assets. In 2021 and 2022, the company signed several acquisitions that explain part of the increase in assets.

DZS acquired ASSIA, assets from RIFT, Inc, and Optelian. In my view, having a look at the balance sheet of ASSIA is appealing. DZS is mainly acquiring intangible assets, mainly software and business connections from targets.

On May 27, 2022, the Company acquired certain assets and liabilities of Adaptive Spectrum and Signal Alignment, Incorporated (“ASSIA”).

On March 3, 2021, the Company acquired substantially all of the assets of RIFT, Inc., a network automation solutions company, and all the outstanding shares of RIFT India Private Limited.

On February 5, 2021, we acquired Optelian Access Networks Corporation (“Optelian”), a leading optical networking solution provider based in Ottawa, Ontario, Canada.

Source: Annual Report

Source: Annual Report

Balance Sheet

As of December 31, 2022, DZS reported cash and cash equivalents of $34 million, restricted cash of $3 million, accounts receivable of close to $153 million, and other receivables of $16 million.

Besides, inventories stood at $78 million with prepaid expenses and other current assets of $8 million and total current assets close to $295 million.

Finally, with right-of-use assets from operating leases of $12 million, goodwill of $19 million, and intangible assets worth $31 million, total assets stood at $385 million.

Source: Annual Report

I believe that the total amount of liabilities is not scary as management did not report a lot of debt, and pension liabilities are rather small. The largest liabilities include accounts payable of $121 million, short-term debt of $9 million, current portion of long-term debt of $24 million, and contract liabilities worth $21 million. Operating lease liabilities were equal to $11 million with pension liabilities worth $11 million and total liabilities of $242 million.

Source: Annual Report

My Assumptions Include Successful Development Of New 5G Mobile xHaul Technologies, Acquisitions Of Emerging Players, And More Partnerships

The strategy for the future is based on generating a global presence. There are many markets out there where the company could improve its operations, for instance in Asia, Vietnam, Korea, China, and Africa. For this, the continuous development of new technological applications and innovation in the provision of services are key elements of customer retention. In this sense, in my view, DZS may try to acquire emerging companies, like RIFT and Optelian, which may expand its portfolio of services besides generating alliances in the market ecosystem, in which the company's operations are involved.

I also believe that further research and development will likely lead to innovations around 5G mobile xHaul technology. Considering the contacts that DZS already has with leading Tier 1 carriers, the company already has the clients for its new solutions, which is quite convenient. Management gave a few hints about what may be coming in the future. I am quite optimistic about the potential new wireless networks and data analytics offerings.

These development efforts include innovating in environmentally hardened DWDM coherent optics and compact ROADM solutions to address emerging transport traffic needs, developing a new generation of SDN/NFV solutions for unified wired and wireless networks, upgrading our broadband access technology for 10 and 25/50/100 gigabyte access speeds, and introducing our cloud managed WiFi solutions and data analytics offerings.

Source: Annual Report

Besides, I believe that further creation of a network of partners all over the world will likely bring revenue growth. Among different partnerships, the company mentioned resellers, system integrators, and distributors, which will likely help in connecting to new clients. In this regard, I believe that investors may want to read the following lines from management.

We have a track record of building a diverse but targeted network of partners to help drive growth in specific segments of our business or in specific geographies. For FiberLAN, we are working with distributors, value added resellers, and system integrators to broaden our enterprise go to market presence. In India, we are working closely with municipalities to deploy their initial fiber-to-the-home vision and help deliver high speed broadband access to residents.

Source: Annual Report

My DCF Model

My numbers for the future include net losses in 2023, net income growth from 2024 to 2033 driven by market growth, and perhaps further inorganic growth. I also assumed D&A growth, stock-based compensation growth, decreases in accounts receivable, inventories growth, and CFO growth. I believe that my figures are realistic. I gave the figures for the year 2020, 2021, and 2022.

Numbers for the year 2023 include net income of $110 million, depreciation and amortization of $5 million, impairment of long-lived assets of close to $4 million, and stock-based compensation of $7 million. I also assumed changes in accounts receivable of -$45 million, other receivables of -$66 million, changes in inventories of $39 million, and changes in prepaid expenses and other assets of close to -$2 million. Finally, I obtained cash flow from operations of $112 million. With purchases of property, plant and equipment of -$13 million, the free cash flow would stand at $100 million.

Source: My DCF Model

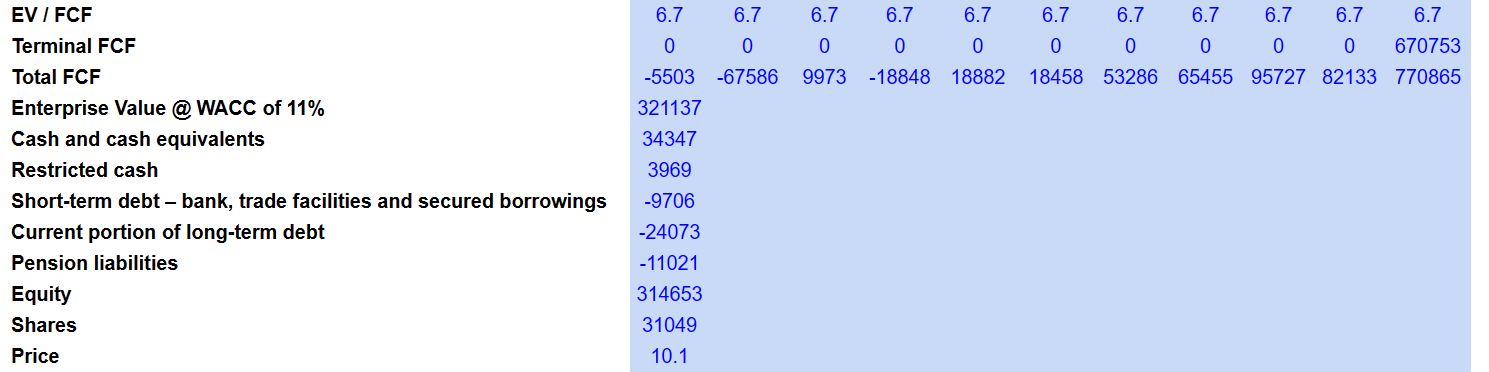

Now, if we assume a WACC of 11%, my results would include an enterprise value of $321 million. Adding cash and cash equivalents of $34 million and restricted cash worth $3 million, and subtracting short-term debt of -$10 million, current portion of long-term debt of $-25 million, and pension liabilities of -$12 million, the equity valuation would be close to $314 million. Finally, the fair price would be around $10-$11 per share.

{kind=link}

Source: My DCF Model

Large Competitors And Many Risks

DZS's competitors often offer products in all the markets in which the company participates, with the telecommunications market being an area of ??high competition and high speed of transformation. Some of the biggest competitors in the core of its business, which is the connectivity offer for both residences and businesses, are Huawei, ADTRAN ( ADTN ), Calix (CALX), Nokia ( NOK ), and ZTE (ZTCOF). There are also Cisco Systems ( CSCO ) and Juniper Networks ( JNPR ), which also offer network solutions, online storage software, and platforms.

There are several risk factors that require consideration from the company. The first factor is the inability to retain key personnel and clients as well as to develop products that comply with the demand and need of the market. If smart individuals leave the company, the company may not offer new innovative products, which, in the long term, will likely deteriorate the brand. As a result, future free cash flow expectations would lower, which may lead to stock price declines.

On the other hand, due to the nature of the products, they usually end up showing flaws. This dislocation in the design and test times can also lead to errors in the operational sphere of the company. If customers dislike the services received, they may leave the company, which may lower net sales growth expectations.

I also believe that introduction of new products may fail because DZS may offer technologies that clients do not need or do not understand. It is also worth noting that acquisitions may also fail because products acquired are not as valued as expected. Under the worst-case scenario, management may have to report goodwill impairments, which would bring book value per share declines and stock price volatility.

DZS does appear to use equity to finance its operations. If management cannot find new investors to buy shares, I believe that liquidity may represent a problem in the long term. If CFO and FCF do not increase as expected, lack of liquidity may not be appreciated by the market. In this regard, management offered an explanation.

As of December 31, 2022, we had approximately $34.3 million in unrestricted cash and cash equivalents, including $11.3 million in cash balances held by our international subsidiaries. If we are unable to raise additional capital, we may be unable to adequately fund our existing operations.

Source: Annual Report

Conclusion

In my view, successful development of new 5G mobile xHaul technologies, further creation of a network of partners, and internationalization could be quite beneficial for DZS. Besides, taking into account the expectations about future growth of Cloud EDGE markets, in my opinion, the company could be worth significantly more than what the market discloses. Yes, I did see some risks from failed introduction of new technologies, failed M&A attempts, or lack of liquidity; however, DZS could be worth much more.

For further details see:

DZS: 5G xHaul Technologies And M&A Could Trigger The Price