DZSI - DZS: Impressive Cloud Software Quarterly Growth Lower Guidance And Undervalued

2023-07-10 08:07:12 ET

Summary

- DZS Inc. reported impressive quarterly revenue growth from cloud software and services, driven by inorganic growth and sales growth expectations for 2023.

- Despite lowered EBITDA guidance for 2023, analysts expect business growth in 2024, supported by recent product launches and the Fiber Upgrade Cycle.

- Despite risks from failed restructuring, supply chain disruptions, or component shortages, DZSI stock price appears undervalued and could trade higher.

DZS Inc. ( DZSI ) delivered an impressive quarterly revenue growth from cloud software and services driven by inorganic growth and further sales growth expectations in 2023. The EBITDA guidance for 2023 was lowered, which the markets seemed to dislike quite a bit. I believe that the reaction of the stock price was too pessimistic. With other analysts expecting business growth in 2024, the recent launches of Xtreme Transport, Xtreme Access, and Xtreme Mobile, and the Fiber Upgrade Cycle, I think that the stock price could trade higher. Even considering risks from failed restructuring, supply chain disruptions, or lack of components, the stock price appears undervalued.

DZS

Incorporated in Delaware, DZS is a global provider of access and optical networking infrastructure and cloud software solutions.

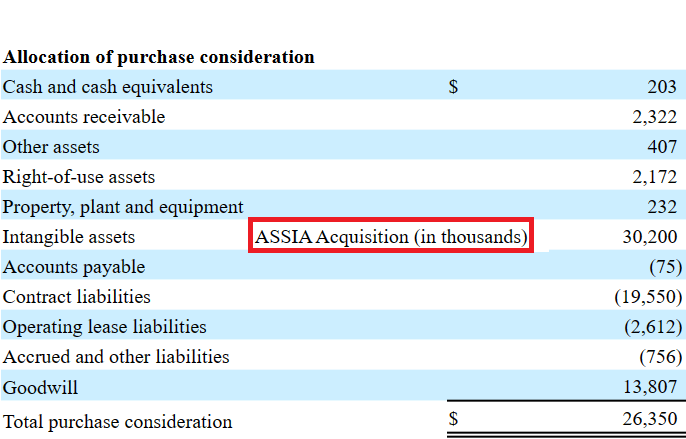

Most of the revenue comes from access networking infrastructure. However, the amount of revenue from cloud software and services is also growing, and is expected to grow more in 2023. In the last quarterly report, cloud software and services increased significantly due to the acquisition of Adaptive Spectrum and Signal Alignment, Incorporated for $26 million.

{kind=link}

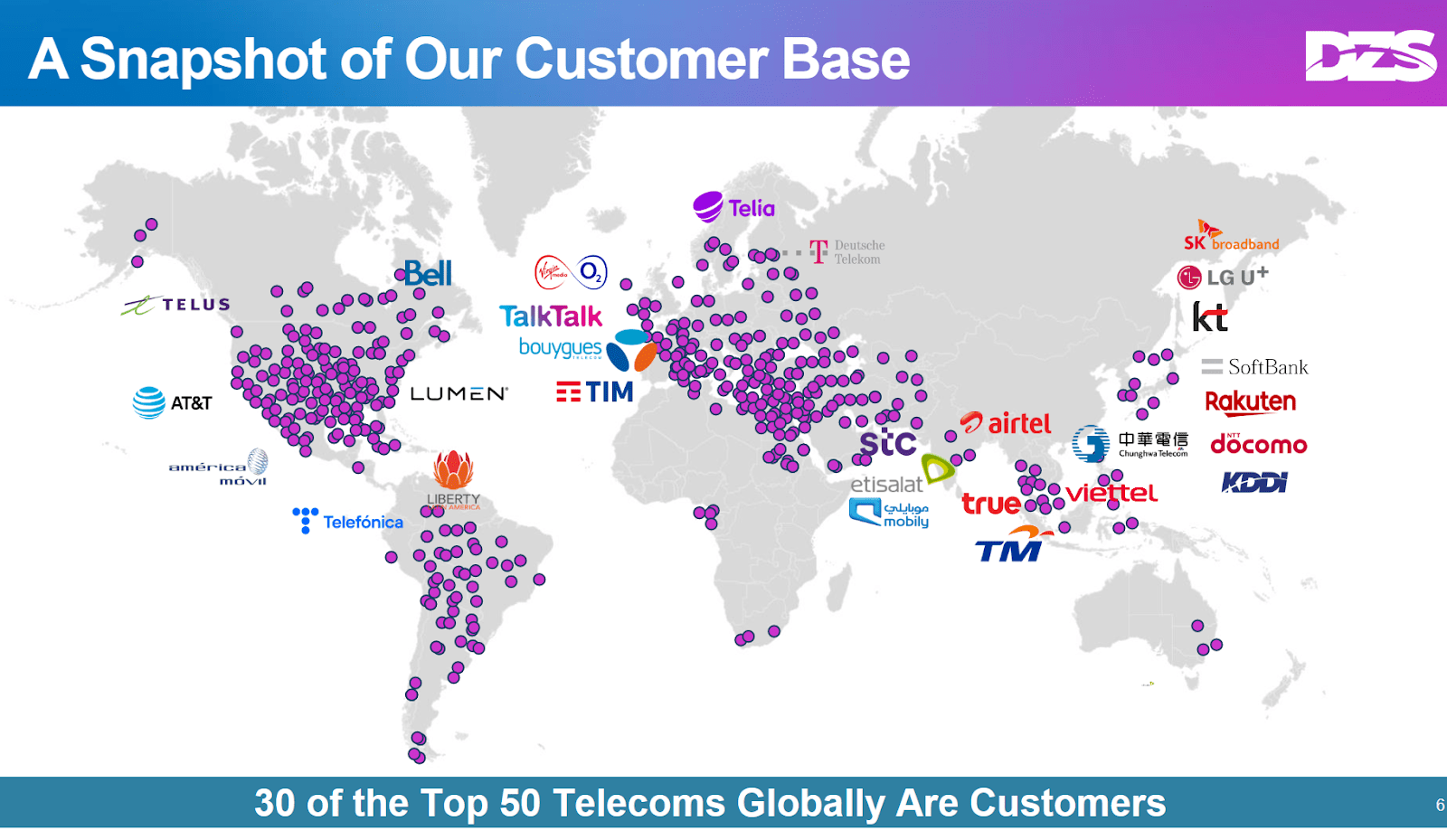

The company invests in growing innovative markets. In addition, the global telecom conglomerates are also customers. With the trust obtained from these large clients, I believe that many investors would most likely be interested in DZS.

Source: Quarterly Presentation

{kind=link}

I assessed the company a few months ago in an article , in which I noted that double digit growth and innovative 5G markets would imply significant upside potential in the stock price.

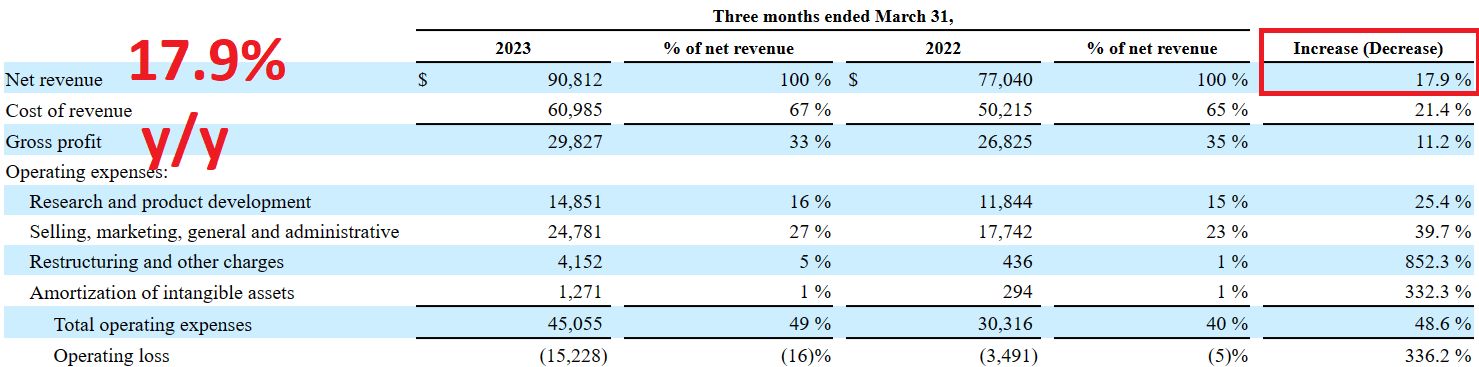

In the last quarterly report, management included net revenue growth of 17.9% y/y and gross profit increase of 11%. We are talking about the previously released results. In June, 2023, management noted that the company will restate its previously issued financial statements. The value of the revenue to be restated is approximately $15 million. It is not a large amount of dollars.

DZS announced that it will restate its previously issued financial statements for the first quarter of 2023, which ended March 31, 2023. The restatement relates to timing of revenue recognition with respect to two customer projects. The value of the revenue to be restated is approximately $15 million, of which the company anticipates the majority will be recognized during the second and third quarters of 2023. Source: DZS to Restate First Quarter 2023 Financial Statements

Increases in restructuring changes as well as selling and marketing expenses led to quarterly operating losses, which some market participants did not seem to like. After the earnings report and the guidance released for the full year 2023, the stock price declined, which does not really change my vision about DZS.

{kind=link}

It is also worth noting that DZS experienced significant acceleration in Asia, where quarterly revenue increased close to 32.4%. In my view, if Asia continues to demand the network offering or DZS, pessimistic numbers in Europe or the United States may not matter that much.

Source: 10-Q

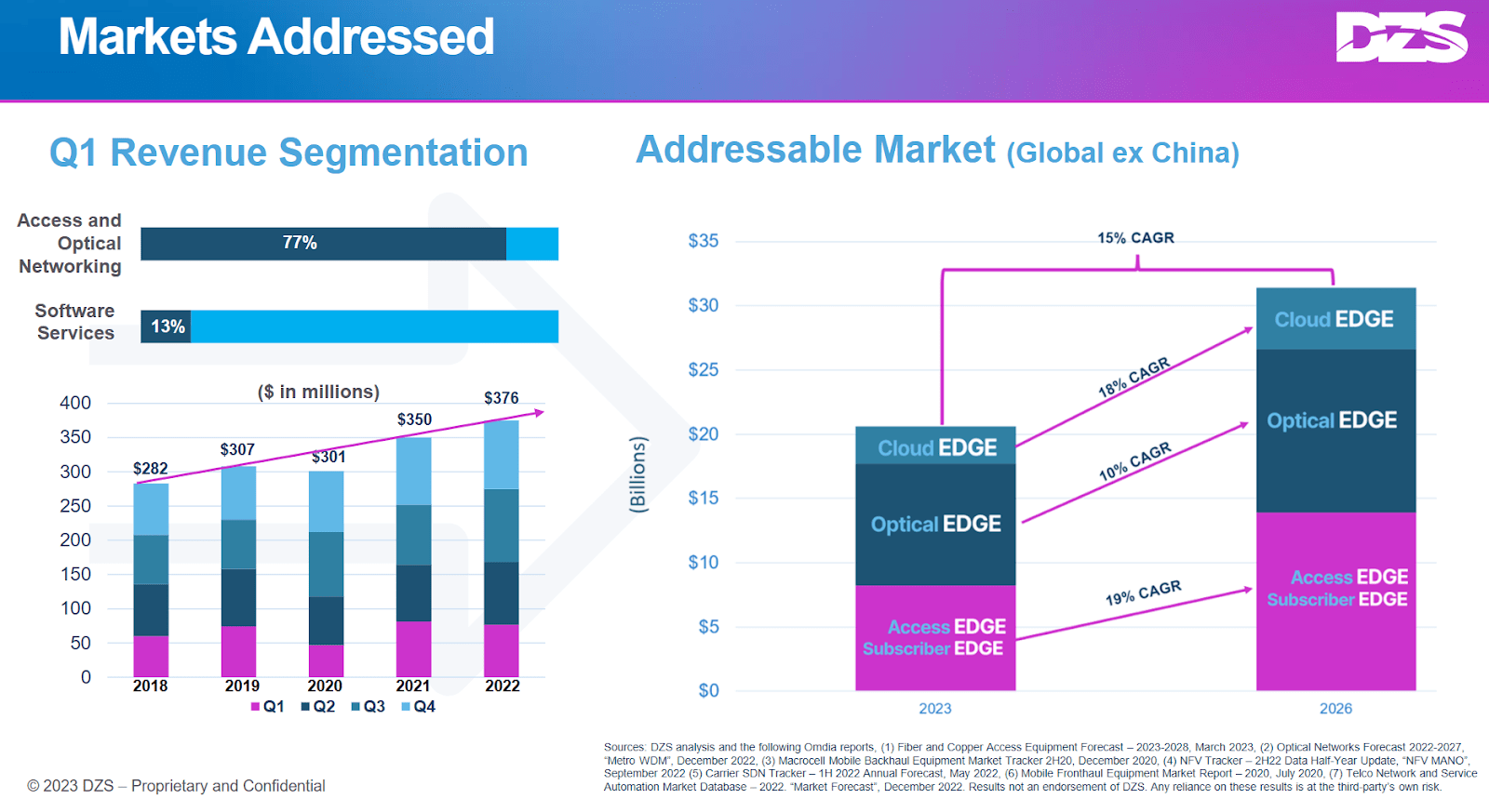

The company continues to target massive addressable market sizes that grow at close to 15%-19% CAGR. The markets of Cloud Edge, Optical Edge, Access Edge, And Subscriber Edge are all growing at a double digit. Hence, I believe that we will, in the future, most likely see DZS growing at similar growth rates.

Source: Quarterly Presentation

{kind=link}

Recent Guidance And Market Expectations

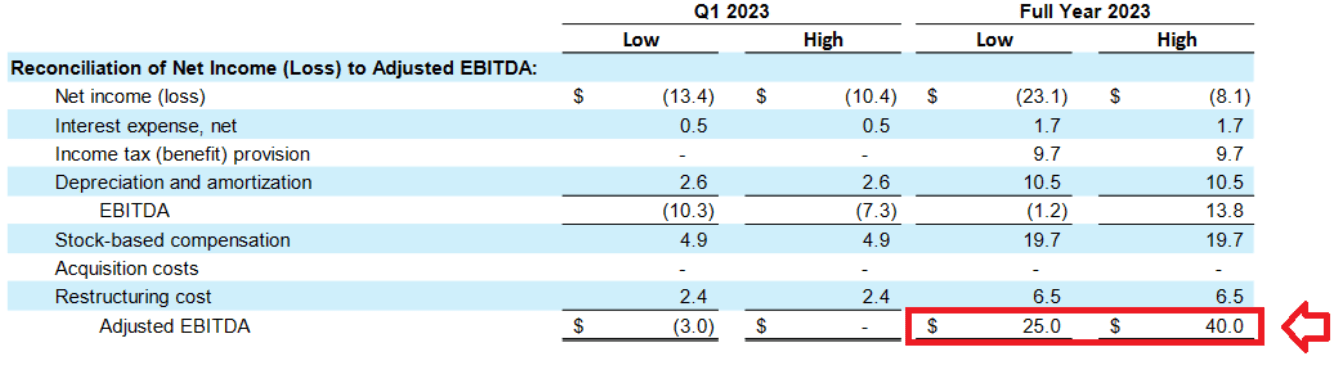

In the quarterly report for the quarter ended December 31, 2022, the company noted its expectations for 2023. Adjusted EBITDA was expected to be close to $25-$40 million, with stock-based compensation of $19.7 million and $6.5 million in restructuring costs. In June, 2023, management lowered its expectations for 2023, which seems to explain the recent stock price decline.

{kind=link}

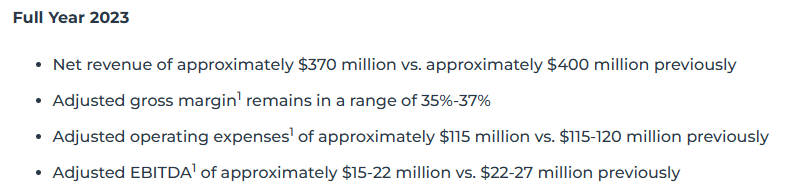

The new guidance included full year 2023 net revenue of $370 million, adjusted gross margin of 35%-37%, adjusted operating expenses of $115 million, and adjusted EBITDA of about $15-$22 million. In my view, the new expectations do not seem to explain well the decline in the stock price. The company noted that DZS would not deliver up to $40 million in EBITDA, but close to $22 million.

Source: DZS to Restate First Quarter 2023 Financial Statements

{kind=link}

The stock price declined from $7 per share to close to $4 per share. We are talking about a decrease of close to 42% in the stock price, which I believe is too much. Even if the EBITDA does not grow that much in 2023, in the future, investors may enjoy sales growth and EBITDA growth to justify $6, $7, and even $8.1 per share.

It is also worth noting that investment analysts are expecting net sales growth, EBITDA growth, and positive FCF in 2024. I believe that market analysts are a bit more pessimistic than DZS for 2023, however they believe that 2024 could be a great year for the company. In my view, the most interesting factor is the FCF. If more investors learn about the FCF growth for 2024, the demand for the stock would most likely increase.

Source: Marketscreener.com

Balance Sheet

I did not appreciate the recent balance sheet reported for the quarter ended March 31, 2023. It may also help explain the recent decrease in the stock price. Cash in hand, accounts receivable, inventories, and the total amount of intangibles decreased. At the same time, the total amount of short term debt increased. This is not the balance sheet that I would expect from a company that seems to be growing at a very decent pace. I hope that things will get better in 2024 as soon as investors see the FCF turning positive.

The list of assets included cash and cash equivalents worth $28 million, accounts receivable worth $141 million, other receivables of close to $21 million, inventories worth $69 million, and current assets of about $274 million. Besides, with property, plant, and equipment worth $7 million, goodwill stood at $19 million, with intangible assets worth $30 million and total assets of $360 million. The asset/liability ratio stands at about 1.5x, so I would say that the balance sheet stands quite stable even if there are lower assets than in 2022.

Source: 10-Q

Liabilities include accounts payable worth $107 million, short-term debt close to $16 million, current portion of long-term debt worth $23 million, and total current liabilities of $202 million. Total current liabilities are lower than the total amount of current assets, so I believe that there are no liquidity issues. Contract liabilities stood at $6 million, with operating lease liabilities of $10 million, pension liabilities of $11 million, and total liabilities worth close to $233 million.

Source: 10-Q

DCF Model

In my new DCF model, I included some reduction in the earnings of 2023 and some lower net sales, however I incorporated new information from the last quarterly report.

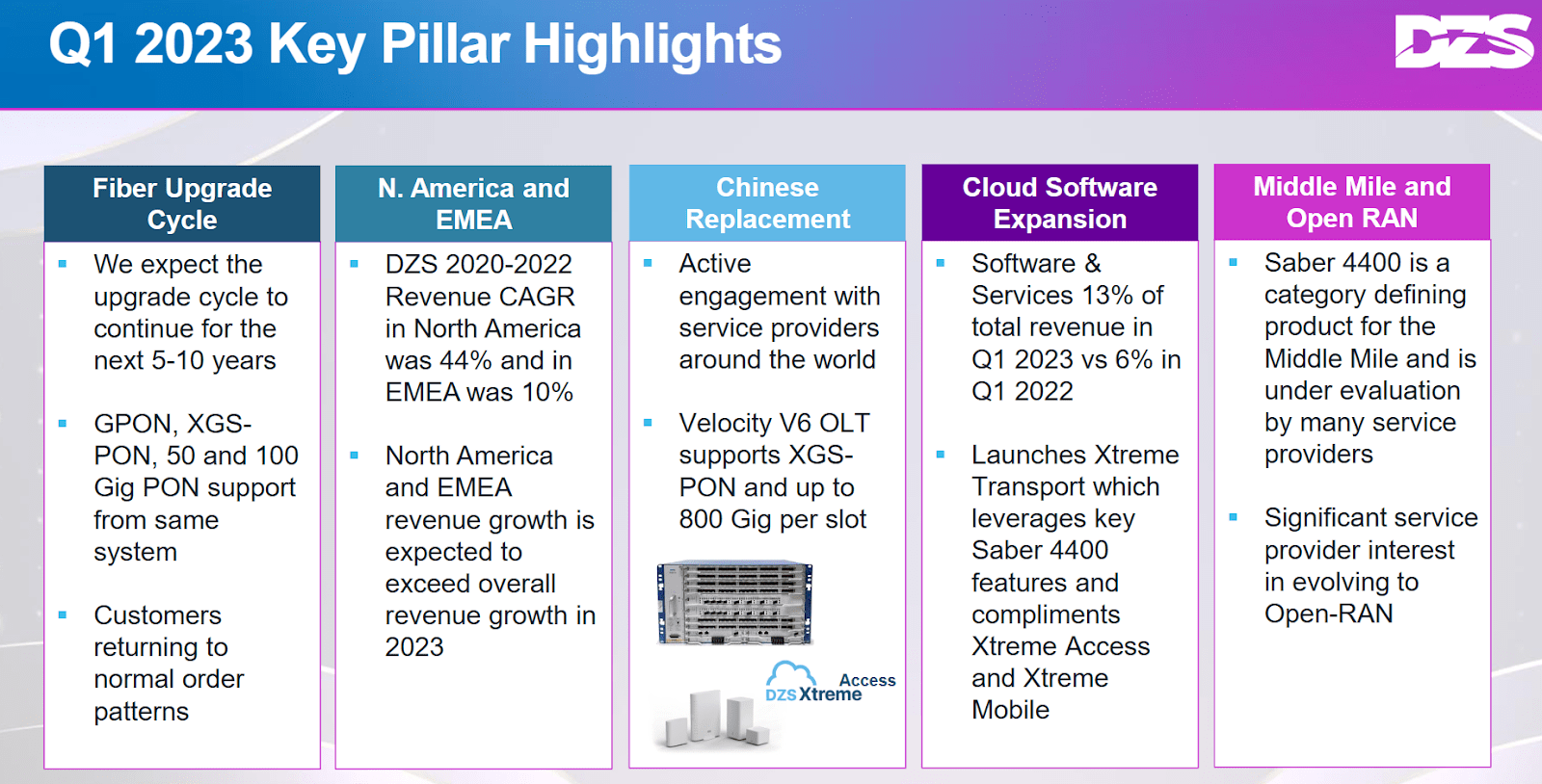

First, in my view, the Fiber Upgrade Cycle, which is expected to continue for the next 5-10 years, and customers returning to normal order patterns could have a beneficial effect on future FCF growth.

Source: Quarterly Presentation

Besides, I believe that the launches of Xtreme Transport, Xtreme Access, and Xtreme Mobile as well as further expansion of the cloud software and services will most likely be beneficial for future net sales. Finally, I would be expecting further service provider interest in evolving Open-Ran in the coming years. Management commented these highlights in the most recent quarterly report presentation.

Source: Quarterly Presentation

{kind=link}

In the last quarterly report, DZS noted that the increase in SG&A was due to strategic hiring decisions and initiatives to accelerate growth and capture market share. Under my financial model, I assumed that these additional expenses seen in the last quarter will successfully accelerate business growth.

Selling, marketing, general and administrative expenses increased by 39.7% to $24.8 million for the three months ended March 31, 2023 compared to $17.7 million for the three months ended March 31, 2022. The increase was primarily due to higher stock-based compensation and strategic hiring decisions across sales and administration with the intent to accelerate growth and capture market share. Source: 10-Q

Considering the growth of the markets reported by DZS, my DCF model included median income growth of close to 12% from 2024 to 2033 and an average income growth of 16%. I believe that my numbers are quite conservative.

{kind=link}

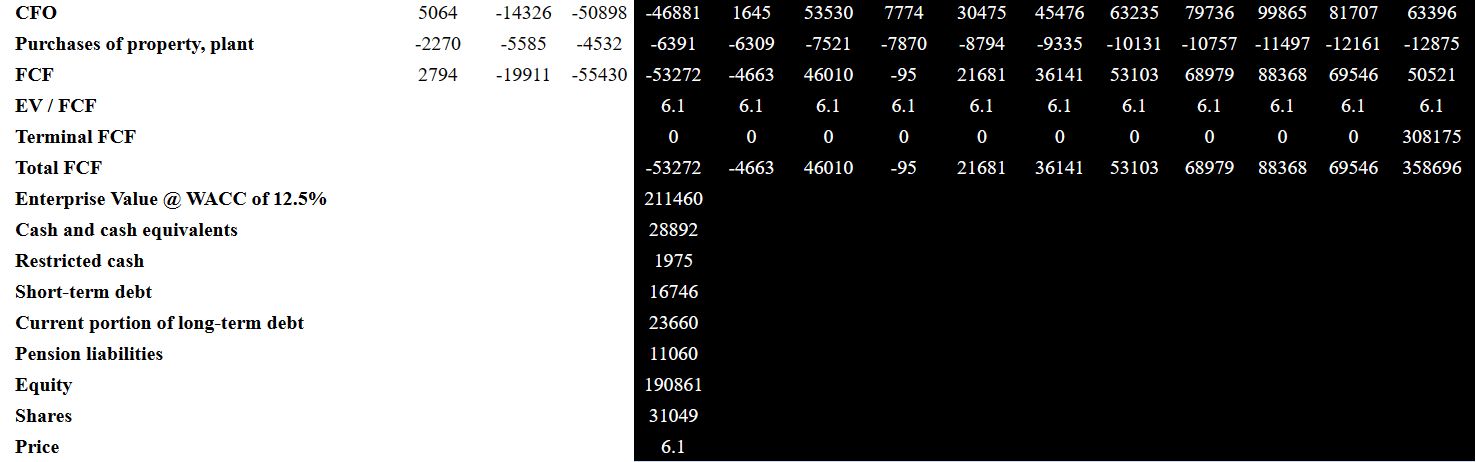

My new financial model include 2033 net income close to $1.6 million, depreciation and amortization of about $5 million, stock-based compensation of about $7 million, accounts receivable worth -$6 million, other changes in receivable of -$45 million, and inventories close to $39 million. Besides, with contract assets close to $5 million, prepaid expenses and other assets of -$2 million, and changes in accounts payable close to $17 million, 2033 CFO would be $63 million.

Source: DCF Model

If we also assume 2033 capex of -$13 million, the implied 2033 FCF would be about $50 million. With an EV/FCF multiple of 6.1x and a WACC of 12.5%, the implied enterprise value would be close to $211 million. Note that my EV/FCF multiple and the WACC are a bit lower than that in my previous article. I wanted to reflect the decline in profitability expected by management.

If we add cash and cash equivalents of about $28 million, restricted cash close to $1.9 million, short-term debt of $16 million, current portion of long-term debt of $23 million, and pension liabilities of $11 million, equity would be $190 million, and the fair price would be $6.1 per share.

{kind=link}

Risks

Considering the recent information given in the last quarter about restructuring, I would be worried about some of these operations not being conducted successfully. If DZS loses some key parts of the organization, or key members leave the company, I believe that future revenue growth may be lower than expected. Shareholders may want to have a look at the following lines about the most recent corporate decisions.

Restructuring and other charges for the three months ended March 31, 2023 primarily related to the strategic decision to outsource manufacturing from the Company's Seminole, Florida facility to Fabrinet, for which the Company recorded $3.5 million of such charges. The Company also included in restructuring and other charges approximately $0.3 million of facility costs related to impaired facilities and $0.4 million of non-capitalizable implementation costs related to replacement of the Company's legacy enterprise resource planning and reporting software. Restructuring and other charges for the three months ended March 31, 2022 related primarily to the transition DZS GmbH and Optelian to sales and research and development centers, for which the Company recorded $0.4 million of such charges. Source: 10-Q

In the last quarterly report, the company also noted that DZS may have to issue new securities or reduce the number of products offered to clients. In both cases, I believe that the market would take these decisions very badly. An increase in the share count could lead to lower fair price, which may bring the stock price down in the long term.

In addition, if necessary, we may leverage our Revolving Credit Facility or issue debt or equity securities. We may also rationalize the number of products we sell, adjust our manufacturing footprint, and reduce our operations in low margin regions, including reductions in headcount. Source: 10-Q

Besides, it is also worth noting that supply chain disruptions, increases in production costs driven by inflation, shortage of semiconductors, or lack of components would be very detrimental for future income statements. Management commented on these risks in the last annual report.

If our vendors for product components are unable to meet our cost, quality, supply and transportation requirements, continue to remain financially viable or fulfill their contractual commitments and obligations, we could experience disruption in our supply chain, including shortages in supply or increases in production costs, which would materially adversely affect our results of operations. The current worldwide shortage of semiconductors and continued inflation may exacerbate these risks. Source: 10-K

Conclusion

DZS delivered significant quarterly cloud software and services sales growth, and expects further sales growth in 2023 and in the future. Besides, I believe that the launches of Xtreme Transport, Xtreme Access, and Xtreme Mobile as well as the Fiber Upgrade Cycle will most likely serve as catalysts for future sales growth. Even considering the decrease in guidance for 2023 as well as the risks from failed restructuring or supply chain, in my view, the stock price could trade higher.

For further details see:

DZS: Impressive Cloud Software Quarterly Growth, Lower Guidance, And Undervalued