ENAKF - E.ON: An Energy Giant Worth Keeping Going Into Q3 2023

2023-11-04 04:46:00 ET

Summary

- E.ON is releasing third quarter results in a week or so - but a question of whether there is a valuation-related upside to investing prior to the release justifies an article update.

- I previously had a "HOLD" rating on the company and sold some of my holdings at a profit.

- I believe that E.ON is currently fully valued and recommend considering alternative investments, such as Enel. Enel is my current largest utility investment.

Dear readers/followers,

In about a week, it's time for the company E.ON (EONGY) to deliver its third quarter results. If you recall my last time on the business, I was at a "HOLD" back in June of 2023. This was one of my first rating changes on E.ON that I've done, ever since being positive for quite some time. I even sold significant amounts of my holdings in the company at a very solid and juicy profit.

I'm a big fan of diversifying portfolios with utility companies because they can provide stability during market volatility, as they offer safer cash flows due to their regulated nature. That's why large amounts of capital in my portfolios are invested in utilities. E.ON has delivered some of these very strong returns, but its valuation when I last wrote about the company was high, prompting a reevaluation of its investment potential.

Here is the RoR since that time.

Seeking Alpha E.ON (Seeking Alpha)

My rating change was therefore a sound one, at least in the few months we can see here. My last coverage on E.ON can be found in this article .

One reader asked me if it was worth, specifically, buying E.ON before the earnings announcement given where the company might go. I will do my best to answer this question, and also see where the company might go from here.

E.ON - A lot to like, just not the price when it goes above a certain level

I remind you that my first article on E.ON was when the company was incredibly undervalued - and I bought it. In fact, I bought very deeply at the time, adding a significant and very nice yield position to my already good investment portfolio with other utilities.

However, E.ON was not, nor is not currently my most significant investment in a utility. That honor goes to Enel (ENLAY). This Italian stalwart, most of which I bought below €5/share has generated significantly market-beating returns while paying out impressive amounts of cash, enabling further investment. While E.ON has annualized over 52% since my article in late October last year alone, that's also as high as I believed when I sold, the company could realistically go given the market environment we're going into and are currently in.

Enel still has a longer way to run.

E.ON's latest results that I'm covering here were good, and the company has gone a long way to deliver clarity and quality in its investment thesis.

Remember - E.ON is two segments; the generation, and customer solutions/retail business

For the last period, the company boosted both of these segments in terms of guidance. E.ON now expects an annual EBITDA on a group level of upwards of €8.8B, with a net income that could come in just below €3B if it edges towards the upper edge of the range.

The company has high hopes for itself, justifiably so, as the "green transition business." (Source: E.ON 1H23 )

{kind=link}

Between the amount of money it means to invest, and the current set of policies we see in Europe, I do not see that the company is at risk of significantly falling short of many of these targets - and the CapEx deployment is going according to plan.

The company's 1H was a very strong set of performances, which has resulted in a downturn only because of what I see as a rising interest rate environment and significant premium in the risk-free rates, which is weighing down things like utilities. The actual results for E.ON were more even than solid, with EPS more than doubling YoY, and EBITDA up more than 50%. (Source: E.ON 1H23)

E.ON IR (E.ON IR)

What else?

Guidance updates - and dividend updates.

Least among those is that the 2027E targets, including this company's dividend policy, are now fully confirmed. That's also part of the "problem" we're seeing here, actually. Investors now know they're not getting "more" than what is being announced here, and this is weighing things down quite a bit given how easy it now is to get a 5% yield safely or more. This obviously wasn't the case a year ago, but it is now.

EOAN, the native ticker that I invest in, now yields 4.55%. This is not bad, given the company is BBB, but it's also not "good", given that I can throw a rock and hit an attractively-priced preferential share with a 6-8%+ yield with similar safety.

This means that we now want capital appreciation potential.

And things there, at least if we're looking at the company's current forecast, are not looking especially bright. Why exactly is that?

Because the company is investing very heavily - pushing capital to work in attempts to grow, while also facing rising cost of capital numbers. Given that net income largely follows EBITDA here in these companies, and that we've yet to see a full-year result with the full impact of increased rates and cost of debt, I believe E.ON's growth rate will be less than the market expects.

I don't question the guidance upgrade, I also don't question the quality of the company. I don't question the confirmed dividend. The problem is that I invested in E.ON at over 6% yield in a market where a risk-free rate of 1.5% was considered good.

We're now investing at 4.5% in a market where 6-8% risk-free is considered standard if you go for prefs and at least 5% in an MMF. There's obviously going to be some valuation correction when this happens.

Honestly, I'm surprised the company hasn't dropped more than we've been seeing here.

The key performance drivers for 2023, including what's going to dictate 3Q, are organic RAB growth, re-dispatch costs in Germany, efficiencies, network loss recoveries in Sweden, and managing the lower volumes in CEE/Turkey - that's for the networks segments, at least. (Source: E.ON 1H23)

In solutions, we're seeing a tricky situation in the normalization of margins, though this is currently positive. Procurement efficiencies and business growth are also likely to deliver synergies and upswings in earnings and margins over time, and I expect we see business normalization in both the UK, NL, and other areas.

However, I also expect going into 3Q23, given the current macro, that we'll see an impact in the asset optimization margins, and despite the current EBITDA growth, which is 30% YoY from the networks segment alone, I don't see this sticking around over time.

The question I received was whether there are arguments why you should buy E.ON before the 3Q23 earnings. This would be the case if there are some major reasons to be positive for a blowout quarter. But that is not the case. The company is not going to be announcing dividend boosts, we're not going to be seeing massive earnings increases - it's a utility. The forward picture here is relatively clear. (Source: E.ON 1H23)

The company isn't massively cheap here either. It's not expensive but it's not cheap. If you recall my last positive article, my PT at the time was conservative and impacted €10.5/share.

Going into valuation, I'm not changing this - even in the case of an upswing in the 3Q23 results.

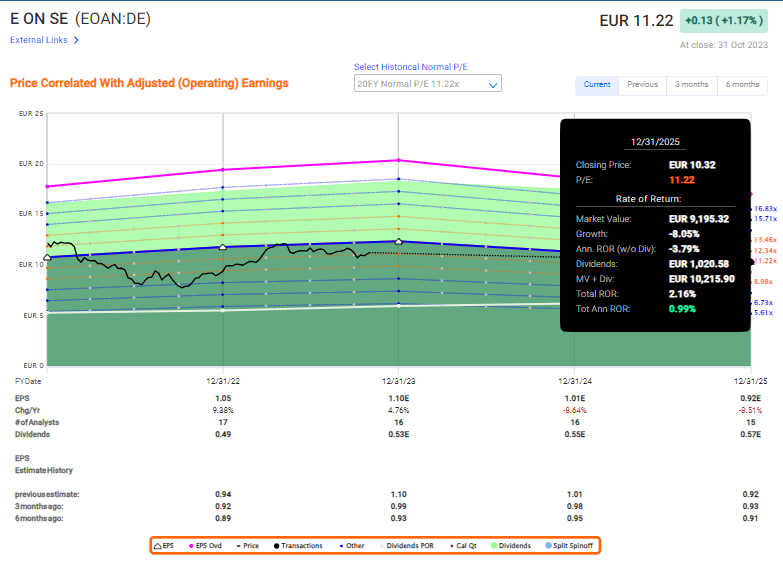

E.ON valuation - Even with a Good valuation, I'm not seeing an upside at €11.2/share.

So, if we were a year ago, I might change my valuation target here. But now, there's no reason for me to do so. 2023E is likely to be a good year - but beyond this year, I believe that investments are going to see the company's earnings on a comparative basis drop down at least a few percent on a YoY basis unless the company can find these efficiencies elsewhere. And the chance of the company doing this in an increased expense environment is, as I see it, not that likely.

The company here is at a blended P/E of 10.3x. If the average of 10-12x P/E is the multiple we're seeing here, which by the way is the 20-year average multiple (11x), then the upside we're seeing here is less than double digits.

And not just less than double digits , we're seeing less than even a single percent annualized upside.

{kind=link}

Are you starting to see why I am saying that the 3Q23 really doesn't matter here?

Even with outperformance, I do not see a significant upside for this company here. The yield is too low, and the forecasts at negative 5-6% for the next few years, this forecast comes at a 60-70% accuracy ratio (Source: FactSet), which means that the "path" to a 15% annualized upside is as follows:

You have to forecast E.ON a 6-year average of 13.5x, and then still go up to 16x P/E, in order to get an above-15% annualized upside , even with the dividend included here.

And a multi-utility trading at 16x P/E which would imply a yield of below 4% should be compared to something like Enel.

Enel, at this time, trades at a P/E of just below 10x, yielding 7.18x, and unlike E.ON is expected to grow 6-7% per year, not decline. Enel also has a safe and confirmed dividend, and an accuracy of 60-70% historically. I've written about Enel previously, and my thesis still stands - read my latest coverage on the company here.

Even just on a 13.5x P/E, the company has an upside of 26.4% annually with dividends included. This is a materially better upside and thesis than E.ON can currently offer - and Enel is better-rated than E.ON, at BBB+.

This is why I am heavily invested in Enel, and why I am not heavily invested in E.ON at this time.

It's also why my response to my reader, who wanted this information, is that the company is not a "BUY" here before 3Q23, and likely not after 3Q23 either. The company is simply too expensive for the near-term forecasts - and I would say you shouldn't buy here.

There's no reason to do so since Enel exists.

Here is my thesis at this time.

Thesis

- E-ON is a market-leading energy company in Europe with some of the best and largest infrastructure networks in the continent. I have successfully invested in the company several times, meaning that I have significantly outperformed the market by investing in E.ON.

- The company is now fully valued for the potential headwinds the company is facing.

- E.ON is a "HOLD" now based on its valuation and a continued conservative PT of €10.5.

- I'm moving to "HOLD" and am starting to look at potential alternatives for investing and reinvesting. I'm not changing my price target here.

- Enel is a far better investment here and is my current choice in multi-utilities.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now a "HOLD" for me due to an unfavorable valuation.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

E.ON: An Energy Giant Worth Keeping Going Into Q3 2023