ESOCF - E.ON: Getting Too Expensive (Rating Change)

2023-06-25 04:59:50 ET

Summary

- Diversifying portfolios with utility companies can provide stability during market volatility, as they offer safer cash flows due to their regulated nature.

- E.ON has delivered strong returns, but its current valuation is high, prompting a reevaluation of its investment potential.

- Despite E.ON's solid financial position and growth prospects, risks such as rising interest rates, market volatility, and potential legislative changes warrant a cautious approach to investing in the company.

Dear readers/subscribers,

It's important to diversify your portfolio, I believe, in correlation to the stability you want to have in the face of market adversity/volatility - such as the one we are facing now. A key component for me in my portfolio has always been investments in utility companies. Utilities are some of the safest cash flows you can find due to their regulated nature and the structure/organization of their cash flows. While it's entirely possible for these companies to see declines or even dividend cuts, they are far less common than in other sectors.

At the same time, these companies don't have the growth potential other companies do. They are, for lack of a better word, bond-like investments.

My current largest position in any one utility is my investment in Enel ( OTCPK:ENLAY ). This Italian stalwart, most of which I bought below €5/share has generated significantly market-beating returns while paying out impressive amounts of cash, enabling further investment.

I'm positive about utilities - and in this article, I'm going to look at E.ON ( OTCPK:ENAKF ) and see what we have going for us with this company.

Is it a "BUY" here, what can we expect, and what do we want to see?

E.ON - The valuation is now high

My returns on E.ON have been very good. In the last article on the company posted, I held a positive stance on this utility, which inclusive of dividends has resulted in 18% RoR in less than 4 months at a time during which the S&P500 has returned about 5%. That's more than a 3x and is solid for my own goals. Since my article in October 2022, when I went "back in", the RoR looks like this.

Seeking Alpha E.ON RoR (Seeking Alpha)

As you might expect, I'm very pleased with a 4x RoR above the S&P500. But that is also why I am revisiting this investment here. The time has come for me to change my rating on E.ON, and consider trimming and potentially rotating this investment for more favorable investments in the sector or adjacent sectors. E.ON at 7.5x normalized was one thing, and it's a "BUY". E.ON at over 11-12x average weighted P/E, that's a different story altogether.

Let's recap what we have here and what we can expect over the next few years. The company reported full-year results in March, about 3 months back. Those results were excellent, and part of what drove the company even higher.

What I mean by excellent is that every single segment delivered at the top end of the guidance range.

{kind=link}

E.ON IR ( E.ON IR)

With total group EBITDA on an adjusted basis as well as Net income for the group, the results were even above the guidance range for the full year - beyond merely "good" results.

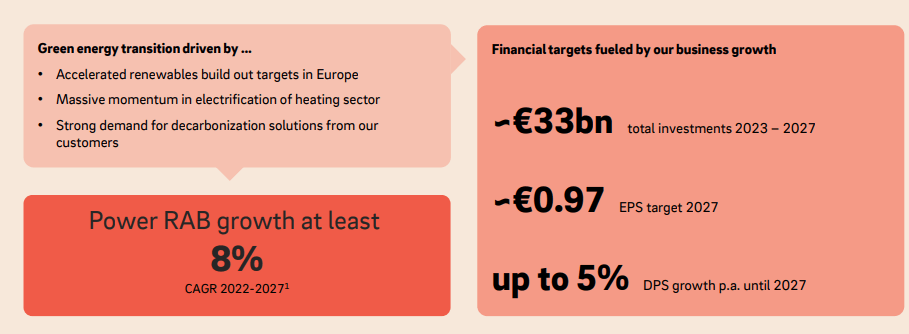

I want to remind you that E.ON, is the largest operator of mission-critical utility infrastructure in Western Europe. This includes being the largest supplier of electricity. To invest in E.ON, while some assume it to be risky, is to invest in a market leader. And that market leader is forecasting stability going forward, new investments, and good returns from an energy transition that's in full force.

{kind=link}

E.ON IR ( E.ON IR)

As I've done in previous articles, I'm going ahead and calling the company dividend "safe" here. There is the potential for a cut - there always is - but the company's official stance and forecast is an up to 5% payout growth per year until 2027. This implies that it won't be lowered.

If the company was cheaper, this would be very good news. But as it stands with today's share price, the yield is actually below 5%, which compared to my own YoC of over 7% is starting to look rather meager.

Forward growth is to be brought by the green growth acceleration. 2022 was a very good example of how E.ON is growing in a volatile macro. The company's negatives for the year came in the form of milder weather, which leads to lower volumes in the energy networks segment, as well as increasing costs for network losses. However, this is in turn offset by higher organic RAB growth and the ongoing realization of organizational synergies that are being delivered across the entire company.

Customer solutions saw similar negatives, but once again, restructuring benefits are starting to really show results. Despite all of the negatives last year, the company ended with a €170M higher EBITDA than 2021 the full year. The company also does not expect payment behavior/nonpayment to become an issue due to strong governmental support. Electricity/heat is not something you can go without, and the governments in the relevant areas know this. E.ON remains, as I view it, safe here - even if they have increased the allowances for what is considered "bad" debt.

However, this ratio is still less than 1% of the company's revenue - only 20 bps higher than in 2021.

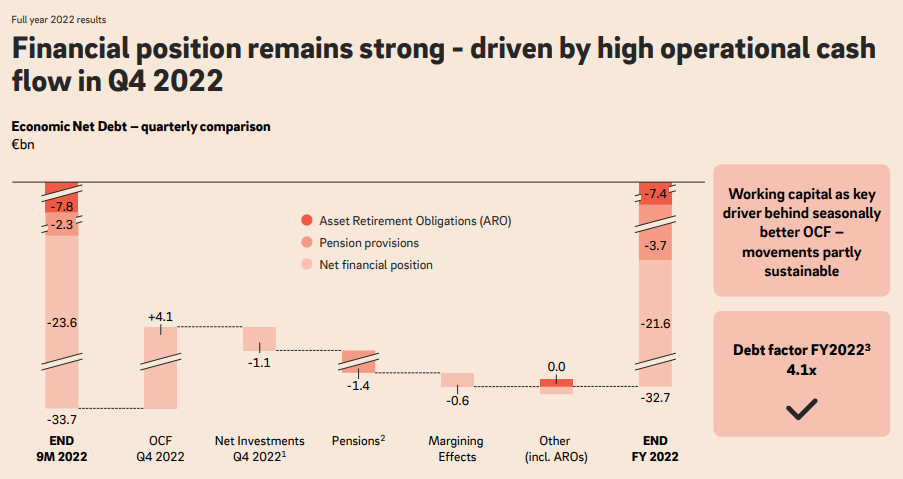

The company's financial position is very solid.

{kind=link}

E.ON IR ( E.ON IR)

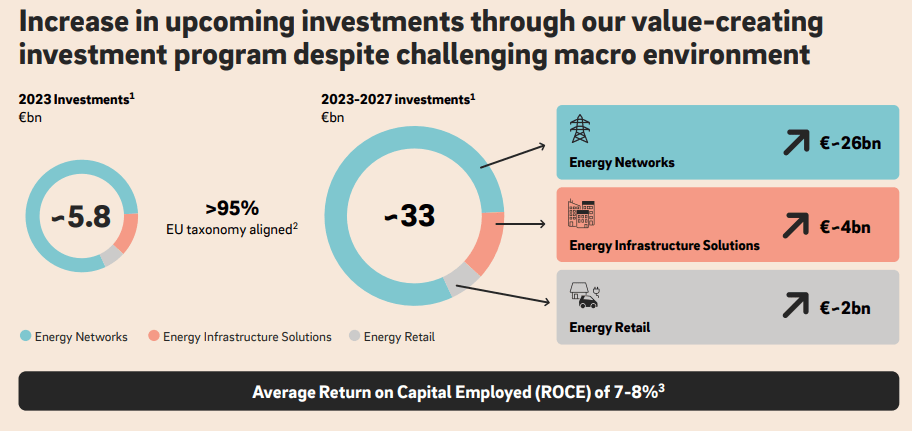

E.ON remains BBB rated, with a debt factor target of below 5x. E.ON foresees no earnings growth issues to continue to offset the growth in leverage from its strong investment targets. These investment targets, going forward, are as follows.

{kind=link}

E.ON IR ( E.ON IR)

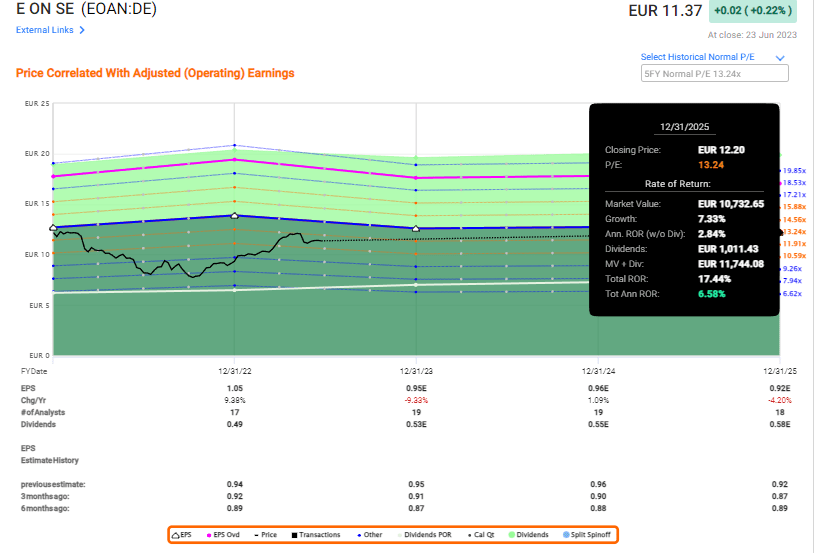

With the relevant ROCE, the company is mostly outperforming a realistic WACC, if only barely. The perhaps largest issue for the company is the rising interest rates - and these are not going anywhere. This raises the bar for what the company must make in order to achieve bottom-line growth. The company expects a 2027E EPS of close to a euro on a per-share.

Key performance drivers going forward are continued organic RAB growth, efficiencies, better recovery of losses, growth in the solutions-based business, and transformation in markets that have not yet seen the impressive transformation seen in others - such as the UK, Romania, and others. For the Energy Infrastructure, expect organic growth from new projects, as well as upside from asset optimization.

The problem I'm somewhat having with this is as follows - I believe the dividend won't be cut lower, and may even follow closely that 5% per share and per year growth. However, to guide for any sort of RAB certainty in growth, or any sort of certainty at all in the energy or utility markets is a bit of a leap. That's why I only invest in utilities when they are cheap, at this time. Even if the company is good, the sheer volatility from European macro, including the Russo/Ukrainian war means we could be in a vastly different situation than we thought. This volatility is on full display in analyst forecasts, with an accuracy of less than 35% (excluding positive beats) for a 1-year basis with a 10% margin of error. We only have to go back to 2016 to find a more than 35% analyst EPS miss.

I don't want to give the impression that E.ON is not being cautious about guidance and targets - because they are. But there are a lot of positive one-offs and synergy assumptions baked in. The company for 2023 is assuming that they're working with the 3Q and 4Q margin levels for 2022 - while this is possible, those are also results from a record year. The company officially does not assume an end to the energy crisis in 2023.

We're also not making any allowances for sudden and potentially unexpected legislative bills or changes, such as the one coming out of Germany in conjunction with 1Q. Such moves can certainly impact E.ON negatively as well.

The combination of all of these risks, and the fact that we're in an environment where governments will be required to protect customer interests and bills above the profits of utilities leads me to take a generally cautious stance on these investments - and I would not go overboard in my targets.

This leads me to valuation.

E.ON Valuation - We're reaching an inflection point, and it's time to change the rating

If you recall my last article, my PT at the time was conservative and impacted €10.5/share.

I am not changing my PT as of this article. This makes E.ON a "HOLD".

The reason I am not changing my PT is, above all, the risks I mentioned above. However, I can illustrate to you the case I see for E.ON if things even go less than expected - because FactSet analyses/targets happen to mirror my own assumptions for the downside in E.ON.

If we see any sort of downside, and even assuming a 12-13x P/E valuation, which is the average for this utility, then you're looking at below-market potential RoR.

{kind=link}

E.ON Forecast (F.A.S.T Graphs)

And that's inclusive of dividends. Note the RoR without dividends. Do I believe these forecasts are likely? Obviously, other analysts have other forecasts that they are working with. A quick glance at the S&P Global analyst averages tells us they begin at €6.6/share (oh, how I'd love to see the assumptions for that analyst) and up to €14/share (very positive, but not insane if basically, everything turns out solid gold for E.ON). The average is now €12.17. That's up from €10.4 back in October when I made my buys and established my PT.

See any patterns here?

Out of the 20 analysts following the company, we're now down to 4 "BUY" and 1 "SELL" - with the remaining at a mix of "HOLD" or "Underperform" or similar stances. The change to me is very clear here, and it mirrors my own sentiment change. The fact is, that at today's valuation and assumption, a clear upside for the company requires macro to go the company's way - and I want to be open to the risk that it may not. If it does not, and the market recognizes this, you're in for non-market beating RoR.

This is not the case for all utilities. Despite a steep climb for my largest position, Enel, there is plenty of upside in that utility which still trades below E.ON and offers a 6.6% yield. Enel is also higher-rated with a BBB+, while not having exactly the same size as E.ON. However, its mix and plans mean that I view the upside in Enel as far more likely than I view the upside in E.ON at this valuation.

And it is for that reason, that I am changing my thesis and my sentiment for this company.

Here is my updated thesis for E.ON - not a change in PT, but a change in rating.

Thesis

- E-ON is a market-leading energy company in Europe with some of the best and largest infrastructure networks in the continent. I have successfully invested in the company several times, meaning that I have significantly outperformed the market by investing in E.ON

- The company is now fully valued for the potential headwinds the company is facing.

- E.ON is a "HOLD" now based on its valuation and a continued conservative PT of €10.5

- I'm moving to "HOLD" and am starting to look at potential alternatives for investing and reinvesting. I'm not changing my price target here

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now a "HOLD" for me due to an unfavorable valuation.

For further details see:

E.ON: Getting Too Expensive (Rating Change)