EONGY - E.ON Has And Will Likely Go Higher After 30%+ RoR

Summary

- I argue that my stance on E.ON has been mostly correct for the longer term, and I've been successfully targeting "BUY" opportunities for the business for some time.

- Since my last article, the company has outperformed the market by a factor of almost 6x. My watchlist position has expanded to a good-sized stake.

- I'll revisit my stance for E.ON for 2023 here, and my stance is positive.

Dear readers/followers,

As I've alluded to before when writing about E.ON (EONGY), the company's dividend remains safe by its own words and estimates. The recent happenings in macro, with Ukraine and Russia, and the way the company's incomes have developed, do not change this thesis in the least. The company may have had a few challenging years - and we may even see some more issues, but at a good price, this utility is a "BUY".

Let's look at what we have here in terms of valuation, targets, and forecasts for the next few years.

E.ON for 2023 - a great utility

So, the returns since my last article have been fairly stellar - even if that was from a dip. I loaded up more, and my position is back up to around 2% of the total here.

Seeking Alpha E.ON article (Seeking Alpha)

That also means that we're back to around the same level we were back when I was "BUY"ing the company earlier.

In the end, utility investing is a fairly straightforward venture. The companies are typically extremely safe, backed by regulated cash flows based on operations that are non-optional. Everyone needs heat and electricity. The one thing that can happen to a company like this, as evidenced by something like Pinnacle West (PNW), is when a regulator beats down on the rate case - and this does happen. At worst, the company needs to cut its dividend, which for a utility massively impacts the share price - since growth is usually fairly hard to come by.

Now, E.ON's basics are great. It has distribution, and customer solutions with 50M customers across Europe mixed with that €35B asset base (regulated), together with a fully functional upstream power generation segment.

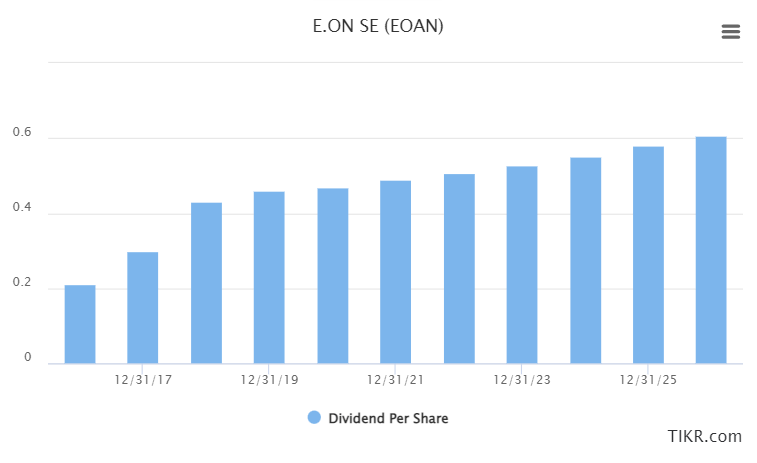

The dividend, even if things are up 30%, is still fairly good - and forecasts for how that dividend is going to grow is positive.

{kind=link}

This puts the current yield at roughly 5% as of the time of writing this article. It's not the best yield in the space - and I own more of a stake in Enel (ENLAY) than I do in E.ON in part because of this. Enel has much the same upside, but with a better yield than E.ON. Where E.ON wins over Enel is the safety and resilience of its operations. Enel, and other peers, are found in more volatile geographies, whereas E.ON's asset base is more Northern-European, which enjoys more stability, as well as a higher quality, more invested grid/infrastructure.

E.ON as a business has the ability to generate upwards of €8B worth of EBITDA in a year, of which around €2.5B goes to net income. The combination of regulated and infrastructure businesses is an attractive one, and the company's core investment upsides - the dividend growth, the state of the company's assets, and its 5-year pathway - remain intact.

The way that the dividend is confirmed is with a 5% annual dividend growth rate until 2026E - and this is the company's own guidance, not analyst estimates. The drawback of this is obviously that you're not getting more than this growth - or at least the chance of this happening is quite low, and with the way inflation is wreaking havoc, a 5% annual DGR might not be enough to offset some of the cost increases and inflation we're seeing.

That being said, company plans and ambitions are very solid.

E.ON IR (E.ON IR)

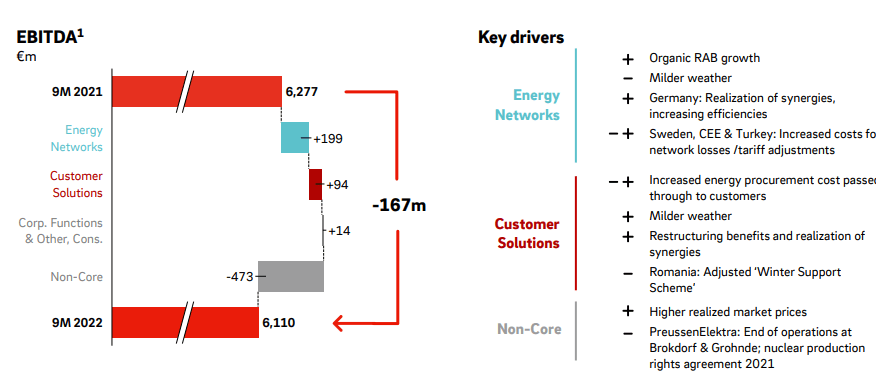

We have 9M22 results, and these results are part of the reason why the company has been outperforming like it has for the past couple of months. E.ON delivered solid results in all core operations. E.ON is on track to yet again almost crack €7B in core EBITDA, while also cutting debt down to potentially below 5x. E.ON is still BBB/Baa-rated.

Some investors believed the company would see volatility related to the core business and how it was due to milder weather, cost increases, support schemes, and the like. But recovery has been good. While we're not yet at 2021 numbers, the 9M22 results are now above €6B in EBITDA.

{kind=link}

The company's financial position remains absolutely stellar, despite what would be expected to be worried in payment behaviors due to very expensive energy bills. However, in every single one of the company's main markets, government intervention measures have worked against negative development in payment behavior, to which the company has not impaired or provisioned more than €100M for bad debt on a YoY basis. This is less than 0.7% of the company's revenue.

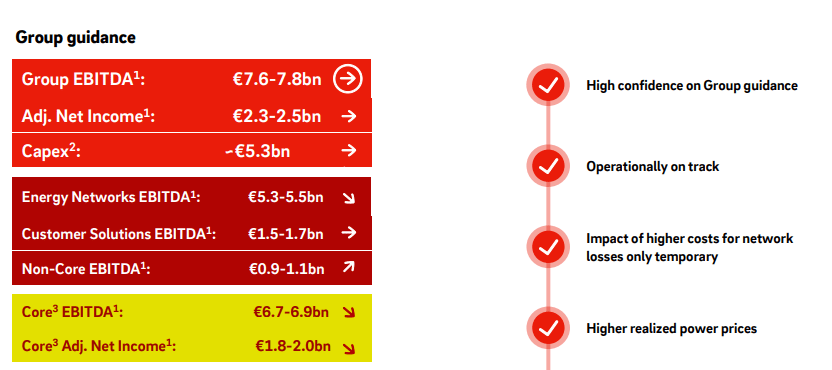

Guidance for 2022 is rock-solid.

{kind=link}

This guidance is also part of the 2026E that the company is following, which calls for a close to €8B annual EBITDA, representing that same 4-5% CAGR which we see in the dividend as well. ROCE for the company in the current target range is expected at around 7-8%, and no improvements in the credit rating is expected.

The underlying reasons for these improvements are fairly simple. Organic RAB growth in all segments, coupled with efficiencies in the German market and Swedish markets, including increasing the fixed prices in Sweden for tariffs and network losses (which the company is already in the process of doing). This is then combined with tariff adjustments in Germany, restructuring in the UK, and asset optimization in Energy infrastructure. The company's PreussenElektra will continue to see advantages from higher energy prices on the market, which given today's macro, is unlikely to go away at least until 2024-2025E.

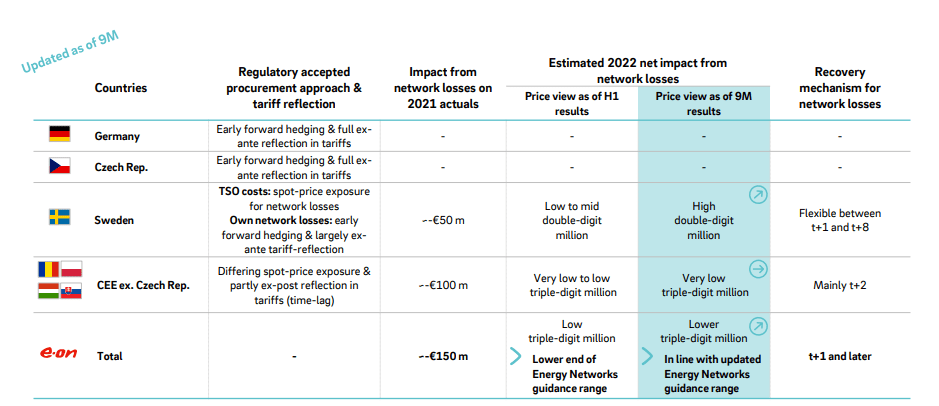

Network losses remain one of the company's major headwinds - and the company is working to address it in most of its markets.

{kind=link}

In the end, E.ON's fundamentals offset any risks and potential downtrends that we can really see as potentially possible. With no segment showing negative trends in terms of financials, it's no surprise that E.ON has been outperforming the market in terms of its share price.

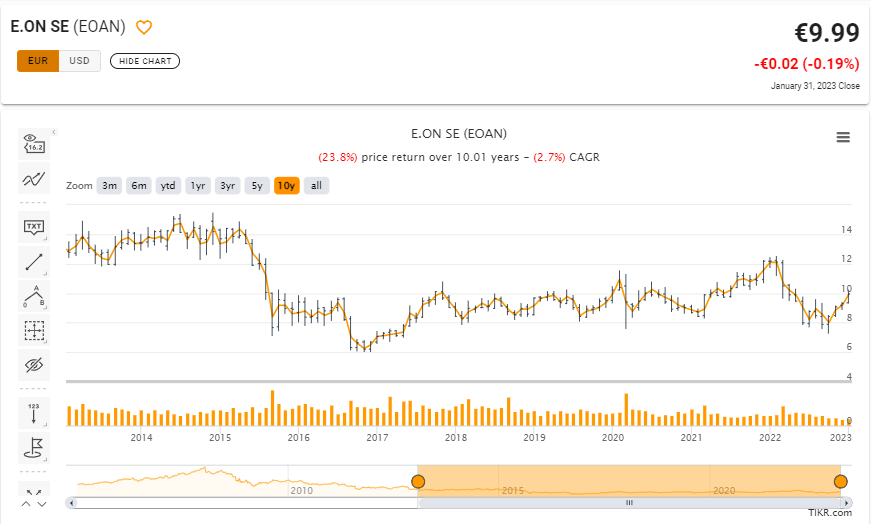

However, let's not mistake this for long-term outperformance, because that is not in the cards for the company. Take a look at the 10-year ROR for E.ON, even with dividends.

{kind=link}

So the company being a good buy at €8 is not the same as it being a good buy at above €11. The key with E.ON is keeping to very tight target ranges, and not straying once they climb too high.

Let's clarify this further in valuation.

E.ON Valuation

The company's valuation here is far from as good as it was only a few months back - but it's not yet "bad" enough to consider me changing my stance. Analyst averages here go from a €6.6 low to a €13.8/share high. Both the low and the high is far too extreme, either discounting much too heavily given the quality of assets available to us, or being too exuberant as to the quality of those assets.

My previous PT for E.ON was €10.5/share. I see no reason as of this article to change that particular thesis. When I last wrote on E.ON, the share price was around €8/share. The problem is that E.ON has plenty of competition on the market that's not exactly lacking quality. Engie (ENGIY) is a company I invest in, and that's perhaps the closest in terms of structure and assets - but Enel is the largest investment that's in the same sector that I own.

The company does have risks - and during 2021-2022, the company has been through a number of impairments - I've already heavily impaired my valuation targets for E.ON. For NAV, I've further impaired the stake in Nord Stream 1, adjusting my resulting NAV down to €10.4/share, which goes up to €10.5 when we look at how peers are being valued.

I actually fully expected E.ON's share price to go down further after my last article - the trend was very negative, but it pretty much shot up, despite estimates still being somewhat negative.

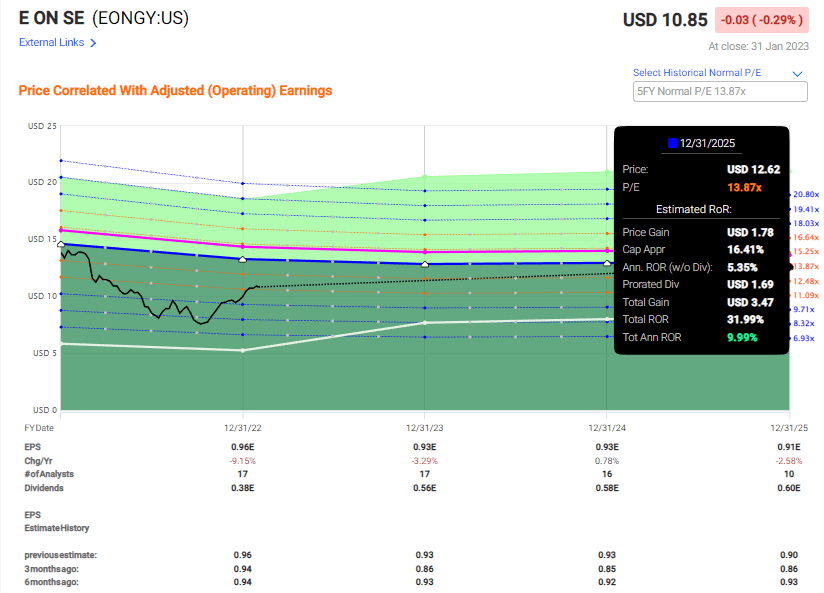

The way the company currently trades, it's fairly easy to see just how much things have deteriorated in terms of upside after a 30%+ RoR. Forecasting at 13-14x P/E, the upside is now less than 10% annually, even if just barely.

{kind=link}

So you're investing in a company that's in a downward trend - but unlike the last time in October, we're now 31% higher compared to back then, which really caps our upside. Back then, we were looking at almost 23% per year - now, much of that upside is realized.

We're not in a "downward streak" in terms of valuation here - but we are in terms of long-term earnings. This means we need to be very careful about how high we do "BUY" E.ON. Unlike some contributors and analysts which much higher price targets, I say that we're getting close to where we should stop buying the company - and for some investors with higher demands on returns, we've already reached that level and we may want to stop buying here.

One option to look at here would be Put options. E.ON is in a fairly good position where, during a negative day, you could lock in some decently attractive Puts at around €1 lower per share or so, which should yield annualized RoR of around 10-12% given that you pick conservative strikes and expirations.

I still view it as illegitimate and illogical to try and argue that E.ON is worth less than €10/share. It's not - almost no matter how bad things get. That means that any option that you manage to write below this, is technically where I would view the company as being discounted. There are risks, but we've already seen in multiple geographies including Scandinavia how E.ON is managing to recoup some of the losses through increases in fixed charges - where the company has already won multiple lawsuits against attempts from regulators to try and hinder it, in this case against the Swedish regulator.

For all of these reasons - the remaining undervaluation to a conservative 13-15x P/E, the underlying fundamentals including a BBB as well as a 4%+ yield, I view E.ON as a "BUY" here, even if the upside is no longer as high as 30-50% until 2025E here. Based on today's valuation, I would say that E.ON's upside is down to around 30% over a 2-3 year period, which represents a similar performance to what we saw since my last article. Now, whether this is an "outperformance" will of course depend on what the market does during those years. Still, I do believe the current volatility in the market coupled with volatile macro will mean a rough couple of years, which should see a double-digit performance as very decent.

However, I do believe it fair to say that there are utilities in Europe - and internationally - with a better upside.

Still, when it comes down to it - for 2023 and for this article, E.ON is a "BUY" with the following thesis.

Thesis

- The company is getting cheap even with the potential headwinds the company is facing. At these prices, things are getting cheap even when considering the headwinds and impairments we're seeing.

- E.ON is a "BUY" based on its valuation, which is now lower than €10/share with a conservative and impacted PT of €10.5.

- I'm buying more here, and I believe you should definitely take a closer look at E.ON here.

I'm not changing my price target, and I'm not changing my thesis yet - but it's not far from it at this point.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

E.ON is not cheap here, but it still fulfills every single one of my other criteria.

For further details see:

E.ON Has And Will Likely Go Higher After 30%+ RoR