ENAKF - E.ON: Investments Acceleration Will Likely Drive Earnings Growth

2023-03-17 11:14:00 ET

Summary

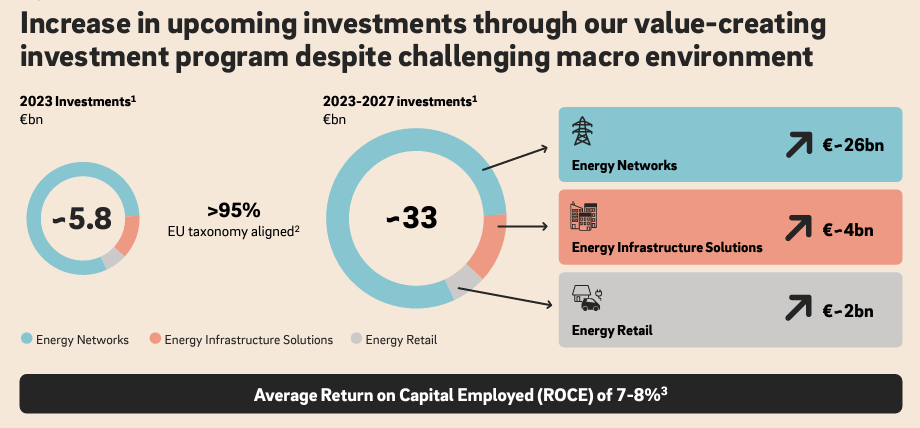

- Germany accelerates on a new hydrogen gas pipeline with Norway. E.ON increased its value-creating investment program by an additional €5 billion.

- By 2030, Germany wants to cut carbon emissions by 65% from 1990 levels.

- EBITDA growth profile is strongly supported by the network business.

- Lower debt, higher DPS, and so we confirm our buy rating.

In our E.ON's initiation of coverage (EONGY), we said: " being back at <€10 per share, we believe that it is a good entry time to start a position on the German player (with also a tasty dividend per share as a margin of safety) ". It was a good call, and since mid-May, E.ON was up by 8% at the stock price level, and including its dividend payment, our performance was up at a double-digit level. Aside from a valuation discount compared to its closest peers, here at the Lab, we positively view the higher investment program contribution for the EU energy transition. E.ON's CAPEX was primarily focused on new connections for renewable energy systems, and network infrastructure modernization.

{kind=link}

Mare Evidence Lab's previous publication

In 2022, we also analyzed E.ON's Russian exposure and its write-off recognized in equity among other non-operating income for the Nord Stream 1 pipeline. We reassured our followers by providing a follow-up note called Downside Risks are Already Priced In . Before analyzing the quarter results just released, it is important to report the following latest indication from the German Government that is fully in line with Mare Evidence Lab's long-term thesis. By 2030, Germany is targeting to reduce CO2 emissions by 65% from 1990 levels and achieve climate neutrality by 2045. Norway has set similar goals and is investing in offshore wind while developing facilities for carbon capture and storage. Germany which is the Eurozone's largest economy has also had to retool its energy policy since the Ukraine invasion and had to end its long-standing dependence on Russian gas. According to rumors, both countries said that would consider building a hydrogen gas pipeline linking the two nations. Gassco Sa, which works on pipelines is currently conducting a study to evaluate the feasibility of the Norway-Germany pipeline, and this spring 2023, we should have the first green light.

The link will likely initially carry blue hydrogen, which is produced by converting natural gas and capturing carbon emitted into the atmosphere. Subsequently, the new Norway offshore wind farms will in turn feed the pipeline allowing it access to a source of green hydrogen that will be produced using renewable energy. According to estimates by the German Energy Agency and E.ON, Germany needs around 66 terawatt hours of hydrogen by 2030. The government, for its part, aims to produce only 10 gigawatts domestically, which means that it will still depend heavily on imports. However, the German Government is ready to spend more than €10 billion under its clean energy subsidy program, which pushes the use of hydrogen and carbon capture as well as to finance B2C green activities (as already happened in Italy under a Real Estate program called 110% bonus).

E.ON higher CAPEX (E.ON Q4 and FY 2022 results presentation)

{kind=link}

Q4 and FY results

The German transmission provider, despite being penalized by a volatile macroeconomic environment, delivered a solid set of numbers. E.ON demonstrated its strength and the company's CEO Leonhard Birnbaum emphasized how : "decarbonization, the energy transition, and the expansion of infrastructure must be massively accelerated. For our business, this will mean big growth potential". Well, we are definitely not surprised by these comments. Growing energy uncertainty and EU support for the energy transition will provide additional relief to the company's current investors

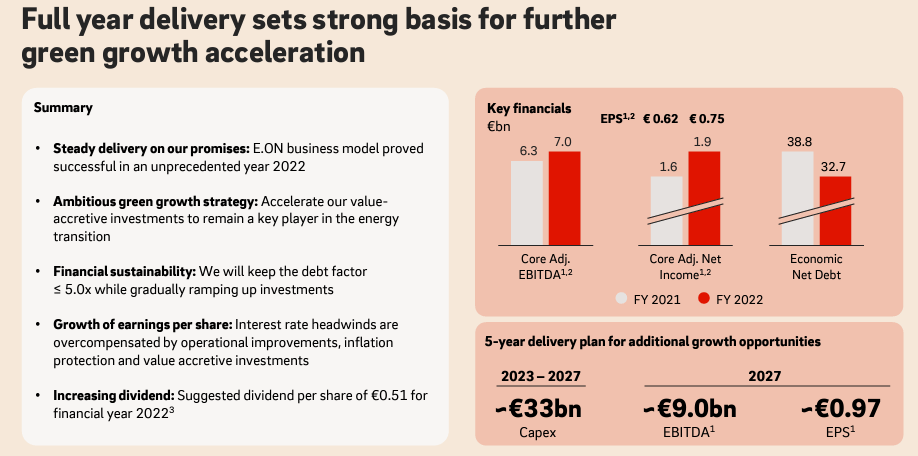

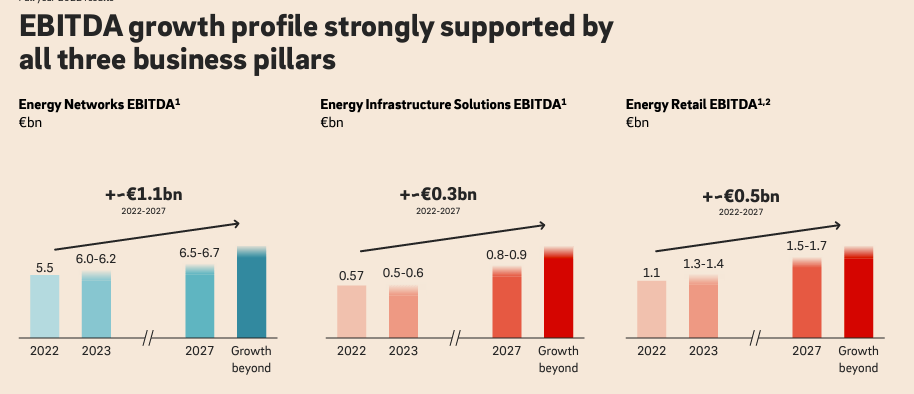

Having participated in the analyst call, here at the Lab, we see the accounts as a small positive take. The adj. EBITDA increased to €8.1 billion in 2022 was €170 million above the 2021 level (slightly above the company's forecast set at €7.6 to 7.8 billion). Looking at the division, the network business earnings reported the highest increase by about €470 million to €5.5 billion (in total support of our buy case recap). Important to note is the economic net debt evolution which declined significantly by almost €6 billion. This improvement was mainly due to strong operating cash flow generation as well as the higher interest rates that drove the pension provisions decline. The company also confirmed its dividend proposal of 51 cents per share with a target of +5% per year until 2027.

{kind=link}

E.ON financials in a Snap

2023-2027 Guidance

2023 guidance was slightly better than Wall Street's expectation. In detail, the German player guides a 2023 EBITDA at €7.8-8.0 billion, which is above Visible Alpha consensus estimates set at €7.53 billion. While E.ON's net profit guidance is more in line (€2.3-2.5 billion) and this can be explained by higher interest rate expenses. What is not in line with sell-side estimates is the company's strategic plan. In 2027, E.ON confirmed an EBITDA of €9.0 billion, and we believe that this will follow by an upgrade in the regulator asset-based (RAB). E.ON's key role in the energy transition will be supported by higher earnings growth. In our numbers, we already incorporated a target of 8% RAB growth over the five years compared to an implied market consensus of 6%. Here at the Lab, we believe that E.ON will see a network acceleration with renewable energy projects build-out and a positive momentum in the electrification of the heating sector supported by strong customer demand. This is also supported by a new CAPEX plan that was increased by more than €5 billion and now stands at over €33 billion until 2027.

{kind=link}

EBITDA growth profile

Valuation and Risks

Despite a plus 8% in E.ON stock price since our coverage, the company is still trading at a discount valuation versus its closest peers both on a P/E (6x vs 9x) as well as at the EV/EBITDA level. Debt was reduced and the dividend just increased (as expected by the plan). Therefore; our buy rating is then confirmed (€12 per share and $12.6 in ADR). Risks to our outperform rating include 1) higher interest rates; 2) an increase in bad debt provisions; 3) (again) a colder winter (due to the gas price evolution); 4) swings in 10-year German government bonds. You can also check our previous Q3 comments results here .

For further details see:

E.ON: Investments Acceleration Will Likely Drive Earnings Growth