ENAKF - E.ON Is On Track To Achieve Its 2027 Objectives

2023-08-22 12:05:53 ET

Summary

- E.ON's H1 financial figures were positive, with a 40% increase in adj. EBITDA and profit at €2.3 billion.

- The company now plans to increase CAPEX investments and upgrade its FY23 outlook.

- Higher estimates but also an increase in debt. We decided to maintain a neutral valuation.

Here at the Lab, we are pleased with E.ON's H1 financial figures (EONGY). We had a good rating update on the German transmission provider. Indeed, when we were overweighting the company (Fig below), we recorded a positive stock price performance of >30%, and then, following our consistency in the sector valuation, continued to imply a P/E of and an EV/EBITDA of 12x and 8x respectively, we maintained a €12 target price, moving the company to an equal weight valuation. Looking back, our rating downgrade was mainly due to a sector average of multiple valuations. Since then, despite a positive Q1 called " E.ON Continues Its Positive Earnings Trajectory ," the company's stock price declined, and performances were broadly flat, including the dividend payment.

{kind=link}

E.ON released an H1 preliminary financial results update in July-end and then disclosed the full report with the company's presentation last week. The two releases showed no changes in estimates, with H1 adjusted EBITDA and net profit of €5.7 and €2.3 billion. In the full report, the company included the net debt development, additional details on retail business, forward-looking strategy with an upgraded outlook. Therefore, today, we decided to return to E.ON analysis and update our internal estimates following solid Q2 results. As a reminder, the company was one of the largest integrated utilities in Europe. In 2016 and again in 2018, E.ON was transformed with an asset swap with German utility RWE. Currently, the company is predominantly a regulated network business (RAB) which ranges its activities mainly in its home country (Germany), Sweden, and Europe Eastern countries, thanks to its large customer base (approximately 50m accounts). Before commenting on its Q2 results, it is also essential to recap that E.ON had a challenging time with energy uncertainty development (here at the Lab, we covered also Uniper ); however, having said that we are believers that the EU will support the current energy revolution transition and this will likely provide relief to E.ON's financials. Within our coverage, we are neutral on Enagás ([[ENGGF]], [[ENGGY]]) and have a current buy with Snam (SNMRF).

Q2 results

Starting the company's words, we reported the following: " E.ON continues its growth path. " This is very similar to our previous publication title. In addition, the CEO confirmed that " the increasingly calming energy market environment had a positive impact on the Group's first-half results with Energy Networks and Customer Solutions segments which delivered a solid operating performance . Looking at the company's results, E.ON adj. EBITDA increased by 40% to €5.7 billion compared to last year. Aside from the recovery in the Customer Solutions division with an EBITDA that moved from €1.2 billion to €2.2 billion thanks to more efficient energy procurement, what is critical to report is the network business's remarkable performance. The division increased its results by approximately €800 million. Supportive CAPEX drove this in all regions with a focus on Germany. According to the P&L analysis, E.ON reported an adjusted net profit of €2.3 billion compared to €1.4 billion achieved last year.

E.ON H1 Financials in a Snap

Why are we still neutral?

What is critical to emphasize is the CEO's words in the Q&A call: "What is desired by Governments is one thing; what the company can finance is something else." With a regulatory-based remuneration system (RAB), there are rumors that the German government is willing to increase the cost of debt and equity for new investments. This positive sign goes in the right direction; however, this should also be performed for maintenance and existing CAPEX. This will provide the proper visibility for the E.ON rating upgrade. Here at the Lab, this is the current downside scenario holding back our over-weight valuation.

Following the solid Q2 results, we decided to update our internal model with the following:

-

Here at the Lab, we already increased E.ON network investment. This is due to a positive view on the German network that will step up new energy transition targets from 2027 onwards. According to our analysis and the company's financial target, this is the main area to drive a higher and growing EBITDA forecast. In Q1, the company invested more than €1 billion in energy infrastructure. However, in Q2, E.ON decided to increase its CAPEX new investments by €1.4 billion, bringing the total company's CAPEX to €2.4 billion. This represents an increase of 36% relative to the prior-year period and is above our internal guidance. On the back of E.ON's strategic plan with investments of approximately €33 billion in the period between 2023 and 2027, we now forecast 2023 CAPEX at €5.8 billion (in line with the company's updated projection);

- The full company's release includes the company's financial obligation development which moved to €37 billion from €35.1 billion in March-end. This was due to the company's dividend outflow and higher working capital requirements. Higher net debt is not coming as a surprise (this is seasonal as well). However, looking at the company's solid results thanks to a higher FCF, we now forecast a year-end debt of €34.5 billion (Fig 1);

- Given the lower energy price environment, we forecast revenue of €81 billion, which aligns with the company's new EBITDA guidance. Having increased the CAPEX, we arrive at a core operating profit of €5.2 billion for the current year;

- Supported by an FCF generation, we are leaving unchanged our DPS estimates of €0.55 and €0.55 per share for 2024 and 2025, respectively;

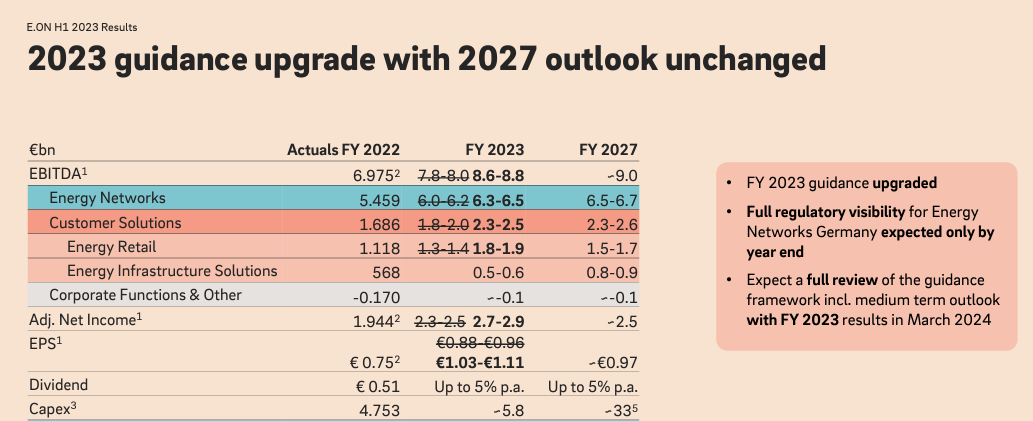

- E.ON also upgraded its FY23 outlook and now forecasts a 2023 EBITDA between €8.6 and €8.8 billion with a net profit of €2.7/2.9 billion. In addition, the company reaffirmed its Fiscal Year 2027 guidance to reach €9 and €2.5 billion in EBITDA and net income (Fig 2);

- On the positive side, we should recall two vital takeaways. The German regulator is more constructive in increasing investment return. This is a solid signal for E.ON, and we might anticipate a more productive outcome. Secondly, the company delivered retail solid margins in the 2023 first half. Despite the CFO explaining these changes as " one-offs for now ," we might anticipate a positive earnings contribution of €200-300 million annually in the foreseeable future. Retail higher margins are also recorded in peers such as our favorite Italian company: Enel;

- To support point 1) network investment might have room for acceleration. We believe that the current CAPEX omits RePowerEU and Germany's Easter Package . As supportive information, the German PV connection requests almost doubled from 2022 levels, and the positive momentum is not pausing.

{kind=link}

Fig 1

{kind=link}

Fig 2

Conclusion, valuation method, and risk statement

H1 financial figures and 2023 Fiscal Year end guidance were raised. In addition, E.ON confirmed its FY27 outlook and is on track to deliver its CAPEX promises. Despite the positive outlook here at the Lab, we continue to believe that E.ON is fairly priced. Having confirmed the left unchanged its FY 2027 outlook, we implied better 2023 results, but over the medium-term horizon, we maintained the company's organic growth trajectory of 3/5% EBITDA with a favorable course over 2027. Continuing to value the company with a P/E of 12x on twelve-month estimates, we slightly increased our target price from €12 to €12.5 per share. An attractive network return and the expected growth of the German electricity investment path support this. However, we decided to maintain a neutral rating thanks to the complete Energy Networks visibility. The German transmission provider almost reached our long-term multiple valuations and is trading at circa 8x EV/EBITDA. At the aggregate level, our target multiple is the average EV/EBITDA multiple of Enagas, Red Electrica Corporation, and Snam (trading at 8.08x, 8.13x, and 8.9x, respectively). An additional upside might come from a strategic plan update in March 2024. On a higher dividend yield opportunity (6.11% vs. E.ON at 4.66%) with more diversification from affiliates' dividends, we suggest checking Snam as the Best-In-Class Gas Transmission . Downside risks include commodities price development, generation margins, supply & demand evolution, taxation and remuneration system changes, worst government policy, and changes in interest rates with lower credit conditions. Any adverse change in these would modify our target price on E.ON stock.

{kind=link}

For further details see:

E.ON Is On Track To Achieve Its 2027 Objectives