EONGY - E.ON: Might Be Time To Get Back In? I Believe So

Summary

- I've been very picky about my favorite utilities ever since I managed to rotate E.ON at what I perceived to be a massive overvaluation earlier this year.

- I hold a small watchlist position - but I believe the time has come to revisit E.ON and its thesis in coming few years. It comes with problems and upsides.

- I hold my thesis on this BBB-rated utility and now consider it a "BUY" here.

Dear readers/followers,

Investing in E.ON ( OTCPK:EONGY ) over the next few years is going to be a tricky business. On the one hand, the dividend is safe. There is, to my mind, no doubting or discussing this due to the absolute clarity of the company's communications in this regard.

On the other hand, E.ON is in for a problematic couple of years that has seen the average PTs for the business sink in accordance with the perceived risks that we might be facing here - and there are of course risks.

Let's use this article to review E.ON and explain why I'm considering the company in the way that I am here.

Revisiting E.ON

Unfortunately, E.ON hasn't performed the best since my last article all the way back in May 2020. I sold my position earlier than that, and I did invest some small capital when the company dropped below €9 for the native, but other investments were more appealing at the time.

Now, however, it might be time to really re-evaluate the company's position in the buyable utility portion of my portfolio.

The base thesis for E.ON is very much intact.

{kind=link}

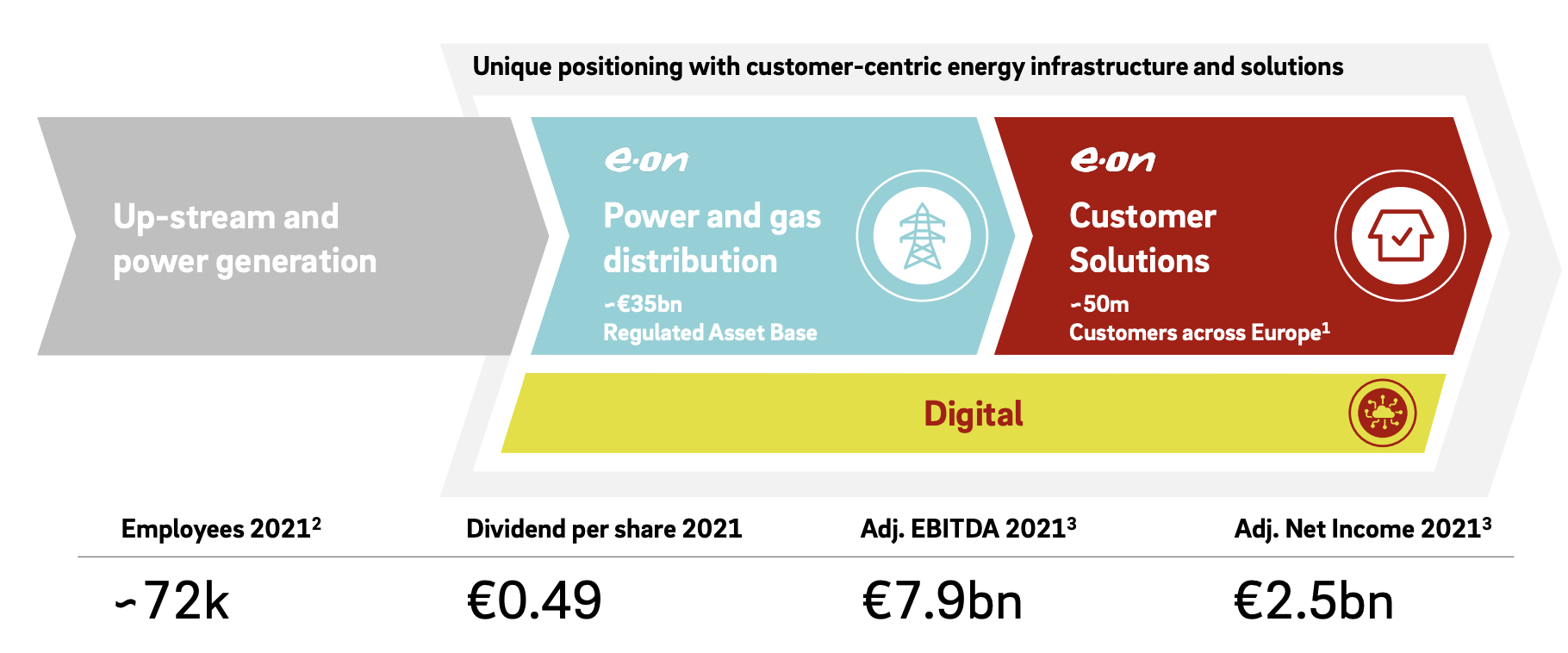

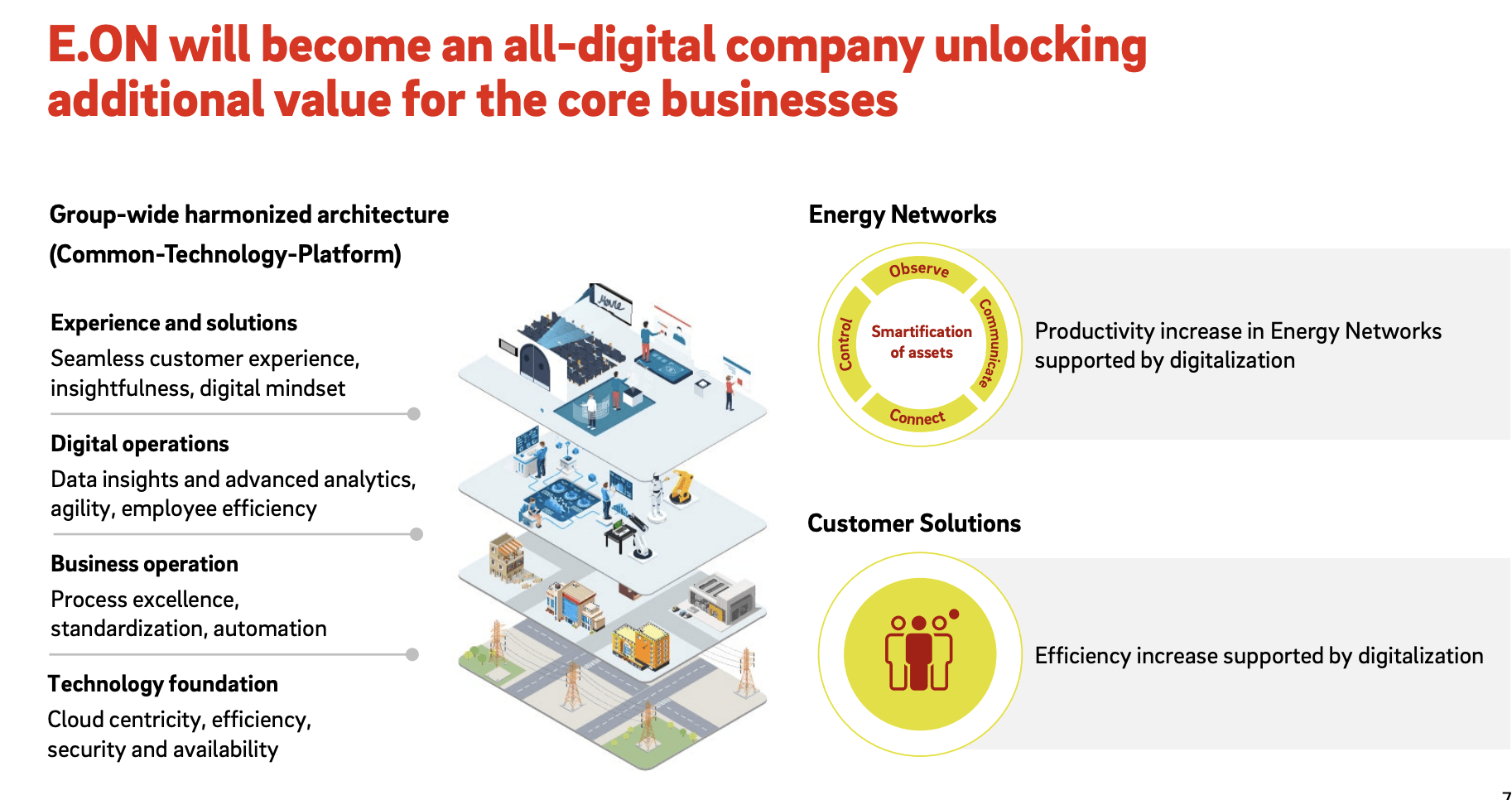

The combination of regulated and infrastructure businesses is an attractive one, and the company's core investment upsides - the dividend growth, the state of the company's assets, and its 5-year pathway - remain intact. Dividend growth is "confirmed" with a 5% DPS growth until 2026, and the company's core markets are growing in terms of demand. This comes from a combination of renewables, changing customer behavior and priorities, reinforcing and hardening existing network assets and digitalization.

{kind=link}

While Russia and the current macro have certainly de-railed the company's near-term target and appeal, more on that later, the current company estimates remain for a native core EBITDA for 2026E of €7.8B, around €1.6B higher than 2021.

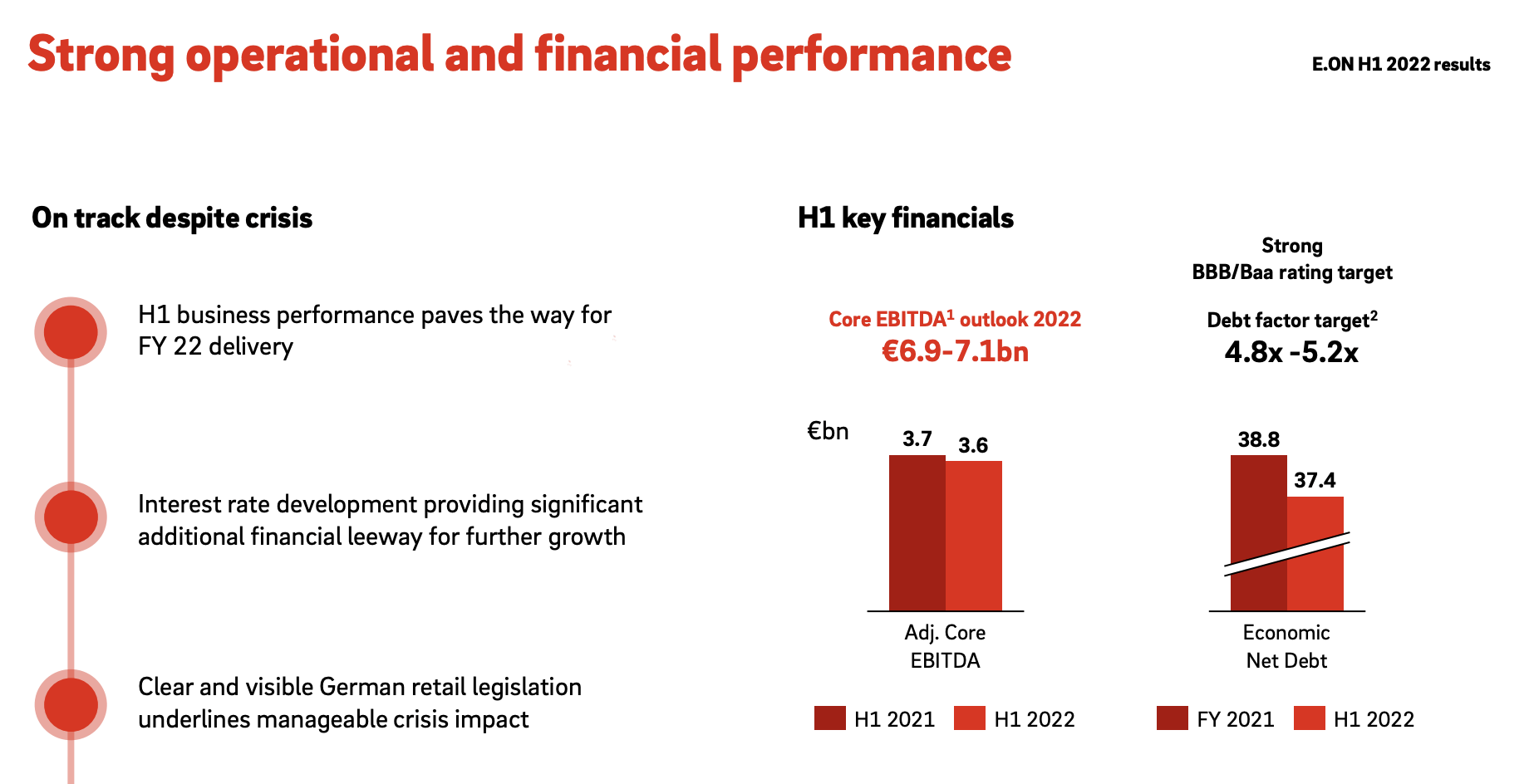

1H22 targets mostly confirm this, delivering absolutely stellar half-year numbers despite an extremely challenging market. The pace of introduction for new energy policies in all of its geographies has broken records as of late, but this has not detracted from the company's focus on financial performance for the past 6 months.

{kind=link}

Because of this, guidance or the year has actually been delivered, with expected group EBITDA of upwards of $7.8B and CapEx of around $5.3B. These are confirmations at this point of expectations, and adjusted net income of upwards of €2.3B-€2.5B.

This is driven by current organic RAB growth, increasing efficiencies and synergies in the German market, adjusting tariffs in Sweden, and further disposals in Hungary.

Customer numbers are mostly flat company-wide, and the divestment of non-core goes according to schedule, with Generation in Turkey and Preussen Elektra now removed, turning non-Core EBITDA down over 50% YoY.

The company still has impressive access to funding at comparatively cheap rates, with long-term preferreds, good bond volumes, most of the company's funding targeted to be green/ESG, and impressive diversification across its funding with good maturities - a few in 2022-2023, but most well after 2026. The company isn't a credit risk and doesn't have excessive leverage as evidenced by its continued investment-grade credit rating.

In 1Q22 management was perhaps a bit too positive with regards to looking at 2022E guidance - but this seems to be mostly corrected at this time, with new guidance and good results despite challenges.

Why is the company so confident despite what we're seeing here?

EON's progress in the core business confirms some of the 2022 upsides. The financial position of the company is also improving, which means the company has more legroom to maneuver in what is a very tricky sort of market. Finally, German legislation to encounter the crisis of specifically German gas importers is now visible and clear.

Also, E.ON isn't seeing any further issues with payment ability:

It is worth highlighting that as of today, we are not seeing any material worsening in payment behavior. Of course, we are carefully monitoring our customers' payment behavior, and we are constantly checking lead indicators such as increases in receivables and overdue receivables, changes to installment plans, insolvency rates, credit scorings, amongst other things.

(Source: E.ON Conference Call)

So, E.ON is essentially an income play with a good yield - around 6%. There are peers with higher yield - but few peers with larger size and network coverage.

However, we can't ignore some of the risks here. Macro and geopolitical risk need to be accounted for. I'm now modeling for negative impacts due to commodity prices combined with an inability to pass these increases on. A best-case scenario calls for a lag period before a pass-on.

When combining this with the nuclear generation that's being phased out, E.ON is leaving legacy nuclear behind, as well as a positive commodity correlation due to nuclear, in a time when it's really not possible to say when the current situation in the energy market will resolve itself. E.ON should, in an ideal world, fire all nuclear assets back up and run them at 100% until this is resolved for the highest amount of positive impact - but this is not how nuclear power plants and phase-out plans work.

This still to date leaves E.ON with problematically low visibility for the remainder of the year - and for as long as this energy situation remains. The worst-case that I see is that the lower earnings for 2022 become some sort of earnings plateau, as long as we're in this sort of situation.

Let's update the target here.

E.ON Valuation

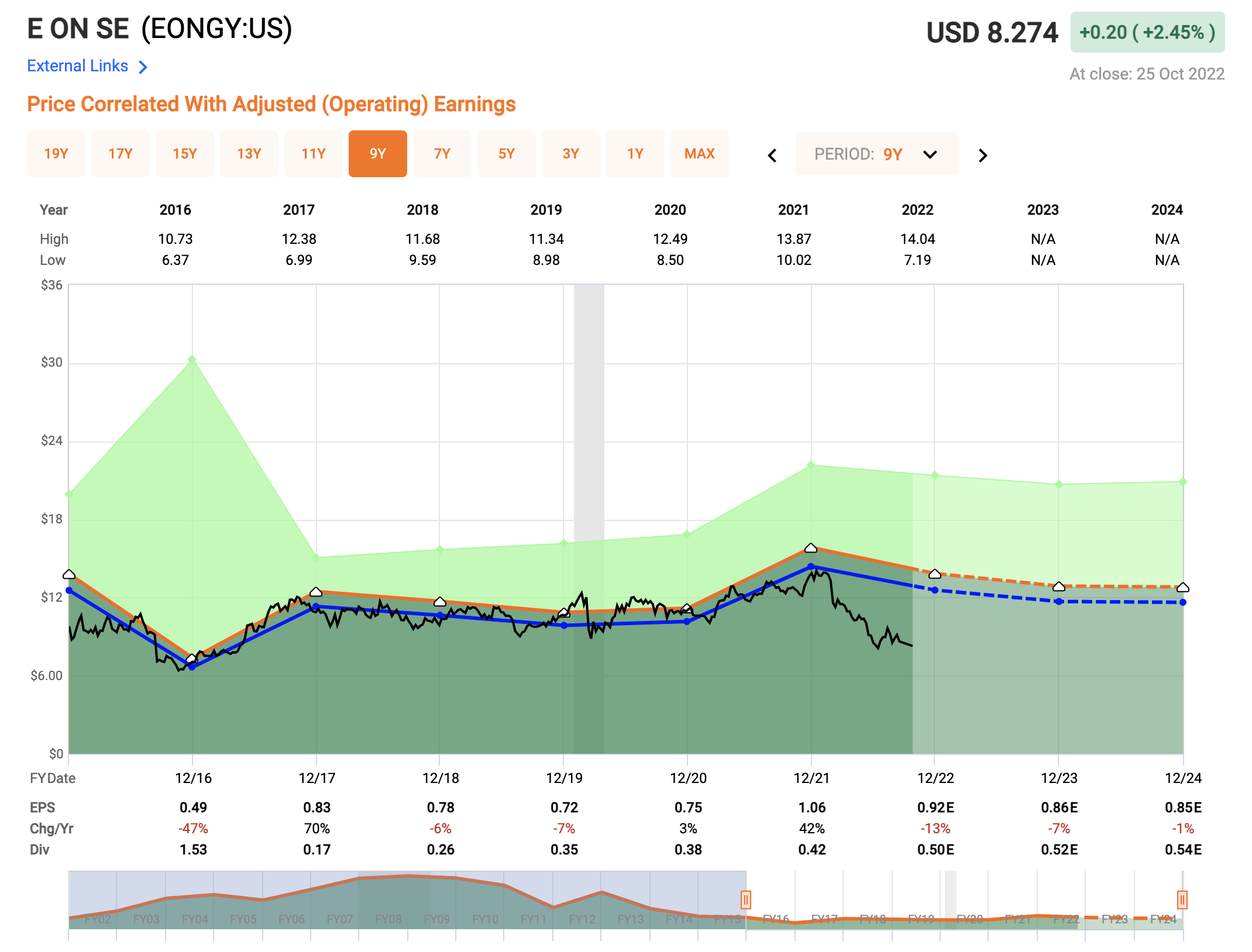

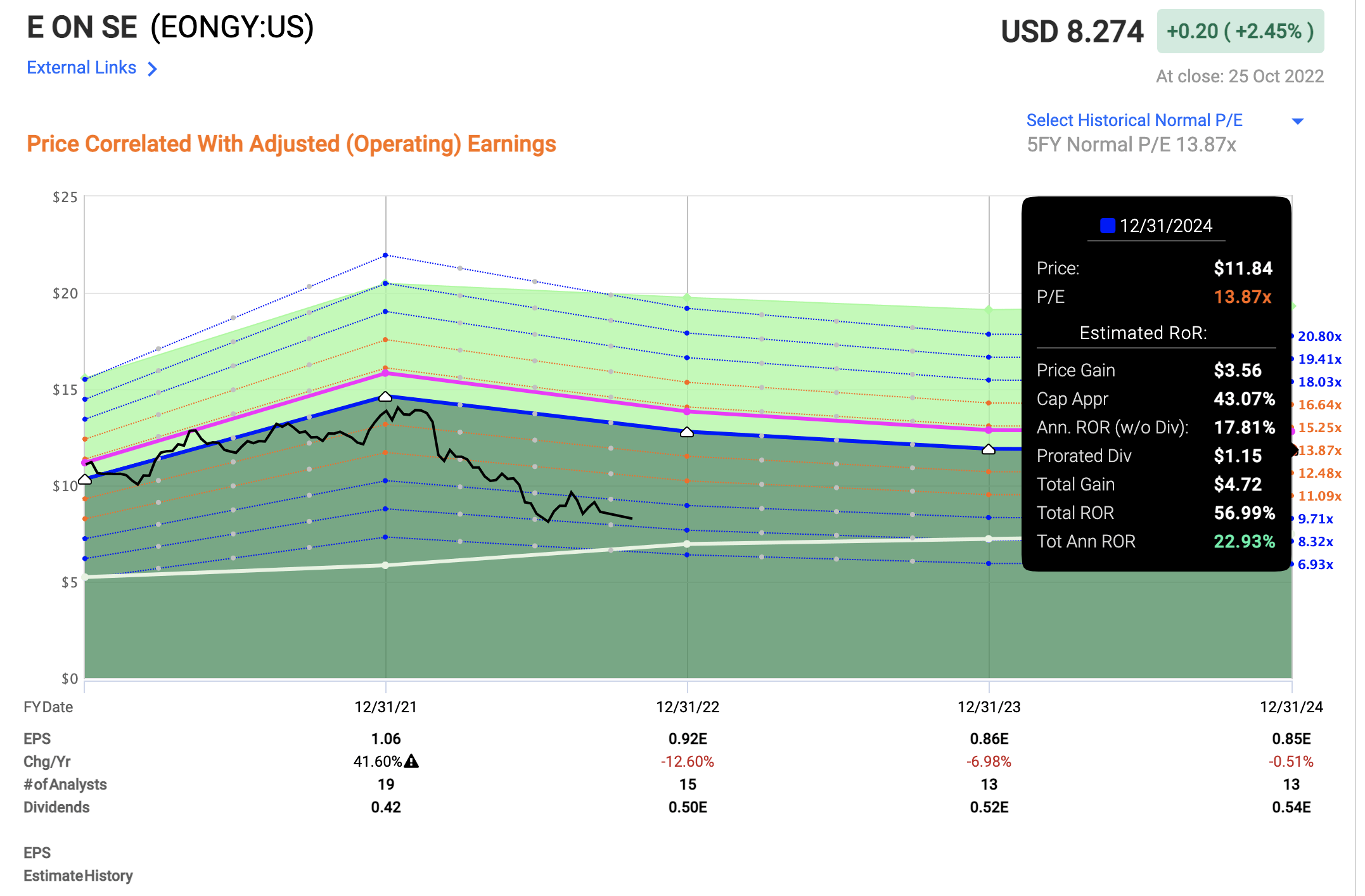

The company's valuation is down to levels below €8.5/share at this time. This alone should clarify some of the investment appeals for you. This is close to the price where I bought most of my original stake - lower in terms of valuation.

Look at the trends.

{kind=link}

I've already heavily impaired my valuation targets for E.ON. For NAV, I've further impaired the stake in Nord Stream 1, adjusting my resulting NAV down to €10.4/share. Including the peer averages and premiums, I lowered my PT from €10.9 to €10.5 for the company. I've also lowered how I account for E.ON in the context of its peers, lowering the premium I accept in purchasing it. So even with all that we're seeing here, the targets have been adjusted pretty heavily already.

Near-term uncertainty still has more potential to drive share prices even lower. E.ON does have upside but comparing a 10-12% upside to one of 20-50% is pretty easy - and the conclusion is self-explanatory. Because current earnings trends are expected to go in the negative. Even at current prices the potential for E.ON during the next few years, if bought today, is around a 10-12% annualized RoR for the company here.

We forecast E.ON at a discount rate of 12-14x P/E going forward, and on that basis, we're seeing a minimum 12 x P/E upside of 17% annually, and upwards of 22-25% annual RoR including dividends until 2024E.

{kind=link}

The current S&P Global targets are for E.ON to trade at around €10.7 native, which is fairly close to my own target, with a minimum range target of €6.8 and a high of €12.5/share. The company is currently followed by 19 analysts and 9 of them consider it a "BUY" here.

It's always tricky buying a company in the middle of a downward streak - and it's hard to argue the forecast that we're likely to see slightly declining EPS in the current trend. On the other hand, company cash flows and income are based on an extremely solid set of conservative assets, likely to outperform and likely to deliver solid income for the foreseeable future.

I still view it as illegitimate and illogical to try and argue that E.ON is worth less than €10/share. It's not - almost no matter how bad things get. But I do believe there are utilities in Europe with a better upside. As subscribers, I'm obviously happy to direct you to these.

Iberdrola (IBDRY) has a less reliant rate base and seems less volatile, with an upside similar to E.ON here. Yield is also somewhat similar. I view Iberdrola as more stable currently, and a company I would buy before E.ON, despite the price increase.

But really, the biggest undervaluation can be found in Italian Enel (ENLAY). I very recently wrote about Enel, and this remains my current #1 Pick in the EU utility sector. I highly recommend that you take a look at this company to see if it might suit your goals.

Here is my thesis for E.ON.

E.ON Thesis

Thesis

- The company is getting cheap even for the potential headwinds the company is facing. At these prices, things are getting cheap even when considering the headwinds and impairments we're seeing.

- E.ON is a "BUY" based on its valuation, which is now lower than €10/share with a conservative and impacted PT of €10.5.

- I'm buying more here, and I believe you should definitely take a closer look at E.ON here.

I'm changing my Price target, but due to valuation, I'm still at a "BUY".

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

For further details see:

E.ON: Might Be Time To Get Back In? I Believe So