AFT - EAD: A Great Junk Bond Fund That Could Experience Some Short-Term Pain

2023-12-27 13:23:35 ET

Summary

- The Allspring Income Opportunities Fund is a junk bond fund that provides a very respectable 9.52% yield to its shareholders.

- The EAD closed-end fund has been performing quite well over the past few months, as investors have become very optimistic about the Federal Reserve cutting interest rates.

- The market is almost certainly wrong about the degree of 2024 rate cuts, which could result in short-term pain for anyone who buys the fund at today's levels.

- The fund managed to cover its 2023 distributions and just increased it. There is still a risk that it will have to reduce the payout during 2024, though, if the market is wrong about rates.

- The EAD fund is currently trading at a very attractive discount to net asset value.

The Allspring Income Opportunities Fund (EAD) is a closed-end fund aka CEF that specializes in providing investors with a very high level of current income. This fund is somewhat underfollowed by many investors, as well as the financial media, which may have something to do with Allspring Global not being nearly as well known as some of the larger fund houses. That does not mean that this is a bad fund, though, and indeed many of the comments on my previous article suggest that it has its fans. Indeed, the fund does seem to be quite competent as a junk bond fund, and its 9.52% yield is competitive with other junk bond funds. However, investors who are seeking to achieve the highest possible level of income that they can from their assets might still want to stick with a good floating-rate fund, such as the 12.36% yielding Apollo Senior Floating Rate Fund ( AFT ).

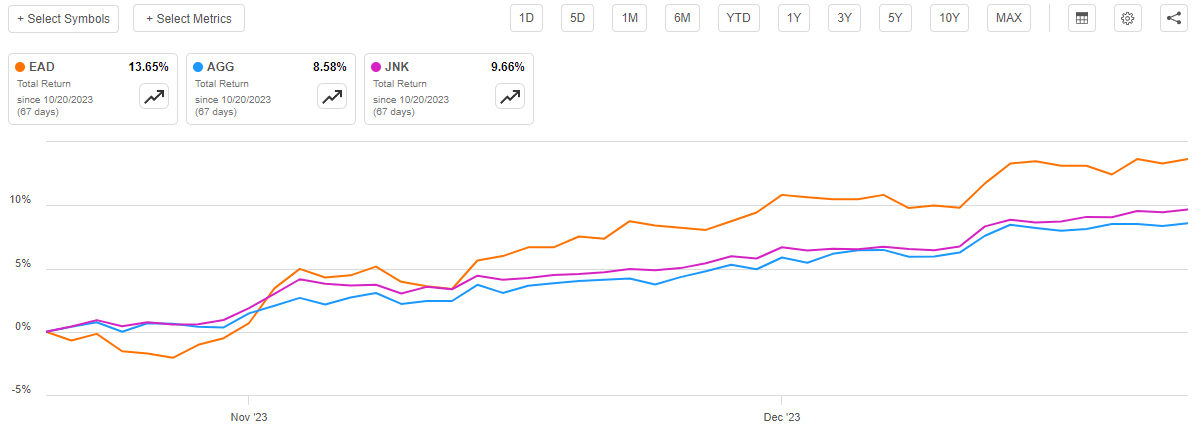

The last time that we discussed the Allspring Income Opportunities Fund was October 20, 2023. The market has generally been very strong since that time, as investors have been attempting to front-run their expectations of a series of rate cuts in 2024 by the Federal Reserve. This has had the effect of pushing junk bond prices up and yields down. As this fund invests in junk bonds, we can expect that this scenario would have resulted in it having a very respectable performance over the interim period. This is indeed the case, as the Allspring Income Opportunities Fund is up 11.84% over the period. This is substantially better than either the Bloomberg U.S. Aggregate Bond Index ( AGG ) or the Bloomberg High Yield Very Liquid Index ( JNK ):

{kind=link}

As I have pointed out numerous times in the past though, it can be misleading to simply look at the price performance of a closed-end fund. This is because these funds typically pay out all of their investment profits to the shareholders in the form of cash distributions. These distributions provide an investment return and naturally result in these funds performing much better overall than their share price would indicate. As such, we need to take the fund's distributions into account as part of our performance analysis. When we do this, we see that investors in the Allspring Income Opportunities Fund have received a 13.65% total return since the date that my previous article was published:

{kind=link}

This is obviously a very strong performance by the fund, and it will undoubtedly satisfy just about any investor who is seeking income. Indeed, this total return should be sufficient to satisfy any investor no matter what their goals are.

Unfortunately, these gains are largely predicated on the Federal Reserve meeting the market's rate cut expectations. There are some reasons to believe that this will not be the case. As such, it may be advisable to urge caution before entering into any new positions in fixed-rate bond funds or junk bond funds.

About The Fund

The website for the Allspring Income Opportunities Fund can be found here , but it is not very informative. It includes absolutely no information about the fund's objectives, strategies, or current holdings, for example. Fortunately, the fact sheet that can be downloaded from the website does include this information. According to the fact sheet, the Allspring Income Opportunities Fund has the primary objective of providing its investors with a very high level of current income. This makes a lot of sense considering the fund's strategy. As the fact sheet explains:

Under normal market conditions, the fund invests at least 80% of its total assets in below investment-grade (high yield) debt securities, loans and preferred stocks. These securities are rated Ba by Moody's or BB or lower by S&P, or are unrated securities of comparable quality as determined by the subadviser.

As I have pointed out in various previous articles, bonds and other debt instruments are income vehicles because they deliver all of their net investment returns in the form of direct payments to their owners. After all, investors purchase these securities at face value, and they receive the same amount back at maturity. Thus, there are no net capital gains over the life of the securities.

With that said, bonds do experience price variations in response to interest-rate changes. It is an inverse relationship, so bond prices go up when interest rates go down and vice versa. This is the reason why the Allspring Income Opportunities Fund has seen such strong price appreciation over the past two months. Over the past two months, long-term interest rates have declined significantly. We can see this by looking at the yield of the ten-year U.S. Treasury, which is generally considered to be the benchmark long-term interest rate. Here is the three-month chart:

{kind=link}

As we can see, the ten-year U.S. Treasury has seen its yield decline from a high of 4.9880% on October 19, 2023 (the day before my previous article on this fund was published) to 3.841% today. That pushed up the bond's price, as well as the price of any other bond that has a fixed-coupon rate because other bonds are typically priced based on the ten-year U.S. Treasury.

This trend has benefited the junk bonds and the preferred stocks held by this fund. However, the fund's description of its strategy also states that it invests in bank loans. Bank loans are floating-rate securities, and as we discussed the other day , these securities do not benefit from falling interest rates. Thus, not all of the securities that may be included in the portfolio of the Allspring Income Opportunities Fund would benefit from falling interest rates.

Unfortunately, the fund does not state what percentage of its portfolio is invested in traditional fixed-income securities as opposed to floating-rate securities. This information is nowhere to be found on either the website or in the fact sheet. CEF Connect has this information, however, as it states that 6.98% of the fund's assets consist of bank loans:

CEF Connect

This does not necessarily mean that the fund's floating-rate percentage is exactly 6.98%, as it is possible for other things to be floating-rate. For example, cash and cash equivalents are typically such short-term instruments that the return that the fund receives on these securities will be more affected by short-term interest rates than long-term interest rates. Right now, short-term interest rates are much higher than long-term interest rates due to the market's expectations that the Federal Reserve will shortly reduce interest rates. As cash equivalents tend to mature very quickly, the price of them is not affected much by interest rate changes. As such, CEF Connect appears to be stating that 10% or so of the fund's assets should not see their price change very much in reaction to interest rate policy. While that may not be an exact figure, we can still see that the majority of the fund's assets should increase in price when interest rates decline and vice versa. Thus, there is a significant amount of interest-rate risk embedded in this fund.

This risk is very important to consider when investing in this fund. This is because there is a very strong possibility that the market is overly optimistic about the Federal Reserve reducing interest rates next year. The fed funds futures market is now pricing in a 14.5% chance that the Federal Reserve will cut interest rates in January. A week ago, the fed funds futures market was pricing in an 8% chance of a January cut. A month ago, the market said that there was a 12% chance of a rate hike in January. It is increasingly looking like the market is running on momentum and trend-chasing right now and will probably be disappointed, as the Federal Reserve is highly unlikely to cut interest rates in January.

The market expects that the federal funds rate will be around 4% at the end of 2024. That would require six rate cuts, totaling 150 basis points over the next twelve months. As I have pointed out in various previous articles, the only realistic way that this happens is if the economy falls into a severe recession within the next two months. There has only been one time in history when the central bank has cut interest rates by more than 125 basis points in a single year in the absence of a recession. The Federal Open Market Committee only meets eight times per year, so it would need to cut interest rates at six of them so it can only fail to do so at two. A rate cut in January is still obviously considered a long shot, but the Fed futures market is pricing in an 83% chance of a rate cut in March. In order for that to happen, the Federal Reserve would obviously have to start seeing signs that the economy is slowing down within the next two months or so at most. That seems unlikely when we consider that the economic measures that the Federal Open Market Committee pays the most attention to actually showed improvement in November compared to October's figures. This decreases the possibility that the central bank will reduce interest rates in either January or March, the latter of which will disappoint the market.

As such, there appears to be a great deal of risk that the Federal Reserve will not satisfy the market's current expectations. That suggests that fixed-rate bonds such as the ones held by this fund will decline in price at some point next year and hand losses to any investor purchasing the fund today. That might not be a problem for long-term investors, as the distributions will eventually offset any short-term losses, and it is a pretty fair bet that interest rates will eventually come down. It might not happen on the market's timetable though, so it is best if you mentally prepare yourself for some short-term pain next year before buying this fund today.

Leverage

As is the case with most closed-end funds, the Allspring Income Opportunities Fund employs leverage as a method of boosting its effective yield beyond that of any of the underlying assets in the portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that money to purchase junk bonds and other income-producing assets. As long as the yield that the fund obtains off of the purchased assets is greater than the cost of the debt that it carries, this works quite well to boost the fund's overall returns. However, this use of debt is a double-edged sword because it increases both the gains and losses that investors experience from asset price movements. As such, we want to ensure that the fund is not carrying too much debt since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed 33% of its assets for this reason.

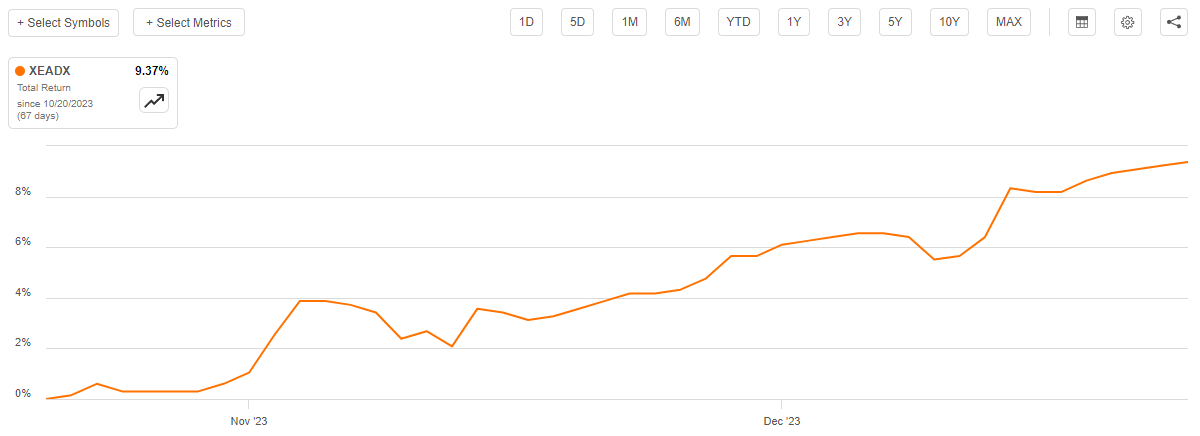

As of the time of writing, the Allspring Income Opportunities Fund has leveraged assets comprising 30.12% of its portfolio. This is quite a bit less than the 31.91% leverage that the fund had the last time that we discussed it. This represents the continuation of a trend that we have been seeing among most of the other closed-end funds that we have discussed in recent weeks. This trend is that the fund's leverage has decreased over the past few months due to its net asset value increasing. As we can see here, the fund's net asset value is up 9.37% since the date that my previous article was published:

{kind=link}

It makes sense that this would reduce the fund's overall level of leverage. After all, an increase in the net asset value means that the portfolio has gotten larger. If the fund simply kept its leverage at the same level, then it would end up representing a smaller percentage of the overall portfolio in such a situation. This is exactly what we see here.

The fund's current leverage is actually a bit less than many other debt-focused closed-end funds possess. It is also well below the one-third level that we ordinarily prefer a fund to possess. As such, the fund's current level of leverage represents a reasonable balance between the risk and the reward. We should not need to worry about its debt too much right now.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Allspring Income Opportunities Fund is to provide its investors with a very high level of current income. In pursuance of that objective, the fund invests in a portfolio that consists primarily of junk bonds and similar assets that pay very high yields and deliver the overwhelming majority of their total returns in the form of direct payments to the investors. The fund collects the payments that it receives from these securities and combines them with any profits that it manages to realize by trading securities that have gone up in price in response to interest rate movements. The fund then pays all of this money out to its shareholders, net of its expenses. As many of these securities boast very high distribution yields and this fund employs leverage to boost the yield further, we can expect that this will result in the fund's own shares boasting a very high current yield.

This is certainly the case, as the Allspring Income Opportunities Fund pays a monthly distribution of $0.0517 per share ($0.6204 per share annually), which gives it a 9.52% yield at the current share price. The fund has unfortunately not been particularly consistent with respect to its distribution over its history. As we can see here, the fund has raised and lowered its distribution multiple times over its history:

{kind=link}

In fact, over the past twelve months, the fund cut its distribution ten times and raised it once. Thus, it certainly does not have the same stability that we see with many other funds, although there were a few periods of time in which it managed to accomplish this task such as the 2013 to 2016 period shown above. For the most part, though, the fund's distribution history is unlikely to appeal to any investor who is seeking to earn a safe and consistent level of income from the assets in their portfolios. The fact that the general trend has been a declining distribution over time adds to this problem, as we want distribution increases in an inflationary environment in order to ensure that our incomes are growing quickly enough to offset the increase in the cost of living.

As I have pointed out numerous times in the past though, the fund's past history is not necessarily the most important thing for new investors. This is because anyone who purchases the fund today will receive the current distribution at the current yield and will not be negatively impacted by actions that the fund had to take in the past. The most important thing, rather, is the fund's ability to sustain its distribution at the current level. Let us investigate this.

Unfortunately, we do not have a particularly recent report that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on April 30, 2023. As such, this report will not include any information about how well the market handled the market volatility that dominated the second half of 2023. As everyone reading this no doubt is well aware, the market strength that existed in the first half of 2023 due to investors getting optimistic about the potential for interest rate cuts this year faded in July as the market began to adjust to the fact that the Federal Reserve was serious about the "higher for longer" mantra. It turns out that the market was wrong, and expectations of a September 2023 rate cut did not play out. We have seen a similar strength since mid-October as the market is now anticipating that interest rates will be slashed severely in 2024. The fund might have been able to take advantage of this volatility by buying bonds during the pessimistic period and selling them during the current euphoria. This report will not reveal any information about its success at this opportunity, though. We will unfortunately have to wait a bit longer for more information. Therefore, we have to work with what we have right now.

During the full-year period, the Allspring Income Opportunities Fund received $41,039,833 in interest and $122,777 in dividends from the investments in its portfolio. The fund also lists $329,897 in "interest from affiliated securities," which typically means dividends paid by a money market fund that is investing the fund's idle cash, but this is not certain. This gives the fund a total investment income of $41,492,507 during the period. The fund paid its expenses out of this amount, which left it with $29,651,296 available for shareholders. That was, unfortunately, nowhere near enough to cover the $39,616,135 that the fund actually paid out over the course of twelve months. At first glance, this is almost certainly going to be concerning since we would typically like a fixed-income closed-end fund to fully cover its distributions with its net investment income.

However, there are other methods through which the fund can obtain the money that it needs to cover the distributions. For example, it might be able to exploit changes in bond prices to earn some trading profits. Realized gains are not considered to be investment income for tax or accounting purposes, but clearly do provide some money that can be paid out to the shareholders. Unfortunately, the fund failed miserably at this task during the period, which might be expected since this report still includes the second half of 2022 which was a terrible time for fixed-rate bonds. During the reporting period, the fund reported net realized losses of $45,003,699 but these were partially offset by $5,217,089 net unrealized gains. Overall, the fund's net assets declined by $53,590,051 over the full-year period. Thus, the fund clearly failed to cover its distributions over the period. This at least partly explains why the distribution was continually cut over the course of 2023.

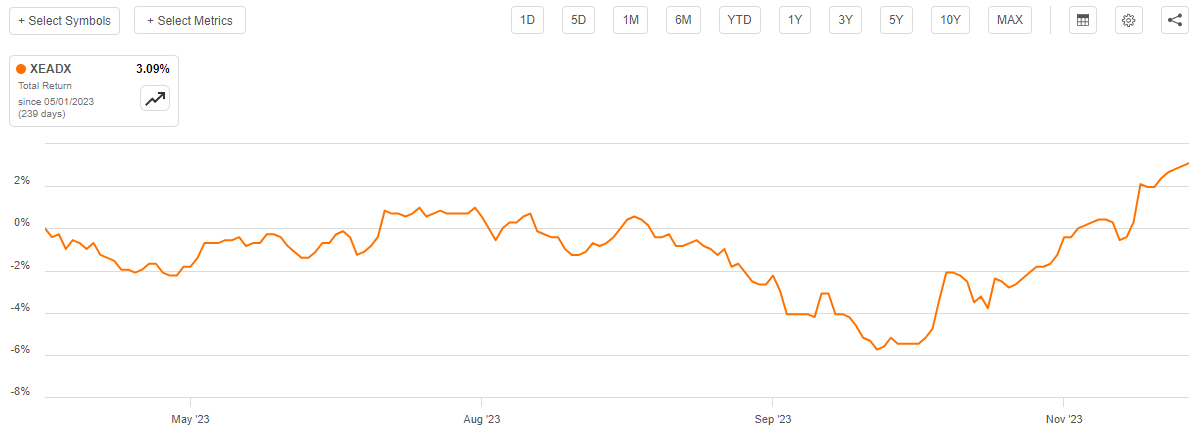

Naturally, though, a lot of time has passed since the closing date of this report. As such, it would be a good idea to try and determine how well the fund has been able to cover its distribution over the past few months. After all, we do not want it to keep paying out too much and destroying its net asset value. We can get some idea of its recent success by looking at its net asset value over time. Here is how the fund performed since May 1, 2023:

{kind=link}

This is a very good sign. As we can see, the fund's net asset value per share is up 3.09% since the closing date of the most recent report. This strongly suggests that the fund has managed to generate sufficient investment profits to cover all of the distributions that it has paid out since that date with money left over. Thus, we probably do not need to worry about a distribution cut and the fund's recent distribution increase reinforces that conviction. This does not mean that the fund will avoid a cut next year though, as there are still some risks that it will not be able to hold onto the recent appreciation of its fixed-rate assets.

Valuation

As of December 26, 2023 (the most recent date for which data is currently available), the Allspring Income Opportunities Fund has a net asset value of $7.35 per share but the shares only trade at $6.52 each. This gives the fund's shares an 11.29% discount on net asset value. This is a reasonable discount that is quite a bit better than the 10.85% discount that the fund's shares have traded at on average over the past month. As such, the current price appears to be a decent entry price for this fund if you wish to add it to your portfolio.

Conclusion

In conclusion, the Allspring Income Opportunities Fund is a reasonable way to add a portfolio of junk bonds to your portfolio. The fund provides a reasonably high yield right now and just recently increased its distribution. It appears that the fund has managed to cover its distributions since May, which is another positive sign.

The big risk here is that Allspring Income Opportunities Fund might not be able to hold onto recent gains as the market is almost certainly overly optimistic about the course of monetary policy next year. Thus, anyone who buys today should be prepared for some short-term pain. This is a very good junk bond fund, though, so it might still be worth considering as long as you are prepared for the risk.

For further details see:

EAD: A Great Junk Bond Fund That Could Experience Some Short-Term Pain