JNK - EAD: Junk Bonds Have Some Risks But This Fund Seems To Be Taking Precautions

2023-10-20 15:49:24 ET

Summary

- The Allspring Income Opportunities Fund offers a current yield of 9.67%, higher than many other options in today's high-yield environment.

- The EAD closed-end fund's performance has been negatively affected by higher interest rates and tighter credit conditions, with shares down 34.26% over the past two years.

- The fund primarily invests in junk bonds, which carry higher yields but also higher risks, although it has a diversified portfolio to mitigate default-related losses.

- Junk bond-rated companies could see higher defaults over the coming risks as they are forced to roll over maturing debt at higher rates.

- The fund's distribution has been challenged, but its valuation is very attractive right now.

The Allspring Income Opportunities Fund ( EAD ) is a closed-end fund, or CEF, that specializes in providing a high level of income for investors. This is evident in the fund's 9.67% current yield, which easily beats many other options available even in today's high-yield environment.

Unfortunately, that is not as high of a yield as some other closed-end funds possess nowadays, as fixed-income houses such as Apollo, Ares, and PIMCO have leveraged bond funds or alternative credit funds that have yields in the double digits. The sustainability of some of those funds' yields is questionable though, and as I have pointed out before a double-digit yield is frequently a sign that the market expects that a fund will have to reduce its distribution in the near future. In the case of this fund's 9.67% yield, the market seems to be telling us that no cut is imminent, but we naturally want to analyze the fund's finances ourselves.

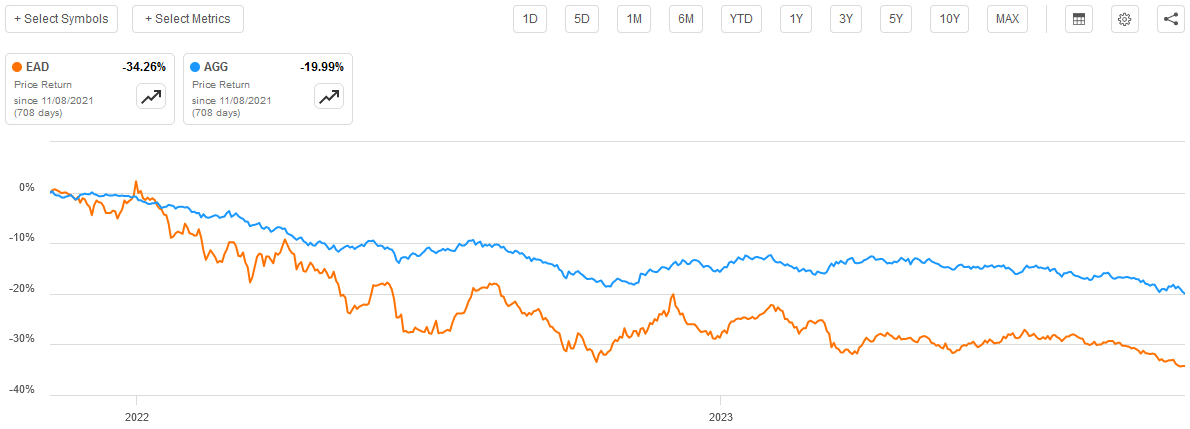

As long-time readers may recall, we last discussed this fund in late 2021. It would be an understatement to say that 2021 was a very different time than today, as interest rates right now are substantially higher and both monetary and credit conditions are far tighter than they were in the aftermath of the pandemic. This has had a punishing effect on pretty much anything whose value proposition depends on the provision of income to shareholders. This fund has certainly not been spared from punishment, as shares of the fund are down 34.26% since the publication of my previous article. This is a worse performance than the broader bond market as a whole has delivered:

{kind=link}

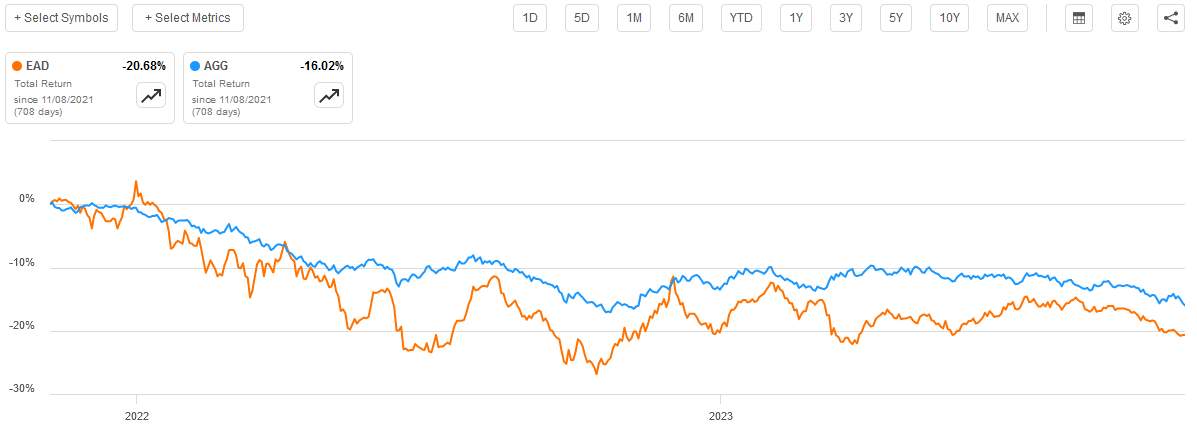

However, as I have pointed out in numerous previous articles, simply looking at the price performance of most closed-end funds does not provide an accurate picture of how investors in the fund have actually fared. This is because these funds pay the majority of their investment returns to investors in the form of distributions. These distributions are sufficiently high that they can offset moderate price declines. When we consider these distributions, the Allspring Income Opportunities Fund still underperformed the Bloomberg iShares Core U.S. Aggregate Bond ETF ( AGG ), but not by nearly the same degree:

{kind=link}

This is disappointing and maybe a bit of a turn-off to potential investors. However, it is exactly what would be expected when interest rates throughout the economy increase. After all, that raises the risk-free rate that is used in the determination of asset prices and generally causes everything to fall in price. The most important thing for potential investors, therefore, is where the fund will go from here. Let us discuss that.

About The Fund

According to the fund's website , the Allspring Income Opportunities Fund has the stated objective of providing its investors with a high level of current income. This makes a great deal of sense for a fund that focuses on investing in the fixed-income market. As we can see here, 98.56% of the fund's assets are invested in bonds, with only very small allocations to cash, common equity, and preferred equity:

CEF Connect

As I have pointed out in numerous previous articles, bonds are by their very nature income vehicles because they have no inherent link to the growth and prosperity of the issuing company. Rather, a bond is simply purchased at face value, makes a regular coupon payment to its investors, and then pays back the face value at maturity. There are no net capital gains over its life and the only net investment return is the regular coupon payment that serves as income. This is the reason why bonds are referred to as "fixed-income securities."

The bonds in which the fund invests are not the traditional investment-grade U.S. Treasuries and corporate bonds that most bond investors focus their efforts on, however. As I explained in my previous article on this fund:

As is the case with many income-focused funds, this one aims to achieve its objectives by investing its assets in high-yield bonds ('junk bonds'), senior secured floating rate loans, and preferred stocks. With the exception of preferred stocks, these securities are somewhat riskier than traditional corporate bonds, which may concern more conservative investors who are primarily interested in the protection of principal. As we will see though, the overall risks here may be overstated, and they are likely less than may be feared.

As mentioned in the quote, it is very common for income-focused closed-end funds to focus their efforts on junk bonds rather than investment-grade corporate bonds or U.S. Treasuries. Perhaps the biggest reason for this is that these funds are specifically trying to generate as high a yield as possible without destroying their net asset base. Junk bonds have far higher yields than investment-grade bonds. As of right now, 30% of new-issue junk bonds have a yield exceeding 10%. The SPDR Bloomberg High Yield Bond ETF ( JNK ) has an average yield-to-worst of 9.38% and an average yield-to-maturity of 9.46%, so that should give you a good idea of current junk bond yields. The ten-year U.S. Treasury bond is yielding 4.99% right now. Thus, we can very quickly see that investing in junk bonds allows closed-end funds like the Allspring Income Opportunities Fund to generate a substantially higher effective yield from its assets than if it were investing in higher-rated securities.

As already mentioned, the fact that this fund is investing in junk bonds may be a bit concerning to investors who are highly concerned about minimizing their risks and preserving the value of their principal. After all, we have all heard about the high risk of defaults that many of these securities possess. Fortunately, the fund has 243 holdings, which should help limit the risk of default-related losses somewhat. After all, such a high number of securities should mean that any individual issuer only accounts for a very small percentage of the overall portfolio.

We can see that this is indeed the case. Here are the largest positions in the fund:

CEF Connect

As we can see, the largest single position here is only 1.54% of the overall fund. That means that even a default from the largest entity whose securities are represented in this portfolio should only cause a 1.54% loss at most. When we consider the yield of junk bonds right now, we can see that such a loss is unlikely to really be noticed, and it certainly will not cause substantial losses to the fund. Thus, a single default probably is no big deal, although we might have to worry about some event that causes widespread defaults in short order. These events tend to be very rare and far between, however.

With that said Moody's Investor Service does expect that junk bond defaults will become more common over the next few years than they have been for most of the past fifteen years or so. The agency points out that a significant amount of debt is maturing over the next five years that will be refinanced at a higher rate. The agency projects that this will cause a surge in defaults as companies either are unable to afford to roll over their debt at today's rates or will be unable to do so because are the tighter conditions in the market. It projects that the default rate will increase to a peak of 5.6% in January 2024 and then begin to decline to 4.6% by August 2024. This could prove to be a bit of a headwind for the fund over the next few months, depending on how many of these defaulting companies are in its portfolio and what percentage of its assets they make up.

Fortunately, we can see that the fund's portfolio primarily consists of highly rated junk bonds:

Fund Fact Sheet

As we can see here, 81.82% of the fund's assets consist of BB or B-rated bonds. In addition, 6% of its assets are in investment-grade securities, and another 2.76% are in cash or cash-equivalent securities. This means that fully 90.58% of the fund is invested in things that are rated B or higher. This should reduce the risk that the fund will suffer from too many losses even as default rates start to rise. After all, the official bond ratings scale states that companies with securities rated B or higher have sufficient financial strength to carry their current debt even through a short-term economic shock. While it is likely that the United States will experience some kind of economic downturn in the near future, we can still see that most of the fund's portfolio companies should be reasonably okay. At any rate, the fund looks to be doing as much as possible to protect itself against the potential for losses.

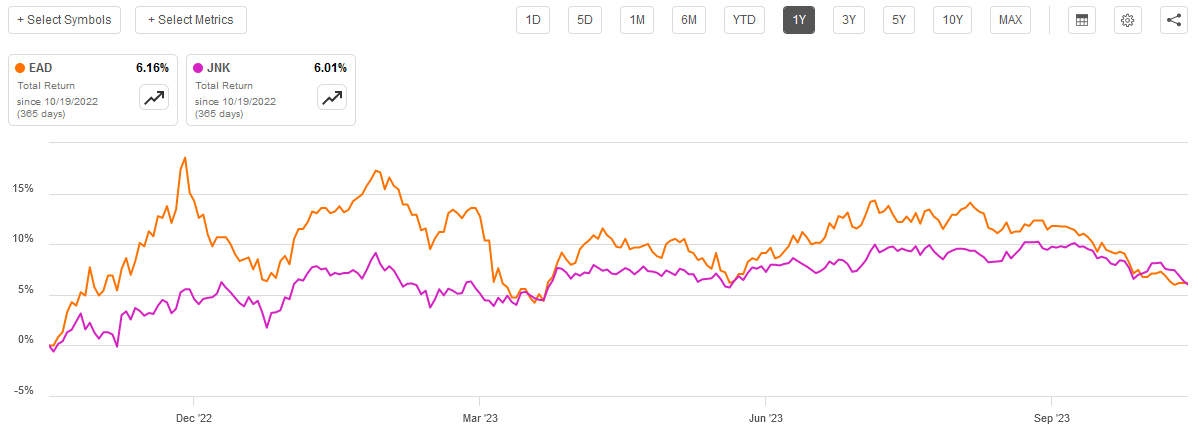

Over the past year, the Allspring Income Opportunities Fund has managed to beat the SPDR Bloomberg High Yield Bond ETF:

{kind=link}

This could be a sign that it is doing a reasonably good job at minimizing losses due to defaults or something else, but it is still a positive sign. I will admit that junk bond investing is one area in which active management can be a big help over a passive investing strategy because a good manager can help the fund avoid losses due to defaults. Naturally, though, there is no guarantee that this is the reason for the fund's outperformance (and it did not outperform year-to-date).

Leverage

As is usually the case with closed-end funds, the Allspring Income Opportunities Fund employs leverage as a method of boosting its returns. I explained how this works in my last article on this fund:

Basically, the fund borrows money and then uses that money to purchase other income-producing assets. As long as the yield that the fund obtains off of the purchased assets is greater than the cost of the debt that it carries, this works quite well to boost the fund's overall returns. However, the use of debt is a double-edged sword because it increases both the gains and losses of an asset. As such then, we want to ensure that the fund is not carrying too much debt since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed 33% of its assets for this reason.

As of the time of writing, the Allspring Income Opportunities Fund has leveraged assets comprising 31.91% of its assets. This is quite reasonable and is actually a bit better than what many other junk bonds possess in terms of leverage. Thus, we probably do not have to worry too much about the fund's use of debt to boost its returns since it is running a fairly reasonable risk-reward trade-off.

Distribution Analysis

As mentioned earlier, the primary objective of the Allspring Income Opportunities Fund is to provide its investors with a high level of current income. In order to accomplish this, the fund primarily invests its assets into a portfolio of junk bonds, which gives it a fairly high yield just by the nature of these assets right now. This fund then takes things a step further and applies a layer of leverage in order to artificially increase the effective yield that its overall portfolio pays out. The fund collects the money that it receives from the assets in the portfolio and then combines it with any capital gains that it manages to realize through bond trading. It pays all of this money out to the shareholders, net of its own expenses. It can be expected that this would result in the fund itself boasting a very high yield.

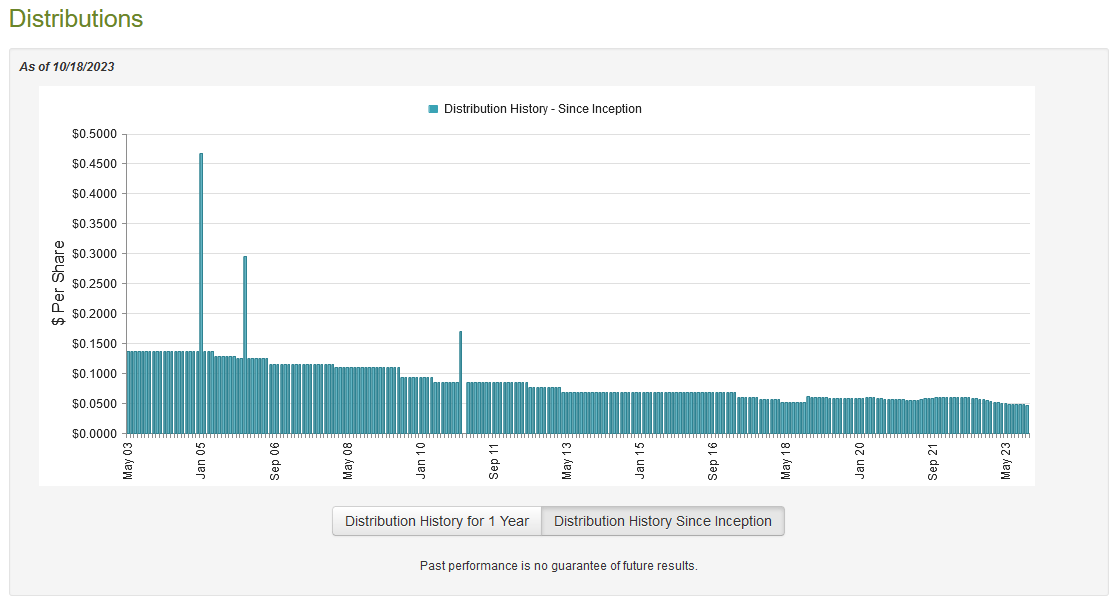

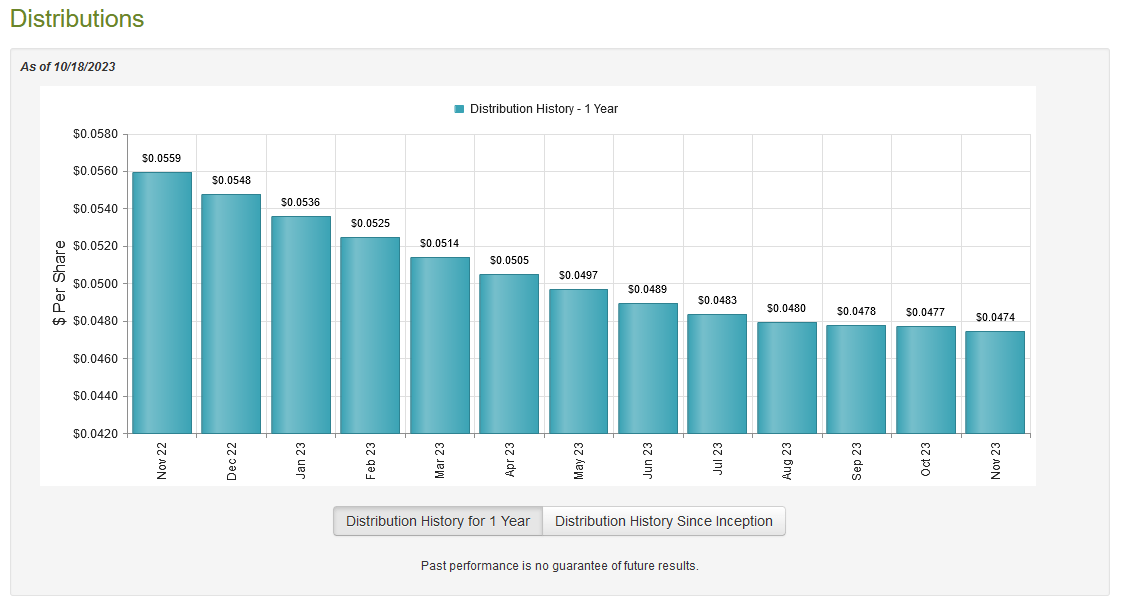

This is indeed the case, as the Allspring Income Opportunities Fund pays a monthly distribution of $0.0474 per share ($0.5688 per share annually), which gives it a 9.67% yield at the current price. Unfortunately, this fund has not been especially consistent with respect to its distribution over the years. As we can see here, it has changed numerous times:

{kind=link}

This will almost certainly reduce the appeal of the fund in the eyes of those investors who are seeking a source of consistent and secure income that can be used to cover bills or other expenses. The fact that the fund has been steadily reducing its distribution over the past year will undoubtedly lessen its appeal further:

{kind=link}

Admittedly, most fixed-income funds have had to decrease their distributions over the past eighteen months due to unrealized losses piling up, but this is one of the worst track records that I have ever seen.

As I have pointed out numerous times in the past though, the fund's history is not necessarily the most important thing to anyone who is purchasing the shares today. After all, anyone buying right now will receive the current distribution at the current yield and will not be affected by any events that happened in the past. As such, the most important thing is how well the fund is covering its distribution today, as that will dictate how sustainable it is likely to be going forward.

Fortunately, we have a relatively recent document that we can use for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the full-year period that ended on April 30, 2023. The fact that this is a full-year report is quite nice because it should give us a good idea of how well the fund handled the incredibly challenging conditions that dominated the bond market in 2022 as well as the optimism that existed in the first half of this year. During most of 2022, the bond market was selling off as investors adjusted to the Federal Reserve adopting a more restrictive monetary stance and raising rates in an effort to combat the incredibly high inflation rate that has been dominating the economy. In the first half of 2023, there was a strong belief that the central bank would pivot and start loosening monetary policy, so traders actually started buying bonds and pushing prices up and yields down. That may have given the fund the potential to generate capital gains if it managed to buy in 2022 and then sell in 2023.

During the full-year period, the Allspring Income Opportunities Fund received $41,039,833 in interest and $122,777 in dividends from the assets in its portfolio. The fund also reported $329,897 worth of income from affiliated securities, which usually refers to the dividends that the fund received from a money market fund, but that is not certain to be the case. Overall, the fund reported a total investment income of $41,492,507 during the period. It paid its expenses out of this amount, which left it with $29,651,296 available for shareholders. That was, unfortunately, not enough to cover the $39,616,135 that the fund paid out in shareholder distributions during the period. At first glance, this will almost certainly be concerning because we usually like fixed-income funds to completely cover their distributions out of net investment income.

However, there are other methods through which the fund can acquire the money that it needs to cover the distributions. For example, it might have been able to earn some capital gains that could be paid out to the investors. Unfortunately, the fund generally failed in this task. During the full-year period, the fund reported net realized losses of $45,003,699, which was only partially offset by $5,217,089 net unrealized gains. Overall, the fund's assets declined by $53,590,051 after accounting for all inflows and outflows during the period. Thus, the fund clearly failed to cover its distribution, and this certainly explains the reason why it has been steadily cutting its distribution over the past year.

Unfortunately, it is uncertain how well the fund can carry its distribution at the current level. Ideally, we want it to have reduced it down so that it is able to pay it entirely out of net investment income, but we will have to wait until the fund releases its semiannual report in a few months to know how close it is to that.

Valuation

As of October 18, 2023 (the most recent date for which data is currently available), the Allspring Income Opportunities Fund has a net asset value of $6.76 per share but the shares currently trade for $5.87 each. This gives the fund's shares a massive 13.17% discount on net asset value at the current price. This is an enormous discount that is a bit better than the 12.48% discount that the shares have averaged over the past month. Thus, the current price seems to be an acceptable entry point for the fund, especially since a double-digit discount is generally a good price to pay for a fund regardless of its average.

Conclusion

In conclusion, the Allspring Income Opportunities Fund is a junk bond fund that has a disappointing recent track record. The fund has been steadily decreasing its distribution over the past year, but at the same time, it has managed to beat the junk bond index. There are some risks here though, as the risk of default-related losses appears to be increasing and that could drag on the fund's portfolio performance. This fund appears to be doing whatever it can to minimize the overall impact of this, however, and the current valuation actually allows for a bit of loss due to the enormous discount.

For further details see:

EAD: Junk Bonds Have Some Risks, But This Fund Seems To Be Taking Precautions