ARES - Earn 11% Yield: 3 BDC Stocks To Buy According To SA Quant And Philip Mause

2023-05-12 08:11:29 ET

Summary

- Banking and Real Estate weaknesses are a catalyst for investors to consider high-yielding Business Development Companies (BDCs).

- BDCs with strong fundamentals can be an excellent opportunity to compound income over the long haul.

- BDCs that have sunk with other financial institutions may also provide capital appreciation potential and substantial yields.

- This article highlights three high-yield BDC stocks outperforming the financial sector this year.

- BDCs can be complex investments, which is why long-term BDC expert and SA Contributor Philip Mause also validates these picks. Not only do the stocks possess sound Quant characteristics, solid dividend safety grades, excellent profitability, and growth metrics, but a combination of Quantitative and Qualitative analysis adds to a rare endorsement.

Where to Invest In a Banking Crisis

We've all heard 'Cash is King,' and when Warren Buffett, considered one of the most successful investors of all time, dumps billions in stocks to sit on a $130 billion cash hoard, it's time to evaluate. Buffett's recent warnings and the fallout from the banking industry are creating market concerns. Where some investors want to sit in cash to wait things out, others want to benefit from the onslaught, and that's when Business Development Companies, aka BDCs, come in.

What are Business Development Companies (BDCs)?

Business Development Companies (BDCs) are similar to a hybrid of Private Equity Funds, Closed-end Funds, and REITs, typically offering some of the best dividend stocks for high yields. One of Warren Buffett's stock portfolios holds Ares Capital ( ARCC ), one of my BDC picks. In addition to the quant ratings and factor grades showcasing my picks' tremendous metrics, I also spoke with long-time BDC investor and senior financial analyst Philip Mause for his thoughts on investing in the industry , given the volatility within the space. In addition to being a lawyer in Washington, D.C., Phil has a long-standing track record analyzing junk bonds, BDCs, and mortgage REITs, some of the most complicated investments in the finance industry. To understand the industry, we must first understand what BDCs are.

Business Development Companies Defined

BDCs are similar to private equity funds for the everyday person, without lockup periods or restrictions, only allowing access to high net worth or institutional investors. Considered specialty finance companies, BDCs are publicly traded on exchanges and primarily invest in small- to mid-sized companies' debt and/or equity.

Similar to REITs , or real estate investment trusts, Congress developed BDCs to encourage corporate tax benefits. Because many BDCs are taxed as Regulated Investment Companies ((RIC)), the BDC pays out at least 90% of net income as dividends, an excellent investment opportunity for high-income yields. From a taxation perspective, BDC dividends are typically not "qualified dividends" and therefore do not get preferential tax treatment, which tends to offer a more favorable tax rate. Instead, BDC distributions are taxed at an investor's ordinary income rate, and BDC gains are qualified dividend income at the capital gains tax rate. While this doesn't matter if traded in an IRA, it's great to know. With BDCs in the financial sector, yields will go up if the tide goes down and share prices fall.

One Stock's Weakness Could Be Another Stock's Opportunity

During periods of banking weakness like we're experiencing now, small- and medium-sized businesses (SMBs) need access to capital. Access to capital provides the ability to sell equity to investors to combine with attractively priced debt for investment in companies' debt and preferred equity. Given traditional banks tightening of credit standards and the demise of Silicon Valley Bank and other regional banks, small- to medium-sized businesses and venture-backed tech startups must look elsewhere for capital. As big banks tighten policies, the floodgates of opportunity and new clients are opening for BDCs.

Business Development Companies to Invest In

Fear moves markets, as we're seeing amid the panic and fall of regional banks such as Silicon Valley Bank, First Republic Bank, and Signature Bank. Due to the structure of BDCs, there could be some opportunities on the heels of a 2023 Financial Crisis. Each bank stock mentioned above, and many other weak Regional Banks , had Quant Strong Sell ratings. And talks of recession and downturn are prompting investors to seek income and alternative ways to capture the upside capital appreciation backed by solid long-term prospects.

Over the last year, the real estate sector ( XLRE ) has been the worst-performing U.S. sector -17%- with financial services ( XLF ) behind. Many investors are searching for distressed assets or those that have recently dropped substantially in price. The bottom fishing in the world of finance has begun, and Seeking Alpha Quant ranks some of these opportunities in Top Asset Management, Custody Bank Stocks, and BDCs. As the financial sector continues to be met with headwinds, I dove into a historical look at bank failures. I immediately reached out and picked the brain of Philip Mause, who experienced the fall of some of the largest banks of the past and felt the impacts of the 2008 Crash that resulted in his affinity for BDC stocks.

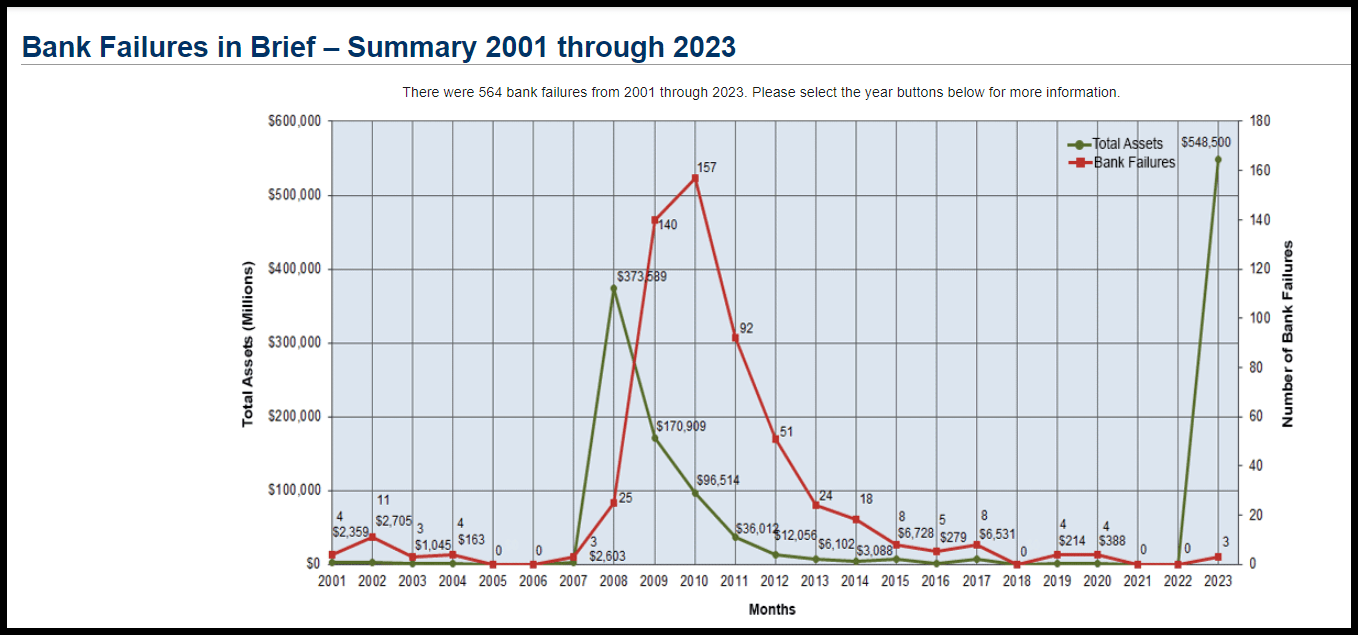

A look at bank failures from 2001 through 2023

A look at bank failures from 2001 through 2023 (FDIC)

{kind=link}

The chart above highlights that the FDIC illustrates 564 bank failures from 2001 through 2023. After being blindsided by the Great Financial Crisis leading up to his retirement, Mause, who studied in great detail the Federal Deposit Insurance Corporation ((FDIC)) and its policy of bailing out big banks, thought back to the 1984 failure of Continental Illinois National Bank & Trust Company, the largest bank failure of the time that resulted in the FDIC's seizure; fast-forward to the $700B bailout of Washington Mutual , aka WaMu, then deemed the largest U.S. bank failure in history, it was seized and sold off to JPMorgan ( JPM ). At the time, the FDIC provided cash access to all of WaMu's depositors, but bondholders and holders of more than $30B in debt were not covered, prompting a massive selloff. In a Seeking Alpha interview, Philip Mause describes :

"You had bank bonds of all sorts of large U.S. banks and smaller banks selling at about 28 cents on the dollar. I started going through this stuff, and then, of course, the TARP program was announced . The large banks that immediately got into TARP - their bonds traded up." After researching and finding the next 10 or so largest banks that I assumed would migrate into the TARP program, bought their bonds.

Then the GMAC (General Motors Acceptance Corporation) situation happened. While it was not a bank holding company, therefore ineligible for TARP, it was a large entity that applied to become a bank holding company. "GMAC had what were called smart bonds that it sold to retail customers for $25 each [and] they were trading at about seven or eight dollars."

All-in-all, my response to the 2008 crash was to buy debt. I learned about a private equity company called Allied Capital ( ARCC ), which at that time was either the largest or the second-largest BDC and under attack by short sellers. Allied Capital's debt was selling for about 28 cents on the dollar. I studied Allied Capital and realized that as a BDC, it had limited leverage; they're not allowed to have as much leverage as banks. So, I became very interested in BDCs as a sector, which I believed was oversold because of its limited leverage.

"I bought a lot of Allied Capital bonds and Allied Capital Equity. I started buying other BDC equity, and I really did quite well come out of the crash, and I learned a lot about BDCs."

Where history tends to repeat itself, much of what Mause describes is happening now. Allied Capital and my other picks are not just about yield. While robust, each stock's fundamentals are consistent contributors to performance, including dividend safety and dividend growth, and given their double-digit yields, these stocks are worth considering. Because there tends to be a correlation between strong dividend growth and strong equity returns, I am focusing on three BDC stocks that also have solid growth and strong capital gain potential:

-

Ares Capital ( ARCC ) 10.49% Div Yield ((FWD))

-

Hercules Capital ( HTGC ) 11.48% Div Yield ((FWD))

-

Horizon Technology Finance ( HRZN ) 11.35% Div Yield ((FWD))

Ares Capital and Horizon Tech's quant ratings are Buy, and Hercules is rated Strong Buy. Each of the picks is fundamentally strong with solid earnings projections. And while this may be a new type of investment consideration, there are benefits and risks associated with BDCs.

Benefits of Business Development Companies (BDCs)

-

Potential high yields - generally greater than common stocks

-

Current income

-

Favorable tax structures

-

Access to private investments not typically available to retail investors

-

Larger BDCs can generally borrow at lower rates and offer greater stability than smaller BDCs

Risks of Business Development Companies (BDCs)

-

Smaller teams make up to the due diligence and investment decision processes that can serve as a benefit or con in case someone leaves the company.

-

Liquidity risks - Because many investments are startups and not publicly traded, they are often illiquid.

-

Diversification risks - Venture capital and venture debt investments held in SMBs may be distressed and in times of economic uncertainty, may not be able to repay loans or weather storms.

-

Credit/Interest risks - Like the banking industry, changes and higher interest rates may affect margins, borrowing, and lending costs. Notably, smaller companies could have difficulty paying off debt as their margins get squeezed, and costs increase.

-

High management fees - It's the price you pay as a retail investor for access to private investments.

Considering these risks, I have three BDC stocks to buy now, with solid fundamentals, excellent profitability, and strong growth metrics.

3 Best BDC Stocks to Buy Now

As the banking industry continues to experience fallout from mismanaged banks, there are BDCs ready to capitalize. BDCs can deliver handsome risk-adjusted returns through diversification and effective investment underwriting, primarily in high dividend yields. Companies that offer regular passive income streams can help offset historically high inflation and surging costs. When evaluating BDCs, Mause considers the following:

-

Loan portfolios

-

Potential default risk

-

The principal amount of loans

-

Fair value

-

List of borrowers

-

Leverage

-

Risk

-

Concentration in sectors (e.g., energy loans, office buildings, etc.)

-

Length of maturity and refinancing terms

-

Identify BDCs well below NAV

Although our BDCs have experienced some slide in share price amid the banking crisis fallout, using Seeking Alpha's quant ratings coupled with an interview from long-time BDC investor and analyst Philip Mause is why I'm highlighting three high-yielding BDCs for portfolio consideration.

1. Ares Capital ( ARCC )

-

Market Capitalization (as of 5/11/23): $9.93B

-

Quant Rating: Buy

-

Dividend Safety Grade: C

-

Forward Dividend Yield: 10.49%

"BDCs are embraced by yield-oriented investors," says Mause, and Ares Capital pays a dividend of $1.96 (in 2022). A market-leading business development company, Ares Capital Corporation specializes in delivering comprehensive financing to middle-market companies. As a global alternative investment manager, the company is focused on acquisition, recapitalization, and complementary primary and secondary investment solutions for credit, private equity, and real estate.

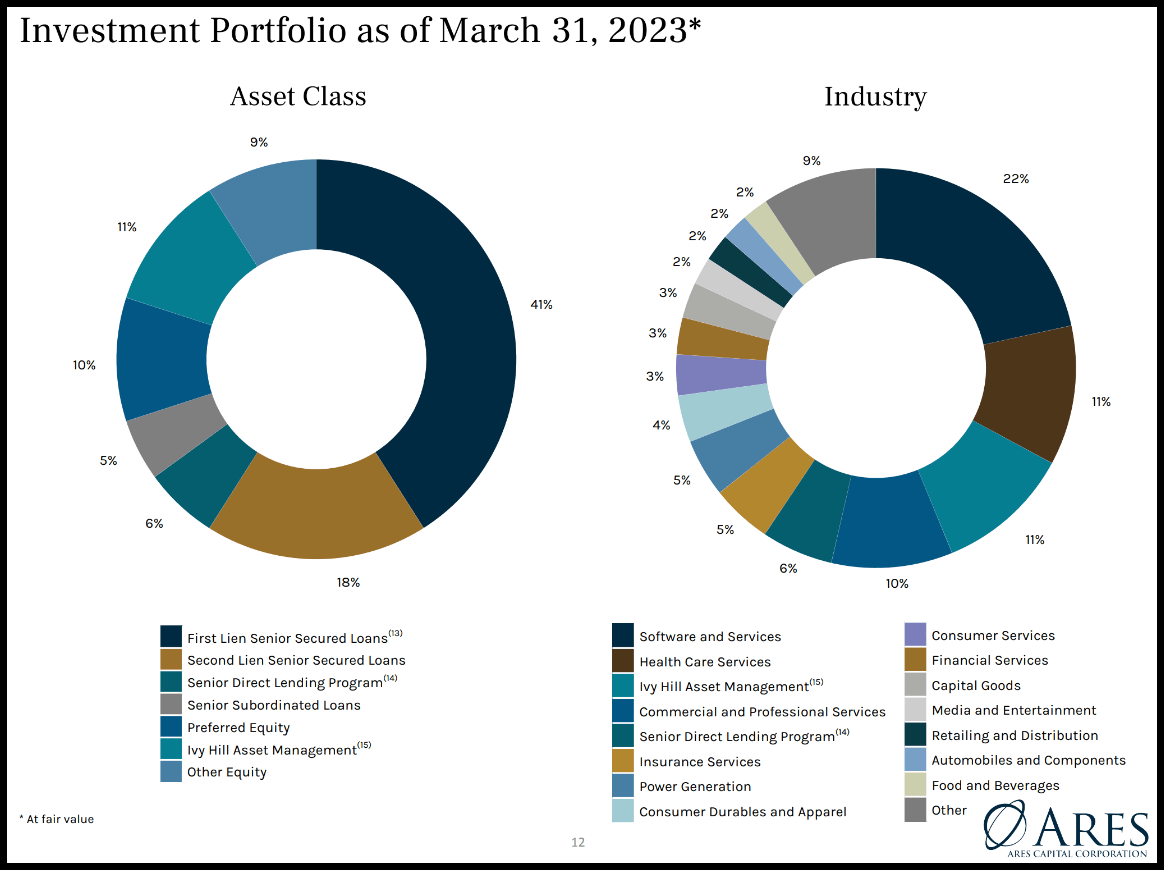

Ares Capital Investment Portfolio Makeup (ARES Capital Investor Presentation)

{kind=link}

Externally managed by Ares Management ( ARES ), Ares Capital is the biggest BDC in terms of market by asset size. With a $21B fair value portfolio as of March 31, ARCC's top industries include software, financial services, and healthcare.

In light of the recent banking turmoil, ARCC has successfully increased its level of liquidity by extending out maturities for more than $4.5B of committed bank funding to relatively attractive prices.

"Through our nearly 2 decades of operating ARCC, we have a time-tested playbook for successfully navigating periods of volatility and market cycles…These capabilities are central to our ability to deliver our industry-leading track record for credit performance since inception, which includes generating a 1% annualized net realized gain rate in excess of losses on our investment since inception…Underpinning our ability to navigate these periods of volatility is the strength of our balance sheet. We deleveraged during the first quarter, and we ended the quarter with a net debt-to-equity ratio below 1.1x," said Kipp DeVeer , Ares Capital CEO.

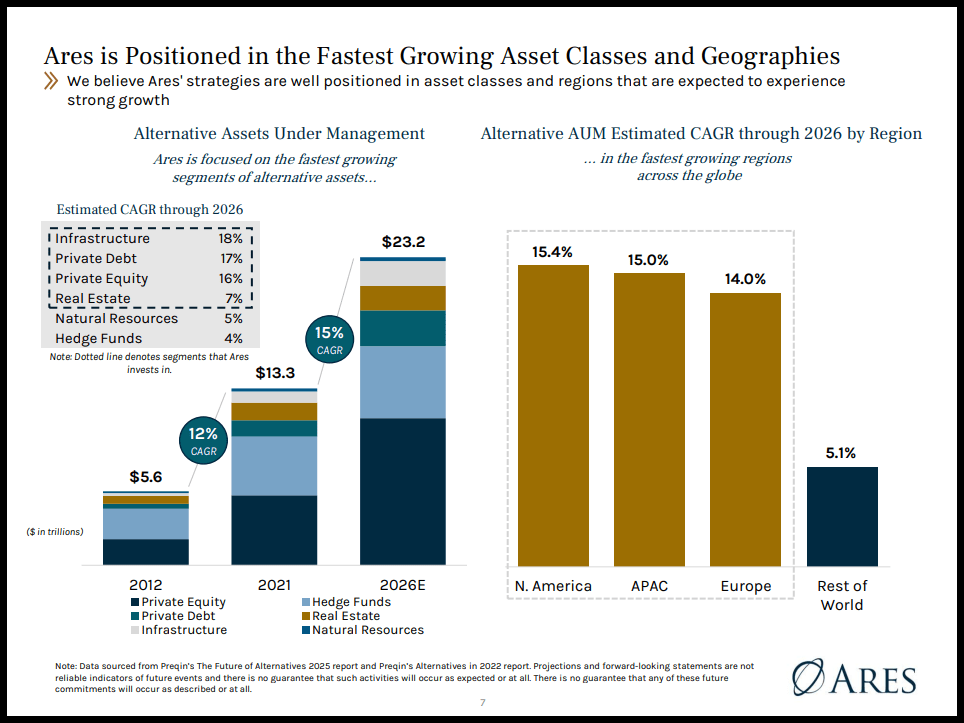

With a strong balance sheet and a team of portfolio management experts focused on mitigating risk and maximizing outcomes, Ares's alternative asset segments are positioned in the fastest-growing asset classes and geographies. Although its first-quarter earnings trailed consensus, Ares maintains earnings strength, excellent profitability, and strong growth potential.

ARES Is Positioned to Grow Fast (Source Link: ARCC Q12023 Investor Presentation)

{kind=link}

ARCC Stock Growth & Profitability

The BDC industry is primed to capture the upside, as tighter credit conditions and constraints open the doors to businesses needing capital and liquidity solutions. Lower leveraging is putting BDCs like Ares in positions of strength to fund loans when banks are tightening. Where the BDCs I'm highlighting can offer a broader range of flexible capital solutions, many, including Ares have capitalized during other periods of market dislocation, as highlighted by Mause. Investing in high-quality and the growth of its direct lending platform, Ares has seen a 14% quarter-over-quarter increase in its deal flow.

Despite a Q1 2023 EPS of $0.57 missing by $0.02, it was still a 36% year-over-year growth that benefit from higher interest rates. Revenue of $618M was missed by $15.13M, but Ares has an investment backlog of nearly $310M and a pipeline of $190M as of April 19, 2023. With a 10.49% yield and discounted valuation, Ares's focus on diversification while avoiding cyclical industries has made its dividend reliable.

ARCC Stock Valuation & Momentum

Showcasing a dividend safety grade of 'C,' this stock has had a solid ability to maintain its current dividend. With a 10.21% dividend yield ((TTM)) and forward P/E ratio of 8.22x versus the sector median of 8.42x, ARCC is also undervalued. In addition to growing its $0.48 quarterly dividend by 6.7% last year, the below dividend scorecard highlights the attractiveness of this high-yielding BDC.

ARCC Dividend Scorecard

ARCC Stock Dividend Scorecard (SA Premium)

{kind=link}

In addition to paying a consecutive dividend for over 17 years, analyst Gen Alpha writes : "As one would expect, ARCC's weighted average yield on debt has grown materially over the past year, by 310 basis points from 8.9% to 12.0% in the first quarter of this year. Net asset value per share also held up well, with actually growing slightly on a sequential basis from $18.40 at the end of 2022 to $18.45 as of March 31." As a stock that continues to help put money in investors' pockets, with tailwinds from the banking crisis, consider ARCC stock and my next pick.

2. Hercules Capital, Inc. ( HTGC )

-

Market Capitalization (as of 5/11/23): $1.89B

-

Quant Rating: Strong Buy

-

Dividend Safety Grade: C

-

Forward Dividend Yield: 11.48%

Like its name, Hercules Capital, Inc. ( HTGC ) is a Strong Buy-rated company, and with the failure of Silicon Valley Bank, its biggest competitor in the asset class, Hercules' is ready to rise.

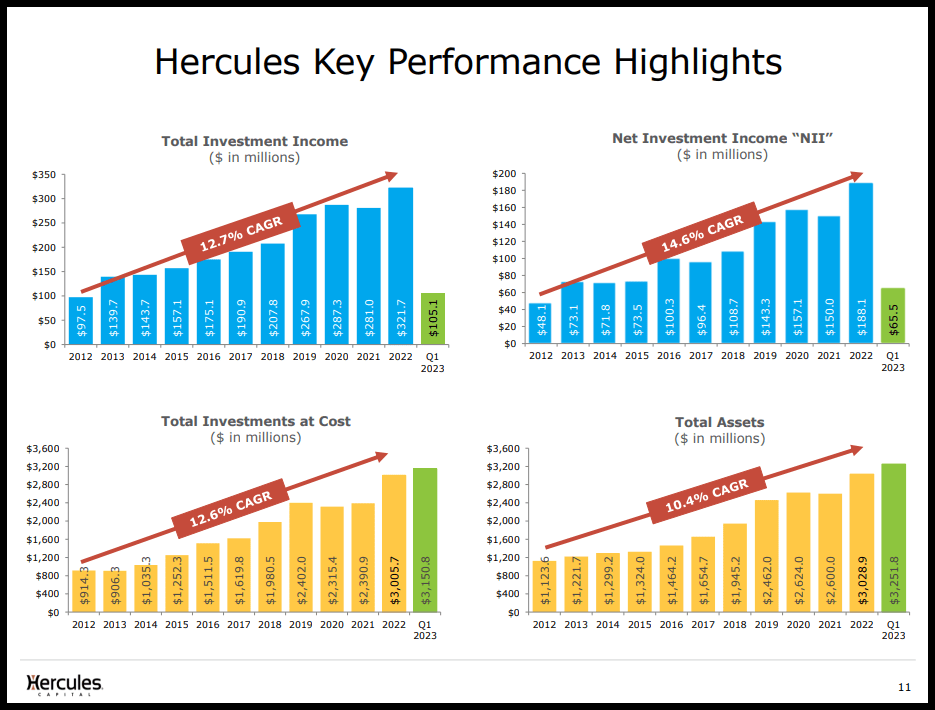

Focused on senior secured loans, and growth capital, Hercules is the largest BDC venture lending company and has funded more than 600 companies; garnered more than 240 IPO and M&A exits; currently has $3.3B assets under management, with more than $17B commitments in its pipeline. "Financing the growth of tomorrow's companies," Hercules Q12023 Investor Presentation offers key insights into its strong growth and profitability, which has delivered strong and sustainable shareholder returns.

Hercules Capital Stock Growth & Profitability

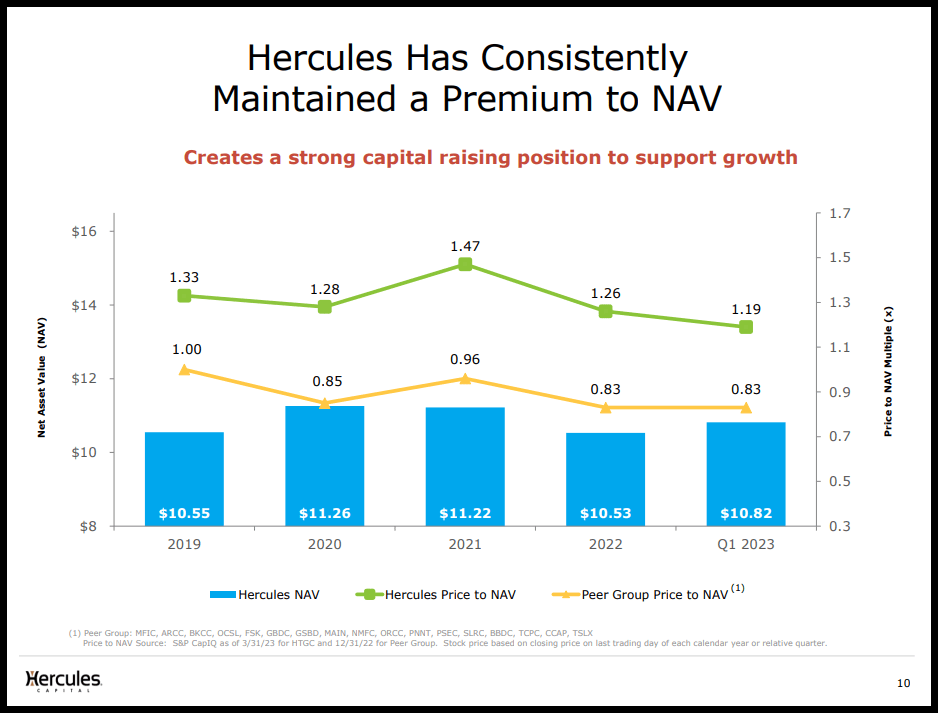

Hercules' strong capital-raising position has benefited from the fall in regional banks. It has accelerated business opportunities and momentum, especially as Hercules has consistently maintained a premium net asset value ((NAV)), one of the primary metrics Philip Mause uses when evaluating a BDC. Looking at the value of the underlying assets for BDCs, similar to an ETF, a publicly traded BDC - like equities with a bid/ask spread - can trade at a discount or premium to its NAV. Hercules has consistently maintained a premium to NAV.

Hercules Stock NAV (Hercules Q12023 Investor Presentation)

{kind=link}

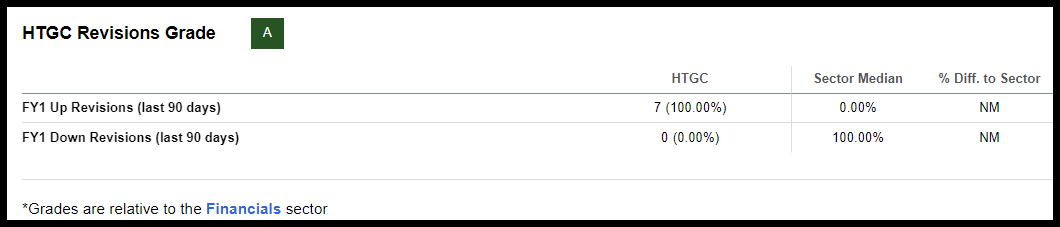

Since the end of Q1, HTGC has funded $3.9M, with an additional $510 in pending commitments. Hercules's first quarter EPS of $0.48 beat by $0.02, and revenue of $105.09M beat by a whopping 61.29% year-over-year, resulting in seven FY1 Upward analyst revisions and zero downward over the last 90 days.

Hercules Stock Revisions Grades (SA Premium)

{kind=link}

Delivering record Q1 operating performance and managing more than $3.9B of assets across its platform, +33% Y/Y, HTGC is focused on strategic and selective deals regarding new business. Hercules not only delivers portfolio growth and underwriting discipline, which has resulted in double-digit CAGR,

Hercules Stock Key Highlights (Hercules Q12023 Investor Presentation)

{kind=link}

By strengthening its platform origination capabilities and establishing a new private credit fund vehicle for enhanced liquidity, Hercules is optimistic going into the future, as it looks to capitalize on the banking fallout. During the Q1 2023 Earnings Call, Hercules Capital CEO Scott Bluestein states :

"The current market requires a combination of playing skillful and selective offense in terms of new business and disciplined and tight defense on credit. We intend to do both, and we believe that we are uniquely positioned to be able to do so successfully…some of the key highlights of our performance for Q1. We started out 2023 with record gross fundings for our first quarter with over $476 million, which led to strong net debt investment portfolio growth of over $153 million. This is the fifth consecutive quarter that we have been able to deliver in excess of $100 million of quarterly net debt investment portfolio growth, which positions us favorably to be able to continue to drive earnings momentum in 2023."

HTGC Valuation & Momentum

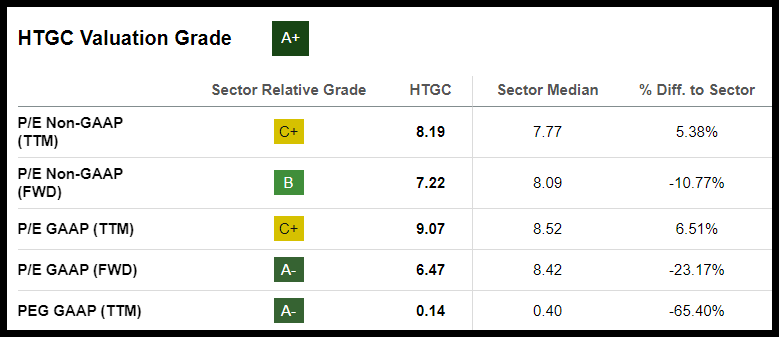

Momentum from 2022, in terms of origination, increased for Hercules in the new year after the failure of SVB and the overall banking turmoil that ensues. Trading at an extreme discount, Hercules' A+ valuation grade is supported by a forward P/E ratio of 6.47x versus the sector's 8.42x, a 23% discount, and a trailing PEG ratio that's -65% difference to the sector. Factoring in its 13.83% dividend yield ((TTM)) and 16 years of consecutive dividend payments, if you're looking for a stock with a solid dividend safety track record and room for upside, look no further.

HTGC Stock Valuation (SA Premium)

{kind=link}

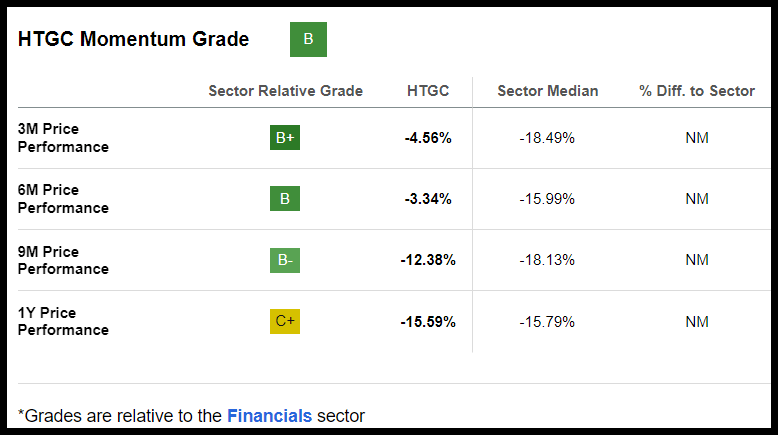

Raising its dividend 8.3% on top of its first-quarter earnings beat, Hercules issued a $0.39 dividend in line with its prior, plus a special distribution of $0.08. Although the stock is -12% over the last year, bullish momentum and Hercules' quarterly price performance continue to trend higher, outperforming its peers.

HTGC Stock Momentum (SA Premium)

{kind=link}

Year-to-date, the stock is up a modest 3%, but that is still significantly better than the performance of the Regional Bank ETF ( KBWR ), down 30%. Given the market volatility, especially in its industry, its outperformance of sector peers and investors' active purchasing of shares to drive the price higher is a testament to an opportunity those of us are seeing to capitalize on potential strong total returns and new business opportunities on the heels of failed banks. Next up, Horizon Technology Finance.

3. Horizon Technology Finance ( HRZN )

-

Market Capitalization (as of 5/11/23): $330.12M

-

Quant Rating: Buy

-

Dividend Safety Grade: C-

-

Forward Dividend Yield: 11.35%

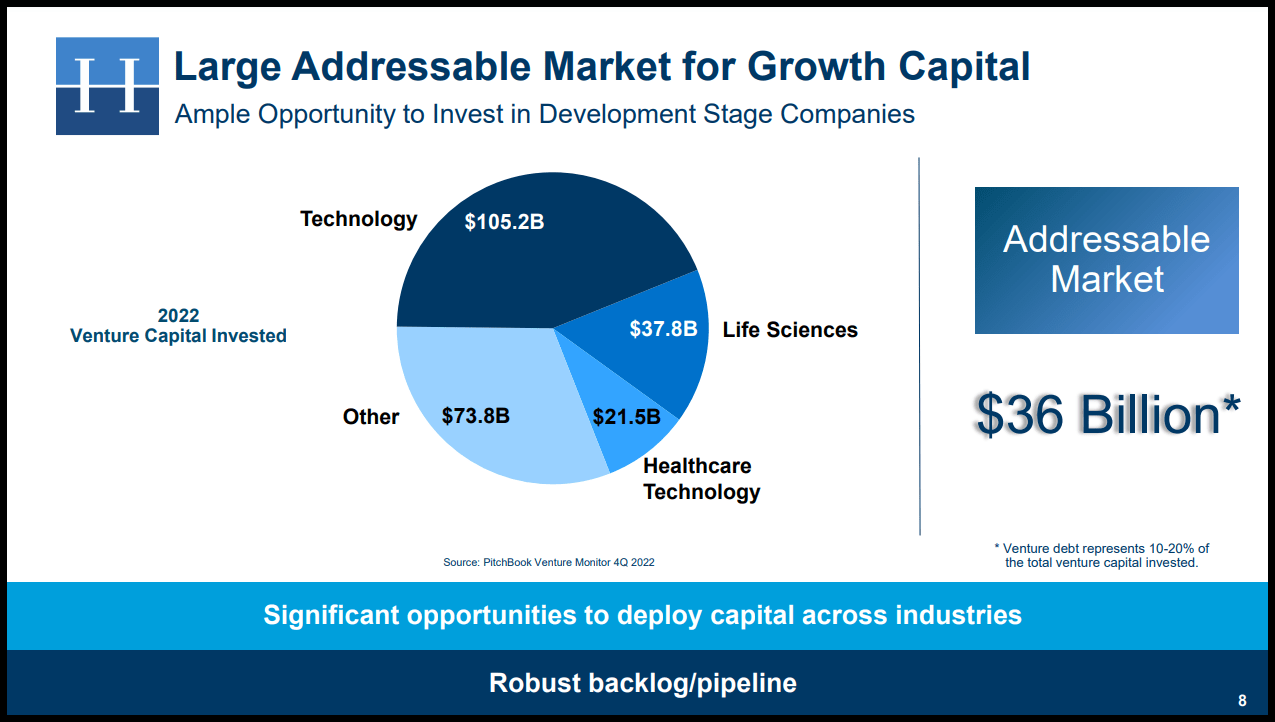

A leading venture lending platform, Horizon Technology Finance offers structured debt products to venture capital companies primarily in the life sciences, technology, healthcare, and renewable industries. Since 2004, Horizon has funded more than 315 companies and originated and invested over $3B in venture loans. With a tremendous portfolio of debt and equity investments, and an attractive 11.35% forward dividend yield, the tailwinds from SVB's fallout leave much to be desired on the horizon.

Horizon Technology Finance Stock Valuation & Momentum

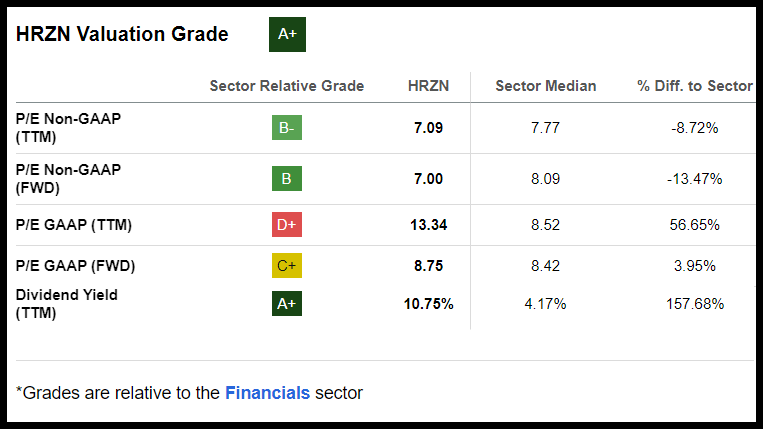

Horizon technology also trades at a discount. As showcased in the below valuation grade, not only is its forward P/E Non-GAAP ratio of 7.0x a 13% discount to its peers, investors receive a tremendous yield for this buy.

{kind=link}

Following consecutive earnings beats, Horizon raised its dividend to end last year by 10%, indicating the stock could trade at a bigger NAV premium. Trading at book value and appealing to passive income investors with its high yield, Horizon Technology continues to capitalize on rising interest rates that have helped expand its premium valuation. When you factor in the prospective opportunities from the fallout of regional banks, this established BDC focused on its specific niches offers ample opportunity for growth and profitability.

HRZN Stock Market Sectors for Growth (Horizon Capital Investor Presentation)

{kind=link}

HRZN Stock Growth & Profitability

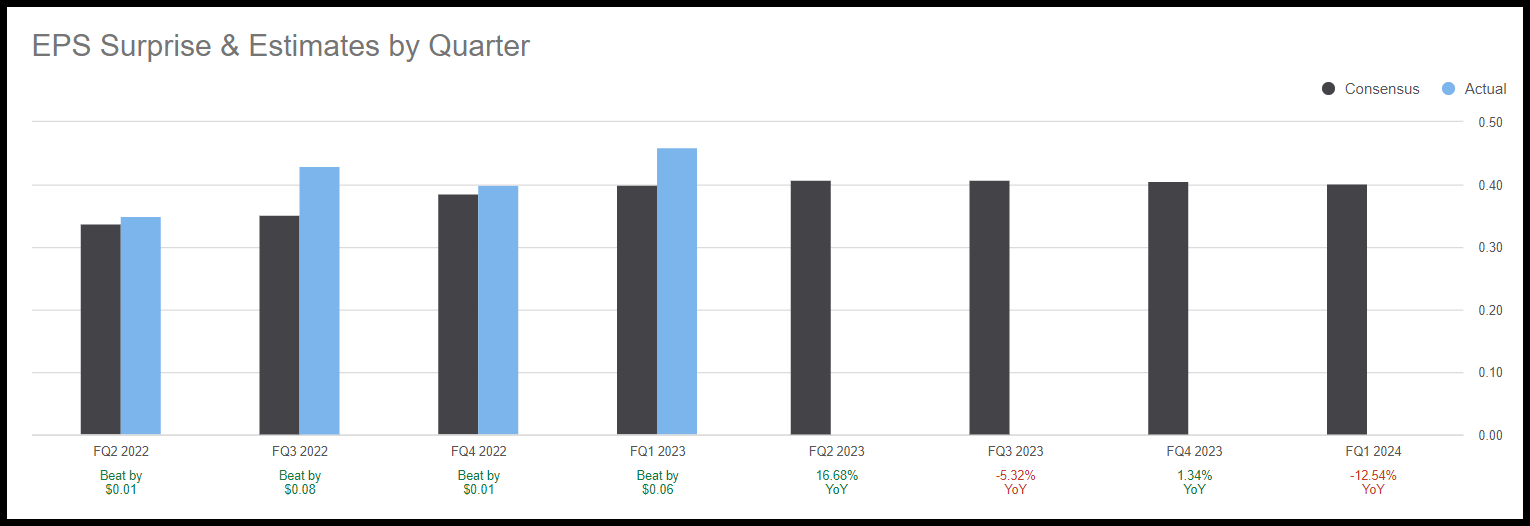

With a robust investment pipeline, strong financials that include 14.4% ((TTM)) average debt portfolio yield, and substantially lower LTV for Horizon's loans compared to the LTV for mid-market, investors can expect a good investment with strong yields. With four consecutive earnings beats, Horizon's latest EPS of $0.46 beat by $0.06, and revenue was up nearly 100% year-over-year.

Horizon Stock EPS Beats

Horizon Stock EPS Beats (SA Premium)

{kind=link}

Higher interest rates served as tailwinds, generating a net investment income of $0.46 per share, well above Horizon's distribution level. Raising $7M of equity at a premium NAV, Hercules' liquidity is strong in funding its backlog of deals and is focused on seeking new debt and equity capital for future growth. During the Q1 2023 Earnings Call, Hercules Chairman and CEO Rob Pomeroy perfectly sums up why BDC's are worth considering.

"With the increasingly challenging macroeconomic environment and fallout from the collapse of Silicon Valley Bank and Signature Bank in the first quarter, Horizon and our adviser, Horizon Technology Finance Management, took a measured approach to originations and redoubled efforts to focus on the credit quality of our portfolio companies. There is no question that the venture capital ecosystem has changed and will continue to evolve. While this creates challenges, this also creates opportunities in both the near and long-term for those that can successfully navigate through the challenges."

Seeking Alpha's quant ratings see each of the three BDC stock picks as buys for portfolios, solidified by Philip Mause's endorsement. Development-stage companies need the right funding, strategy, sponsors, and opportunities to address a market ready to grow. In my opinion, we have identified BDCs that should be able to weather the current crisis, generate high premium yields, and offer capital appreciation potential on the back of the financial sector's weakness.

BDC Stocks for Investment Income and Capital Appreciation

BDCs are a unique investment opportunity in an uncertain time, offering the right combination of growth and yield, bullish momentum, and profitability. The financial sector is riddled with concerns and uncertainty surrounding monetary policy, and inflation is paving the way for BDCs offering yield and income to help ease some investors' concerns. In the words of Mause, "Heading into a possible downturn in the economy - there is always a risk of defaults on loans owned by BDCs. Investors should watch quarterly reports carefully as they come out." And, given tighter credit conditions in the market, BDCs' ability to offer execution and flexible capital solutions to borrowers could enhance their competitive positions, enabling attractive investments for this market cycle. While some negative sentiments and serious economic risks surround the industry, the business development companies I've outlined offer a unique type of investment with mitigated risk through good management teams, sound portfolio management, lower leverage, and solid dividend safety grades.

This year, Ares Capital, Hercules Capital, and Horizon Technology have outperformed the financial sector. The stocks possess excellent profitability, momentum, and overall sound Quant characteristics. Although BDCs can be complex and very risky investments, consider their potential advantage in the current market, validated by our Quant Grades and long-term BDC expert Philip Mause; a combination of Quantitative and Qualitative analysis offers a rare endorsement.

For further details see:

Earn 11% Yield: 3 BDC Stocks To Buy According To SA Quant And Philip Mause