SEVN - Earnings Preview: REITs At Rock Bottom

2023-10-18 10:30:00 ET

Summary

- Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies.

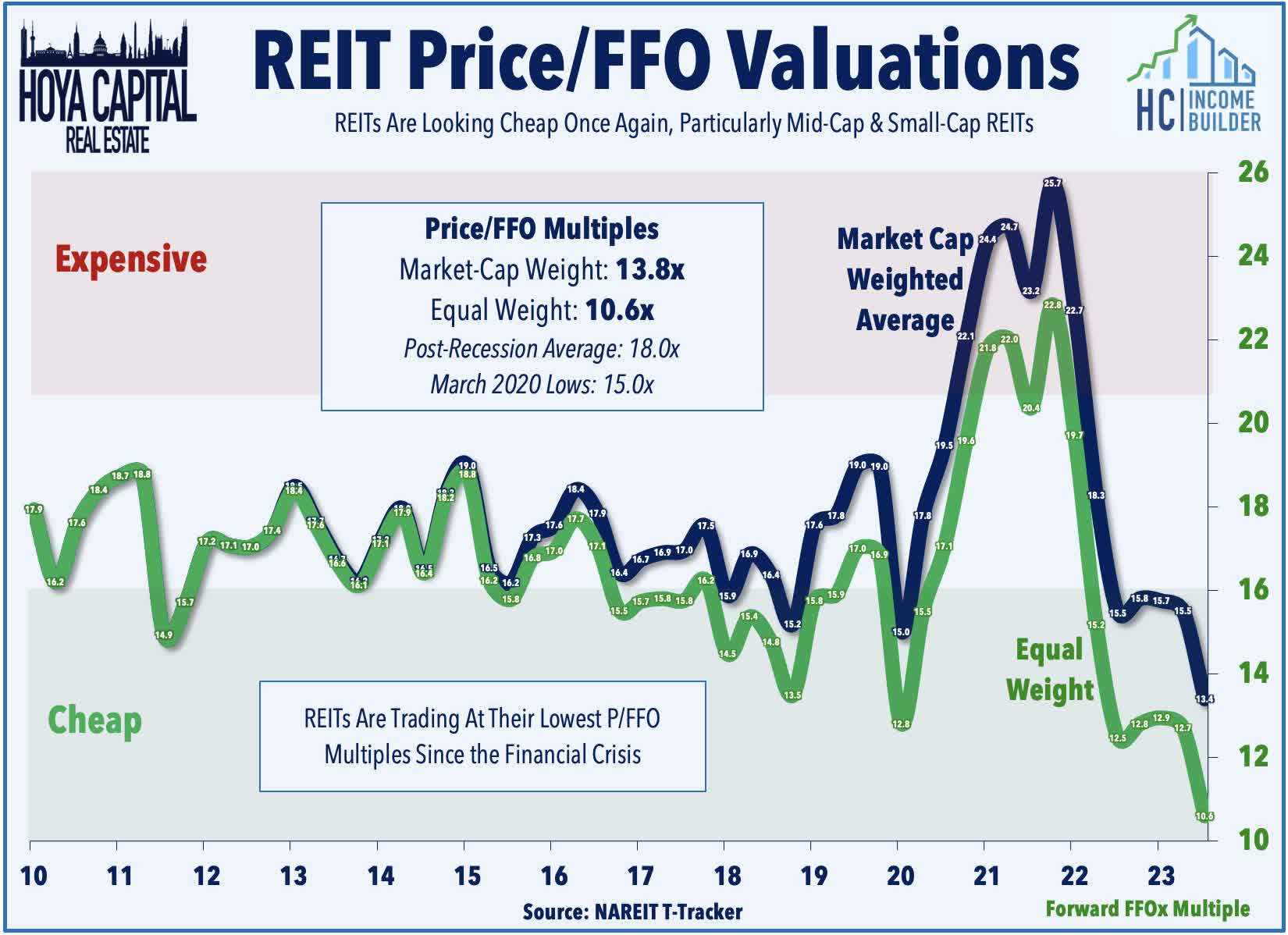

- Have REITs hit "rock bottom?" Pressured by the surge in interest rates, REITs enter earnings season on a skid, with the Equity REIT Index at its lowest level since May 2020.

- While many public REITs have best-in-class balance sheets, even the most well-capitalized real estate owners have been unable to escape the gravitational force of the "higher for longer" environment.

- Property-level fundamentals have remained surprisingly resilient across most property sectors this year - notably in the residential, retail, and logistics sectors - but we're looking for early signs of cracks. We expect the most post-earnings volatility in coastal office, public-pay healthcare, and mortgage REITs.

- Distress has generally remained isolated to the most debt-burdened private market portfolios, but the refinancing clock is ticking ever louder. Capitulation from debt-burdened private portfolios will create consolidation opportunities for well-capitalized REITs.

Real Estate Earnings Preview

{kind=link}

Real estate earnings season kicks off this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies, which will provide key insights into how the real estate industry is adapting to the "higher for longer" higher interest rate regime - and whether the outlook has shifted from last quarter when it appeared that relief from rate pressures was on the immediate horizon. This report discusses the major high-level themes and metrics we'll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders. (Note: Companies that have not yet confirmed an earnings date are in italics.)

{kind=link}

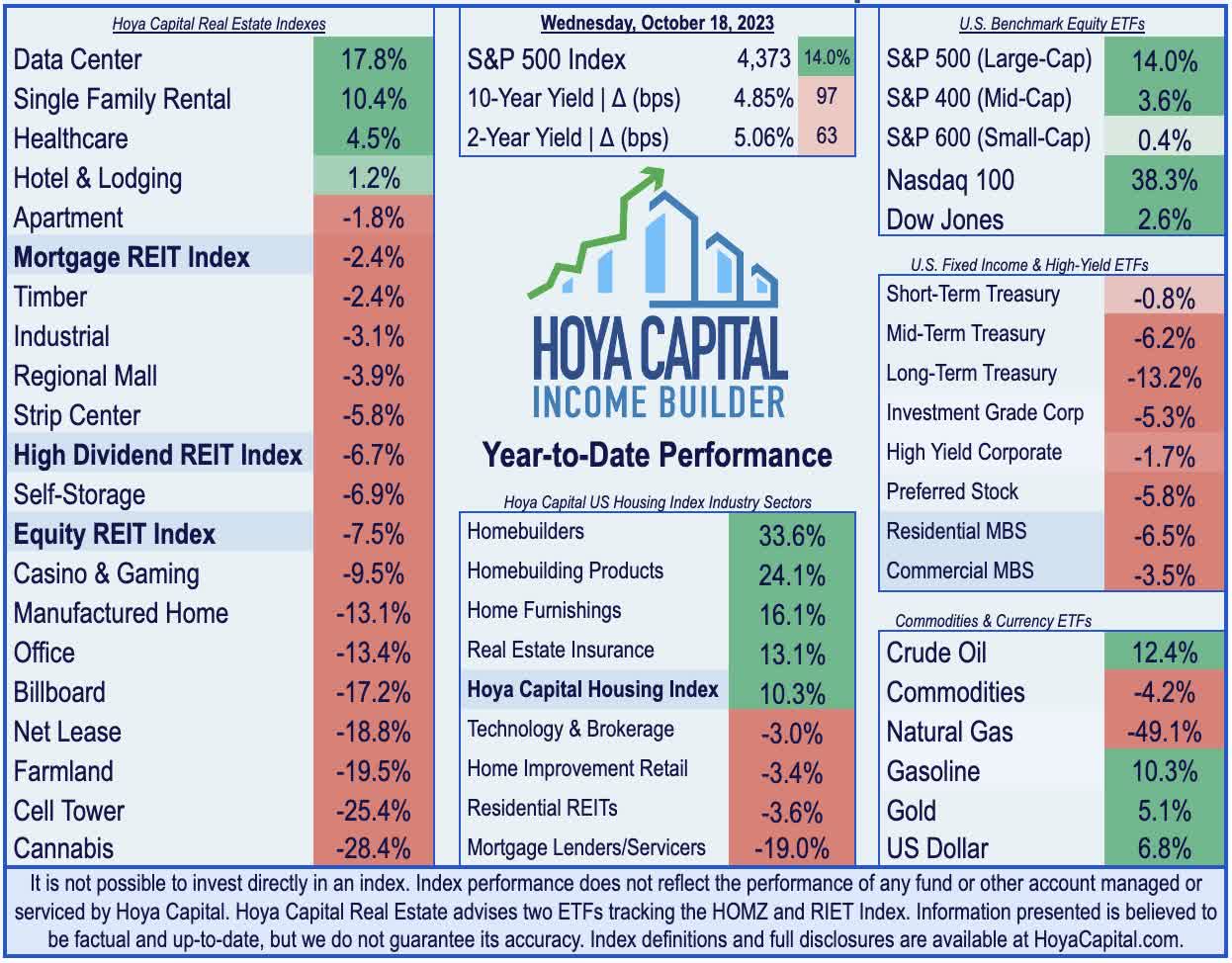

Have REITs officially hit "rock bottom?" As noted throughout the year, the naturally rate-sensitive commercial and residential real estate markets remain an easy transmission mechanism - or "punching bag" - of the Federal Reserve's historically swift monetary tightening cycle. Pressured by the surge in interest rates through multi-decade highs, REITs enter earnings season on a skid, with the Equity REIT Index back near its lowest levels since May 2020. Climbing to fresh two-decade highs this week, the benchmark 10-Year Treasury Yield is higher by over 100 basis points from the start of the last earnings season in mid-July. The Vanguard Real Estate ETF ( VNQ ) is lower by roughly 7.4% on a price return basis this year (-4.5% total returns) on the year, while the Mortgage REIT Index is lower by 2.5% (+3.5% on a total return basis). Within the real estate sector, just 4-of-18 property sectors are still in positive territory on the year, led by Data Center, Single-Family Rental, and Healthcare REITs, while Cell Tower and Specialty REITs have lagged on the downside.

{kind=link}

Before diving into the specific sector-by-sector metrics we're focused on this earnings season, we discuss the three higher-level themes that we're focused on this earnings season:

- 'Higher for Longer' Effects

- Guidance Updates & Initial 2024 Outlook

- Dividend Policy & Capital Deployment

1) 'Higher for Longer' Effects

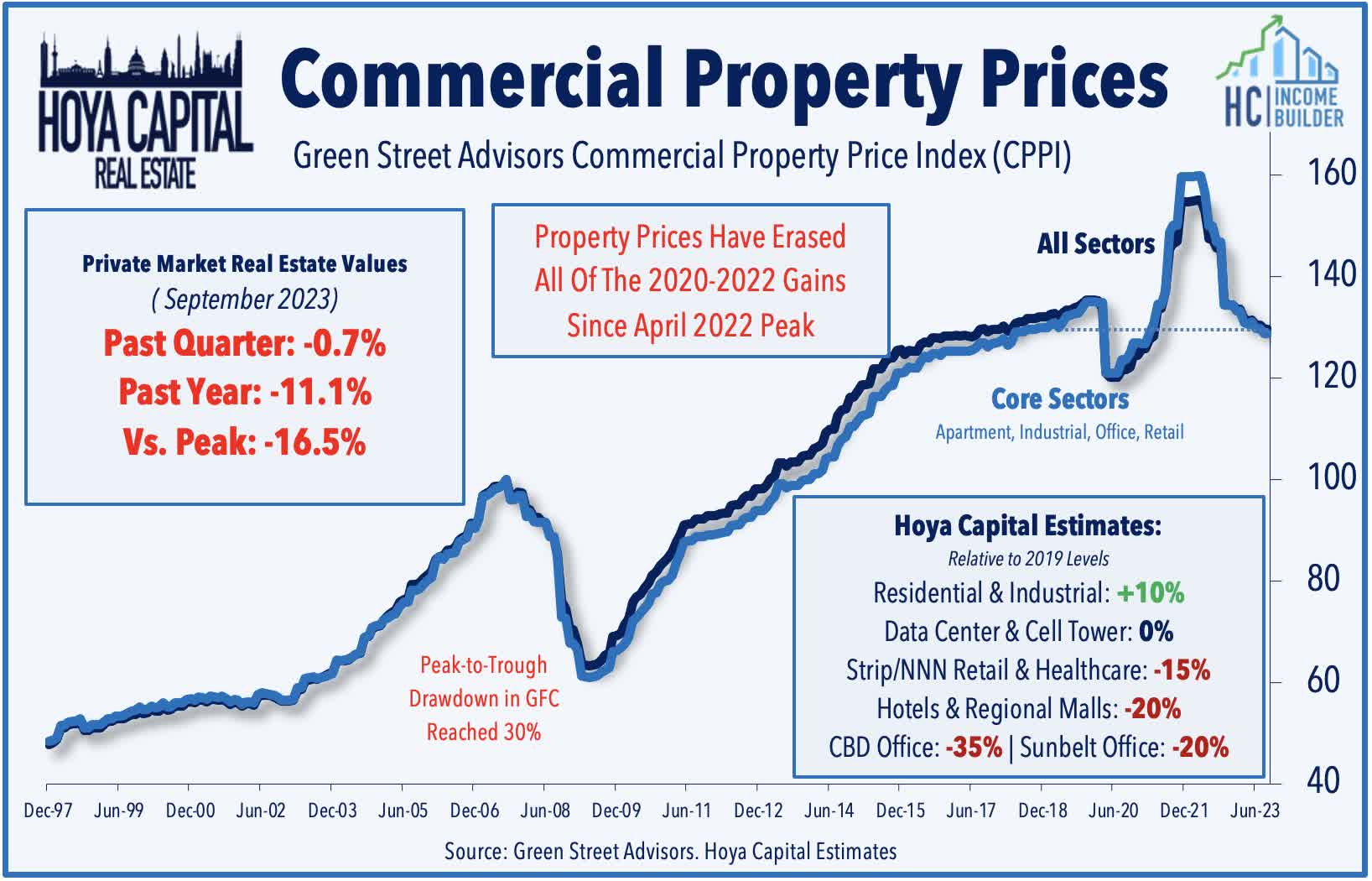

While many public REITs have best-in-class balance sheets, even the most well-capitalized real estate owners have been unable to escape the gravitational force of the "higher for longer" environment, and we're keyed-in on commentary regarding any shifts in strategy or sentiment related to this higher interest rate regime. Green Street Advisors' data shows that private-market values of commercial real estate properties have dipped by 16.5% from the April 2022 peaks - giving back all of their pandemic-era gains - but the pace of the declines had started to flatten out this summer as interest rates appeared to be stabilizing. We expect that the latest surge higher in rates will put further downward pressure on property valuations - likely another 5% at least - that will be revealed in the data in the months ahead, bringing the peak-to-trough decline to over 20%. By comparison, the peak-to-trough decline during the Great Financial Crisis reached roughly 30%.

{kind=link}

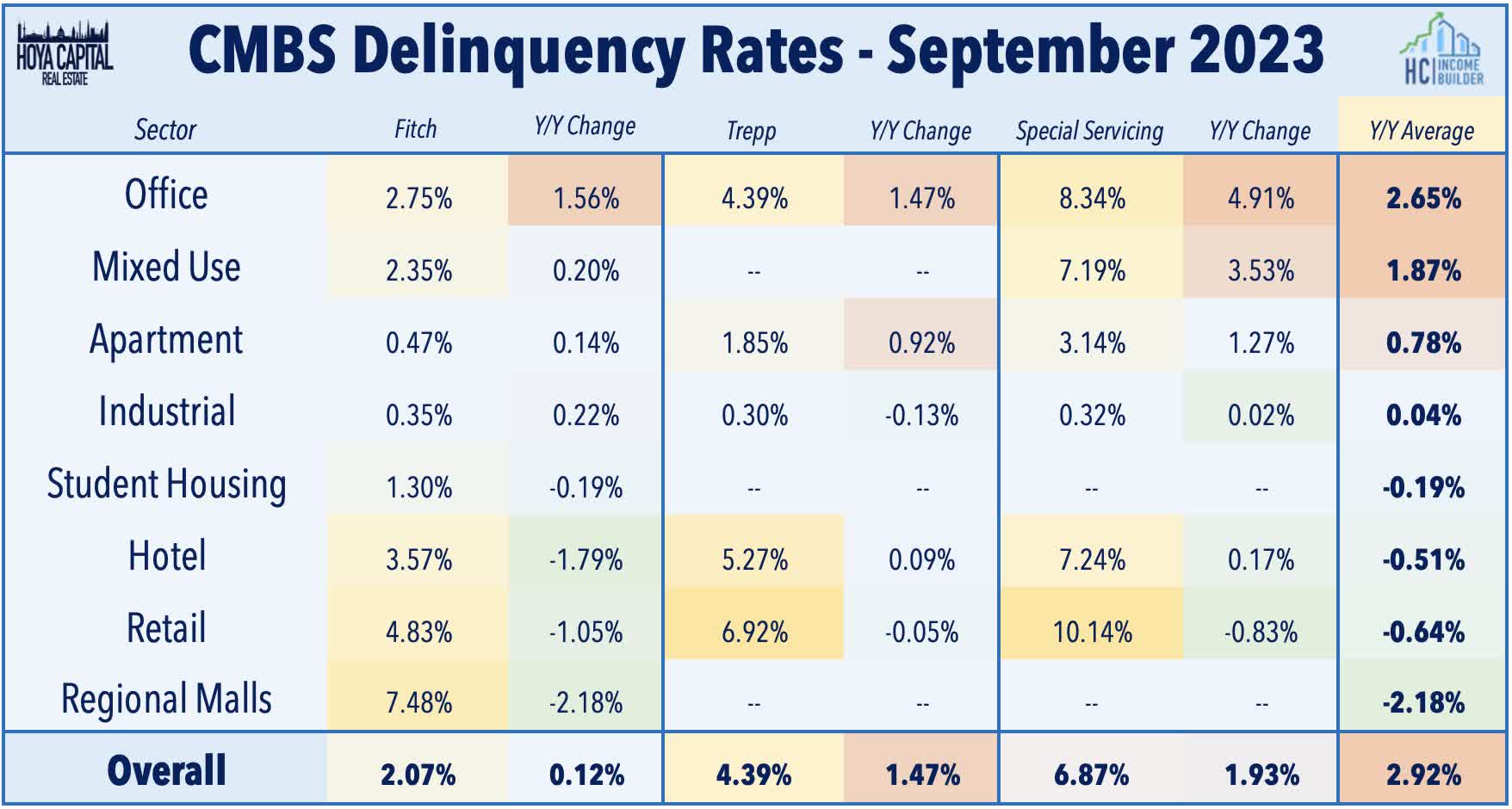

As noted in our State of the REIT Nation report, the business models of many private equity funds and non-traded REITs were not designed for a period of sustained 5%+ benchmark rates or double-digit declines in property values. Distress has generally remained isolated to the most debt-burdened private market portfolios, but the refinancing clock is ticking ever louder, especially for operators with significant variable rate debt exposure. The Mortgage Bankers Association's 2022 Loan Maturity Survey showed that roughly a third of commercial mortgages mature by the end of 2024. Trepp reported last week that CMBS delinquency rates rose to 4.39% in September, up 147 basis points from last year. Trepp also reported that its CMBS Special Servicing Rate - a more high-frequency measure that includes loans at high risk of default - rose to 6.87% in September, up sharply from below 2% at the same time last year. The office sector has accounted for the vast majority of this increase, however, with its delinquency rate roughly doubling over the past year. Apartment and industrial distress has increased slightly, while hotel and retail delinquency rates have actually declined over the last year.

{kind=link}

2. Guidance Updates & Initial 2024 Outlook

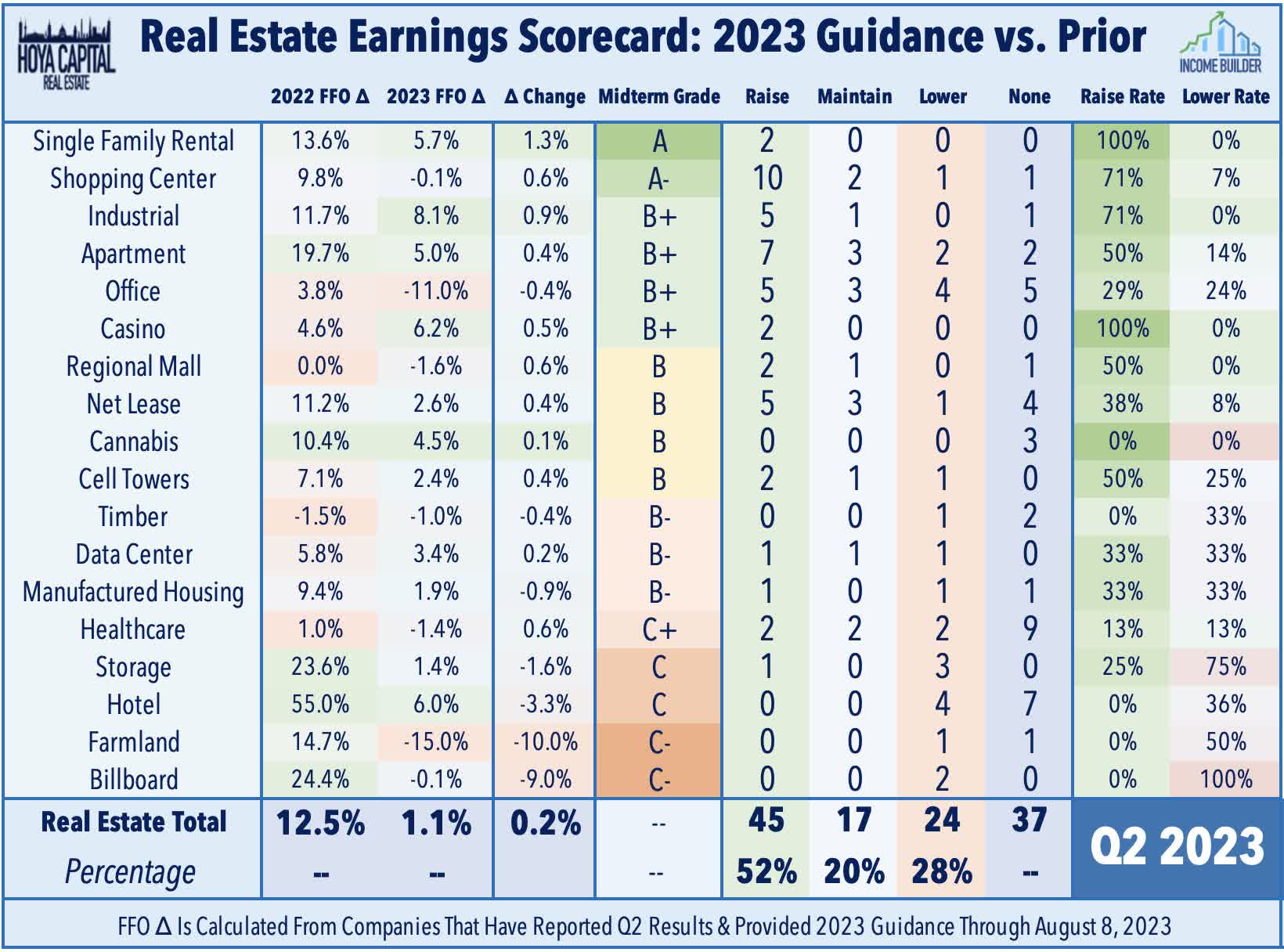

Property-level fundamentals have remained surprisingly resilient across most property sectors this year - notably in the residential, retail, and logistics sectors - but we're looking for any early signs of cracks or any indication of a shift in sentiment. We expect the most earnings season volatility in sectors with shakier fundamentals, notably coastal office, public-pay healthcare, and mortgage REITs. We're keyed in on these REITs' full-year 2023 guidance updates and expect to see a handful of REITs provide preliminary 2024 metrics as well. Of the 86 equity REITs that provided full-year Funds from Operations ("FFO") guidance in the second quarter, 52% raised their full-year earnings outlook (down from 63% in Q1), while 28% lowered guidance (up from 18% in Q1). The third quarter historically sees the highest rate of guidance increases, but we expect that the interest rate headwinds will offset this typical seasonal tailwind, and expect an FFO "raise rate" around 50%.

{kind=link}

Last quarter, earnings "misses" and downward earnings revisions were driven predominately by elevated debt servicing expenses, underscoring the continued challenges facing more highly leveraged real estate portfolios from the higher rate environment. These more debt-heavy REITs will be under the microscope this quarter, as will REITs that downwardly revised guidance last quarter due to demand softness, notably in the billboard and storage sectors. We again expect property-level Net Operating Income ("NOI") guidance to be stronger than corporate-level FFO guidance, given the tailwinds related to the moderation in inflationary pressures since most REITs provided their initial expense outlook. The more labor-intensive sectors - including hotels, residential, and senior housing - have the most potential upside from a moderation in inflationary expense pressures, and we observed last quarter that most REITs were trending below their full-year expense outlook.

{kind=link}

3) Dividend Policy & Capital Deployment

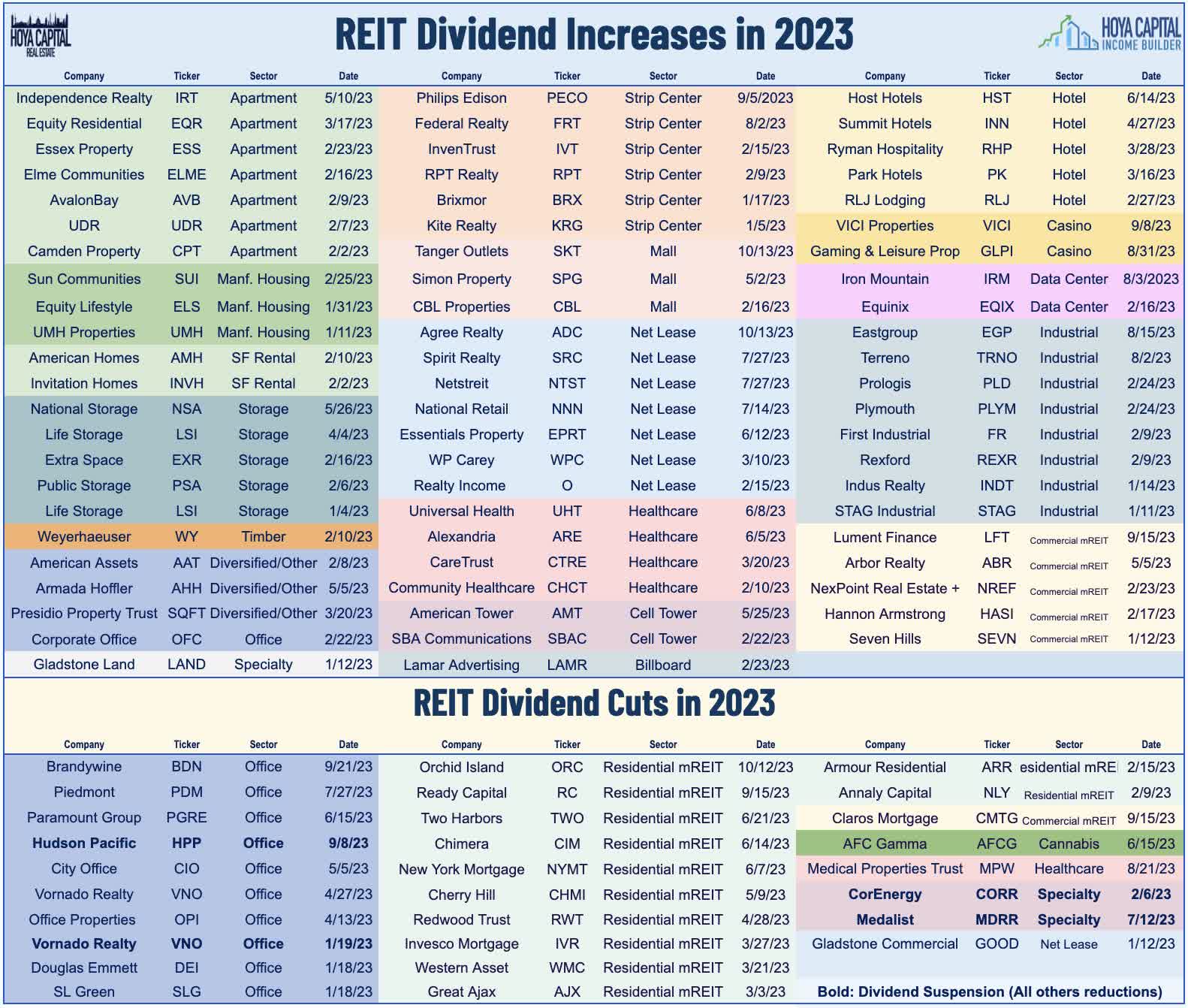

Following a record-setting pace of over 120 REIT dividend hikes in the prior two years, another 68 REITs have raised their dividend this year - trending at about 75% of the pace of the prior two years. 28 REITs have lowered their payout - up from a total of under 10 in each of the prior two years. While sector-level dividend coverage ratios remain quite healthy with an average payout ratio of around 70% - slightly below the long-term historical average - dividend commentary will be a major focus for office and mortgage REITs - the sectors that have been responsible for essentially all of the 28 dividend reductions so far this year across the REIT sector. We believe that the "bleeding" in these sectors from a dividend cut perspective is largely contained at this point, but the surge in interest rates makes us less optimistic that we'll see additional headway on dividend increases in the back-half of this year.

{kind=link}

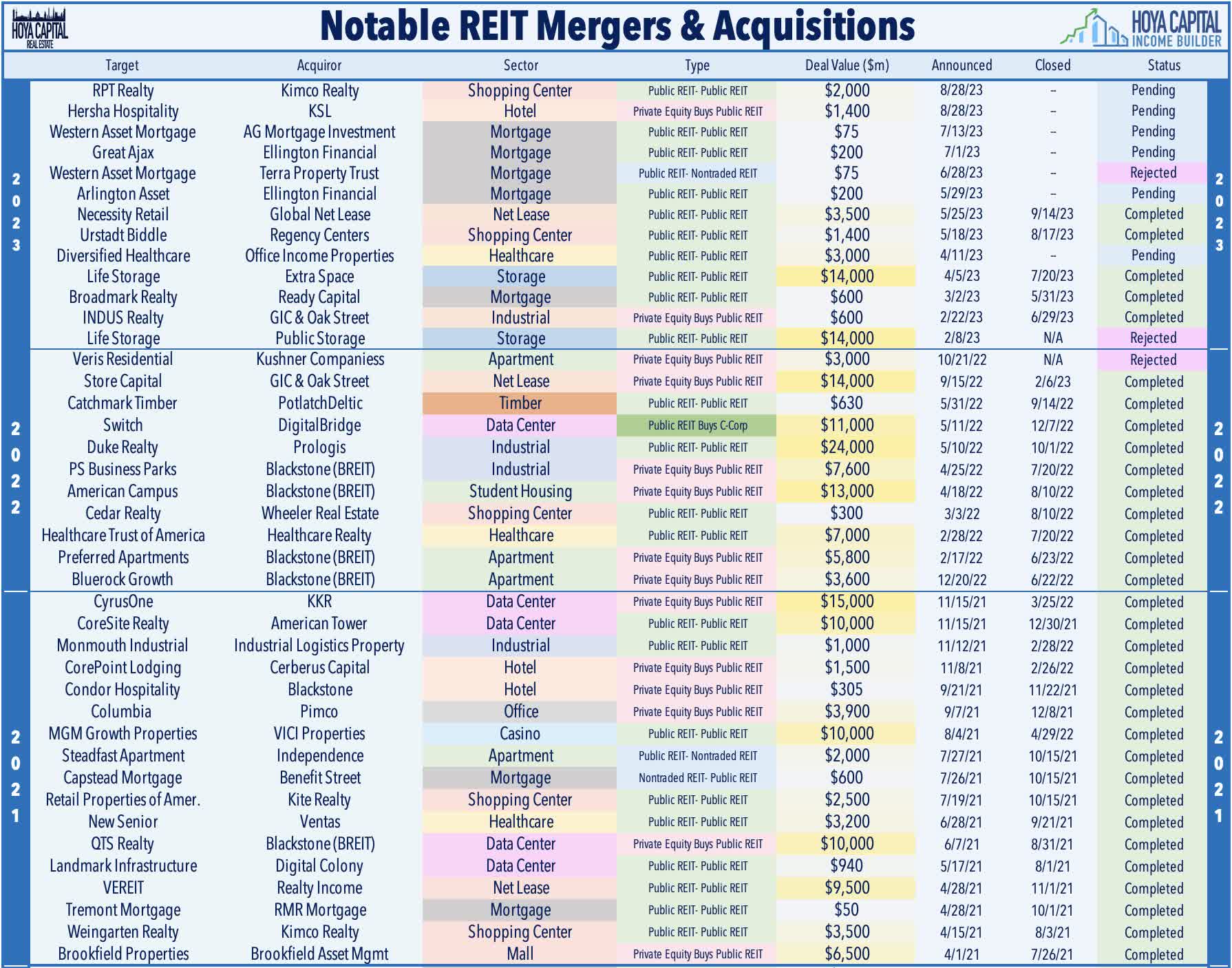

With an average dividend yield of around 4.5% already - a sizable premium to the S&P 500 dividend yield of roughly 1.6% - REITs have been more inclined to deploy free cash flow towards balance sheet reinforcement (or "repair" for some with elevated levels of variable rate debt). REITs with enough existing balance sheet firepower have looked within the public markets for external growth opportunities, fueling a notable surge in public REIT-to-REIT consolidations this year - and conditions are ripe for this type of activity to continue. Activity this year has been headlined by the merger between two of the four largest self-storage REITs Extra Space ( EXR ) and Life Storage, and by Regency Centers' ( REG ) acquisition of fellow strip center REIT Urstadt Biddle . Markets have generally been receptive to these moves, and we expect several additional small and mid-cap REITs that trade at size-related discounts to be picked-up by larger peers. We've also seen a handful of mortgage REIT mergers in recent months as well - activity that has also been well-received given the steep Book Value discounts.

{kind=link}

Residential Real Estate Earnings Preview

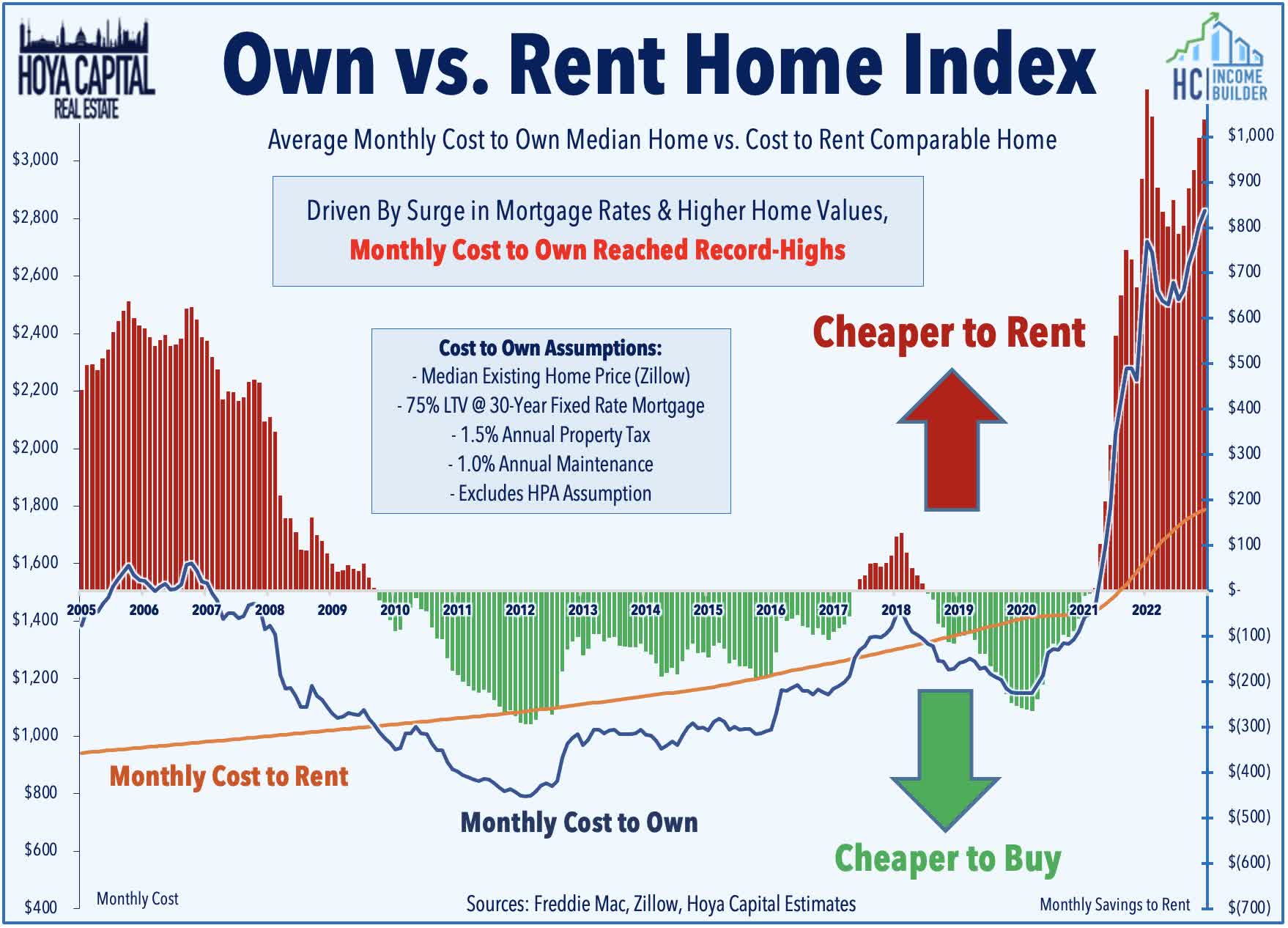

Apartments : The state of the U.S. housing market will be a critical focus throughout earnings season - the industry that has felt the most direct effects from the historically swift monetary tightening cycle that began in mid-2022. Sentiment around apartment REITs has generally improved throughout the year as recent industry data has shown a stabilization in rental rate and occupancy trends since bottoming in January, with rent growth appearing to stabilize in its typical "inflation-plus" range between 3-5%. Supply concerns have been the unabating refrain from 'bears' over the past decade of outperformance - which has weighed on Sunbelt REIT valuations. While the multifamily pipeline is historically large, overall housing development remains below equilibrium levels, and tighter financing conditions have curbed groundbreaking. We'll be closely watching rent growth metrics on new and renewed leases and anticipate upside NOI revisions will be driven by an improved expense outlook, driven in the near-term by lower utilities expense.

{kind=link}

Single-Family Rentals : Buoyant rent growth has been particularly apparent across the single-family rental sector, which is not facing the same supply headwinds as the multifamily side - and is enjoying a mild tailwind from the rate-driven affordability constraints on ownership markets. We're expecting a strong quarter for property-level fundamentals, aided by a cooling of expense headwinds. Negative home price appreciation and tighter credit conditions quickly neutralized the pockets of speculative housing market activity - including the "fix-and-flips" and highly-levered short-term rental ("STR") startups that were beginning to fizzle in 2021 and 2022, an environment that made it difficult for SFR REITs - or any large-scale institution - to accretively add to their portfolios. As a result, the institutional SFR industry has been especially quiet in recent quarters following a frenzy of activity in prior years. In addition to rent growth metrics, we're interested in commentary about these external growth prospects - specifically, whether these REITs are beginning to see any pockets of private-market distress that could be ripe for the picking.

{kind=link}

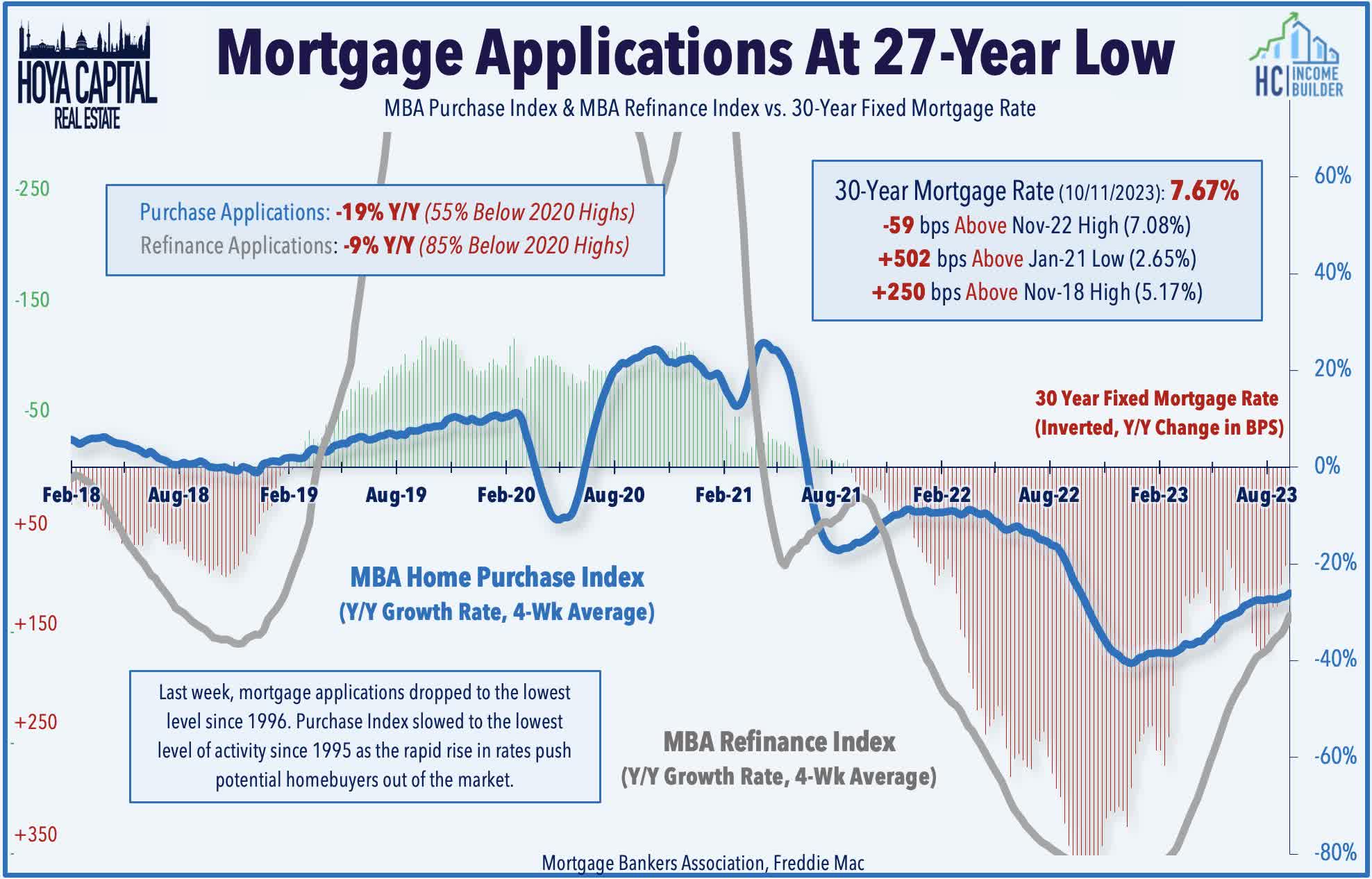

Homebuilders : It's all about rates: the U.S. housing industry started to emerge from its year-long recession during the summer - thawing from a deep freeze induced by historically aggressive monetary tightening - but the resurgence in mortgage rates to three-decade highs has again sapped the momentum. Historically low inventory levels of existing homes have kept a floor on home values - preventing the type of cascading issues that prompted the GFC meltdown - and has provided a narrow avenue for the largest homebuilders to effectively "corner the market" as the lone source of housing inventory in many high-demand markets. We continue to believe that higher mortgage rates have delayed - but not permanently altered - the existing secular fundamentals supporting the single-family market: a "lost decade" of single-family construction ahead of a wave of demographic-driven demand. The sharp slowdown in housing activity and home prices was necessary to avoid a painful correction, but don't expect a return to the "boom times" either. We're focused on net orders and cancellation rates to see if we're headed for a repeat of the rate-driven downturn seen in 2022.

{kind=link}

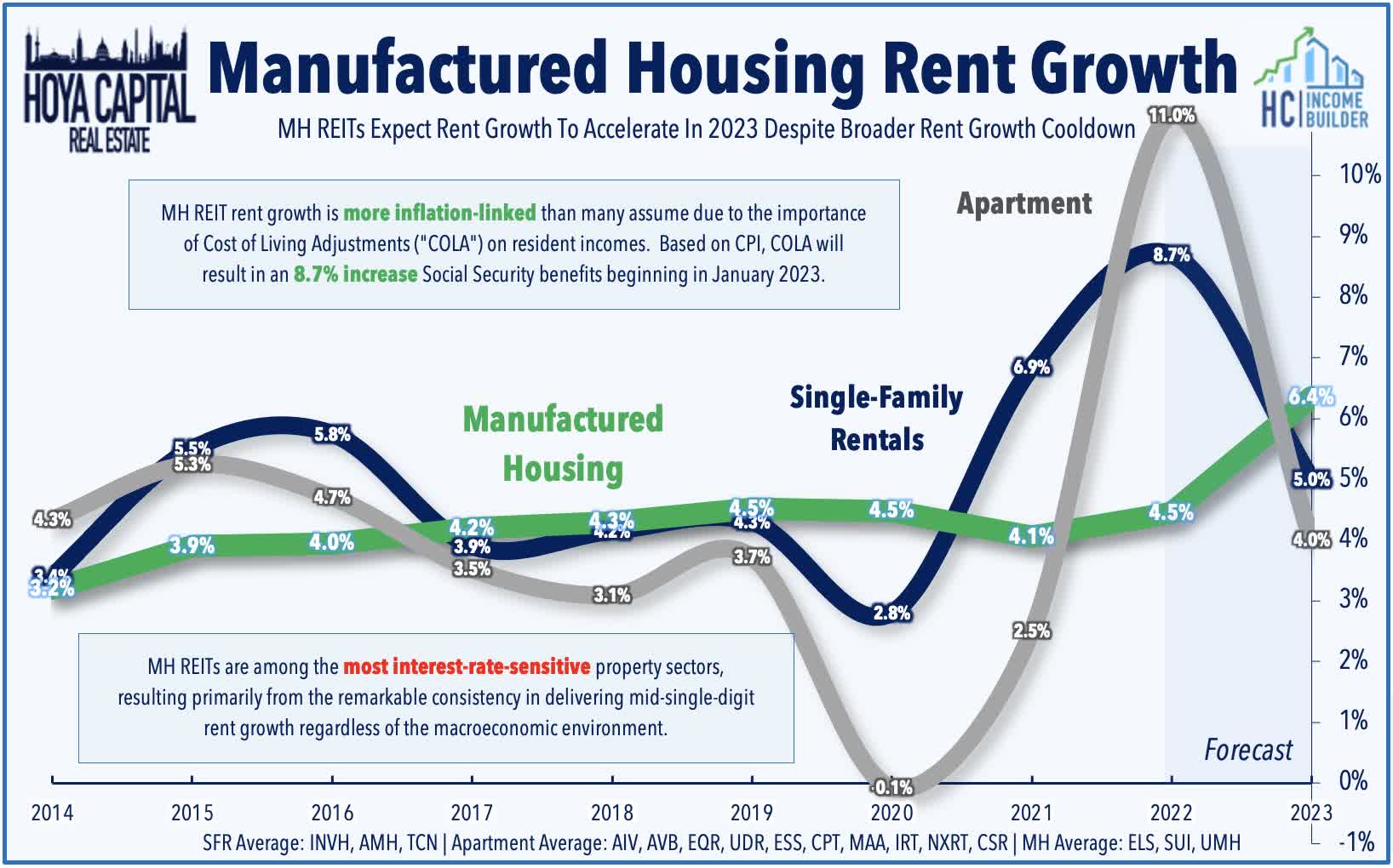

Manufactured Housing: Equity LifeStyle ( ELS ) kicked-off earnings season on Monday with a solid report. ELS maintained the midpoint of its full-year FFO outlook - which calls for full-year FFO growth of 6.3% - as strength in its core manufactured housing ("MH") segment offset continued weakness in its transient recreational vehicle ("RV") segment. ELS maintained its full-year outlook for MH same-store revenue growth at 6.8%, but downwardly revised its RV & Marina outlook to 3.8% - lower by 80 basis points - as seasonal and transient RV revenues were down over 10% from last year, pressured by rising fuel prices and a post-pandemic normalization in RV utilization. Excluding the struggling transient RV component, full-year revenues in the RV & Marina segment are expected to increase 8.6%. ELS also noted that it will begin sending renewal offers to its MH residents this month for the 2024 period, with average rent increases of 5.4%. ELS has set annual rates on 95% of its annual RV sites, with average rent increases of 7.0%.

{kind=link}

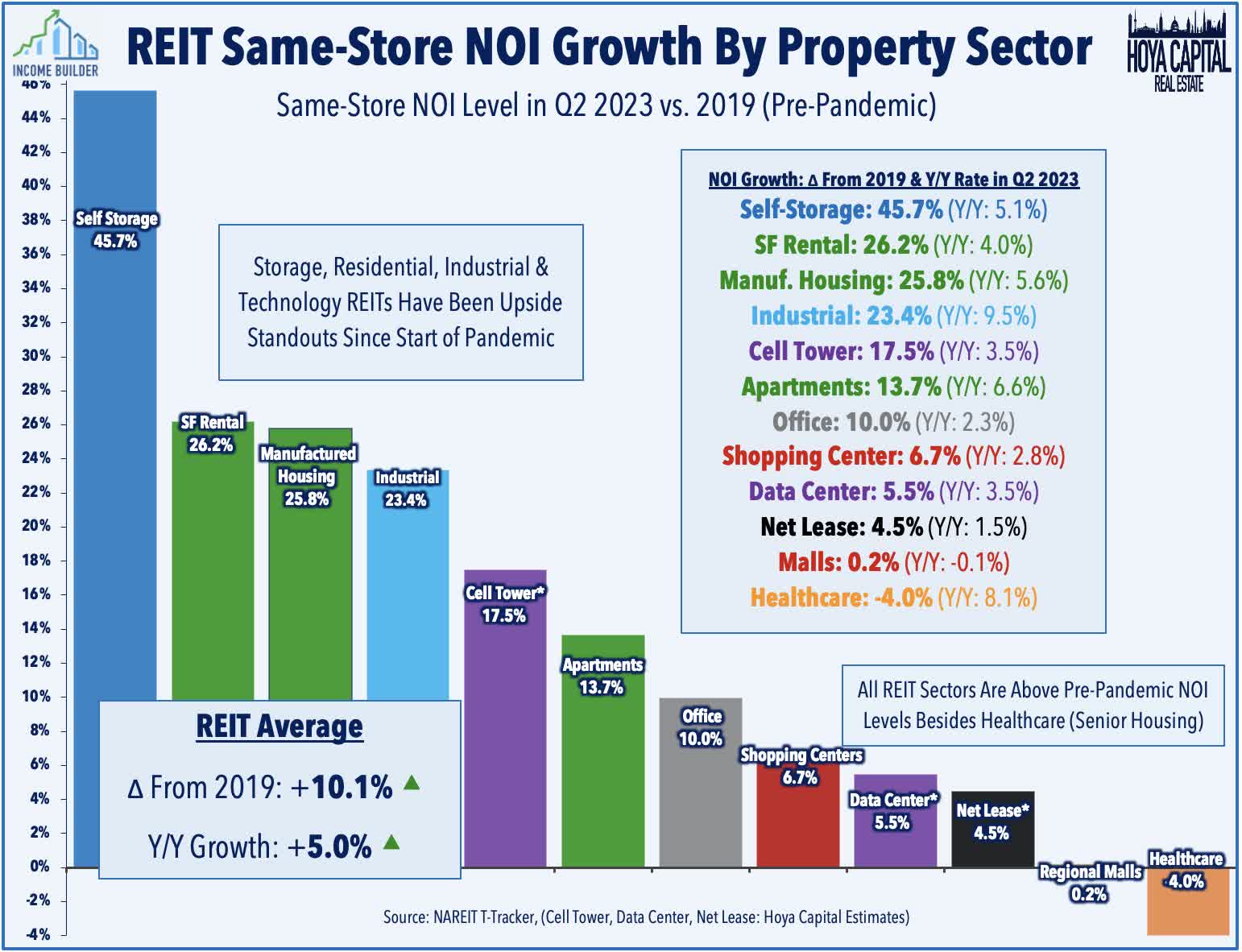

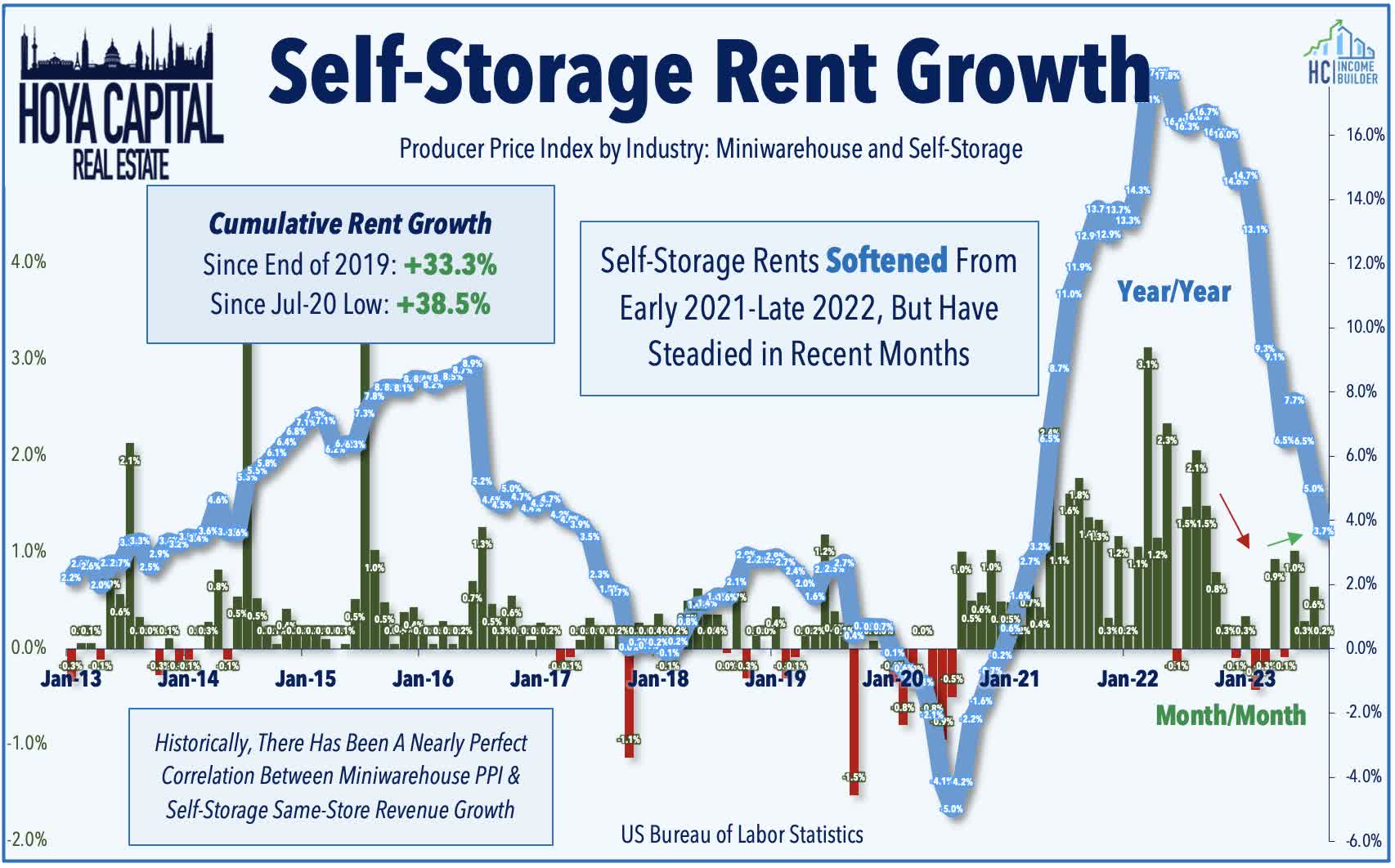

Self-Storage: The sector with the strongest aggregate NOI growth since the start of the pandemic, self-storage REITs have stumbled over the past quarter following a weak slate of Q2 reports in which three of the four REITs lowered their full-year FFO and NOI outlooks. All four self-storage REITs reported double-digit declines in "street rates" on new customers in Q2, but this pricing weakness was offset by high-single-digit rent growth on renewal leases, resulting in a total rent PSF increase of about 6.5% during the quarter compared with last year. Given that storage demand is driven largely by housing activity – specifically, home sales and rental market turnover - demand headwinds are expected to continue in the final months of 2023. Recent PPI data indicates that self-storage rent growth has continued to moderate from the surge seen from early 2021 through mid-2022, but stayed in positive territory month-over-month throughout the summer after posting sequential declines in four-of-six months from December 2022 to May 2023.

{kind=link}

Hotel & Casino REIT Earnings Preview

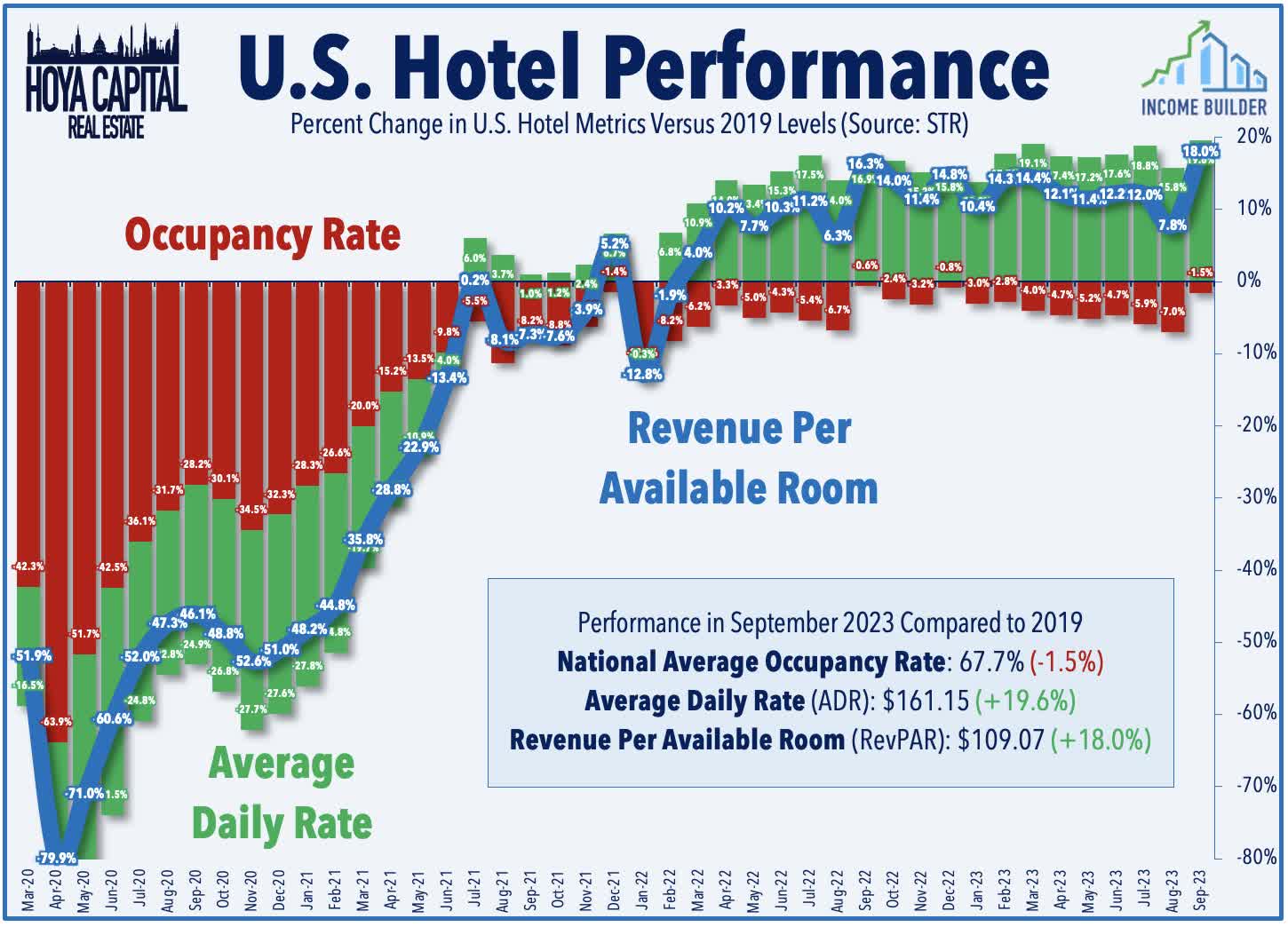

Hotels : Despite a pull-back in recent weeks after the terrorist attacks in Israel, hotel REITs are still pacing for a second-straight year of outperformance, buoyed by steady post-pandemic operating improvement and the long-awaited return of dividends. Domestic travel recovered to pre-pandemic levels in early 2023 and has - somewhat surprisingly - held-up around these record-high levels throughout the year. Business and group demand has marginally improved, offsetting some moderation in leisure demand, while international travel demand has started to provide a tailwind as the final pandemic-era travel restrictions were lifted in May. We're expecting a strong quarter from hotel REITs, as recent TSA Checkpoint data shows that throughput climbed to 104.1% of 2019-levels in September - the highest since the pandemic - and has averaged 102.5% thus far in October. Hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was roughly 12% above 2019 levels during the third quarter, as a roughly 18% relative increase in Average Daily Room Rates ("ADR") offset a roughly 5% relative drag in average occupancy rates.

{kind=link}

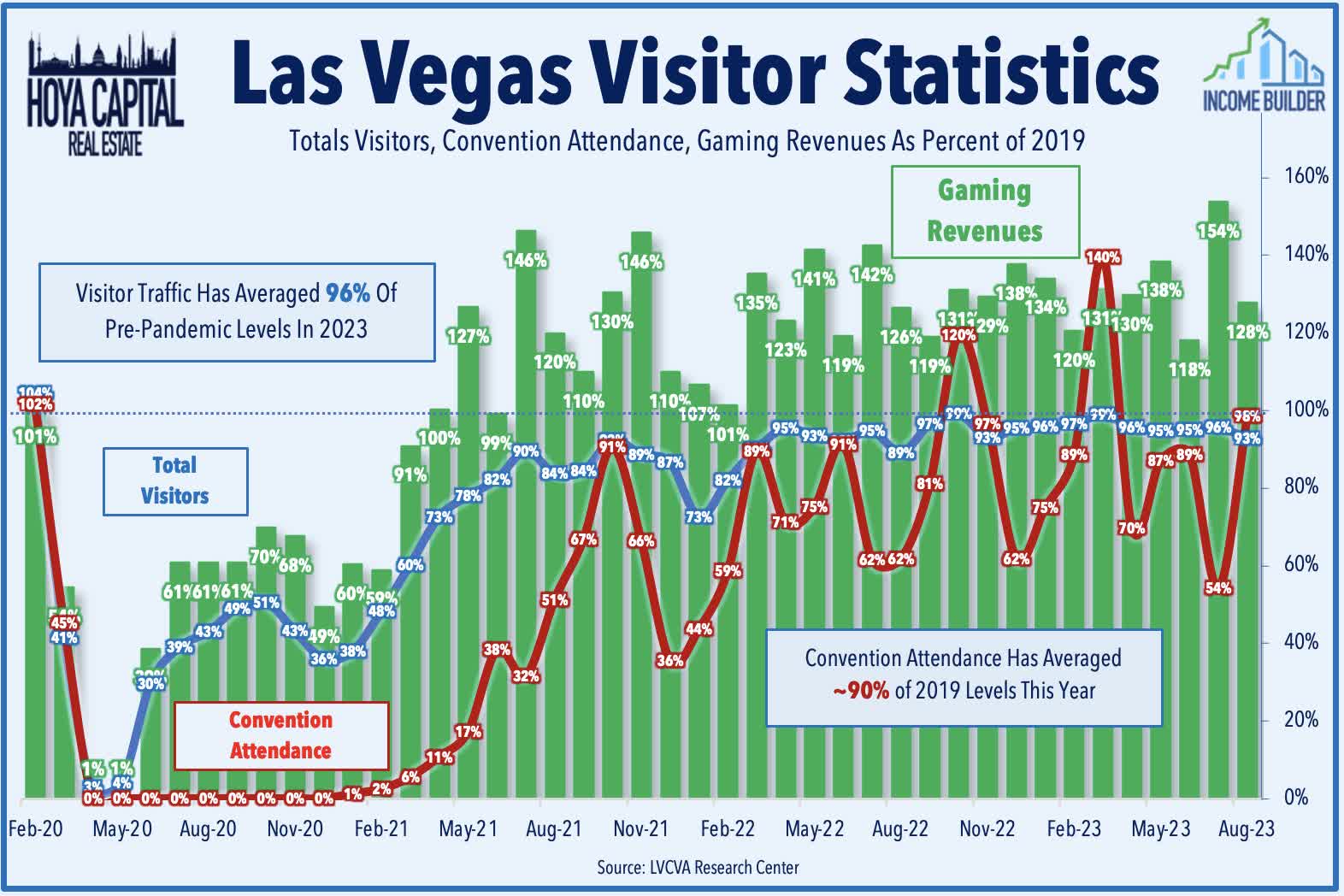

Casinos : Heralded last year for their inflation-hedging characteristics, casino REITs have faced the other side of that trade this year as inflation normalizes from the four-decade highs seen last year, but have closed their underperformance gap in recent months following a strong Q2 earnings season in which both REITs raised their full-year FFO guidance. M&A opportunities will again be the focus of both REITs' earnings calls following Blackstone's partial sale of the Bellagio to Realty Income ( O ) last month. VICI Properties ( VICI ) noted last quarter that Las Vegas is continuing to see robust demand trends - momentum that has continued in recent months per the latest LVCVA data - and noted that regional casinos are performing well "as the high-value consumer segment remains healthy." Gaming and Leisure Properties ( GLPI ) - which has been quiet on the M&A-front since last June - noted last quarter that tighter credit conditions have made it difficult to source new deals.

{kind=link}

Tech and Industrial REITs Earnings Preview

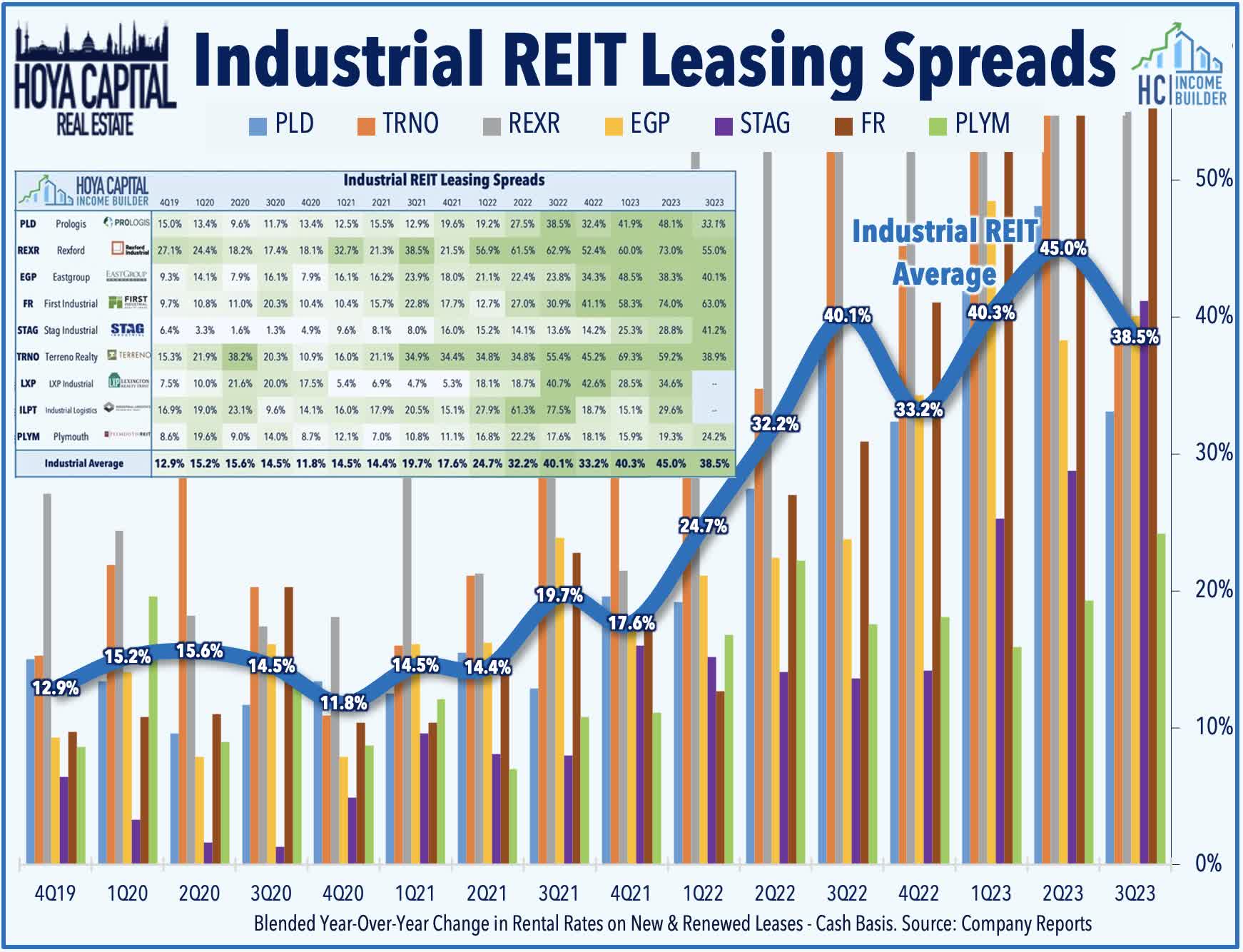

Industrial : Following their worst year of performance on record in 2022, industrial REITs been among the better performers this year after results in the first half of the year showed a surprising re-strengthening of property-level fundamentals following a moderation in the back-half of 2022. Prologis ( PLD ) kicked off earnings season this week with another solid "beat and raise" results, but reiterated its expectation that elevated supply growth will negatively impact market fundamentals in the coming quarters. Interestingly, this cautious commentary was nowhere to be seen in the third-quarter metrics or the updated full-year outlook, which continued to reflect extremely strong supply/demand conditions for logistics space, especially in the United States. Fueled by a record-setting cash re-leasing spread of 54.2% - led by a 63.1% increase in the U.S. - PLD raised both its full-year FFO and NOI outlooks as well as its occupancy forecast. PLD now sees FFO growth of 10.4% this year - up 20 basis points from its prior forecast - and expects NOI growth of 9.9% - up 10 basis points from last quarter. Prologis also upwardly revised its forecasted spending on development starts and acquisitions. PLD expects completions to outpace net absorption by 150-200M square feet over the next three quarters but expects that trend to reverse by mid-2024, with demand exceeding supply by 75-125M SF in the following three quarters.

{kind=link}

Cell Towers : Cell Tower REITs have been the weakest-performing property sector since the start of 2022 – lagging even the battered office sector- amid a telecommunications industry-wide slump inflamed by tight monetary conditions. Cellular carriers have curbed their capital-intensive network expansion plans in recent quarters following a significant wave of investment and tower equipment upgrades from 2019-2022 to deploy nationwide 5G networks. Apart from the interest rate headwinds, industry headwinds are rooted in the ongoing disintermediation of legacy wireline business segments towards fully wireless deployments and the mounting competition on the two industry juggernauts from within the wireless industry itself via T-Mobile, Amazon, and Dish. We're focused on commentary regarding carrier network investment and any movement among these new entrants.

{kind=link}

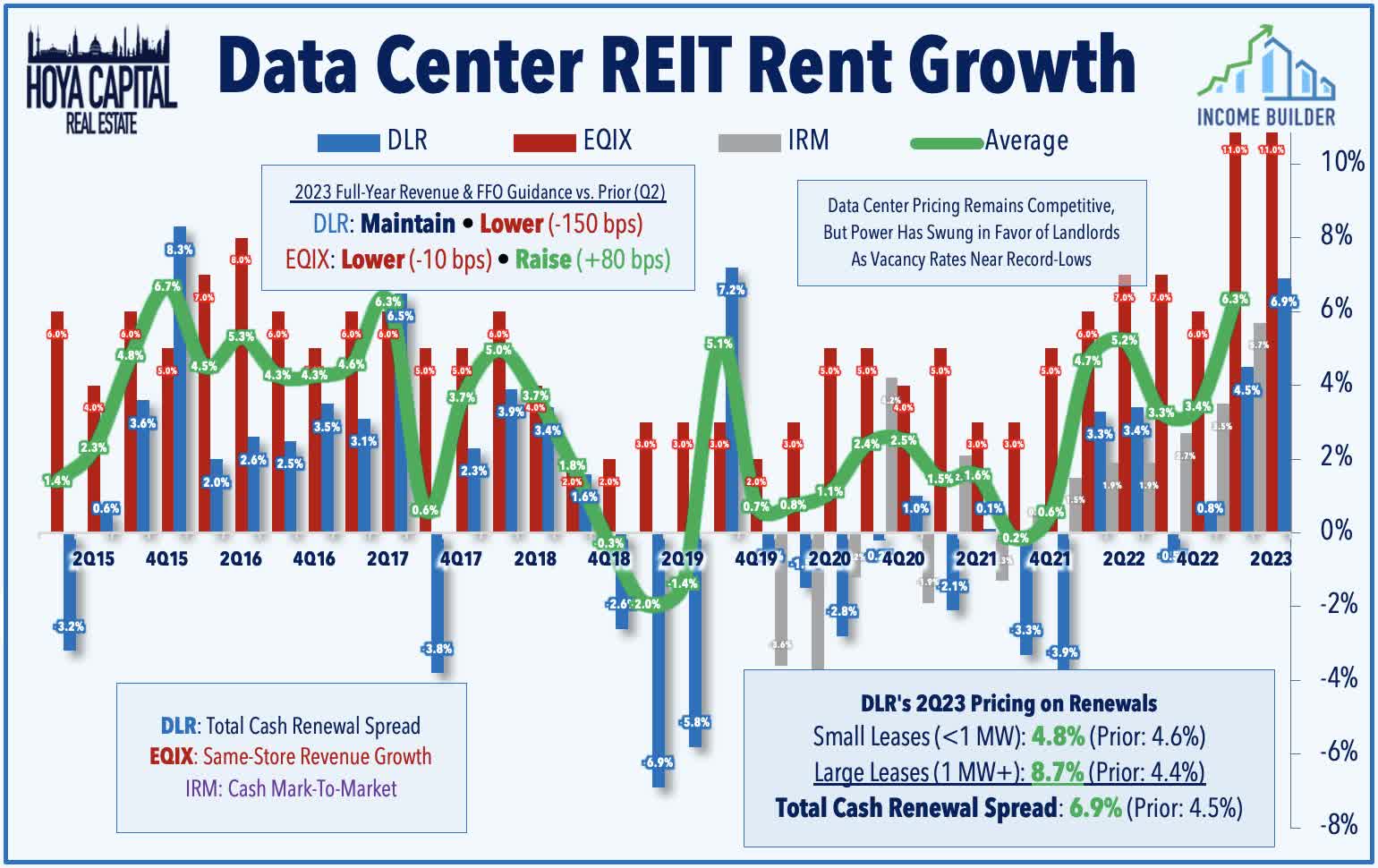

Data Center : The top-performing property sectors this year, the Data Center REIT rebound has been augmented by reports of "booming" demand for artificial intelligence ("AI") focused data center chips. Ironically, this AI-wave comes just as Data Center REITs became a trendy “short” idea centered on a thesis of weak pricing power and competition from the "hyperscalers"- Amazon, Google, and Microsoft. A confluence of development bottlenecks - power shortages, higher cost of capital, supply chain constraints, ecopolitics, and NIMBYism - have created a more favorable dynamic and swung the pendulum of pricing power towards existing property owners. Barriers to supply growth combined with AI-accelerated demand should bring some sustained pricing power to a sector long-burdened by near-unlimited supply. With negotiating power tilting back towards landlords, there appears to be enough economic value to be shared. We'll again watch renewal pricing trends and leasing volumes closely this quarter.

{kind=link}

Retail REITs Earnings Preview

Strip Centers : Strip Center REIT fundamentals have improved materially over the past year and continue to be underappreciated in the market as a decade-long “retail apocalypse” narrative has been tough to shake. The combination of near-zero new development and positive net store openings since 2021 has driven occupancy rates to record-highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. These favorable property-level supply/demand fundamentals have translated into impressive double-digit rent growth spreads since mid-2022 and the best earnings “beat rate” of any property sector during that time. Despite several high-profile retail bankruptcies - including Bed Bath & Beyond and Party City - store openings have continued to outpace store closings by about 10% so far in 2023, led by demand for space in large-format open-air strip centers. We'll again be focused on leasing spreads and occupancy rate trends - which have been impressive of late - and on updates on re-lease progress at these vacated Bed Bath and Party City locations, in particular.

{kind=link}

Malls : With recent distress across office markets seizing the headlines, Mall REITs are no longer the "Problem Child" of the REIT sector, particularly after weaker players and lower-tier malls closed shop. Following three years of rental rate and occupancy declines, the supply-demand dynamic has recently favored retail landlords, which has helped these stumbling mall REITs regain some footing and repair balance sheets in anticipation of tougher times ahead. Traffic and sales levels at higher-end mall properties were back to pre-pandemic levels during the holiday season, but we're interested to see if this momentum continued into the third quarter, given the relatively softer trends seen in the Commerce Department's retail sales reports and the uptick in store closings announcements in recent quarters following the handful of bankruptcies noted above. We're focused on same-store occupancy rates this earnings season - which remained relatively soft last quarter despite improving NOI and FFO trends - and we want to see rental rates stabilize before we can officially call the bottom to the decade-long downward pressure on FFO.

{kind=link}

Net Lease : Net Lease REITs- one of the most "bond-like" and interest-rate-sensitive property sectors- have lagged in recent months as investors come to grips with a potential "higher-for-longer" interest rate environment. Thriving in the "lower forever" environment, the industry has been reluctant to acknowledge the higher-rate regime, keeping private-market values and cap rates surprisingly "sticky" and resulting in compressed investment spreads. Despite the tighter investment spreads, acquisition activity has slowed only modestly for some REITs- paying top-dollar for recent purchases - a strategy that could prove costly if rates remain elevated. "Do less." Strong balance sheets and limited variable rate debt exposure had afforded these REITs the ability to be patient until the price is right, but while some REITs have exhibited prudence, others have plowed ahead with acquisitions or - in the case of W. P. Carey ( WPC ) - initiated poorly-received pivots. WPC's earnings call will be one of the most closely-watched this earnings season. More broadly, we're focused on commentary regarding cap rate movements in early 2023 for a read on whether private market asset owners are holding tight or ready to adjust price expectations to the reality of higher benchmark rates.

{kind=link}

Office & Healthcare REIT Earnings Preview

Office : The battered Office REIT sector has been among the better-performing sectors since June, lifted by a decent slate of earnings reports and recent indications that the long-awaited "Return-to-Office" is gathering momentum. Debt service expenses have been the primary culprit behind the wave of recent loan defaults on coastal office properties from private equity firms Brookfield, Blackstone, and PIMCO, but the question remains whether there's any value in being the best house in a bad neighborhood or whether the downward inertia and spiraling effect on prices eventually drags even the better-capitalized players into the sinkhole. The office outlook isn't as bad as market pricing reflects, but it's not necessarily good either, particularly for the highly-levered players and those focused in markets with long transit-heavy commutes. It's all about the commute: Work From Home ("WFH") is ultimately an 'economic' decision and several major markets (SF, NYC, CHI, DC) have an unavoidable structural issue: it takes too long to get to work - largely a byproduct of decades of bad housing policy and urban planning. Coastal-focused office REITs are no longer trading at deep discounts, but these discounts are still available for a handful of Sunbelt-focused REITs, which are better-positioned in markets with net population growth, shorter commute times, and a more favorable industry mix for the WFH era.

{kind=link}

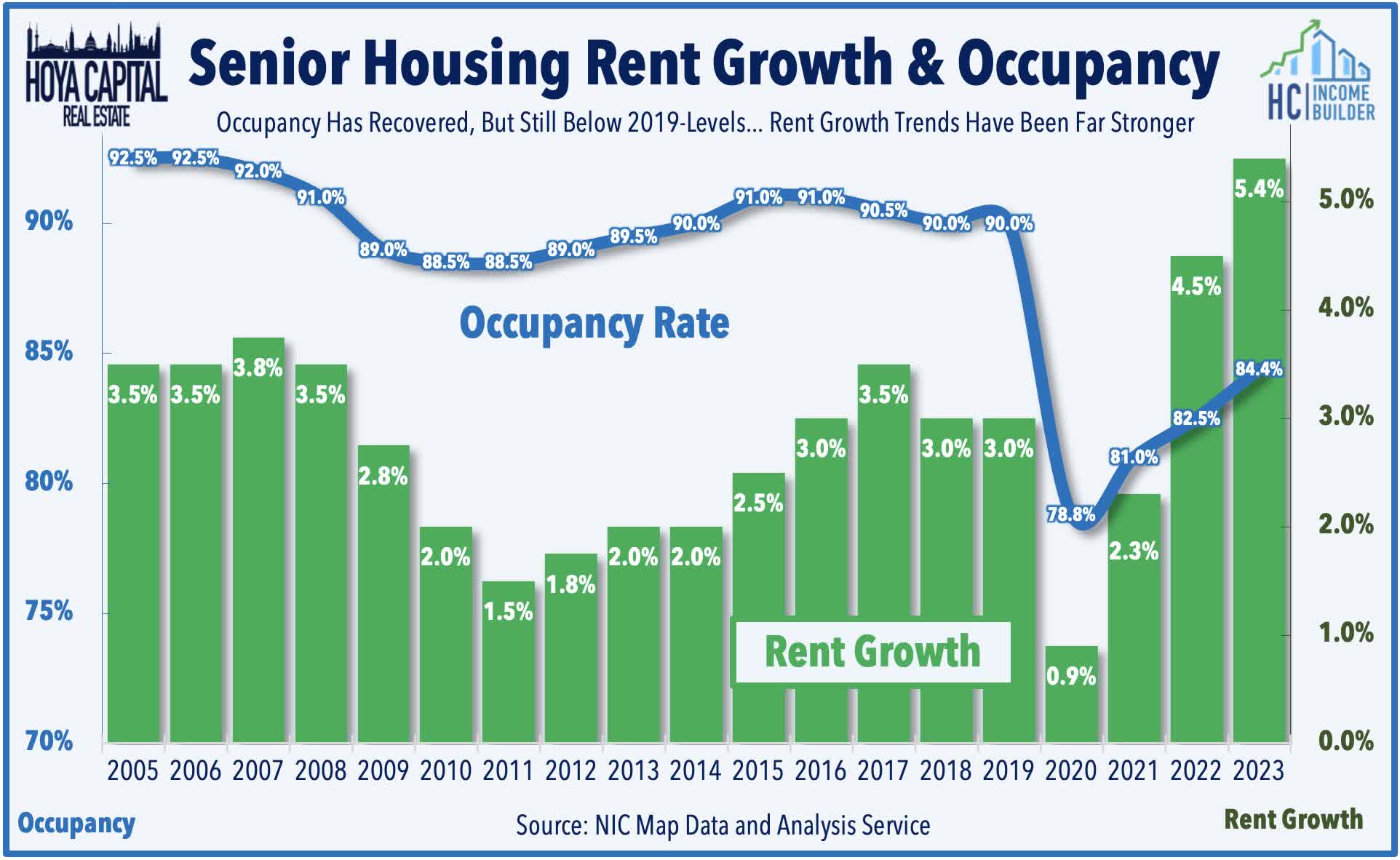

Private-Pay Healthcare : For Senior Housing REITs, the long-awaited recovery is finally taking hold. Robust rent growth is being fueled by rising resident incomes from record-high Cost-of-Living-Adjustments (“COLA”) to Social Security benefits. Welltower ( WELL ) and Ventas ( VTR ) have been among the best performers this year, buoyed in recent weeks by NIC data showing that the senior housing occupancy rate increased to 84.4% in the third quarter, continuing a slow-but-steady rebound from its pandemic lows of 77.8%. While occupancy rates remain below the pre-pandemic levels of around 90%, rent growth has averaged over 5.5% this year, strength that has been fueled, in large-part, by the nearly-9% increase in social security benefits, which has allowed SH owners to push rent increases. Positively for senior housing REITs, supply growth has finally cooled following a decade of elevated inventory growth, as NIC reported that units under construction amounted to 4.9% of total inventory, which is the lowest seen since 2014. Results from lab space owners Alexandria ( ARE ) and Healthpeak ( PEAK ) will be closely watched for updates on tenant health and leasing volume.

{kind=link}

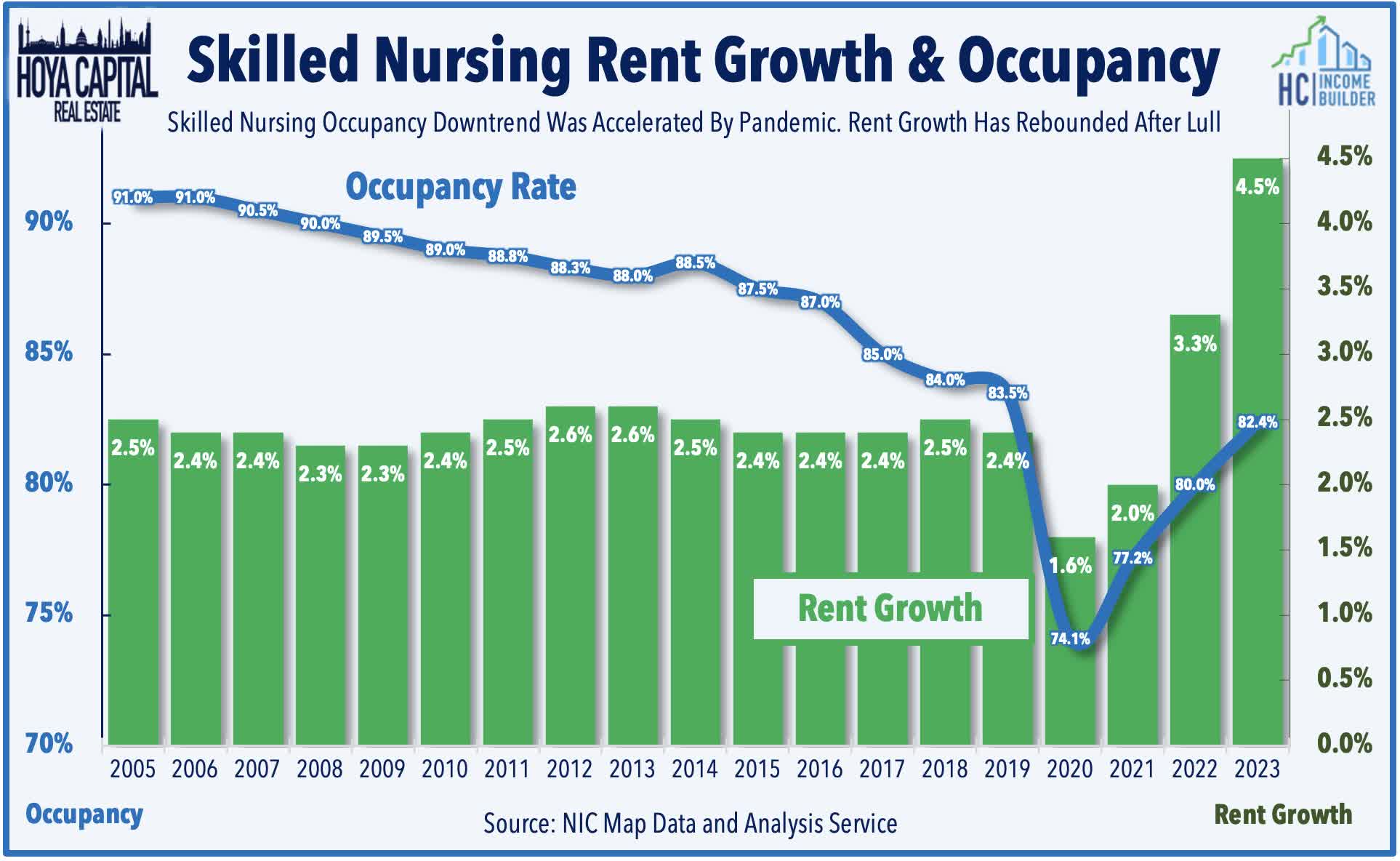

Public-Pay Healthcare : Public-pay segments- Hospital and Skilled-Nursing- have seen a re-intensification of tenant operator issues amid pressure from soaring labor costs and waning government support, triggering some missed rents and lease renegotiations. Gibbins Advisors reported early this year that bankruptcy filings for healthcare companies nearly doubled in 2022 compared to the prior year, which it attributes to this “COVID hangover” resulting from waning government support and higher labor costs. Medical Properties Trust ( MPW ) - which remains in the cross-hairs of short-sellers - has been a laggard this year, with tenant concerns still in focus. Skilled nursing REITs Omega Healthcare ( OHI ) and Sabra Health Care ( SBRA ) have also reported lingering rent collection difficulties from a handful of struggling operators, but also highlighted some progress over the past two quarters in restructurings. Tenant health - and resulting dividend sustainability is the primary focus of earnings season for these public-pay healthcare REITs.

{kind=link}

Key Takeaways: Real Estate Earnings Preview

Seemingly as "unloved" as any asset class, REITs enter earnings season on a skid, with the Equity REIT Index back at its lowest levels since May 2020 and Price-to-FFO valuations below the Great Financial Crisis era lows. While many public REITs have best-in-class balance sheets, even the most well-capitalized real estate owners have been unable to escape the gravitational force of the "higher for longer" environment. Property-level fundamentals have remained surprisingly resilient across most property sectors this year - notably in the residential, retail, and logistics sectors - but we expect post-earnings volatility in coastal office, public-pay healthcare, and mortgage REITs. Distress has generally remained isolated to the most debt-burdened private market portfolios in the weaker property sectors, but the refinancing clock is ticking ever louder for many debt-burdened private portfolios, which we expect will soon create potentially transformation opportunities for well-capitalized REITs similar to the most comparable macroeconomic period in the early 1990s - which spawned the 'Modern REIT Era' and a golden age for public real estate.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website

For further details see:

Earnings Preview: REITs At Rock Bottom