VLKPF - East 72 - Volkswagen: A Heavily Discounted Treasure Trove And Potential IPOs

2023-04-05 05:45:00 ET

Summary

- Volkswagen has an equity market capitalisation of ~€73billion, apportioned roughly 65/35 to ordinary and preferred shares.

- The analysis below suggests that it would not be a ludicrous outcome to value VWAGY equity at 2.5 times this current pricing.

- VW is a veritable treasure trove of assets; our methodology is to value the identifiable components.

- We believe VW trades at a 60% discount to a sum of the parts valuation.

The following segment was excerpted from this fund letter .

Volkswagen ( VWAGY )

VW has an equity market capitalisation of ~€73billion, apportioned roughly 65/35 to ordinary and preferred shares, which have equal economic rights, but the latter have no voting rights. The analysis below suggests that it would not be a ludicrous outcome to value VW equity at 2.5 times this current pricing. We accept that this would require unwinds of some discounts and further moves by management to liberate brand value along the lines of the Porsche AG (P911) float.

It is noteworthy in this context that a year ago, we wrote [1] about the large-scale discount versus a sum-of-the-parts valuation at which shares of Volkswagen were then trading and highlighted the catalysts of an IPO of Porsche AG in closing that gap. We were more conservative than the prevailing hype around the P911 valuation, but nevertheless felt there as more than enough upside to provide a stimulus to VW shares.

In the subsequent year, we were wrong about P911 and wrong about VW. The P911 valuation metrics were significantly higher than we felt might be reasonable and despite this, the value of VW shares has declined – even allowing for two subsequent large-scale dividends!!

As a guide, we noted that a FT article of February 2022 had surmised that VW would sell off Porsche AG at a €90billion equity valuation, which we thought was too high, and postulated a €60billion value. The P911 IPO in late September 2022 – at €82.50 per preferred share - came in just over halfway between the two – a €78bn equity value (€38bn pref; €40bn ordinary). The 43% appreciation in the P911 price to €118 – an implied €112bn equity value has well outstripped our thinking of that time. So, taking VW’s 75% share of Porsche AG implies just under an €84bn value – €24billion more than we thought, equivalent to about €48/VW share (preferred and ordinary). It is worth noting that in the intervening period from 31 March 2022, many “luxury” goods company share prices have been on a tear with increased profitability from growing margins, China re-opening and the “rich getting richer with inflation” argument. For example, the king of luxury stocks, OTCPK:LVMHF ) is up close to 28% from €660 since 31 March 2022.

Our VW investment has been in the preferred shares; since 31 March 2022, they have paid €26.62 in dividends (May 2022 €7.56; Jan 2023 €19.06) but even adding these payments back to the prevailing price of €125.64 leaves us about 4% below the price of €157 at end March 2022.

Hence, it is clear that markets have taken an even dimmer view than they did in March 2022 – just after the Russian invasion of Ukraine – about the value of the “residue” of VW’s assets. In our view that is an especially pessimistic approach. Since the mid-March release of the VW Group’s financial statements, as a result of P911 being separated and other changes in global valuation metrics, an even deeper valuation assessment of VW is possible, and shows that the discount to our estimate of fair value of VW shares has ballooned out to 60%.

Our approach to VW

VW is a veritable treasure trove of assets; our methodology is to value the identifiable components – especially the two listed spin-offs P911 and Traton at market prices – break out the associated companies (with due care given that two are owned by P911 and Traton), assess the potential for a Lamborghini spin out, put a proper (if conservative) value on VWFS and see what are paying for the mainstream branded ICE business. Or rather, what are we being paid to own it.

Listed exposures

VW (parent) has shareholdings in four publicly listed companies as follows:

- 75% (341million) of each of the ordinary and preferred shares of Porsche AG ; only the preferred shares are listed with the “minority” ordinary shares issued to Porsche SE (PAH3>DE) at a 7.5% premium to the preferred;

- 88.7% of Traton ( OTCPK:TRATF ) the manufacturer and distributor of Scania, MAN and Navistar trucks together with selected investments in the space (Sinotruk) and a finance subsidiary;

- An associated investment of 21.5% of equity in QuantumScape Corp ( QS ), a battery technology company with whom VW also have a 50-50 JV to develop solid state battery cells in California; and

- 24.7% equity in Gotion High-Tech Co Limited, a Chinese EV battery manufacturer which supplies to VW in its China business; Gotion is also listed on SIX (Swiss stock exchange) through Global Depository Receipts.

A 10.3% stake in Traton was spun off in June 2019 at €27/share; the shares have subsequently traversed lows below €12.50 but at the prevailing €18, have a market capitalisation of €9billion. However, the company labours under a net debt load – excluding leases and financing for receivables - of €10billion and had constrained cash flow in CY22 due to working capital build despite significantly improved adjusted (for Ukraine) profitability. Traton has strong order books which it is struggling to fill due to supply chain issues; CY23 guidance suggests the company will earn non-finance operating profit of €2.9billion and will be free cash flow positive. On that basis, the shares trade at ~6.6x EV/operating profit.

Traton is three times the size by revenue (€40bn versus €14.5bn) of its European peer Iveco IVG.MI), spun out of CNH International, controlled by Exor, last year. However, Iveco is extraordinarily lowly rated; it has an equity market capitalisation of $2.37billion (271m shares at €8.72) has net cash of €1.7billion (excluding financing debts against receivables), and equity in the finance subsidiary of €760million. On a consolidated basis, Iveco shares trade at around 5x operating earnings.

Equity accounted companies China exposure declining over time

VW has three joint ventures in China, and is the largest manufacturer in the country with around a 15% market share of the 21.1million unit market as follows:

- 40% of FAW-Volkswagen Auto Co (FAWVW) established in 1988 with 60% owned by the state owned FAW Group (First Automotive Works), China’s second largest of the “Big 4” local auto-makers [2] ;

- 50% of SAIC-Volkswagen Automotive Co (SAICVW), established in 1984, but due to expire in 2030, with SAIC (Shanghai Automotive) as the co-shareholder; and

- 30% of SAIC-Volkswagen Sales Company which sells the SAICVW production

FAWVW and SAICVW both manufacture at six locations; the former has a focus on the Audi, VW and Jetta brands/models; the latter on Skoda, VW and new BEV models. With increased penetration of other foreign manufacturers into the Chinese market together with domestic production, profitability of the JV’s has been in gradual decline since peaking in 2015:

{kind=link}

The latest three years also reflect manufacturing issues related to COVID, with plant closures, labor shortages and delayed parts availability. We would expect growth in 2023 in unit volumes and profitability, with increasing penetration from the prevailing 5% level of BEV sales (155k in 2022).

VW received around 70% of its proportionate profit in dividends (after withholding tax) in 2022, slightly down on the 77% in 2021.

Due to the vagaries of equity accounting, VW carry their shares of the three China JVs on balance sheet at just above €3.5billion – representing a 65% dividend yield in CY2022!! Given expected improvements in profitability, we have conservatively chosen to value the JV’s at 3.5x trailing proportionate contribution, being €11.5billion. Based on normal payout ratios, this would represent a yield of around 22% on improving earnings.

Battery technology

In July 2022, VW unveiled a new initiative PowerCo to eventually build six factories in Europe, commencing in its home base at Salgitter in Lower Saxony, Germany with a factory to commence production in 2025. The initial investment of €1.7billion will be replicated at Valencia in Spain and one other as yet undisclosed but decided location. The aim is to be responsible for the group’s battery business, which sits alongside various other investments in the area noted in associated companies and in the e-mobility space

Not mentioned in the 2022 VW Annual Report, but noted on 23 March 2023 by the Chair of Porsche SE was that “we are hearing from VW that interest is extremely high on the subject of PowerCo. That should be a positive case” in relation to a potential IPO. In our view, that would be a significant positive, potentially alleviating negative cash flow from VW and bringing forward the relevant valuation premium to the group.

VW’s three existing specific associated company investments in battery technology can be assessed as follows:

| holding |

| shares |

| price |

| € value |

| Carry value |

| Notes |

| QuantumSpace |

| 21.5% |

| 68.24m |

| US$8.19 |

| € 559m |

| €1123m |

| Per listed price 31 Mar 23 |

| Gotion HiTech |

| 24.7% |

| 440.6m |

| ¥29.81 |

| €1,776m |

| €1021m |

| Per listed price 31 Mar 23 |

| Northvolt AB |

| 23.6% |

| € 911m |

| € 911m |

| Per VW annual report Note 15 & p296 |

| Northvolt AB c/note |

| € 240m |

| € 240m |

| Per VW annual report p296 |

| TOTAL |

| €3,486m |

| €3,296m |

VW also participated in a 66% subsidiary undertaking with Attestor (27% a London PE manager) and Pon Holdings [3] (7% the Dutch VW franchisee) to successfully acquire Europcar Mobility via the Green Mobility Holding vehicle for an equity value of €2.553billion, with VW’s share being €1.685billion.

The hidden “rich get richer” play: Lamborghini

Lamborghini was acquired by Audi in June 1998 from companies controlled by Tommy Suharto (son of the former Indonesian president) and a Malaysian financial company for an estimated US$111million; the Asian partnership had owned the marque for five years having acquired it from Chrysler in 1993. At the time of the deal, Audi and Lamborghini were in discussions about the adaptation and use of Audi’s powertrain to expand production from the then level of just over 200 cars (not a misprint).

In 2021, a group of ex-VW executives operating via Quantum Group AG allegedly made a $7.5 billion offer to buy Lamborghini; this was (apparently) flatly rejected by Audi/VW. There was foresight and logic in doing so - the Ferrari spin-out continued to roll on and increase its stock market rating and profitability, but also the significant inter-connectedness of Audi componentry in certain of the Lamborghini cars – notably the “Urus” (5500 units sold per annum).

Of course, this makes it an ideal IPO candidate for VW in a similar vein to P911, retaining some semblance of control and with an ongoing co-operation agreement between the two companies.

So, what’s Lamborghini potentially worth? The world of luxury cars is very simple – the higher the price, the higher the margin and the higher the valuation. Even Aston Martin (AML.L) has an equity valuation of £1.595billion (equity + £765m debt = enterprise value of £2360m) even though it will not be cash flow neutral on its ~6,500-unit sales at average price of ~€230k until CY2024.

The Ferrari ( RACE ) story continues to grow with units sold flatlining in CY2023 at the mid 13,000 area but with increased forecast average selling prices – remember there is a waiting list – the company has forecast net profit growth of 20% for both EBITDA and EPS. The shares at prevailing prices have an enterprise value of $49billion and trade at ~22x EV guided CY23EBITDA and 44x EPS.

Lamborghini sits in between AML and RACE with sales of 9,233 units in CY2022 and a revenue base of ~€2.4billion. The VW annual presentation [4] (slide 13) discloses a “return on sales” (i.e.. operating margin) of 25.2% implying operating profit of some €620million. There is an 18-month waiting list for a Lamborghini.

P911 shares trade at a valuation of ~13.5x EV/forecast CY2023 operating profit (€103.5bn EV; operating profit €7.35bn). In this context given there are no cars available before 2024, and against the cohort, is it unreasonable to postulate that on an IPO, Lamborghini would trade at ~16x EV/CY2023 operating profit and command a valuation close to 11billion? That alone would represent close to €22/share upside to VW, given the abnormally low rating attributed to the “residual assets” (actually the core ICE brands) within the group.

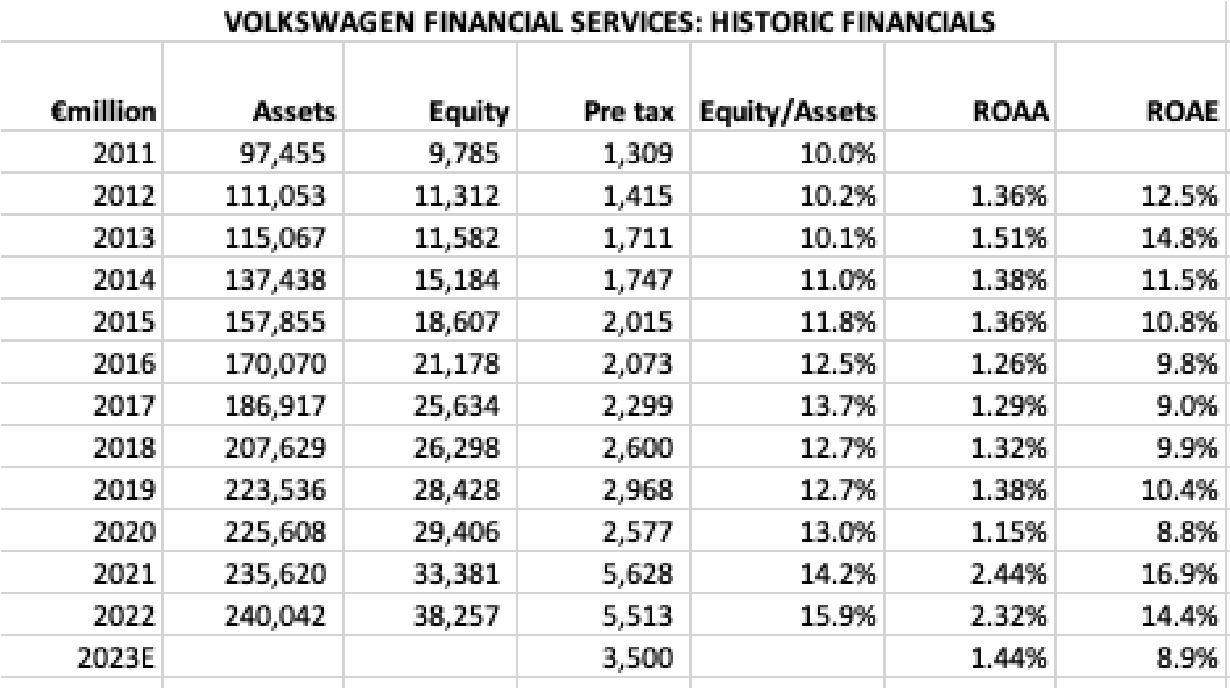

VWFS – dissection suggests a very valuable financial asset

We are strong believers that finance companies attached to car manufacturers are usually extremely valuable conveyances. There is obvious cynicism by many given the symbiotic relationship between financier and manufacturer such that if VW cars are unattractive, then clearly the demand for the various financing options – leases, loans etc. – will fall away. In addition, we recognise that there is residual value risk, which in the case of VWFS, has worked spectacularly in their favor during COVID with increases in used car prices across the globe. Demand for cars and high residuals are responsible for the significant lift in profits in VWFS during 2021 and 2022 illustrated in the table below:

{kind=link}

It is noteworthy that VWFS on a consolidated basis – including the Porsche Financial Services component which is now within P911 – have been able to step up the level of equity to assets significantly over the past few years which will bolster the business as the level of excess profits starts to wind down to more normal – but still high levels. On a consolidated basis, the company has flagged an operating profit – roughly equating to pre-tax profit of €3.5billion in the 2023 year [5] .

Having due regard to our consolidation methodology and leaving the profits from Porsche Financial Services – approximately €340m or 6% of VWFS - within P911, we believe a capitalisation multiple, and cross-check can be applied to a 2023 outcome of ~€3.2bn at the operating level.

Traditional finance companies with additional risks have over recent years tended to trade at discounts to book value and single digit multiples of after-tax profit. It is not unreasonable to apply these types of metrics to VWFS. On that basis we believe VWFS could be valued at €23billion, being a 35% discount to book value which would equate to 9x forecast post tax profit in 2023.

Sum of the parts assessment suggests Volkswagen is extraordinarily cheap

We believe VW trades at a 60% discount to a sum of the parts valuation which contains some premium components but also some heavily discounted areas, as follows:

| €million |

| Est “parent” net cash |

| 47,100 |

| Includes receivables from associates, P911 and Traton fully adjusted for P911 float |

| 75% P911 at market value |

| 80,623 |

| Assumes NO premium on voting shares |

| 88.3% Traton at market value |

| 7,868 |

| China JV’s |

| 11,500 |

| 3.5x proportionate earnings |

| Associated (battery) companies at market value |

| 3,486 |

| See discussion |

| Lamborghini at value |

| 11,000 |

| See discussion |

| VWFS at value |

| 23,000 |

| See discussion |

| Green Mobility |

| 1,685 |

| 66% - owns Europcar Mobility |

| Pension liabilities (“parent”) |

| (20,738) |

| Page 362 of 2022 Annual Report less attributable to P911 and Traton |

| Diesel litigation |

| (4,200) |

| Note 38 2022 Annual Report and pages 420427 for detailed assessment |

| NET VALUE OF NON-VW CORE BUSINESS |

| 161,324 |

| “Residual” ICE [6] business earnings after overhead including CARAID expenses (€2bn) |

| 19,025 |

| €7,610 estimate at 2.5x EV/Operating earnings – Skoda, VW, SEAT, Cupra, Audi, Bentley |

| TOTAL EQUITY VALUE |

| 180,349 |

| Versus current €73billion |

If we allocate our estimated equity value in the manner in which VW ordinary and preferred shares have traded in recent times – 65/35 – then a full equity value for each, on the basis of the assumptions above, would be:

| Attributable Value (€bn) |

| Shares ((mn)) |

| Attributable/ share |

| Current price |

| discount |

| Ordinary |

| 117.2 |

| 295.1 |

| €397 |

| €158.00 |

| 60% |

| Preferred |

| 63.1 |

| 206.2 |

| €306 |

| €125.64 |

| 59% |

As a cross-check, the consensus consolidated forecast for 2023 for VW, which has some higher degree of certainty given the bounce back in China and the pre-order book, is for EPS of €31 per share; on the preferred shares this equates to a P/E of 4.1x and a dividend yield of 7%, for numbers which include the strong attractions of 75% of Porsche AG and Lamborghini. Even at our full valuation of the shares, the P/E on the preferred stock would still be below 10x.

The catalysts to unwind at least some of this discount remain the same: fungibility of the attractive components of the group. VW will continue to control these companies, essential for engineering and other co-operation, so to some degree they will act like tracker stocks. However, the clear success of the P911 IPO versus our expectations suggests there is an appetite from non-VW shareholders for the growthier parts of the company.

Porsche SE (Porsche Automobil Holding): double discount but with gearing

Porsche SE is the largest but not controlling shareholder of Volkswagen by dint of owning 53.3% of VW’s ordinary (voting shares); however, their full control is negated by the State of Lower Saxony holding a 20% voting stake and under the German Volkswagen Act of 1960, can act to veto major strategic decisions including plant closures, but also takeovers etc.

Porsche SE is the holding company of the Porsche and Pietsch families, who own all of PAH’s 153.1m voting shares; the 153.1m listed preferred shares are all non-voting.

Porsche SE was instrumental in pushing for an IPO of Porsche AG (P911) but in doing so, wished to ensure it could keep a handle on its “name”. To do so, PAH acquired 25% of P911 voting shares, which were not listed; only P911 preferred shares are publicly traded. To do so, the company agreed to pay a 7.5% premium to the IPO price for its stake which involved an investment of €10.1billion.

To make this investment, PAH needed to raise a significant quantum of debt - initially €7bn – of which €2.7billion has been successfully refinanced in March 2023 via a “Schuldshein” loan – a loan with differing traches and maturities and with fixed and variable rates.

Porsche SE has a very simple balance sheet structure as follows:

| Shares |

| Price |

| Value (€mn) |

| VW ordinary shares |

| 157.283m |

| €158.00 |

| 24,851 |

| P911 ordinary shares |

| 113.875m |

| €118.00 |

| 13,437 |

| Assumes no voting premium |

| Other portfolio investments |

| 116 |

| Inrix, ETS |

| Cash and receivables |

| 1,067 |

| Debt at 31.12.2022 |

| (7,093) |

| Other liabilities |

| (276) |

| EQUITY AT MARKET PRICE |

| 32,102 |

| €104.84/share |

Assuming no differentiated distribution to voting/non-voting, at prevailing prices Porsche SE has a net asset value of ~€105/share. At the current market price of €52.92, the shares trade at a 49% discount to pre-tax value based on the prevailing VW share price, which we believe is a 60% discount to the sum of the parts valuation.

In our portfolio, we are cognisant of the double exposure, notwithstanding the cheapness of both VW and Porsche SE. In the event that VW shares traded at our valuation of €397/ordinary share, PAH3 would theoretically be worth close to €70billion or €228/preferred share.

DisclaimerThis communication has been prepared by Andrew Brown and East 72 Management Pty Limited ( E72M ) (ACN 663980541); E72M is Corporate Authorised Representative 001300340 of Westferry Operations Pty Limited (AFSL 302802) of which Andrew Brown is a Responsible Manager. While E72M believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. E72M and its related companies, their officers, employees, representatives and agents expressly advise that they shall not be liable in any way whatsoever for loss or damage, whether direct, indirect, consequential or otherwise arising out of or in connection with the contents of an/or any omissions from this report except where a liability is made non-excludable by legislation. Any projections contained in this communication are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of E72M and therefore may not be realized in the future. This update is for general information purposes; it does not purport to provide recommendations or advice or opinions in relation to specific investments or securities. It has been prepared without taking account of any person’s objectives, financial situation or needs and because of that, any person should take relevant advice before acting on the commentary. The update is being supplied for information purposes only and not for any other purpose. The update and information contained in it do not constitute a prospectus and do not form part of any offer of, or invitation to apply for securities in any jurisdiction. The information contained in this update is current as at 31 March 2023 or such other dates which are stipulated herein. All statements are based on E72’s best information as at 31 March 2023. This presentation may include forward-looking statements regarding future events. All forward-looking statements are based on the beliefs of E72M management, and reflect their current views with respect to future events. These views are subject to various risks, uncertainties and assumptions which may or may not eventuate. E72M makes no representation nor gives any assurance that these statements will prove to be accurate as future circumstances or events may differ from those which have been anticipated by the Company. |

Footnotes[1] East 72 Holdings Quarterly Report March 2022 [2] In order SAIC, China FAW, Dongfeng Motor and Changan Automobile [3] In 1997, the Pon Family also founded one of the first vineyards of the Uco Valley in Mendoza, Argentina at 1,200m above sea level. I have been lucky enough to visit Bodegas Salentein – a very special place. [5] VW 2020 Annual Report page 231 [6] Internal Combustion Engine but with significant BEV exposure |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

East 72 - Volkswagen: A Heavily Discounted Treasure Trove And Potential IPOs