EWBC - East West Bancorp: Investors Have This Gem Completely Wrong

2023-06-30 12:43:35 ET

Summary

- East West Bancorp, a bank with a focus on servicing the lending needs of Chinese and Asian Americans, has grown to $64 billion in assets and operates in a unique hybrid space between the US and Asia.

- The bank's stock has seen a significant fall due to the regional banking crisis. Compared to its peers, East West Bancorp has a high net margin and profitability, and it has successfully translated this into returns for shareholders.

- While there are risks associated with investing in regional lenders like East West Bancorp, the bank has one of the strongest regulatory capital ratios for regional banks and its exposure to commercial real estate is not significant.

- Selling puts could be an enticing way to invest in the bank or buying equity directly.

East West Bancorp

East West Bancorp (EWBC) is a fascinating business that is not simply characterized as a "regional US lender". They celebrated 50 years of being in business in the heart of Chinatown in Los Angeles with a focus on servicing the dynamic and growing lending needs of Chinese and Asian Americans. The business has grown to $64 billion in assets and it is now a full service bank with 120 locations across the US and Asia, with experts based in Southeast Asia to maintain their competitive lending moat. They are actually one of the only banks that operates in this hybrid space between continents and they have leaned into this advantage to ensure that they have a global network that continues to capture the growth in Asia.

The bank has successes that range from lending to families and community small businesses in their diverse markets, to actually funding BYD (BYDDF) directly - the world's largest electric vehicle firm based in China. For those familiar with the market in China this is a unique opportunity: being able to bridge the cultural gap and add value as part of the funding transaction.

Fundamentals - Balance Sheet and Income Statement

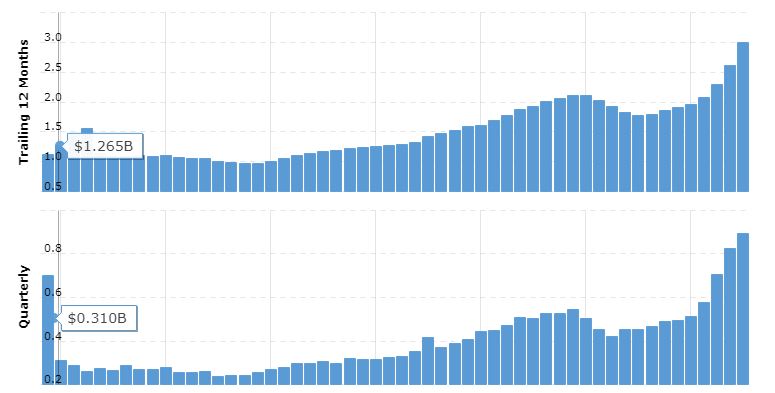

Revenue Growth is strong and that's a key factor that we should be assessing, as it needs to have demonstrated this over periods greater than 10 years:

{kind=link}

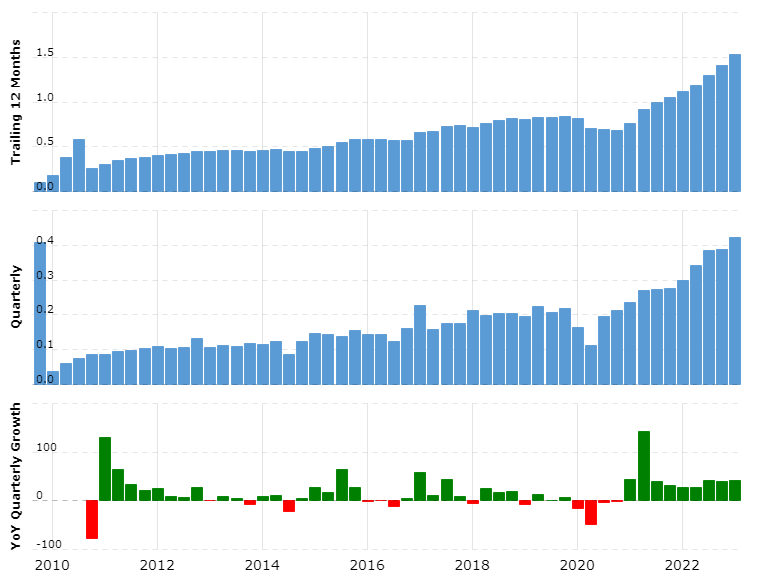

Profit has grown 15-fold since the bottom of the global financial crisis:

{kind=link}

The story is not perfect, however, as gross and net margin have recently seen a dip albeit from a very high level. Operating margin peaked at 57.4% in 2022 and has come down to 51%, and net margin this quarter sits at 40.38%.

Over the past 11 years they have grown earnings per share every year apart from 2019/2020 with steady and dependable growth.

Macrotrends 2023

Turning to financial health of the business it is achieving an 18.8% return on equity and has a book value of $42.46 per share. Free cash flow is positive and sits at $6.33 per share - the business is clearly operating at a high level and returning significant amounts of cash and capital.

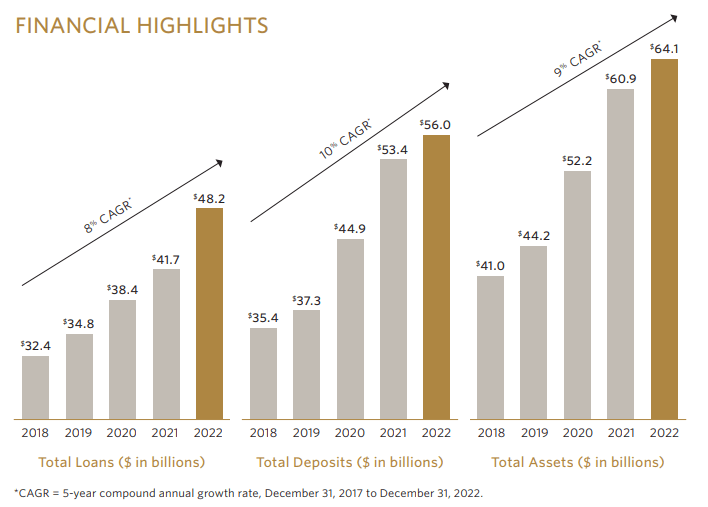

This is no surprise given their impressive growth in loans, deposits and total assets:

{kind=link}

Performance of EWBC

What I find surprising is that East West Bancorp has been embroiled in the regional banking crisis and 'tarred with the same brush' as other regional US banks, some of which have fairly unscrupulous lending practices and exposures to risky crypto ventures and over-valued tech funds.

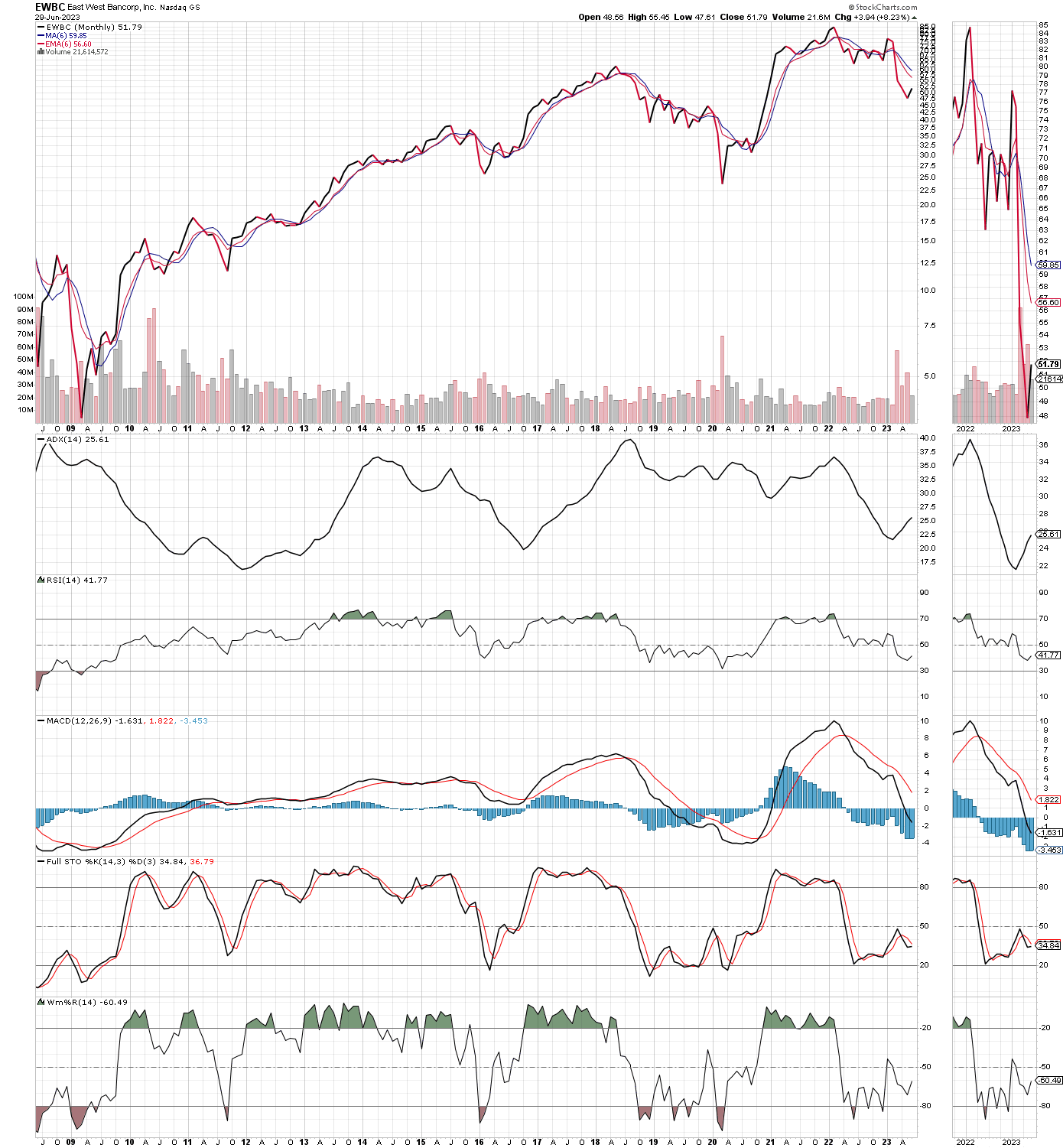

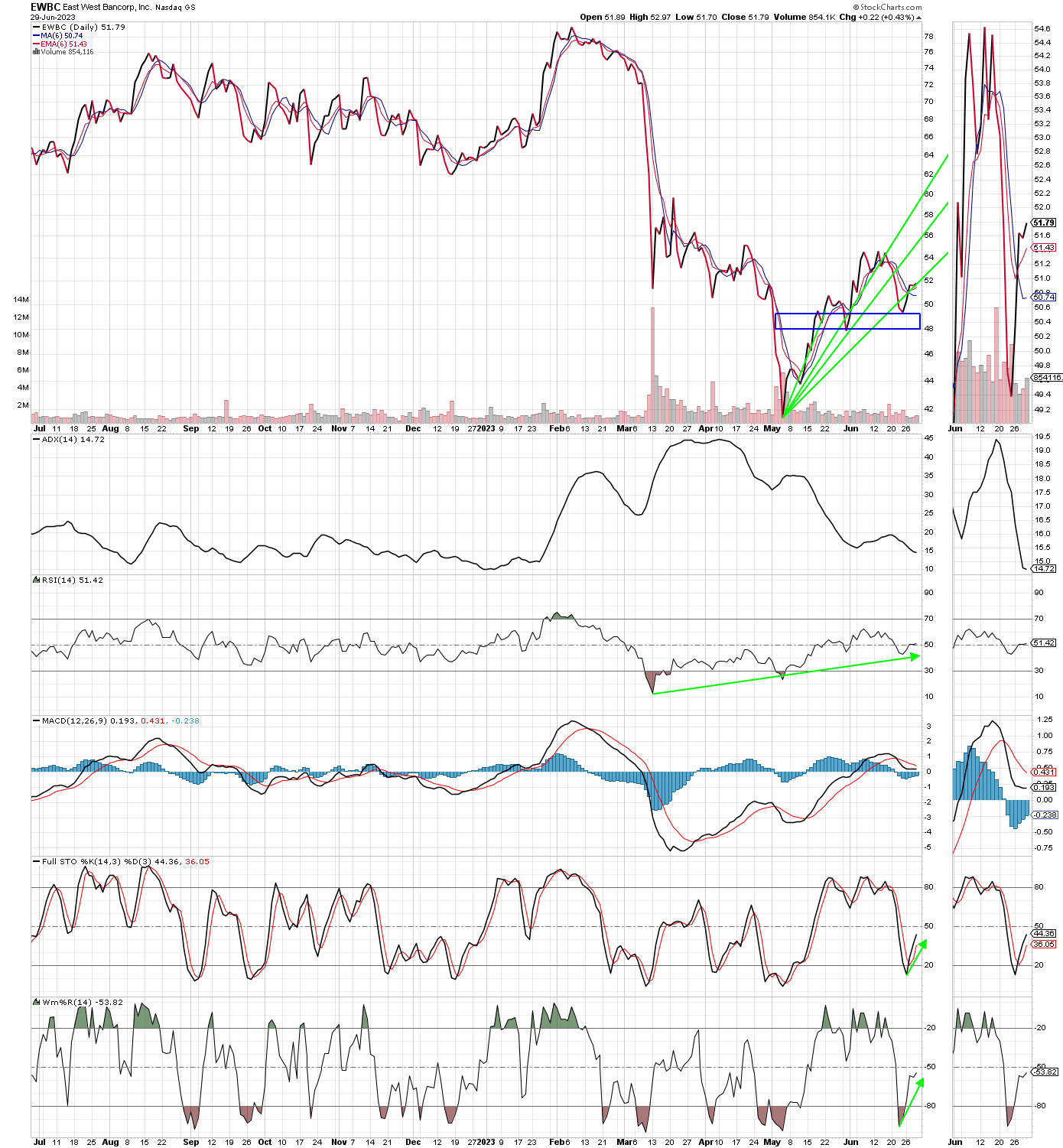

On the monthly scale EWBC has had a sizeable peak to trough fall of 42.5% (probably better described as a drubbing since it peaked in February 2022):

{kind=link}

Let's look at the daily scale and zoom in a bit further:

{kind=link}

The stock has managed to gain momentum since potentially bottoming in May 2023. Provided it can hold support in that range between $48-$50, we should continue to see upward momentum in EWBC as the regional banking crisis fades from memory and investors realize that they have incorrectly dumped all of these banking shares into one pot.

Comparison to Peers

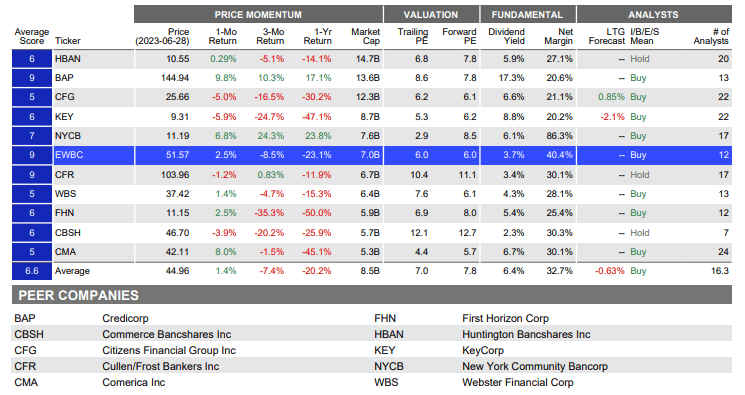

What I like to see though is how a company stacks up against the competition. EWBC has an advantage here and let's see if you can spot the difference in this chart from Refinitiv:

{kind=link}

For those eagle eyed readers, you can see that Net Margin and profitability EWBC storms ahead. It is the second highest in the list next to New York Community Bancorp (NYCB) yet it has one distinct advantage that NYCB doesn't: it manages to convert that profitability into actual underlying profit and EPS that shareholders benefit from.

NYCB is worth looking at from a valuation and income perspective, but it has missed earnings for 4 out of the last 9 quarters and shown relatively modest gains in EPS since 2012 ($1.13 in FY 2012 and $1.23 in FY 2022).

So imagine that: you get a business here with EWBC that has a 40.4% net margin, however unlike its peers, it's taking that performance to the final mile that counts and translating that to returns for shareholders. Over that same 9 quarter period EWBC has missed one quarter (Q4 2021) and grown earnings since 2012 from $1.89 to a staggering $7.92.

Risks to Consider

I admit I had to do a lot of digging to really understand the risks and issues facing EWBC, including reading several of their annual and quarterly reports and building a picture of how the bank has positioned itself and what it has promised to stakeholders. The elephant in the room is, of course, the banking crisis itself and the risk or potential that EWBC, like other regional lenders, goes under or has to shutter its doors during a financial crisis or "US regional banking crisis 2.0".

The EWBC is not the safest bank in America. It's difficult to put a list together and say which one that would be, but the point is that investors have one thing right, regional lenders are more at risk during a downturn than large conglomerates at the heart of the banking system. For one thing the Federal Reserve has all but come out and said it won't be rescuing them en masse. For another, there seems to be appetite to allow for consolidation and fewer banks.

That being said, EWBC has as of the end of March 2023 one of the strongest regulatory capital ratios for the regional banks and sits at CET1 Capital Ratio of 12.58% against a requirement of 6.5%. Their leverage, capital ratios and common equity ratios all look good:

EWBC Quarterly Report Q3 2023

Above and beyond that the bank also has even higher tangible book value which has risen to $41.28 against a share price of just over $50.

The other risk to consider is their exposure to commercial real estate. This isn't something to dwell on too much because despite claims in other sources, CRE retail accounts for $4.1 billion and it is spread across North and Southern California, the Bay Area, San Francisco and other regions of the US. It could definitely be a drag on future performance but compared to their $54.7 billion deposit base it's not huge.

Investment Case

Overall EWBC appears to have been unfairly punished during the regional banking crisis and is in recovery mode. Above $48 and based on the fundamentals, the business itself, and weighing up the risks associated with investing in this type of lender it appears that a buy and hold strategy above $48 is worth considering.

However there's a unique way to get access to the bank and it's probably our base case for an investment. Due to the instability and turbulence with regional lenders, it happens that derivatives are particularly expensive and command high premiums. That can be a real issue if you're thinking of buying calls to invest in EWBC, but a great reward if you wanted to sell puts.

To put this into perspective - selling a $50 put against EWBC that expires on 21st July, 2023 (in 21 trading days from the time I write this), would give you a premium of $1.55. As a function of the current share price that means investors will pay you 3.04% if you agree to buy the company at $50 by July 21st. That's a really severe premium and means that selling puts here could be an enticing way to pick up the equity at a breakeven price that is actually 6.44% below today's price.

Have a look at this overview:

OptionsStrat 2023

If EWBC closes above $50.50, you keep the $1.55 premium which is worth 3%. It would need to close below $48.45 for you to lose money, and if it does, you'd simply be taking the stock and your average buy price would be cheaper.

For further details see:

East West Bancorp: Investors Have This Gem Completely Wrong