EWBC - East West Bancorp: Navigating Challenges In The Banking Landscape

2023-09-21 00:38:08 ET

Summary

- East West Bancorp is a profitable and growing bank with over 120 locations in the U.S. and Asia.

- EWBC's success is driven by its unmatched efficiency, low-cost deposit base, and strategic approach to lending.

- The bank's ability to sustain profitability and growth makes it an attractive investment option in the financial landscape.

- Bank's exposure to the most toxic Commmercial Real Estate loans is limited.

East West Bancorp ( EWBC ) has its roots as savings bank serving the immigrant Chinese-American community and over the years has grown into a full-service commercial bank financing businesses and commercial real estate projects primarily in California. East West Bank currently has over 100 locations in the U.S. and total assets of over $60 billion.

EWBC is leading the banking industry in profitability and has been growing consistently. In 2022 it has been named as a top performing US public bank by S&P . The share price of the bank has been under pressure since the collapse of the Silicon Valley Bank and several others in the sector. This could present us a good opportunity to invest in a good quality regional bank at a lower price.

What makes EWBC a good bank?

- The Engine of Efficiency:

At the heart of EWBC's success lies its unmatched efficiency, which has catapulted the bank into a league of its own. One of the primary drivers of this efficiency is its low-cost deposit base, coupled with streamlined operations. This synergy allows EWBC to operate with some of the lowest funding costs in the industry, a critical advantage in today's competitive banking landscape.

As a result, EWBC is well-positioned to offer loans at highly competitive rates while simultaneously expanding its market share within the commercial lending sector. This strategic advantage translates into increased profitability, positioning EWBC as a formidable force in the banking world.

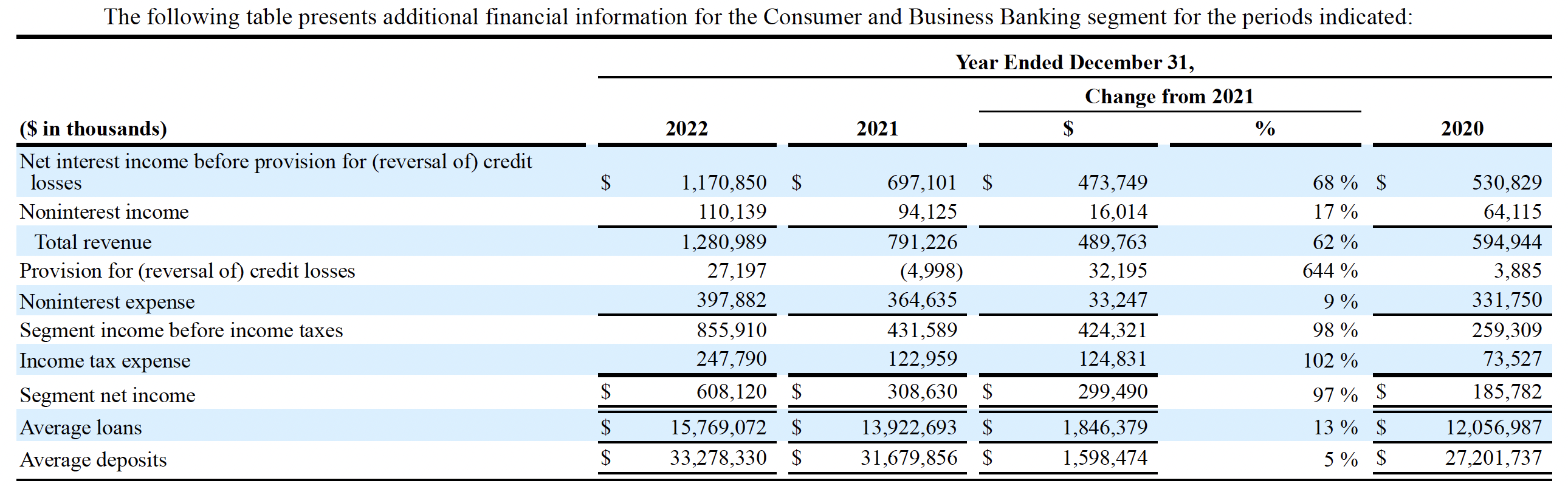

- The Power of Consumer and Business Banking:

EWBC's Consumer and Business Banking division serves as the linchpin for the bank's deposit-gathering activities. With total deposits averaging an impressive $33 billion, approximately half of which are non-interest-bearing demand deposits, this division is the lifeblood of EWBC's operations.

What sets EWBC apart is its ability to leverage these deposits effectively. Despite only lending out half of the funds residing in its accounts, the bank manages to maintain an impressive net interest margin. The remaining funds are strategically employed in commercial lending activities and investments in securities. This unique approach allows EWBC to maximize the utility of its deposit base and extract optimal returns.

{kind=link}

EWBC financial reports

- Efficiency as a Competitive Edge:

EWBC's industry-leading efficiency ratio, resting comfortably in the low 30% range, is nothing short of remarkable. This feat is even more impressive when considering the bank's significant Consumer and Business banking presence, complete with a sprawling branch network and a dedicated workforce.

The key to this efficiency lies in the specialized services that EWBC offers to an often underserved demographic – the Chinese-American immigrant population. By catering to this unique clientele, the bank can command higher-than-average loan margins, thereby mitigating the impact of fixed costs on its overall revenues.

- Low Funding Costs and Competitive Advantage:

EWBC's funding costs tell a compelling story of financial prudence. With funding costs of 1.85% in FY2022 and 3.6% in H1 2023, the bank has managed to keep these costs competitive and, in many instances, lower than its peers. This advantage is pivotal in maintaining profitability and offering attractive lending rates to its customers.

| Funding Cost of EWBC and Peers |

| H1 2023 |

| East West Bank |

| Funding cost |

| 3.6% |

| Deposits and interest-bearing liabilities |

| 58,000,000 |

| Interest Cost |

| 575,033 |

| Non-Interest Expense |

| 480,236 |

| Loans as a share of assets, % |

| 72% |

| Bank of America |

| Funding cost |

| 4.9% |

| Deposits and interest bearing liabilities |

| 2,624,000 |

| Interest Cost |

| 32,403 |

| Non Interest Expense |

| 32,276 |

| Loans as a share of assets, % |

| 33% |

| Wells Fargo |

| Funding cost |

| 4.8% |

| Deposits and interest-bearing liabilities |

| 1,686,634 |

| Interest Cost |

| 13,687 |

| Non Interest Expense |

| 26,663 |

| Loans as a share of assets, % |

| 50% |

| U.S. Bancorp |

| Funding cost |

| 4.6% |

| Deposits and interest bearing liabilities |

| 627,341 |

| Interest Cost |

| 5,441 |

| Non Interest Expense |

| 9,124 |

| Loans as a share of assets, % |

| 54% |

| Cathay General |

| Funding cost |

| 4.1% |

| Deposits and interest bearing liabilities |

| 19,097,003 |

| Interest Cost |

| 211,523 |

| Non Interest Expense |

| 176,007 |

| Loans as a share of assets, % |

| 82% |

| CVB Financial |

| Funding cost |

| 2.1% |

| Deposits and interest bearing liabilities |

| 14,483,177 |

| Interest Cost |

| 46,762 |

| Non Interest Expense |

| 108,898 |

| Loans as a share of assets, % |

| 53% |

| First Financial |

| Funding cost |

| 3.0% |

| Deposits and interest bearing liabilities |

| 11,458,204 |

| Interest Cost |

| 58,361 |

| Non Interest Expense |

| 114,869 |

| Loans as a share of assets, % |

| 51% |

Financial reports and our estimates

- Building a Strong Lending Foundation:

EWBC has not only excelled in gathering deposits and managing costs but has also forged a robust presence in both retail and commercial lending. Loans constitute a significant portion, approximately 76%, of its interest-earning assets. This diversification is a strategic move to ensure the highest risk-adjusted returns and maximize return on equity.

- The Path to Shareholder Rewards:

With an average Return on Equity of about 14% and a dividend payout ratio of roughly 25%, EWBC strikes a balance between rewarding shareholders and reinvesting earnings for growth. This approach has allowed the bank to consistently grow book value per share, loans, and deposits at an attractive pace.

| EWBC track record |

| 2012 |

| 2017 |

| 2022 |

| 5yr CAGR |

| 10yr CAGR |

| BVPS |

| 16 |

| 26 |

| 42 |

| 10% |

| 10% |

| NII |

| 918 |

| 1185 |

| 2046 |

| 12% |

| 8% |

| EPS |

| 1.9 |

| 3.5 |

| 8 |

| 18% |

| 15% |

| RoE |

| 12% |

| 13% |

| 19% |

| DPS |

| 0.4 |

| 0.8 |

| 1.6 |

| 15% |

| 15% |

| Shares |

| 141 |

| 144 |

| 142 |

| -0% |

| 0% |

| Net Loans Bn |

| 15 |

| 29 |

| 48 |

| 11% |

| 12% |

| Deposits Bn |

| 18 |

| 32 |

| 56 |

| 12% |

| 12% |

| Compensation and benefits |

| 171 |

| 335 |

| 477 |

| 7% |

| 11% |

Financial reports and our estimates

The issues with regional banks

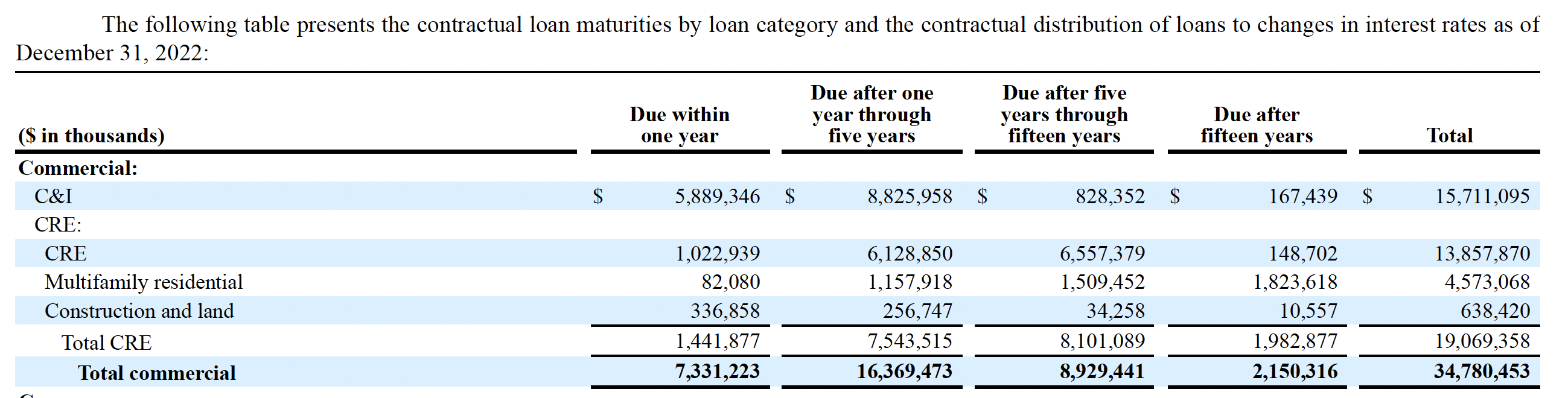

East West Bancorp has enjoyed a stellar reputation in the banking industry, built on its efficiency and profitability. However, like any financial institution, it faces its share of challenges. In recent times, concerns have arisen regarding EWBC's exposure to Commercial Real Estate ((CRE)) loans and the potential impact on its performance.

It's worth noting that smaller banks in the US carry a substantial portion of CRE loans, accounting for approximately 70% of these loans. These loans represent a significant portion, around 43% , of small banks' assets, compared to only 13% for larger lenders.

EWBC, despite being a prominent player, is not immune to these challenges. The CRE sector has been a cornerstone of its lending activities, making it susceptible to the inherent risks associated with this market.

- The Unsettling Dynamics of Commercial Real Estate:

Within the CRE sector, concerns have intensified, especially in the face of rising interest rates, rising capitalization rates and falling valuations. Most of the assets are financed using 50-60% debt. If value of a property falls in excess of 40% then all the equity of an asset owner is wiped out and there is no incentive for the borrower to refinance the loan when the term expires. In such a scenario, defaults on loans become a real concern. And they have already started .

Forced liquidations are particularly worrisome, especially when the market lacks willing buyers. This could lead to a substantial erosion of equity within the sector. With an LTV of 50-60% the lenders have a significant cushion, though some of the most distressed assets in the industry have recently been changing hands at 75% below the pre-pandemic values. Lenders most likely incurred losses on these loans.

Among the various CRE sectors, the office and sub-prime retail segments face the most acute challenges. Structural headwinds, including the rise of remote work, have further strained these sectors. California, a key market for EWBC, has not been spared from these challenges.

Office vacancy rates have surged in Southern California, doubling since the pre-pandemic era to reach 21% . The national office vacancy rate has also escalated, reaching 17.1% by the end of July. San Francisco is the hardest hit market, with vacancy rates reaching 32% .

The sub-prime retail sector, while facing structural issues for several years, is not as dire as the office space. The most vulnerable properties are often those in declining cities or enclosed out-of-town malls. The prime locations are doing well on the other hand.

As for geographic exposure, San Francisco Bay Area seems to be the most troubled out of the locations where EWBC is present. San Francisco's commercial real estate market, once a beacon of prosperity, now confronts potential defaults on billions of dollars of debt. Owners of major properties in the city have ceased loan payments and returned the keys to lenders. The toxic landscape extends to various types of commercial real estate loans in the San Francisco Bay Area, including office, hotel and retail.

- Bright Spots in Uncertain Markets:

Commercial property markets are known for their illiquid nature, often taking time to reflect real values, especially in declining markets. In times of decline, sellers may adopt a "wait-and-see" approach, further complicating the market dynamics. The lack of real transaction data adds to the complexity.

To gauge the true pulse of the market, investors often turn to publicly quoted property funds, where share prices provide a more immediate indicator of market sentiment than reported asset values.

REIT sector has been rather resilient overall. The S&P U.S. Equity All REIT and MSCI US REIT Index were down c25% in 2022. The worst performing sector unsurprisingly was office, down 38% in 2022. Residential and Industrial have also performed poorly in 2022, but have since recovered somewhat. Weakness in office occupancy is continuing into the 2023.

A 38% reduction in equity value of a REIT being financed with say 55% debt, would imply an underlying asset value reduction of 21%. Thus we could imply that office values have declined by a relatively modest amount on average.

What is the exposure of EWBC?

EWBC has an equity of $6 billion and it carries c$20 billion in commercial real estate CRE loans on its books. Significant defaults and poor recoveries could weaken its equity position and in the worst case cause a run on the bank.

The risk exposure that the bank has is not all that easy to quantify, as potential losses depend on the situation in specific markets, sub-sectors and areas and loan book disclosures are never this granular. Under such uncertainty, it would be best to be out of the most troubled sectors entirely or assume a sizeable haircut on the whole of the sector.

EWBC, a Californian bank with a large CRE loan book, is exposed in several sectors and geographies. Office, San Francisco Bay Area and Retail are the largest categories of exposure. Bay Area exposure is rather limited and is mostly contained in the broader Office and Retail sectors.

We assumed that in the worst case troubled sector loans get haircuts ranging from 20% to 50%. A loan haircut of 50% with a loan to value of 50% would mean that a distressed asset is either sold at 25 cents on the dollar in bankruptcy or that the lender agrees to take a 50% haircut when refinancing to reduce the interest cost burden of the borrower and avoid having to take possession of an asset. These a really conservative assumptions.

We sum up different sector exposures of EWBC and apply different loan haircuts to different CRE sectors. Our conservative estimate of potential losses from CRE loans could approach $2.4 billion. This is not a forecast but rather a stress test.

| Main exposures |

| H12023 |

| Value Correction |

| Value |

| Total stockholders’ equity |

| 6,461 |

| -2,414 |

| 4,047 |

| Office CRE loans |

| 2,354 |

| -50% |

| 1,177 |

| Retail CRE loans |

| 4,183 |

| -20% |

| 3,346 |

| San Francisco multifamily (approx.) |

| 500 |

| -30% |

| 350 |

| San Francisco hotel (approx.) |

| 500 |

| -50% |

| 250 |

| Total risky loans |

| 7,537 |

| 5,123.4 |

| Average LTV |

| 50% |

Financial reports and our estimates

A significant share of CRE loans have variable rates and staggered maturities mainly spanning 5 to 15 years. Borrowers also protect themselves with IR swaps, therefore the pressure from higher interest service is postponed and a lot of the negative effects are not seen yet. We do not know how long the customer-level swaps are and when exactly the customers will face a steep rise in debt service costs. Having said that, the defaults have already started and according to Morgan Stanley, defaults should peak somewhere in 2024-2025 .

{kind=link}

EWBC financial reports

Valuation

In our conservative valuation, we assume that EWBC’s interest-earning assets do not grow due to impairments of CRE loan values, and the spreads stay at the level of H1 2023. On the other hand, the bank should be able to cover the impairments from retained profits in other divisions.

If the business can weather the CRE storm and maintain its competitive advantages, it is likely to continue growing and will likely fetch its historic PE multiple.

We estimate that in three years’ time, EWBC could be worth about $104 per share or about $78 discounted to present value.

| FY2021 |

| FY2022 |

| FY2023 H1 |

| FY2023 |

| FY2024 |

| FY2025 |

| FY2026 |

| Interest bearing liabilities |

| 31,077 |

| 32,322 |

| 39435 |

| 39435 |

| 39435 |

| 39435 |

| 39435 |

| yield/cost |

| 87 |

| 275 |

| 1262 |

| 1262 |

| 1262 |

| 1262 |

| 0.3% |

| 0.9% |

| 2.9% |

| 3.2% |

| 3.2% |

| 3.2% |

| 3.2% |

| Interest earning assets |

| 56,256 |

| 59,309 |

| 62799 |

| 62799 |

| 62799 |

| 62799 |

| 62799 |

| yield/cost |

| 1,618 |

| 2,321 |

| 3517 |

| 3517 |

| 3517 |

| 3517 |

| 2.9% |

| 3.9% |

| 5.59% |

| 5.6% |

| 5.6% |

| 5.6% |

| 5.6% |

| Net interest income |

| 1,531 |

| 2,045 |

| 2255 |

| 2255 |

| 2255 |

| 2255 |

| Provision (reversal) for credit losses |

| 35 |

| -73 |

| -800 |

| -800 |

| -800 |

| -100 |

| Provision rate |

| Noninterest income |

| 285 |

| 298 |

| 298 |

| 298 |

| 298 |

| 298 |

| Noninterest Expense |

| 796 |

| 859 |

| 963 |

| 997 |

| 1,032 |

| 1,068 |

| Amortization of tax credit and other investments |

| 96 |

| 118 |

| 118 |

| 118 |

| 118 |

| 118 |

| Other |

| 700 |

| 741 |

| 845 |

| 879 |

| 914 |

| 950 |

| PBT |

| 1,055 |

| 1,411 |

| 790 |

| 756 |

| 721 |

| 1,385 |

| Tax |

| 183 |

| 283 |

| 300 |

| 300 |

| 300 |

| 300 |

| Net Income |

| 490 |

| 456 |

| 421 |

| 1,085 |

| PE multiple, 10 yr median |

| 13.6 |

| 13.6 |

| 13.6 |

| 13.6 |

| Shares |

| 142 |

| 142 |

| 142 |

| 142 |

| Value per share |

| 78 |

| 104 |

| Current price |

| 54 |

Financial reports and our estimates

Risks

- Rapid defaults on CRE loans, especially in office and retail sectors.

- Contagion in the regional banking sector, potentially leading to deposit funding loss and forced liquidations at distressed prices.

- Possible need for additional capital, in the worst-case scenario.

- Contraction in net interest margins.

Conclusion

Despite the challenges posed by its exposure to commercial real estate loans, EWBC remains a profitable and well-operated bank and we believe it has the financial resources to overcome a rather adverse scenario with the commercial loans.

Its current valuation, significantly below historical multiples, is primarily attributed to market concerns. While the bank may face losses, particularly in the office space market, these losses should not be fatal, barring an outright panic. With a modest dividend payout and ample room for organic capital growth, EWBC's strong business fundamentals and attractive valuation make it a compelling investment.

For further details see:

East West Bancorp: Navigating Challenges In The Banking Landscape