DEA - Easterly Government Properties: 7.6% Yield Not Worth It

2023-06-02 03:59:08 ET

Summary

- Easterly Government Properties is an office REIT that leases primarily to US government agencies, offering high occupancy levels and long lease terms.

- The stock has been underperforming, and guidance suggests a decrease in FFO, making it a less attractive investment opportunity.

- The company's high dividend yield of 7.6% is appealing, but the balance sheet and potential future performance raise concerns, leading to a Hold rating.

Today I would like to take a look at an office REIT that leases primarily to agencies of the US Government – Easterly Government Properties ( DEA ). This can seem like a safer option for an investment into office REITs since it is not as affected by work from home as much as other sectors because institutions like the FBI or VA, which are some of the biggest tenants as I will discuss later on, simply cannot work from home to the extent that a computer engineer can. The portfolio has high occupancy levels and long lease terms so with a tenant base such as this one it sounds promising; however, DEA stock has been underperforming and the guidance suggests it will continue to do so. With that, let’s look at the company’s performance and see if it is worth investing in or not.

DEA owns 86 properties all across the United States, leasing a total of 8.7 million square feet. 62% of the buildings are offices, 20% VA outpatient, and the rest is dedicated to labs, courthouses, and other spaces that you would normally call a “government building”. They lease to the US government agencies such as the FBI, VA, FDI, DEA, FDA and others. Their occupancy is really high standing at 98.8% and the weighted average remaining lease term is 10.3 years. The obvious advantage of leasing to the US government is that the REIT doesn’t have to worry about collections at all. There is simply no way that the government is going to default on their rent payments. A second advantage has to the with the “stickiness” of the government as a tenant. It takes the administration much longer to make and approve a decision which means that it’s more likely to keep the status quo, renew their leases and stay in the existing buildings. When is the last time you saw a courthouse move into a new building?

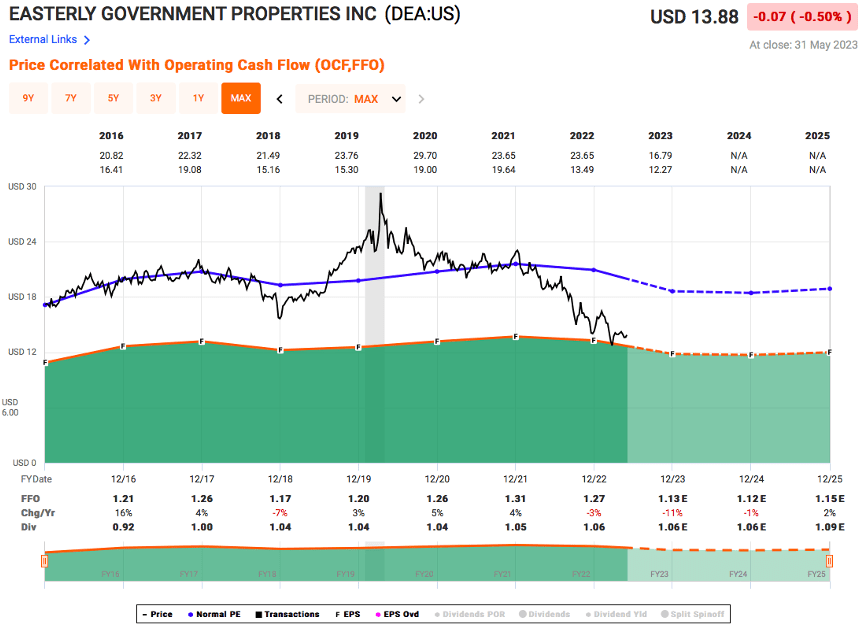

The core FFO for the first quarter was $29.5 million or $0.29 per share. For the last year, the core FFO per share was $1.24. The net income for the first quarter of 2023 was $4.4 million ($0.40 per share). The guidance provided by the company states that the FFO is going to be between $1.12-$1.15 in the next year which is a 7-10% decrease from this year’s FFO. This is in line with analysts’ consensus. DEA is a safety story, not a growth story.

Now I would like to take a look at their balance sheet. The debt totals in $1.2 billion with a weighted average interest rate of 3.7% and weighted average maturity of 5.5 years. They have no maturities in 2023 and only $160 million matures in 2024. That is great, however, what I do not like is the debt/EBITDA ratio that is 7.2x which is pretty high for any REIT and especially considering a large part of DEA’s portfolio is office. But seeing as the company has little maturities it is not an immediate threat, but definitely something that we should consider in the valuation.

DEA

The dividend of the company is really high standing at $1.06 per share per year ($0.265 per quarter). This translates to a dividend yield of 7.6% which is really solid when you consider that your tenant is the federal government. The payout ratio is 85% so the dividend is covered for now. But considering the guidance for the company there is a possibility the dividend will be cut in the near future or at the very least it will not grow at all.

The P/FFO of the company is 11.45x with a historical average of 16.48x. For reference, Corporate Office Properties Trust ( OFC ) which also leases to the US government agencies trades at 9.68x. Leaving me to believe that DEA is a bit overvalued.

Considering the firms current performance and the guidance that suggests a decrease in FFO I do not see DEA stock as a good investment opportunity right now. Sure, the yield is very attractive but I would not take it as a guarantee as of right now. Furthermore, even though the balance sheet is okay for now the company is not expected to perform well until their maturities are due and how they will deal with them could result in a further decrease. All of this leads me to a Hold rating.

{kind=link}

For further details see:

Easterly Government Properties: 7.6% Yield Not Worth It