DEA - Easterly Government Properties: At Risk Of A Dividend Cut

2023-08-01 10:01:26 ET

Summary

- Easterly Government Properties is a small REIT that leases properties exclusively to US government agencies.

- The risk lies in the expiration of leases, as the government may choose not to renew and consolidate its buildings to cut costs.

- DEA's dividend is at risk of being cut, as it is already barely covered by quarterly core FFO and the payout ratio is above 100%.

Dear readers/followers,

Investing in REITs can be very rewarding, but not all REITs are created equal. At a time of economic uncertainty, it's more important than ever to pick REITs that are well positioned to grow their cash flows and try to avoid those that are likely to see their cash flows contract and consequently be forced to cut their dividends.

Today I want to cover one REIT which I consider at risk of a dividend cut - Easterly Government Properties ( DEA ).

Easterly Government Properties

This is a relatively small REIT which owns just 86 properties located across the US. What makes the REIT special is that it leases its properties exclusively to agencies of the US government. What this means is that 98% of all rent is backed by the full faith and credit of the U.S. government.

{kind=link}

Having the government as your tenant has its advantages. Most of the leases are very long term with a WAULT of over 10 years and the REIT doesn't really have to worry about collections. The government will, of course, pay rent for the duration of the lease.

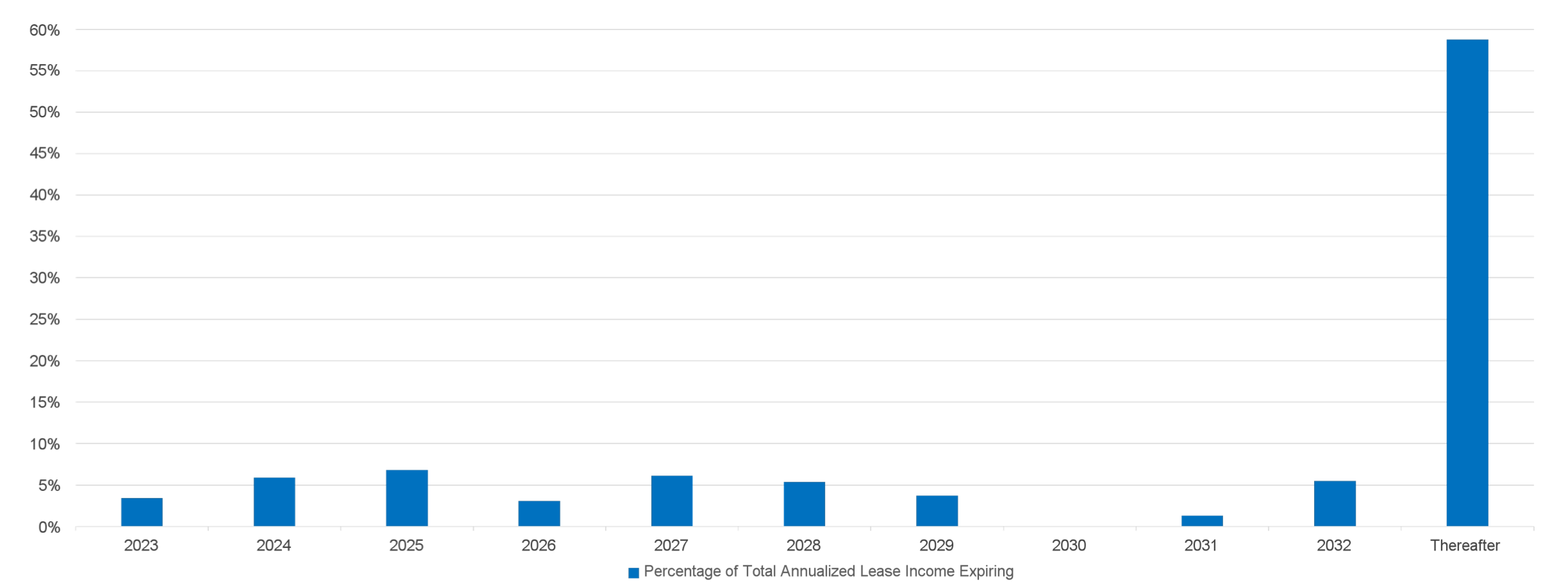

The trouble starts when leases expire, because just like any other tenants, the government is under no obligation to renew its lease. This is where part of the risk for DEA lies. Of course, it helps that near-term expirations are somewhat limited - just 3.4% this year and 5.9% next year.

{kind=link}

But eventually leases will expire. And the thing is that with the ever increasing budget deficit, the government might want to cut costs and consolidate some of their buildings.

Moreover, work from home might arguably be more of a threat here than to traditional offices, because the government is likely to have lower productivity standards for their employees than a private corporation, meaning that they may be more accommodating to employees staying on home office.

With less people in the office, this would likely mean that say two or three properties would get consolidated into one (perhaps newer) building. The risk to DEA's occupancy is obvious, particularly for office space.

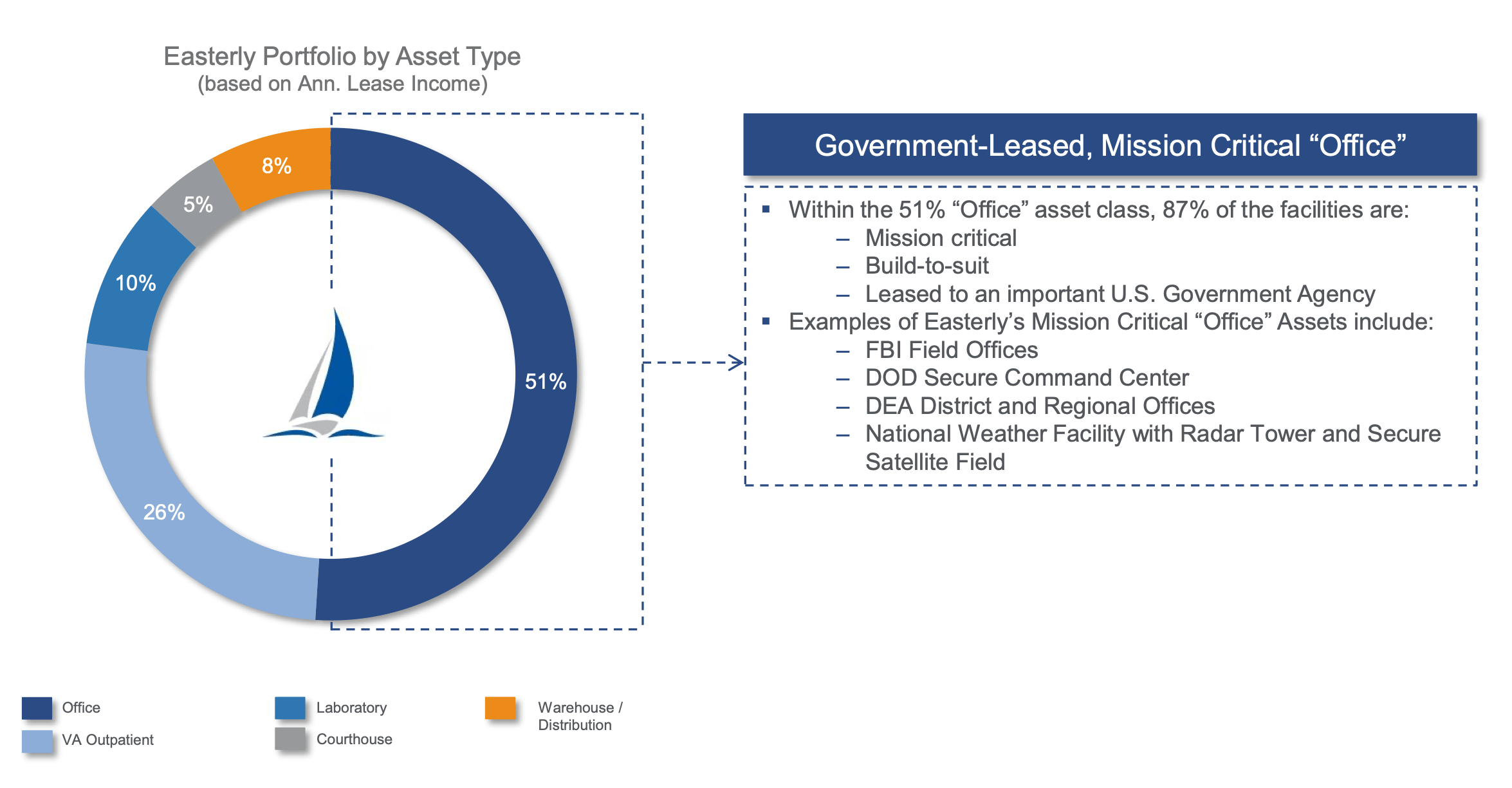

Office space accounts for 51% of total annual ABR, but the company claims that 87% of facilities are "mission critical". These include weather facilities with radars on the roof or government intelligence command centers.

These are, of course, unlikely to be done entirely from home, but the fact that the properties are almost entirely build-to-suit gives the government enormous bargaining power when renewing their lease.

DEA may have no alternative but to give the government rent discounts or higher improvements just to keep them in the building. This is why I expect FFO to be flat to slightly declining (as it has been) and definitely don't see growing cash flows.

{kind=link}

Currently, the REIT pays a quarterly dividend of $0.265 per share which translated into a yield of 7.5%. Management has confirmed on the most recent earnings call that they fully expect to keep the dividend as is, but the thing is that right now its barely covered by quarterly core FFO of $0.29 and when we include maintenance CAPEX, the payout ratio is already above 100%.

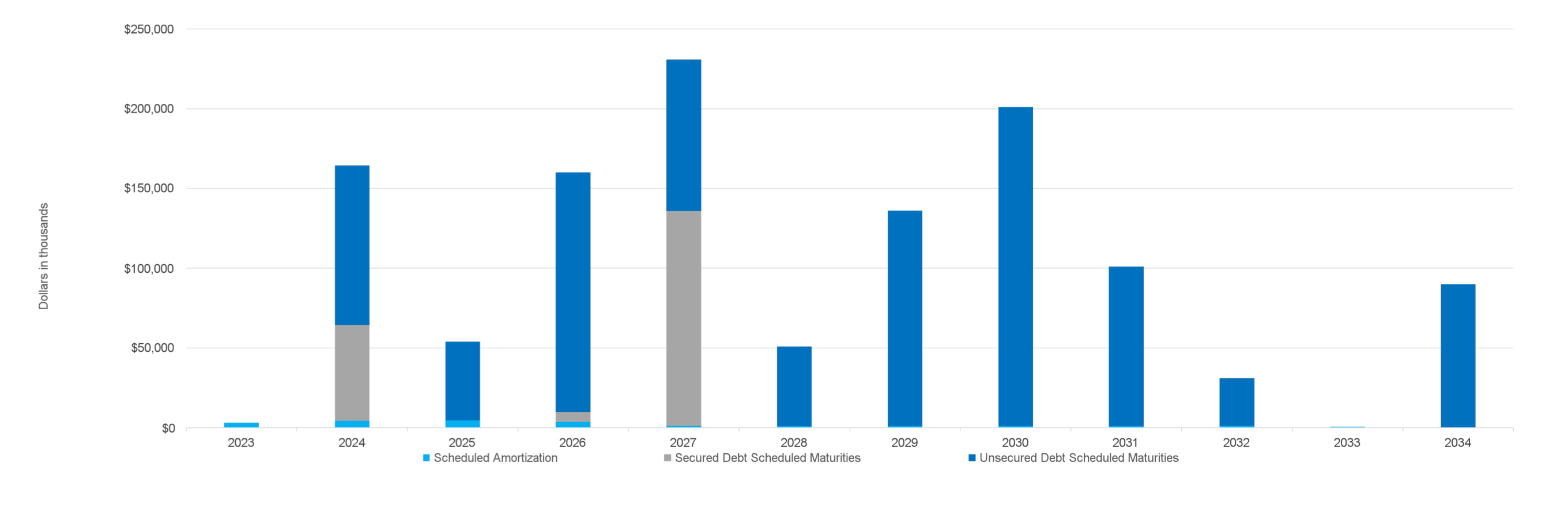

A dividend cut may be in the cards for Easterly Government Properties, but may come right away, because it would really discredit management which essentially confirmed the dividend on the last earnings call. Moreover, there are no debt maturities until the end of March 2024 so there is still more time for them to play the wait and see approach. As 2024 maturities approach, I think management will have no choice but to cut the dividend.

{kind=link}

Bottom line

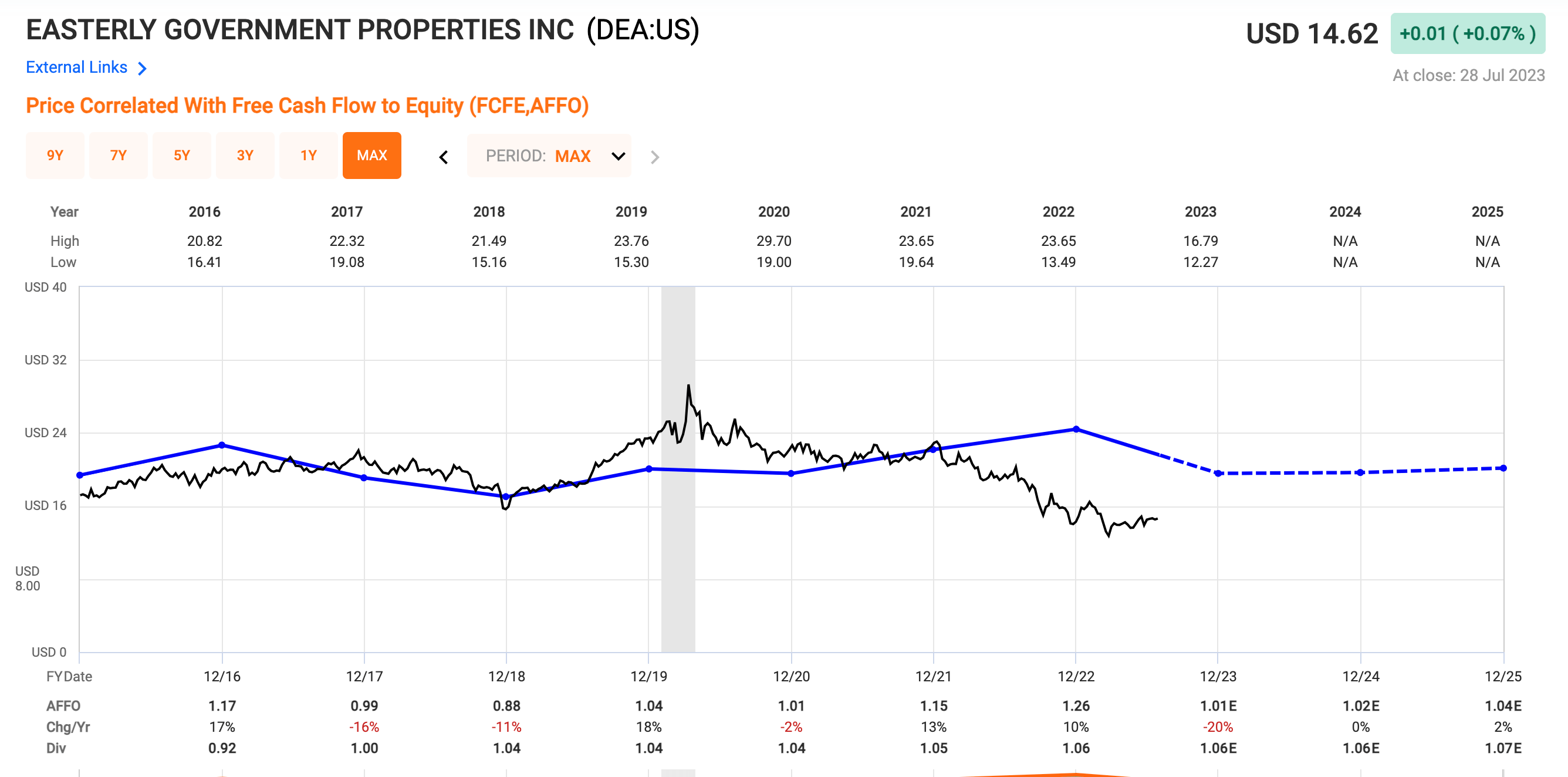

The bottom line is that business model hasn't proven itself over the years as per share AFFO has gone nowhere since 2015 (blue line below).

Going forward I expect much of the same, expect now the macroeconomic environment is tougher and interest rates are higher.

Beyond the dividend, which is now at risk of being cut, I see no other reason to invest in DEA's business. I consider the stock a value trap and rate it as a HOLD here at $14.60 per share.

{kind=link}

DEA is a great example of a REIT which promises safety, but fails to deliver value. It's important not to fall for such business models, because they're bound to underperform over a long-enough horizon.

DEA's price will be more stable than some of its peers, but the upside when things take off simply isn't there. That's why I will prioritize one of many undervalued REITs that have managed to grow their cash flows over the past year and a half and trade at more appealing valuations.

For further details see:

Easterly Government Properties: At Risk Of A Dividend Cut