DEA - Easterly Government Properties: Disappointing Guidance Outweighs The Attractive Dividend

Summary

- Easterly Government Properties has an interest in a portfolio of properties, leased primarily to the United States Government.

- Their properties are distinguished by full occupancy levels and long-duration leases to agencies serving essential functions.

- For income investors, shares offer an attractive dividend that is currently yielding 7% at current trading levels.

- The payout itself, however, is not enough to justify new initiation.

- Though there were many positives on their recent earnings release, guidance came in light and provided little to gain new bulls.

Easterly Government Properties ( DEA ) has an interest in a portfolio of properties that are primarily leased to agencies in the United States Government (“USG”) that serve essential functions.

Their portfolio is distinguished by full occupancy levels and long weighted average lease terms. The remaining lease terms on their existing leases, for example, are over ten years. And there have been several leases signed or will be signed at 20+ year terms.

The longer duration leases provide security and stability to the portfolio. A tenant class comprised principally of the USG is another competitive advantage in relation to other REITs due to the virtually non-existent risk of default.

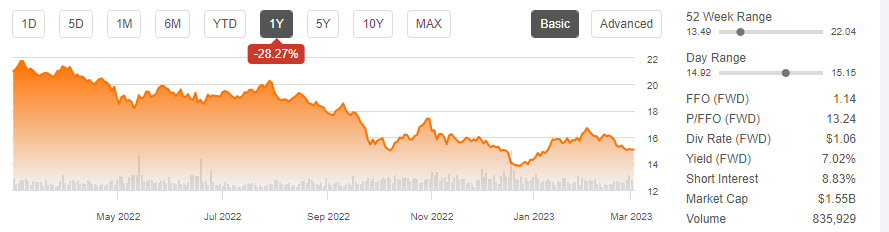

Given the defensive nature of their cash flows, one would expect the stock to outperform. On the contrary, shares are down nearly 30% over the past year. And since a prior update , they are down about 3%.

{kind=link}

Seeking Alpha - Basic Trading Data Of DEA

For investors, shares come paired with an attractive dividend that is currently yielding about 7%. This is on the higher end from recent years. While that may entice some, their recent earnings release didn’t impress enough to get bullish on the stock. There were certainly positive developments, such as a reduction in their floating rate exposure, a recent portfolio disposition, and positive leasing highlights. Guidance, however, came in light, due primarily to the loss of recurring income from their portfolio disposition, with no corresponding acquisition recycled into. As such, it may be best to keep shares on watch in the near-medium term.

Recent Performance and Current Portfolio Metrics

At December 31, 2022 , DEA had an interest, wholly or through their joint venture (“JV”) in 86 operating properties, 85 of which were leased primarily to USG tenant agencies. They also had one property under re-development that, when complete, is expected to be leased to the GSA for a period of 20 years.

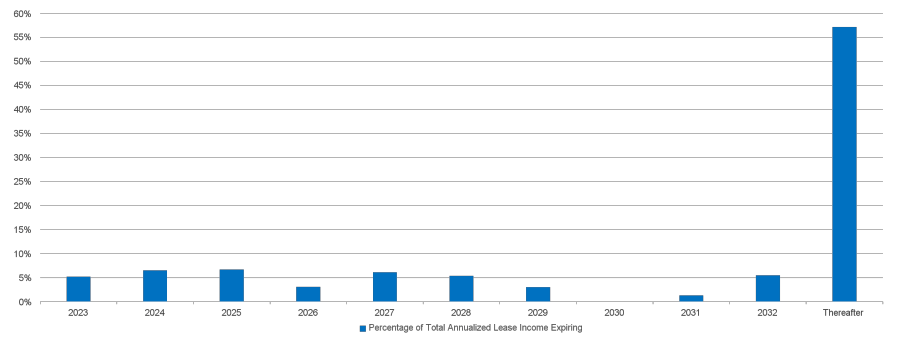

The properties within their portfolio currently have a weighted average age of 13.8 years and have a weighted average remaining lease term of 10.3 years. Looking ahead, they have less than 10% of their total annualized lease income expiring each year until at least the mid-2030s.

{kind=link}

Q4FY22 Investor Supplement - Lease Expiration Schedule

For those leases that have come up for renewal, DEA has achieved average rent spreads of approximately 8%. This is based on the execution of 11 renewals in 2022, excluding renewals at their Arlington and Fresno properties.

In addition, there were also a handful of leases that were signed but have either yet to commence or have commenced but are still pending tenant improvement approval from the USG, which creates a lag on the final spread realized. Ultimately, however, DEA is expecting to realize a renewal spread of 26% on these leases.

For the full fiscal year, DEA reported total adjusted funds from operations (“FFO”) per diluted share of $1.27. This is down from the $1.31/share reported last year, due primarily to the dilutive effect of a higher share count.

Looking ahead, management sees core FFO on a fully diluted basis in a range between $1.12 to $1.15/share. This incorporates the dilutive effects of their recent portfolio disposition, which generated about +$15M in annualized net operating income (“NOI”) in 2022. It also doesn’t factor in any acquisitions to their wholly-owned portfolio.

Liquidity and Debt Profile

In 2022, DEA acquired seven properties for a total contractual price of approximately +$252M. In addition, they completed their first portfolio disposition during the fourth quarter for total gross proceeds of just over +$200M.

This portfolio was comprised of ten buildings that had a weighted average age older than their current portfolio. The disposition is, therefore, believed to have increased the quality of their existing portfolio via a reduction in the overall weighted average age of their properties.

The net proceeds from the sale were used to pay down outstanding debt obligations. And as a result of the sale, they were able to reduce their floating rate exposure from 14.1% to 6.5%. In addition, it added further capacity to undertake any opportunistic acquisitions that may arise in later periods. At present, they have about +$385M available on their line.

DEA also expects to receive net proceeds of +$92.5M via the sale of the company’s common stock that has not yet been settled. This would add to the approximately +$9M previously raised in 2022.

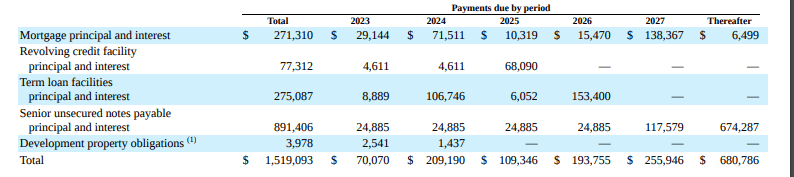

Nevertheless, net debt as a multiple of EBITDA still stood at over 7x at year end, which is on the higher side. This, however, is offset by their lower floating rate exposure than in prior periods as well as their current funding sources, which is sufficient to cover all of their short-term funding requirements.

{kind=link}

FY22 Form 10-K - Summary Of Contractual Cash Commitments By Year

Dividend Safety

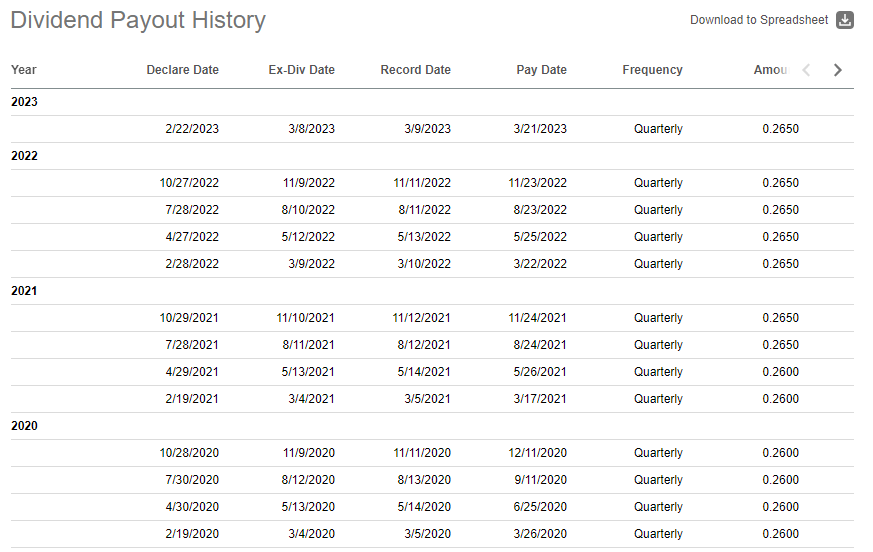

In 2022, DEA maintained a quarterly dividend of $0.2650/share after increasing it by just under 2% in the middle of 2021. The payout has been otherwise flat in recent periods.

{kind=link}

Seeking Alpha - Recent Dividend Payout History

At current trading levels, however, the dividend offers an attractive yield to income-focused investors, at about 7%. This is a modest premium over risk-free alternatives, such as U.S. Treasury’s, which are currently offering anywhere between 3.5-4.5%.

In 2022, the payout ratio came in at 83%, which, though covered, is above sector averages. And when looking ahead to 2023, the payout appears to be cutting it even closer on an estimated range of $1.12 to $1.15/share. This would bring the payout into the upper 90s at the low end of their range.

The reduction of their floating rate debt exposure helps, but their overall debt load is still high. The servicing costs on this could constrain liquidity, as could other reoccurring and necessary capital expenditures. While the yield is attractive, one would be remiss to tune out the risks of a rightsizing.

Final Thoughts

DEA’s overall portfolio remains secure. This is especially so after the renewal of their largest 2022 expirations for average durations of nearly 20 years. Furthermore, they appear to be realizing attractive spreads on their renewals. While the longer maturities do inhibit the company from capitalizing on mark-up opportunities, their embedded escalators on their existing leases provide an adequate offset.

The company also made significant strides in reducing their floating rate exposure, reducing it from 14.1% to just 6.5%. This was necessary, given their inherently higher debt load, which runs in the 7x range. This was made possible, in part, by their first portfolio disposition, which offloaded an older class of properties and generated over +$200M in gross proceeds.

The dilutive effects of the dispositions, via loss of operating income, however, resulted in disappointing guidance for 2023. In 2022, for example, DEA turned in FFO of $1.27/share. This compares to estimates of just $1.12 to $1.15/share in 2023. This incorporates both the effects of the disposition and assumptions for no acquisitions in 2023.

Yielding 7%, the dividend does provide one draw to the stock. But on forward guidance, the payout is breaching past a 90% payout. One could be forgiven, therefore, for not getting too comfortable with the continuity of the dividend; even more so, considering current operating leverage.

At 13x forward FFO, shares trade lower than Postal Realty Trust ( PSTL ), which is another REIT that serves the USG, but higher than Corporate Office Properties Trust ( OFC ), which perhaps has more upside at its current trading levels, at just 10.6x. For investors, the upside appears limited for DEA in the near-medium term, and their dividend, though attractive, isn’t entrenched enough to justify new initiation.

For further details see:

Easterly Government Properties: Disappointing Guidance Outweighs The Attractive Dividend