DEA - Easterly Government Properties: Is The 7.71% Dividend Yield Safe?

2023-04-03 05:41:19 ET

Summary

- Easterly Government Properties touts itself as a unique Office REIT, unlike other office REITs that have been hit hard because it has tenants that are unlikely to default on rent payments.

- However, there are other risks to having a single customer (i.e. US government) that are unrelated to rental default, risks that other types of REITs do not experience.

- 35 of the 119 leases or 29.4% of its leases are set to expire within the next three years.

- These 35 leases represent 18.4% of the DEA's total annualized lease income. If DEA is unable to renew these leases, it stands to lose almost a fifth of its 2022 income.

- Debt repayment for the next few years may be difficult for DEA to handle without cutting its dividend. It has already resorted to selling physical assets and pausing acquisitions.

Preamble

Our leases with U.S. Government agencies are backed by the full faith and credit of the U.S. Government... Furthermore, the U.S. Government has never experienced a financial default to date. In addition to stable rent payments, our U.S. Government leases typically have initial total terms of ten to 20 years with renewal leases having terms of five to 15 years. U.S. Government leases governing properties similar to the properties that we target have historically had high renewal rates, which limit operational risk...

As of December 31, 2022, our operating properties were 99% leased with a weighted average annualized lease income per leased square foot of $35.28 ($34.96 pro rata) and a weighted average age of approximately 13.8 years based on the date the property was built or renovated-to-suit, where applicable.

The above was taken from the Easterly Government Properties (DEA) 2022 Q4 10K (pages 4 and 30).

REIT investors will find these very attractive; an almost 0% vacancy rate in relatively young properties tenanted to the US government, an entity with a AAA credit rating so it is unlikely to default on rent payments, with options to renew leases.

I have had my eyes on DEA since July 2022 because of the above pluses. However, I had concerns that stopped me from pulling the trigger so I decided to observe the business and listen to earning calls for a few quarters. In hindsight, I was glad I did not invest in DEA since from 2 July 2022 to 1 April 2023, the stock price has fallen by 35%.

What happened? Was DEA falling in sympathy with other office REITs? Or is DEA facing issues of its own?

In this article, I will examine some of the factors that investors should take note of when investing in DEA.

Business Overview

The company describes its business in the 10K as follows:

We are an internally managed real estate investment trust, or REIT, focused primarily on the acquisition, development and management of Class A commercial properties that are leased to U.S. Government agencies that serve essential functions. We generate substantially all of our revenue by leasing our properties to such agencies either directly or through the U.S. General Services Administration, which we refer to herein as the GSA. Our objective is to generate attractive risk-adjusted returns for our stockholders over the long term through dividends and capital appreciation.

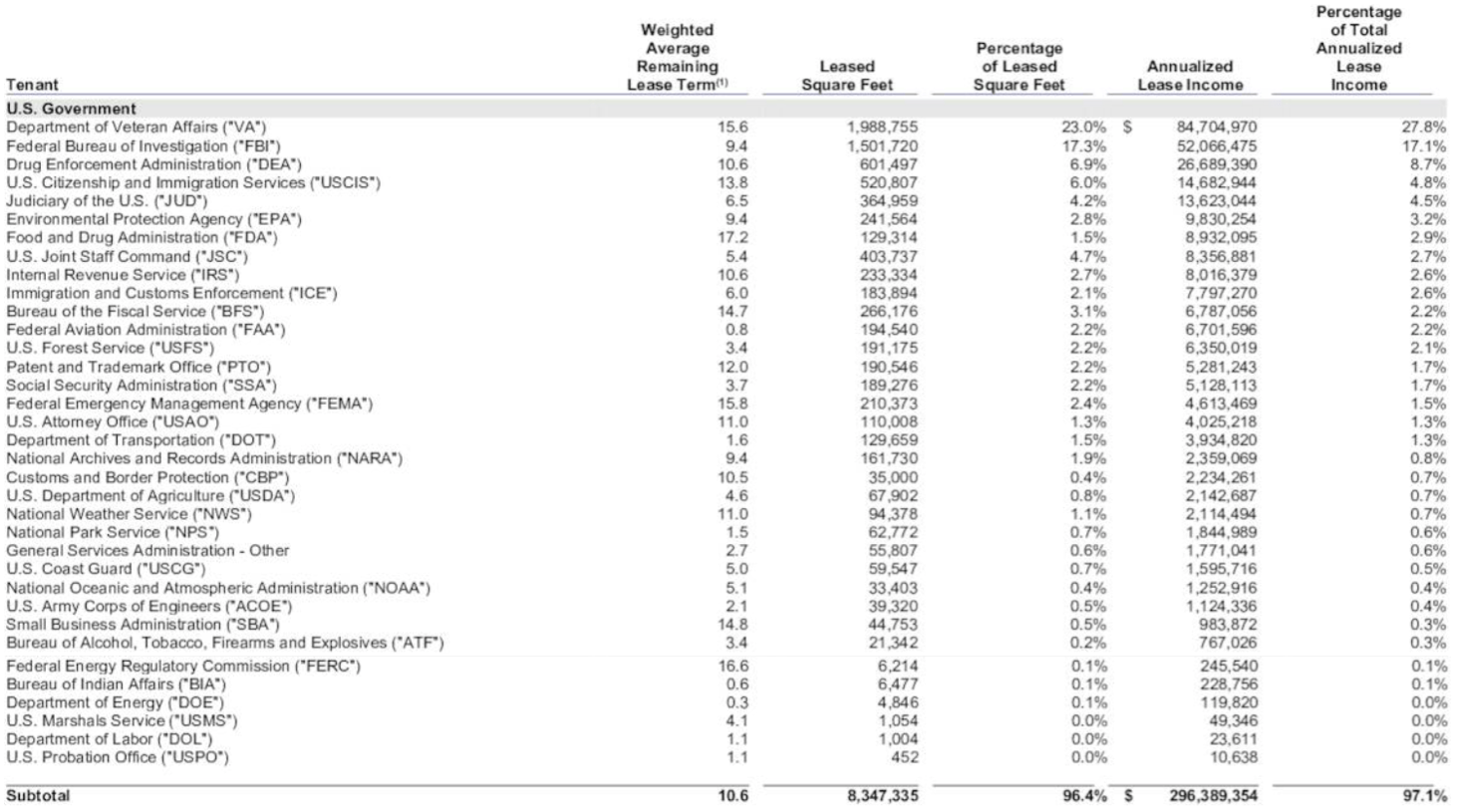

Who exactly are DEA's tenants?

Think of all the 2-and-3-letter acronyms representing different government agencies and you are probably right: FBI, VA, EPA, FDI, DEA, CBP, FDA and more.

DEA Q4 2022 Investor Presentation Slides

{kind=link}

DEA boasts of owning 86 properties as of 31 December 2022, which is slightly down from the 89 it owned as of the end of 2021 but still way up from the 79 it owned as of the end of 2020, the 70 it owned in 2019, and the 62 in 2018. This represents a growth rate of 38.7% in the number of properties owned in 4 years . Bear this in mind as I will return to this later.

DEA's funds from operations ((FFO)), a measure of cash flow from its operations, grew from $1.17 per share in 2018 to $1.26 in 2022, a 7.7% FFO growth in 4 years .

Next, I will examine possible reasons for the price decline.

REITs Have Been Under Pressure in 2022

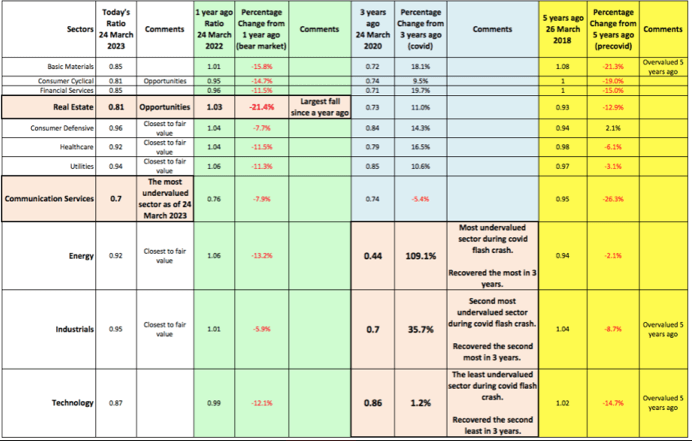

The following table was compiled on 24 March 2023 from data from Morningstar's Fair Value page.

Data were taken from Morningstar's FV page

{kind=link}

A ratio of 1 means the sector is trading at fair value as determined by Morningstar analysts' assessment of fair value. A ratio below 1 means the sector is trading below fair value.

The two most undervalued and beaten-down sectors are Real Estate at 0.81 and Communication Services at 0.7. DEA belongs to the REIT sector. According to an article by Seeking Alpha Contributor and REIT expert Jussi Askola, he listed more than 24 different types of REITs, and DEA is in the Office REITs sub-industry.

Jussi Askola wrote:

95% of REITs are not investing in office buildings, and yet, they are all heavily discounted, guilty by association.

So, is DEA falling just because it is guilty by association, being lumped in with other Office REITs?

Management begs to differ. In the 2022 Q4 earnings call , DEA's chairman Darrell Crate set the stage for the decline in this sector. He said:

I'm going to contrast our business, with office because many of the analysts who follow our company compare our performance to the office universe of REITs. One meaningful way our portfolio is differentiated from office is our occupancy profile. As we've seen, office has been materially affected by the adoption of work from home flexibility that was born from the pandemic . For DEA, our mission-critical facilities support agency functions that require worker collaboration. You can't close down a met lab from your dining room table.

CEO Bill Trimble followed up with his take that DEA is not just another Office REIT:

Other office REIT's earnings calls this quarter are centered around several themes including work-from-home trends , building occupancy percentages , local market metal rates, subleasing activity and projected layoffs in various industries that might result in real estate downsizing.

To be clear, these are not of concern at Easterly . We invest for the mission of the government's paramount and the federal employees need to work from our facility cannot be accomplished in their homes.

In short, DEA is unlike other office REITs because unlike the rest its tenant is the US government and due to the nature of government agencies like the Food and Drug Administration and Drug Enforcement Administration with their special laboratories designed to their specifications, or the National Archives and Records Administration with their specific requests for temperature and humidity controlled rooms for storing documents, these workplaces just cannot shut down easily like typical offices, and people who work in these places cannot simply transit to a work-from-home arrangement as special facilities are needed due to the nature of their work.

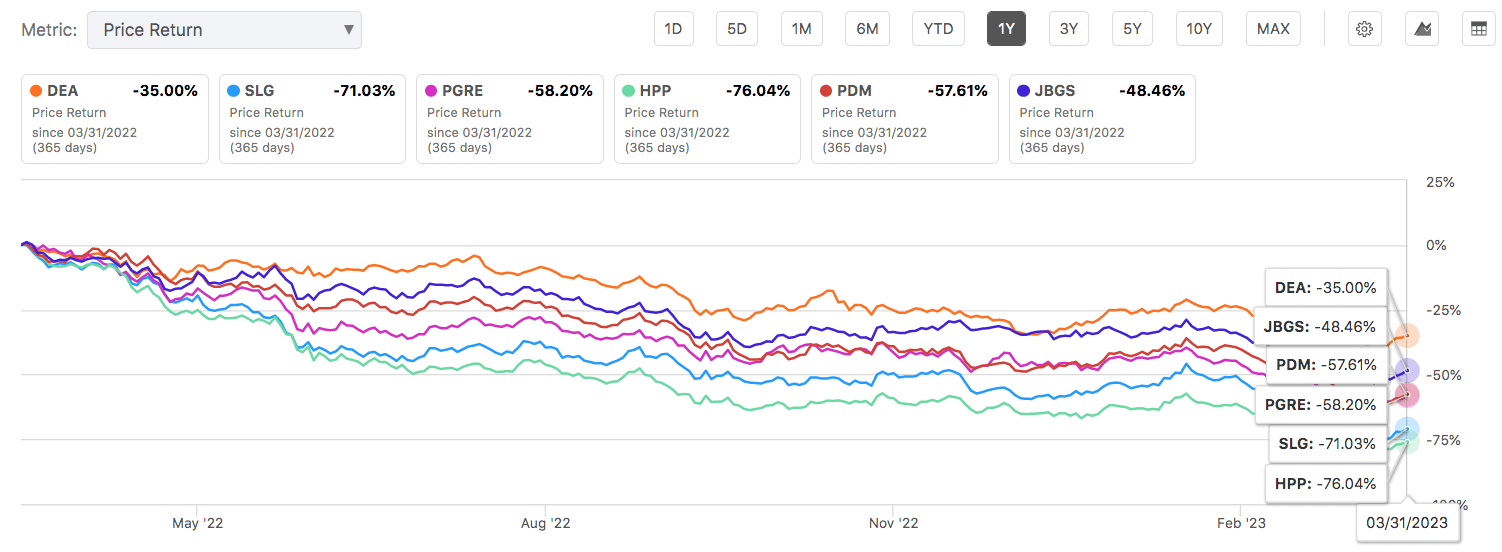

Yet, DEA has fallen hard in the past year, like other Office REITS (see chart below), although its 35% decline is less traumatic than some of its peers.

Seeking Alpha DEA Peer comparison

{kind=link}

DEA is not facing issues that are plaguing other office REITs like occupancy rates (99% occupied), tenant quality (US government with AAA credit rating) and changing work trends like work-from-home trends due to the pandemic (many agencies are mission-critical and require special work environments like laboratories that are only available in the official workspaces), and the average remaining lease term was 10.3 years.

However, a REIT can lose rental revenue in other ways even if the tenant profile is great and everything above is true.

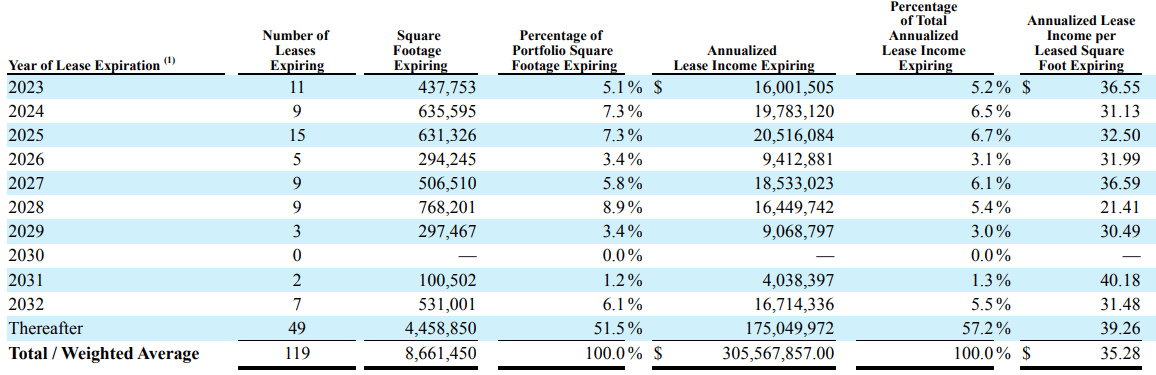

29.4% of The Leases Are Expiring in 3 Years

According to this table on page 38 of the 2022 Q4 10K , 35 of the 119 leases or 29.4% of its leases are set to expire within the next three years. If not rectified, this can become a problem as these 35 leases represent 18.4% of DEA's total annualized lease income.

{kind=link}

Now, management has claimed in the 10K ( page 4 ) that renewal rates are high, that:

U.S. Government leases governing properties similar to the properties that we target have historically had high renewal rates, which limit operational risk.

However, the company has not reported actual renewal rates to support this claim. In the Q 4 2022 Earnings Presentation slides 18-20 , only three leased properties have one 5-year renewal option built into the contracts (JUD Jackson, SSA Charleston, and DEA Albany), and when renewed, these three properties only represent a total of 2.1% of DEA's 2022 total annualized lease income. There is no guarantee that government agencies will renew their leases. The company admitted to that possibility in its risk summary section ( page 2 ):

We may be unable to renew leases or lease vacating space on favorable terms or at all as leases expire, which could adversely affect our business, financial condition and results of operations.

The company claims on its website that the management team has :

over two decades of exclusive focus on acquiring U.S. Government leased assets, and over 30 years of experience developing nearly five million square feet of build-to-suit construction.

However, the fact remains that DEA is a relatively new company. It launched its IPO only in 2015. This means the company is just starting to come into a period where many of the properties that it is handling are entering the phase where the leases are either expiring or nearing expiring and in DEA's case a staggering 29.4% of the leases are set to expire within the next three years, which represents 18.4% of its annualized rental income. Even after accounting for the three properties with the single 5-year renewal option, DEA is still facing a loss of 16.3% of its annualized rental income within the next three years.

This is not a hypothetical risk, the kind of companies includes in their "risk summary" section just to protect themselves from legal liabilities. As recently as Q3 of 2022, DEA had to realize an impairment cost for one of their properties.

In the third quarter of 2022, we recognized an impairment loss totaling approximately $5.5 million for our ICE - Otay property and reduced its carrying value to its estimated fair value, which declined due to the changes in expected cash flows related to the existing tenant's lease expiration in 2022. ICE - Otay is a 47,919 rentable square foot office building located in San Diego, California

Having such a strong tenant (with an AAA credit rating) is both a plus and also a weakness as there is no diversification in its revenue source since 97.1% of DEA's current rents come from U.S. Government tenant agencies and the company expects that leases to these agencies will continue to be the main source of revenues in the future.

I am surprised that management did not say more about this, or that analysts did not probe management further. Perhaps analysts are confident in the management. Perhaps the management team knows what it is doing. After all, CEO William C. Trimble has been involved in real estate investing as early as 2009 when he was the Chief Operating Officer of an investment management firm that managed funds that invested in properties that were leased to the U.S. General Services Administration, or GSA. And the executive vice-president and vice chairman of the board of directors Michael P. Ibe was the co-founder of Western Devcon in 1987, a real estate company that focused on the acquisition and development of built-to-suit GSA properties.

I will maintain my healthy dose of skepticism and conservatism and wait to see how management overcomes this hurdle. I will let data form my opinion, and if the data from the next three years show that DEA has no problem renewing the leases on these 35 properties, I will relook at DEA through a different set of lenses.

After all, despite its unique tenant profile, DEA is still a REIT and faces similar issues that other REITs face, and this is the segue to the next concern.

Can DEA Maintain The 7.71% Dividend Yield?

REIT Basics

REIT investors are typically income investors; at least I am and that is what REITs are supposed to do in my portfolio. The most important thing for income investors is dividend safety and consistency, and DEA with its strong and unique tenant profile seems to fit the bill. A high occupancy rate plus an almost 0% chance of rental default makes a landlord happy.

In order to grow their portfolio and rental income, REITs would usually acquire new properties or assets, and funds are needed to do that. And since REITs are legally obligated to pay out at least 90% of their taxable income to shareholders, REIT managers have to raise the funds they need for acquisition in two ways. They either take on more debt - which will result in more interest repayments - or they can issue more shares.

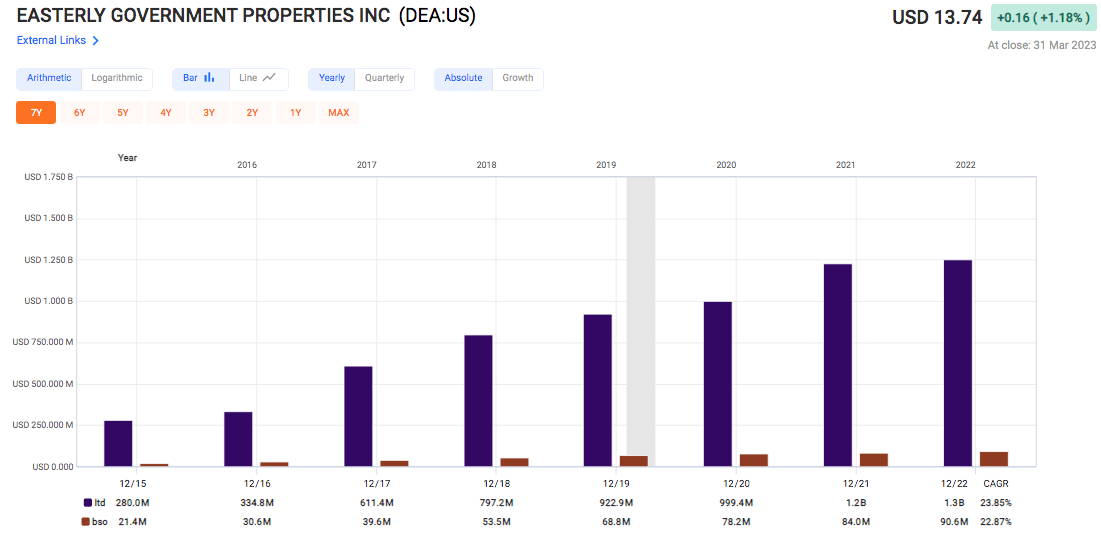

DEA, like other REITs, has done both. Long-term debt has increased at a CAGR of 23.85% from $280 million in 2015 to $1.3 billion in 2022, while the number of basic shares outstanding has increased at a CAGR of 22.87% from 21.4 million in 2015 to 90.6 million in 2022.

Fast Graph Long-Term Debt and Basic Shares Outstanding

{kind=link}

Taking On More Debt And Issuing More Shares Were Fine - Until They Weren't

Taking on more debt when interest rates were near to 0% was fine in the pre-pandemic era of low-interest rates. If not, DEA would not have been able to increase the number of properties in its portfolio from 29 in 2015 at 2.1 million square feet in total leased space, to 86 properties covering 8.7 million square feet of leased space. In the three years leading up to now, DEA acquired a total of 27 properties from 2019 to 2021.

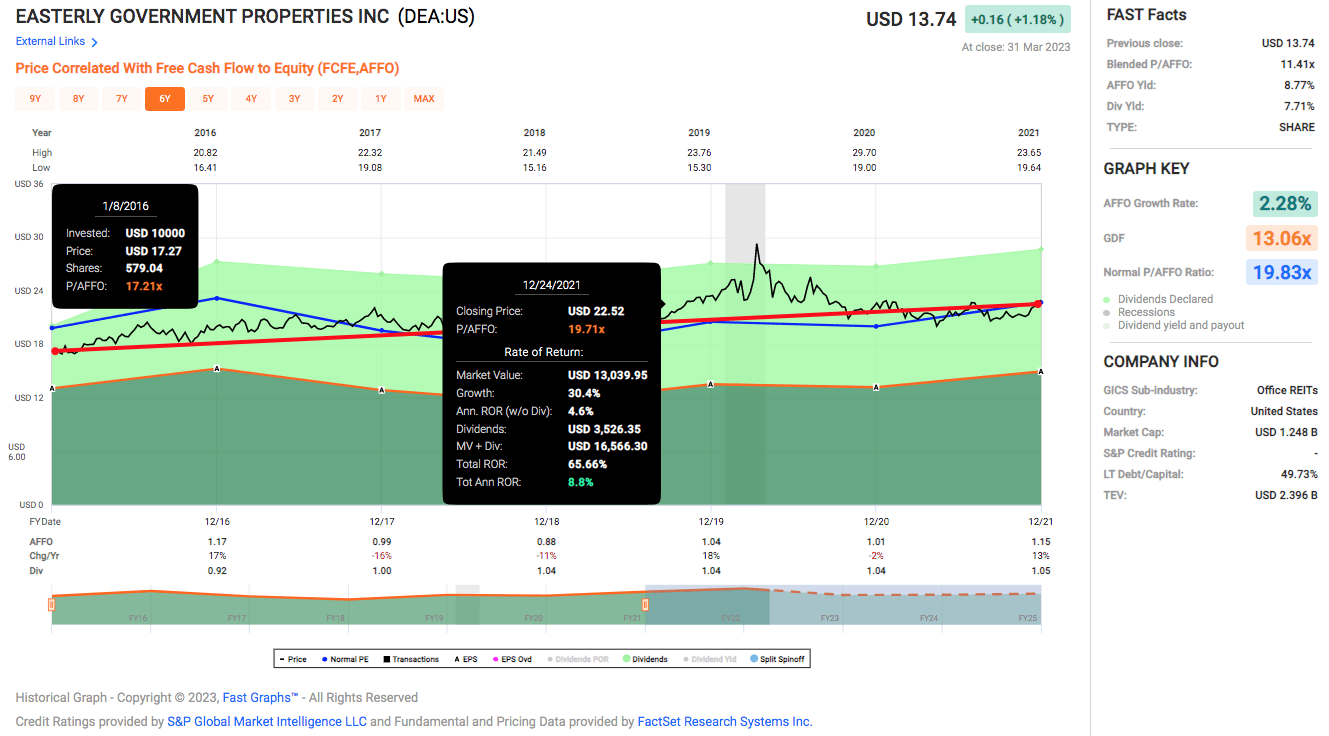

DEA's stock price often exceeds $19 per share between January 2016 and December 2021. Issuing shares at that price, which was often trading above its normal P/AFFO of 19.83, was a good move as investors were willing to pay a premium for DEA's dividends which were perceived as safe.

Fast Graph Jan DEA 2016 to Dec 2021

{kind=link}

In the past year, with the share price plummeting 35%, issuing more shares now may not raise enough capital. During the Q4 2022 earnings call, the CFO seems confident that DEA does not need to raise cash by issuing more shares.

As previously mentioned, we believe there may be the potential to help distressed developers. With over $434 million in debt capacity and just under $93 million in unsettled forward equity, Easterly has ample opportunity to execute on accretive deals without needing to go to the capital markets.

If DEA is not issuing more shares, it has to take on more debt, but if DEA does deploy more debt, that will incur more interest costs.

The company warns in the 2022 Q4 10K (page 13) of possible adverse actions that it may have to take if it is not able to raise sufficient capital on good terms:

If sufficient sources of external financing are not available to us on cost effective terms, we could be forced to limit our acquisition , development and renovation activities or take other actions to fund our business activities and repayment of debt, such as selling assets , reducing our cash dividend or paying out a smaller percentage of our taxable income (subject to the annual distribution requirements applicable to REITs under the Internal Revenue Code of 1986, as amended (the "Code")).

There are four possible measures that the DEA could take:

- Selling assets

- Limiting acquisition

- Reducing cash dividends, or

- Paying out a smaller percentage of the taxable income.

The company has already carried out the first two measures of limiting its acquisition activities and selling assets. The CEO Bill Trimble said in the Q4 2022 earnings call :

The disposition portfolio was comprised of 10 buildings, approximately 668,000 leased square feet, with a weighted average age that was older than the remaining and now current portfolio.

The CFO added that:

At this time, our guidance incorporates the dilution from the disposition of our 10-property portfolio but does not yet assume any wholly-owned acquisitions for the year .

DEA has to take strong measures. It adjusted the mix of its floating-rate and fixed-rate loans so it has more fixed-rate loans (93.5%) than floating-rate ones (6.5%, down from 14.1%) of all outstanding debt obligations to have more visibility into its cash flow.

The big question now is whether the implementation of the first two measures is sufficient to allow DEA to maintain its dividend. Selling the 10 properties allowed DEA to raise cash to pay down debt without taking on more debt or going to the capital markets, but that was not a perfect solution. With a decline in the number of properties, DEA naturally expects to collect less rental income in 2023. And if it does not acquire (or could not afford) more properties, it cannot increase its rental income.

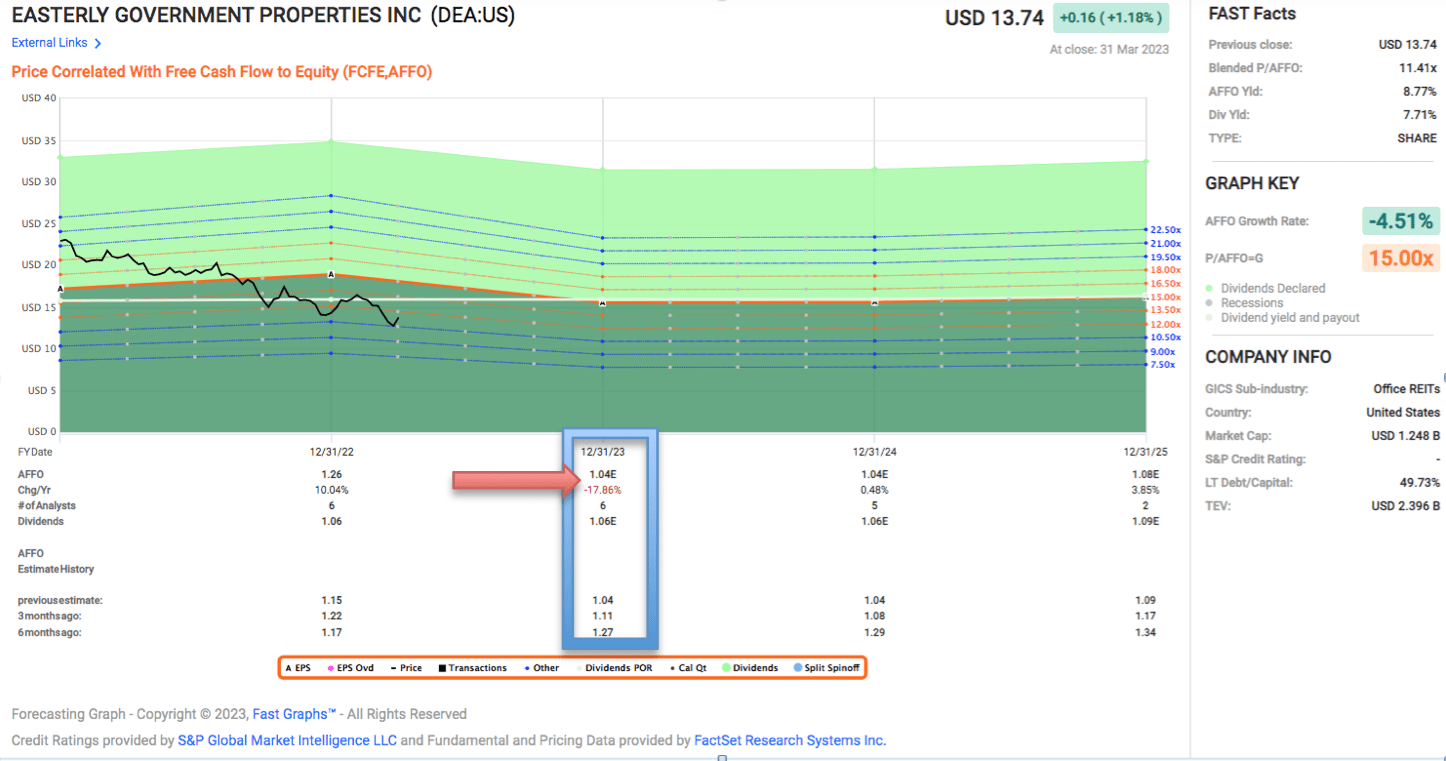

The 6 analysts from FactSet are bearish, expecting a 17.86% decline in AFFO from $1.26 per share in 2022 to just $1.04 per share in 2023, and they expect the AFFO to remain at $1.04 in 2024 and only to recover slightly to $1.08 in 2025. On an FFO basis, that translates to a 10.4% decline from an FFO per share of $1.27 in 2022 to $1.14 in 2022. That forecast is in line with the higher end of management's core FFO per share guidance of between $1.12 to $1.15.

{kind=link}

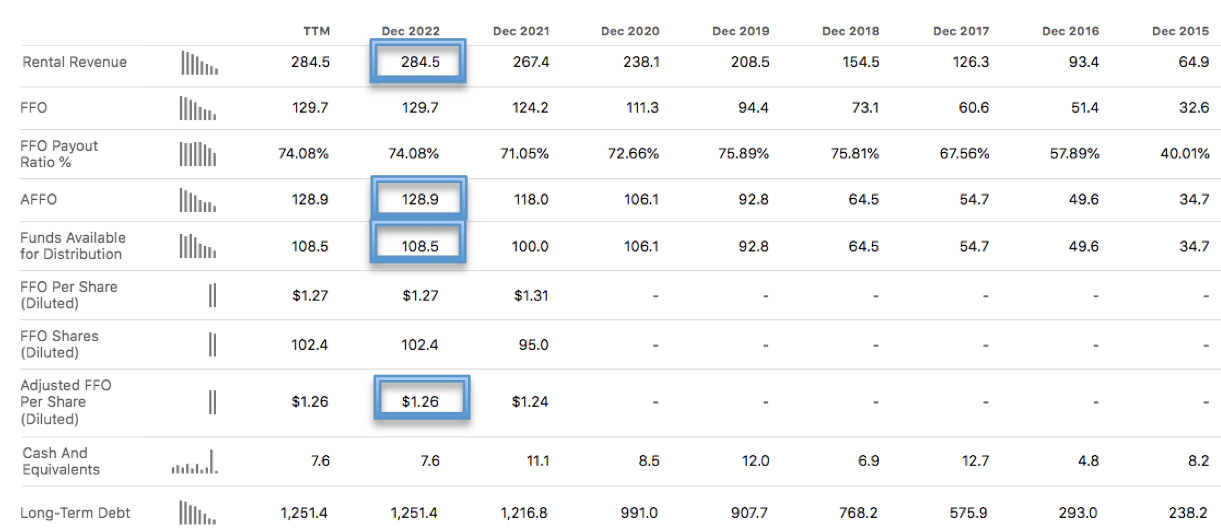

In 2022, DEA generated $284.5 million in rental revenue, and after accounting for capital expenditures and maintenance costs, it has adjusted funds from operations ((AFFO)) of $128.9 million remaining, just sufficient to distribute $108.5 million in dividends, leaving around $20 million for future deployment. Together with the $7.6 million in cash and cash equivalents that it has, DEA may have up to $27.6 million by Q1 of 2023 for reinvestment.

Data collated from Seeking Alpha Financials Pages

{kind=link}

To maintain the $1.06 per share cash dividend payout in 2023, and assuming that DEA stops issuing shares this year, it needs to have $1.06 x 90.4 million shares outstanding = $95.8 million of distributable cash in 2023.

If the analysts are right about the AFFO forecast of $1.04 per share, then DEA is expected to have $1.04 x 90.4 million = $94 million for cash dividends, which is insufficient if the dividend payout of $1.06 per share is maintained.

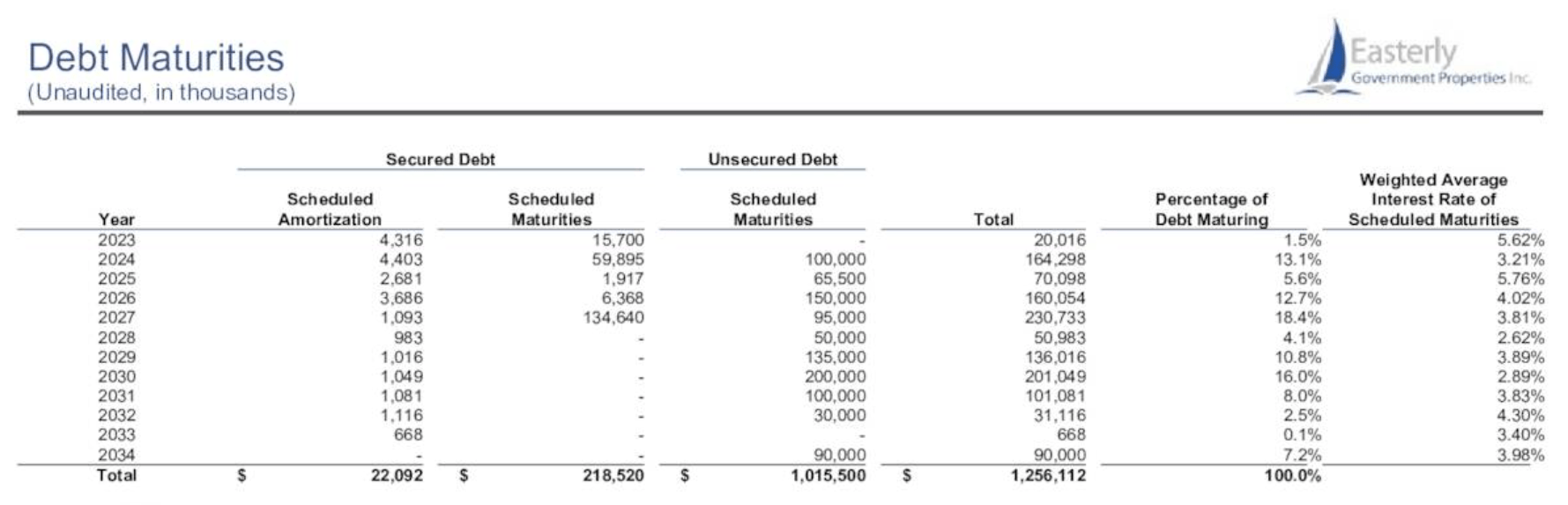

DEA has a $15.7 million loan due in 2023 and another $164 million due in 2024. The supposed $27.6 million may be sufficient to shore up the cash shortfall for dividend distribution and to pay down debt in 2023 without the need to issue more shares or take on more debt, but 2024 will be different. And I have not yet gone into debt repayment in the not-so-distant future of 2025, 2026, etc.

{kind=link}

Will DEA need to sell more properties in 2023 to pay down debt in 2024, which will reduce its portfolio value and rental income, and call into question the multiple acquisitions from earlier years?

Will it take on more debt at higher rates? DEA still has $384 million in capacity remaining on its line of credit.

Or will it take the third measure of reducing cash dividends?

I do not know what management will do but it may not have many choices left with debt repayment looming.

Conclusion

Easterly Government Properties is a unique Office REIT that derives rental income almost exclusively from leasing properties to US government agencies. Backed by the full faith of the US government and its AAA credit rating, a 99% occupancy rate, a near 0% chance of tenancy default, and in the past 8 years, DEA has never cut its dividend once, not even during the pandemic, DEA appears to be a safe choice for income investors.

At first glance, the 35% in DEA's stock price is an aberration since its tenancy profile is largely different from other office REITs, and it was unjustly punished along the decline in the Office REITs category, and in such a situation, DEA may be a value investor's dream as it suggests that DEA could be a company that has been grossly mispriced.

However, there are issues that investors have to be aware of.

35 of the 119 leases or 29.4% of its leases are set to expire within the next three years. These 35 leases represent 18.4% of the DEA's total annualized lease income. If DEA is unable to renew these leases, it stands to lose almost a fifth of its 2022 income. And since these facilities had been configured to meet the needs of existing tenants, even if DEA is able to find new tenants, the company will have to incur additional costs to redevelop the existing properties to meet the needs of the new tenants. It is likely that with the expertise and experience of the DEA leadership, the company should be able to renew these leases since it has invested a lot in the properties according to the needs of the tenants to increase the likelihood that they would continue their lease but as of now, this is still far from a certainty.

Compounding the potential threat of revenue decline is the looming debt repayment of a quarter of a billion dollars in the next three years. DEA does not have a lot of cash on hand and it had to sell 10 properties in Q4 of 2022 to raise cash to pay down some debt, which incidentally reduces its rental income for 2023. At the moment, it is difficult to see any good options available to the company to meet its future cash needs and shareholders' expectation for the company to grow. It has adjusted the mix of its floating-rate and fixed-rate loans so it has more fixed-rate loans (93.5%) than floating-rate ones (6.5%, down from 14.1%) of all outstanding debt obligations. Management has declared that it is not going to the capital market to raise cash. It has already taken other measures such as selling assets and pausing acquisitions. What is left on the table is reducing cash dividends. DEA may not need to reduce its dividend but I will not be surprised if it does. The best scenario may lie in having another REIT with a stronger balance sheet buy out DEA at a premium to get its business and assets but that is pure speculation and income investors do not speculate; we invest in predictable cash flows and dividend payout. Even in the unlikely scenario that DEA does get bought out, existing DEA shareholders will lose that stream of dividend income and have to find a replacement dividend income stream.

Although I like DEA's business model of renting to a tenant of superior quality, I think management might have expanded the business a little too fast in the earlier years and as a result, took on more debt than it could comfortably handle once the interest rate environment changed unexpectedly and rapidly in the past 18 months. I will avoid DEA for now and observe how the management navigates the next 12 to 24 months.

For further details see:

Easterly Government Properties: Is The 7.71% Dividend Yield Safe?