EBC - Eastern Bankshares: Better Opportunities Are Out There

2023-08-12 09:16:38 ET

Summary

- Eastern Bankshares has struggled this year from a deposit and profit perspective.

- Despite this, the picture for the company is not all that bad, but it's not particularly great either.

- Shares look pricey and there are multiple signs of weakness that make this a subpar process.

For months now, I have been looking into the banking sector in the hopes of finding some really attractive prospects. I have found some companies that have been appealing, while some others have fallen flat. My original desire stemmed from the idea of buying on the cheap following the banking crisis that erupted in March. One of the firms that I recently came across is Eastern Bankshares (EBC). In recent years, management has done a good job growing the company's net interest income and net profits. In response to a surge in deposits. But so far this year, the bank has struggled some. I could handle some of these struggling if the stock were cheap enough. But when you really drill down, shares are actually a bit lofty compared to many of the other players that are out there today and there are some other worrisome signs that make this, at best, a 'hold' candidate.

A mediocre play

Operationally speaking, Eastern Bankshares is far from the smallest bank out there. But with a market capitalization of $2.37 billion as of this writing, it is quite small. For those not aware of the firm, it operates as a bank holding company that's based out of Boston, Massachusetts. Shockingly, the institution dates back to 1818, making it one of the oldest banks still in existence. With over 120 branches in operation, the company has a rather sizable footprint. For the most part, its presence is centered around the Boston area. However, it also has locations throughout the rest of Massachusetts, as well as in Southern New Hampshire and Northern Rhode Island.

Through its branches, the company provides customers a wide array of services. These include deposit related offerings, wealth management services, insurance products, and a variety of loans. It even provides automated lock box collection services, cash management services, account reconciliation services for corporate and institutional customers, and more. Even though the company has a large physical footprint, it boasts only a small market share in the seven separate banking markets tracked by the Federal Reserve Board that it operates in. This market share is about 5.4%. Even in Boston, where the company gets 94.9% of its deposits from, it has a market share of only 3.5%. However, this does place it as the 5th largest firm in that area.

{kind=link}

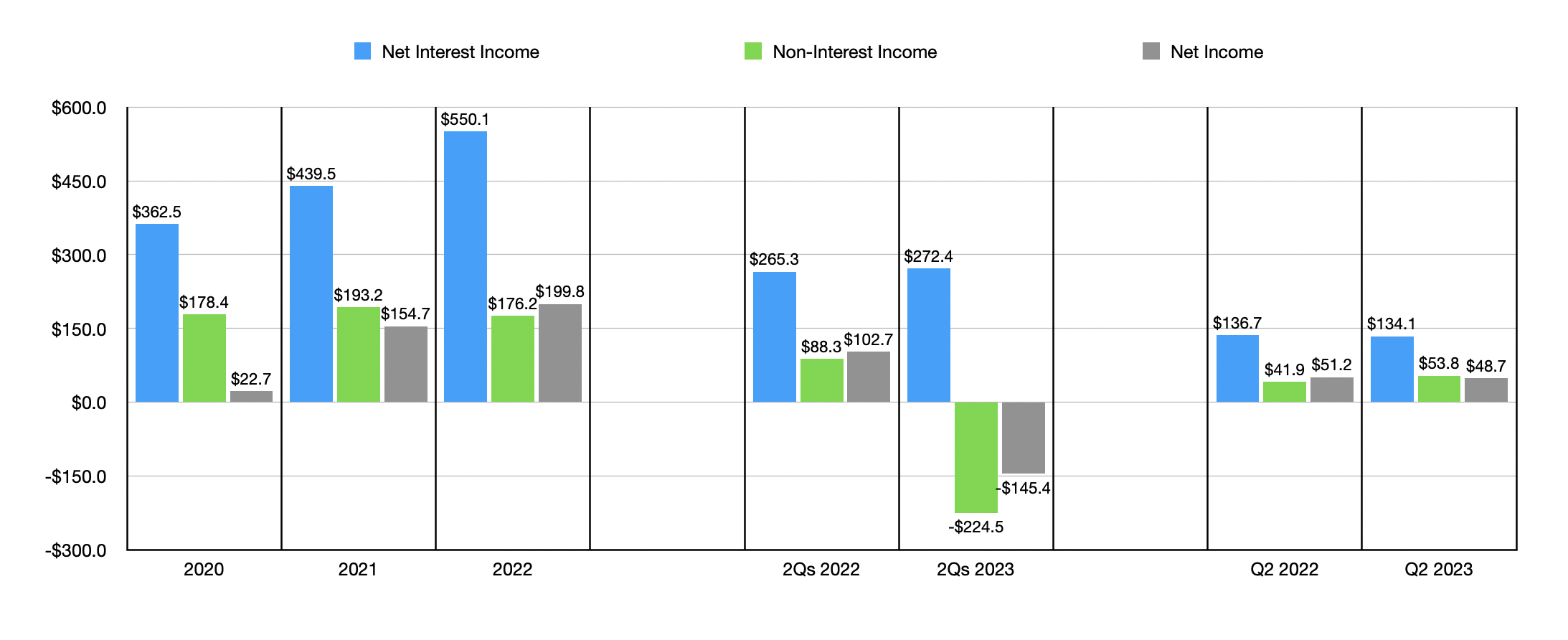

Over the past few years, management has done a good job growing the company's top and bottom lines. Net interest income, for instance, expanded from $362.5 million in 2020 to $550.1 million in 2022. Non-interest income remained in a fairly narrow range, with a low point of $176.2 million and a high point of $193.2 million. Meanwhile, net income for the business shot up from $22.7 million to $199.8 million over that three-year window. While this is impressive, it is important to keep in mind that the company allocated $95.3 million in the form of charitable donations during the 2020 fiscal year. That is the only year in which it had a separate category for that kind of expense. So actual bottom line growth has not been quite as impressive.

When it comes to the current fiscal year, we have seen continued growth on the top line. Net interest income in the first half of the year came in at $272.4 million. That's up from the $265.3 million reported one year earlier. Non-interest income went from $88.3 million to negative $224.5 million. But this was largely the result of $333.2 million in the form of losses on sales of securities that were available for sale. Based on a review of the company's financial condition, this was largely associated with the firm's decision to offload certain assets in order to reduce debt. So investors should view this as a one-time thing. Meanwhile, net profits sank as well, going from $102.7 million to negative $145.4 million. But just like with the non-interest income, this pain can be chalked up to the sale of securities I mentioned already.

It is worth noting that, while net interest income has risen so far this year, the recently announced results for the second quarter painted a slightly different picture. Net interest income actually dipped from $136.7 million to $134.1 million. A surge in the interest that the company has to pay on deposits was responsible for the vast majority of this change. This number spiked from $3.1 million to $56.1 million. The company also suffered from an increase of nearly $14.2 million associated with higher interest paid on federal funds sold and on other short-term investments. Higher interest rates, combined with additional debt and actions taken to mitigate the fallout from the banking crisis can really be blamed for this.

{kind=link}

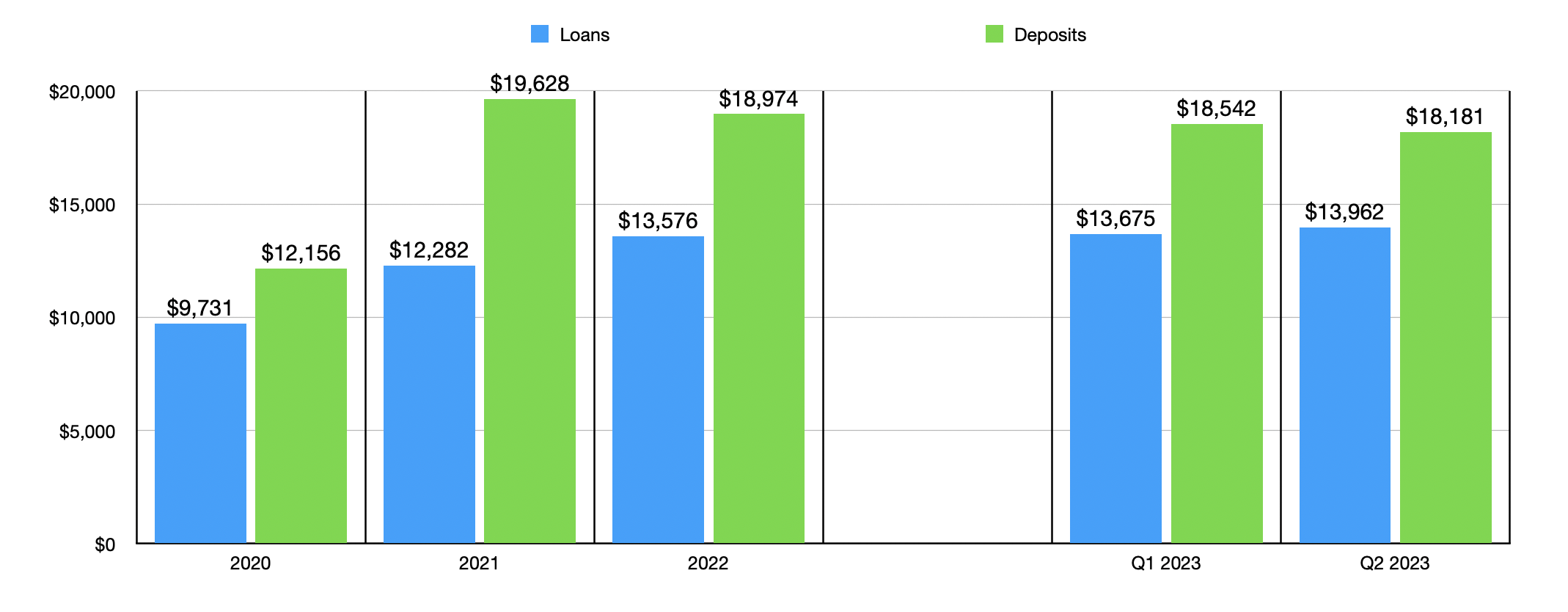

One thing I would like to mention is that the overall trend of increased revenue and profits for the company in recent years has only been made possible by a jump in deposits. Deposits went from $12.16 billion at the end of 2020 to $19.63 billion in 2021. However, they declined to $18.97 billion by the end of 2022 before falling further over the next two quarters, sequentially, eventually hitting $18.18 billion. I'm not surprised by the drop from 2021 to 2022. Other banks have also seen this and it is likely the result of depositors looking for more attractive yield in this high interest rate environment. But since the end of last year, it's very probable that a good portion of the pain was driven by concerns about the bank's stability.

{kind=link}

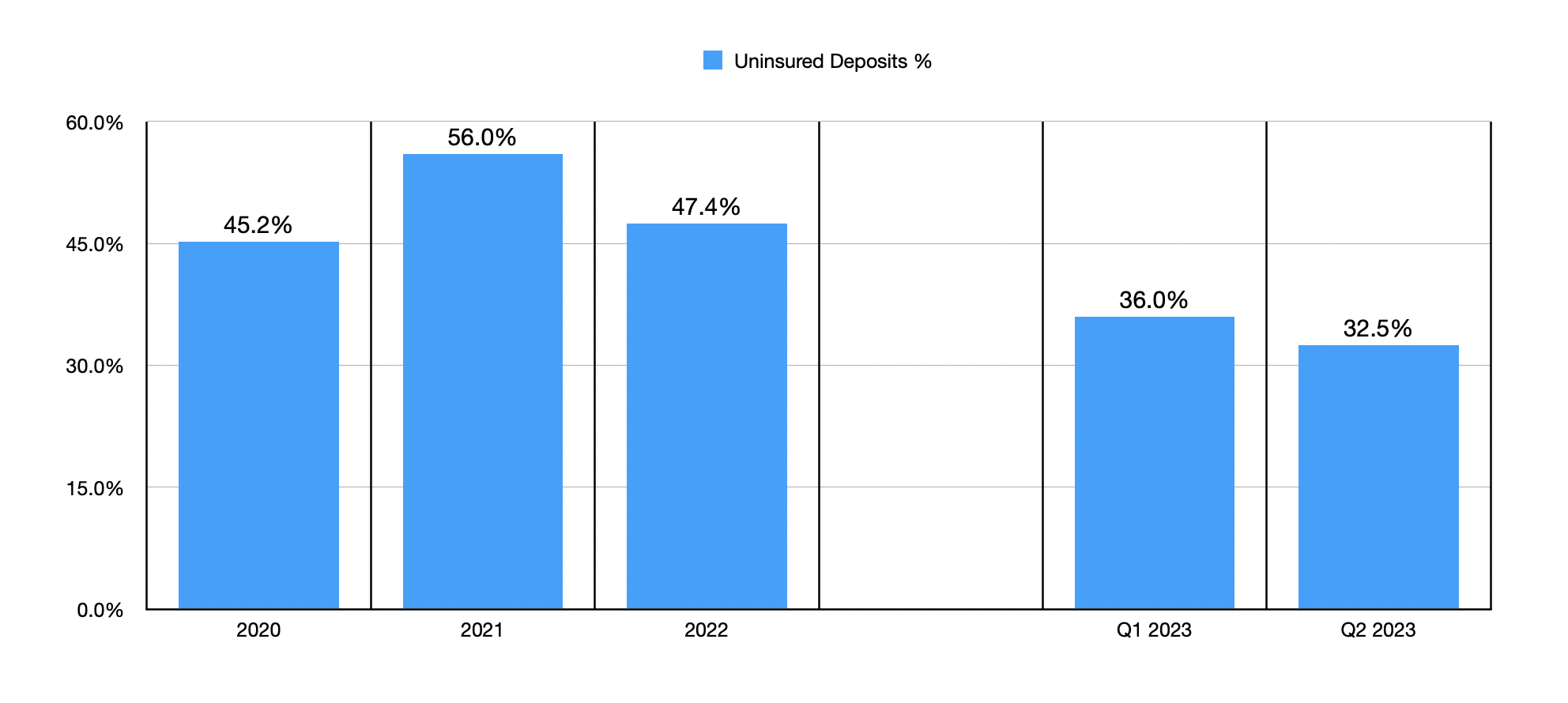

The one good news piece on this is that management has been active in trying to mitigate the bank's exposure. At the end of the first quarter, for instance, 36% of all deposits were classified as uninsured. This number dropped to 32.5% by the end of the second quarter. Put another way, uninsured deposits declined from $6.68 billion to $5.91 billion. This drop of $774 million accounts for more than 100% of the decline in deposits seen from the end of the first quarter when carnage in the space began to the end of the second quarter. Absent this, we probably would have seen deposits increase sequentially.

{kind=link}

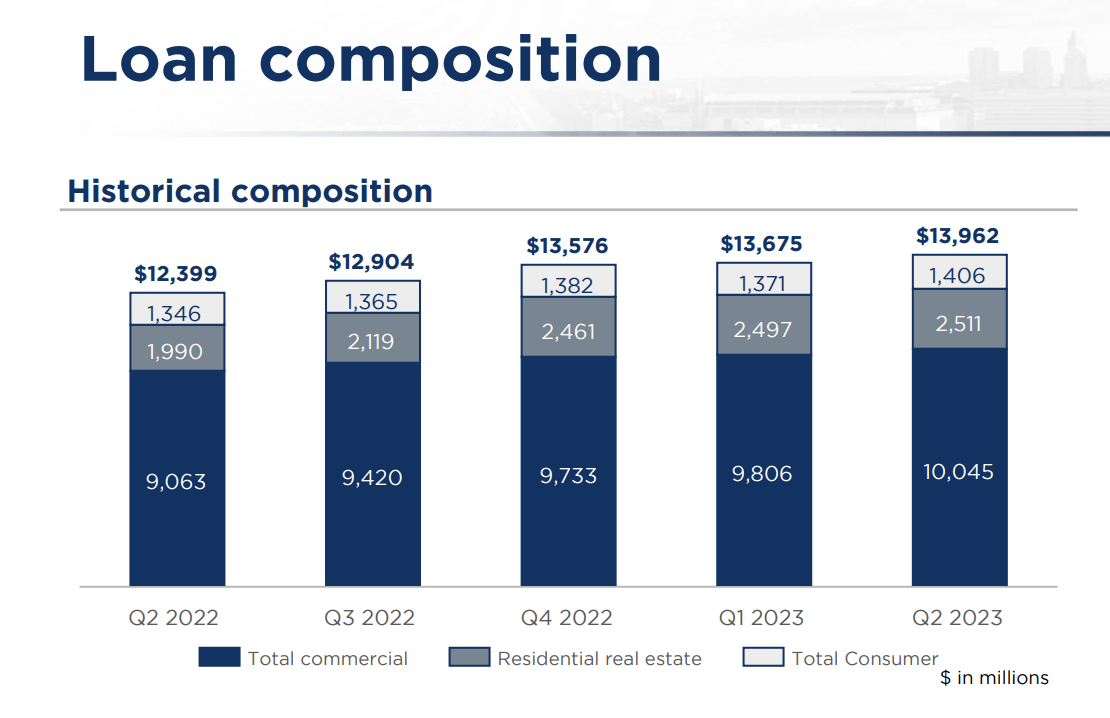

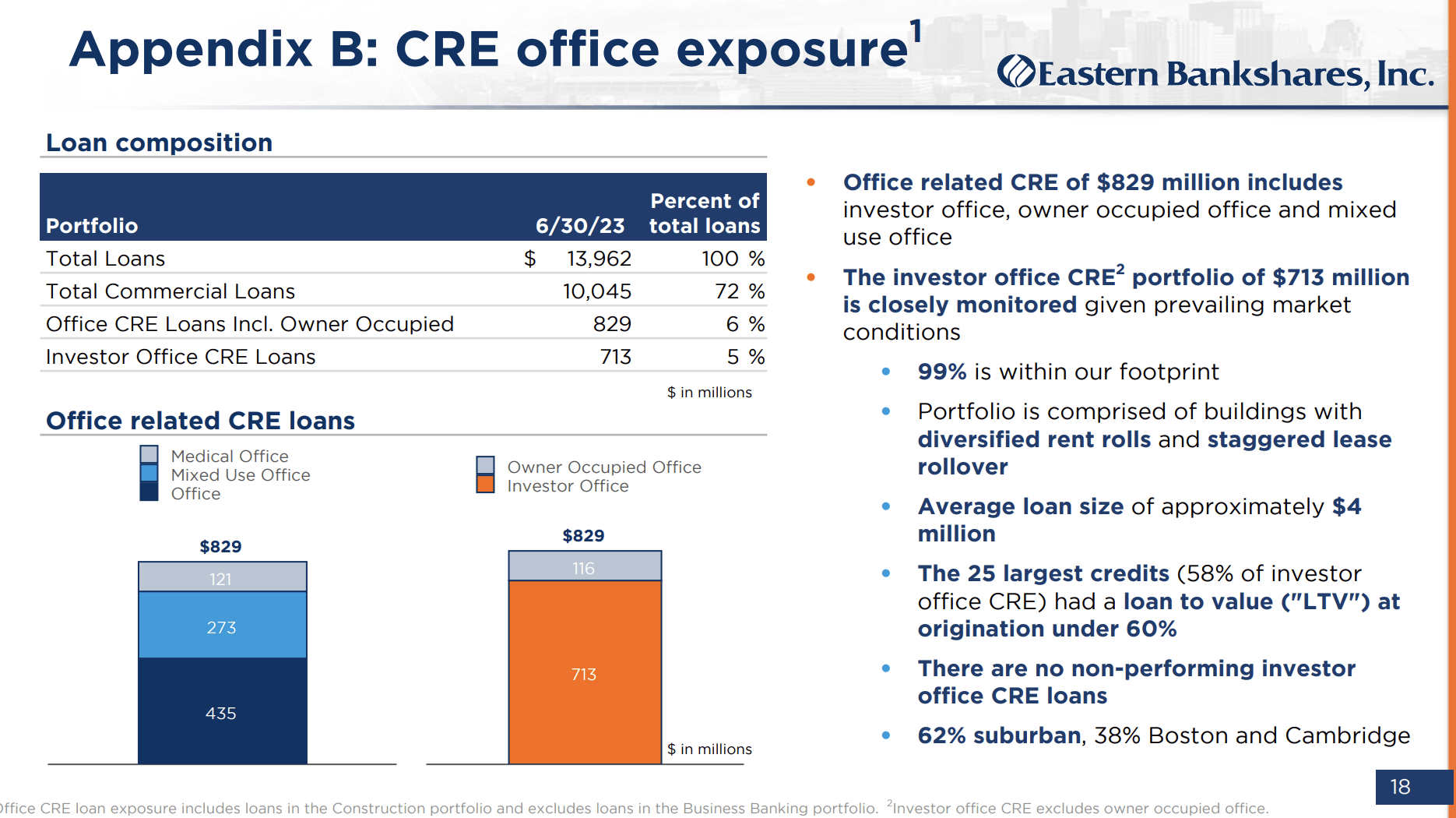

When it comes to the loan portfolio, the picture has also improved in recent years. Driven by both organic growth and acquisitions, the increase in deposits allowed the loans on the company's books to expand from $9.73 billion in 2020 to $13.58 billion in 2022. Loans continued to grow through the second quarter of the year, hitting $13.96 billion. I understand that many investors and market watchers are concerned about exposure to office properties because of high vacancy rates. And I can definitely imagine this fear being elevated when it comes to a company based in Boston where so much business activity takes place. This fear is probably not made any better by the fact that, as of the end of the most recent quarter, 71.9% of the company's overall loan portfolio is in the form of commercial loans. But this is something that investors should feel more comfortable with. I say this because, according to management, only $829 million, or roughly 6%, of the company's loans are focused on the office category. And of these, 32.9% involve mixed-use properties, while another 14.6% are centered around medical offices. Both these are categories that should be more stable than more traditional office assets.

{kind=link}

Although the uninsured deposit exposure is still a bit higher than I would like to see and the decline in deposits is not awful from quarter to quarter, these items alone are not necessarily deal Breakers for me. But when you add in a couple of other factors, I view the company as somewhat problematic. For starters, while the value of debt did decrease from the first quarter to the second quarter, dropping from $1.14 billion to only $351.2 million, the company saw the value of cash plummet $1.26 billion during this time.

{kind=link}

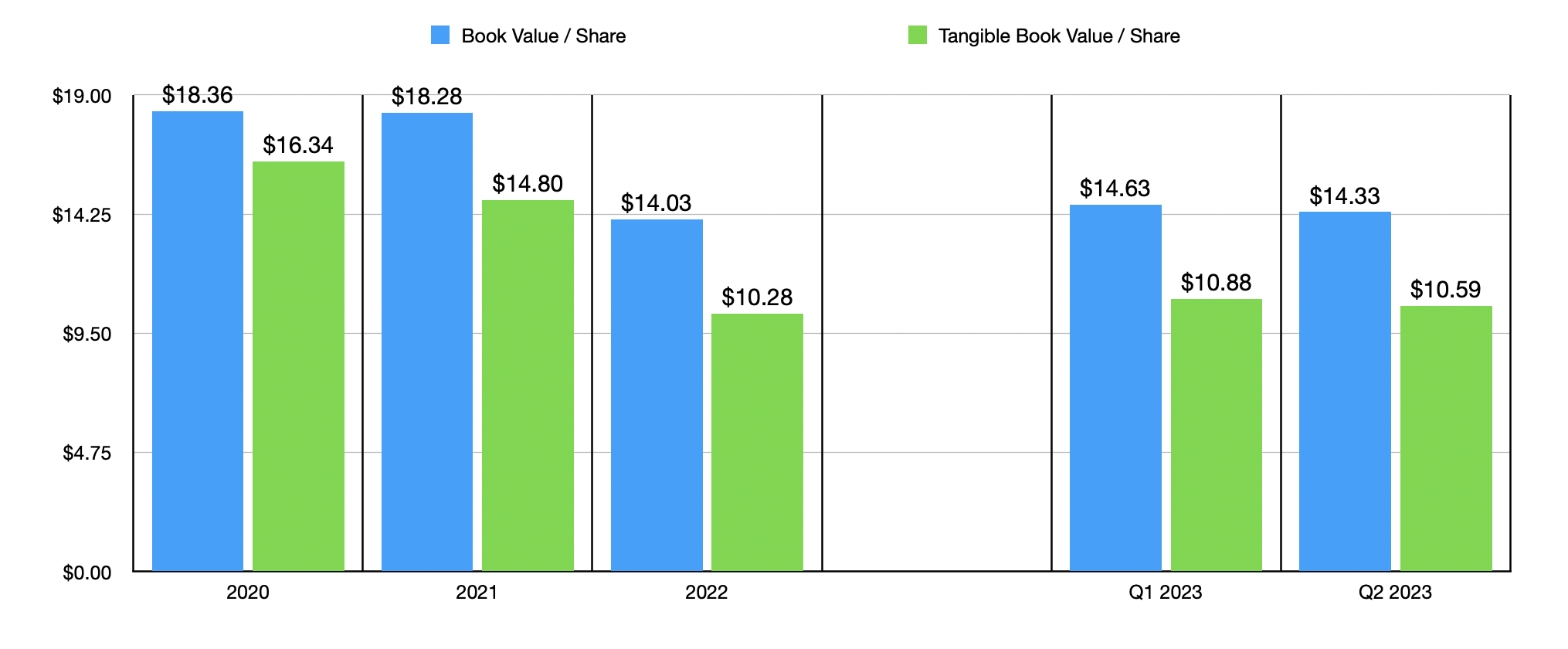

Even worse than this though is the fact that the company has continued to see its book value and tangible book value, both on a per share basis, decline. As you can see in the chart above, both of these have dropped over the past few years. That kind of deterioration in per share value is the exact opposite of what you want to see. And unfortunately, that trend has continued into the current fiscal year. On top of this, I would argue that shares of the business are not exactly cheap. With units of $14.12 apiece, they are trading at around book value per share. But they are still at a lofty premium to tangible book value per share, especially if we assume that it will continue to decline. Add on top of this the fact that, using data from 2022, the bank is trading at a price to earnings multiple of 13.7 at a time when many other banks are trading at levels of between 6 and 9, and I feel comfortable taking a pass on it.

Takeaway

From all that I can see right now, Eastern Bankshares is not at a substantial risk of experiencing some sort of downward spiral like we saw other banks experienced earlier this year. But this doesn't necessarily mean that it makes for an attractive investment either. Relative to other players in the space, the stock is quite pricey. Book value per share and tangible book value per share both continue to decline. Recent quarterly performance has been somewhat discouraging and deposits continue to drop. Add all of this together, and I feel as though a 'hold' rating is the best that I can assign the bank for now.

For further details see:

Eastern Bankshares: Better Opportunities Are Out There