EBC - Eastern Bankshares: Headwinds Starting To Ease

2023-11-16 11:38:01 ET

Summary

- Eastern Bankshares has lagged peers in a very tough year for regional and community bank stocks.

- Net interest margin compression is easing now while recent inflation trends also appear supportive.

- Although not a near-term driver, Eastern looks like a clear M&A target further down the line.

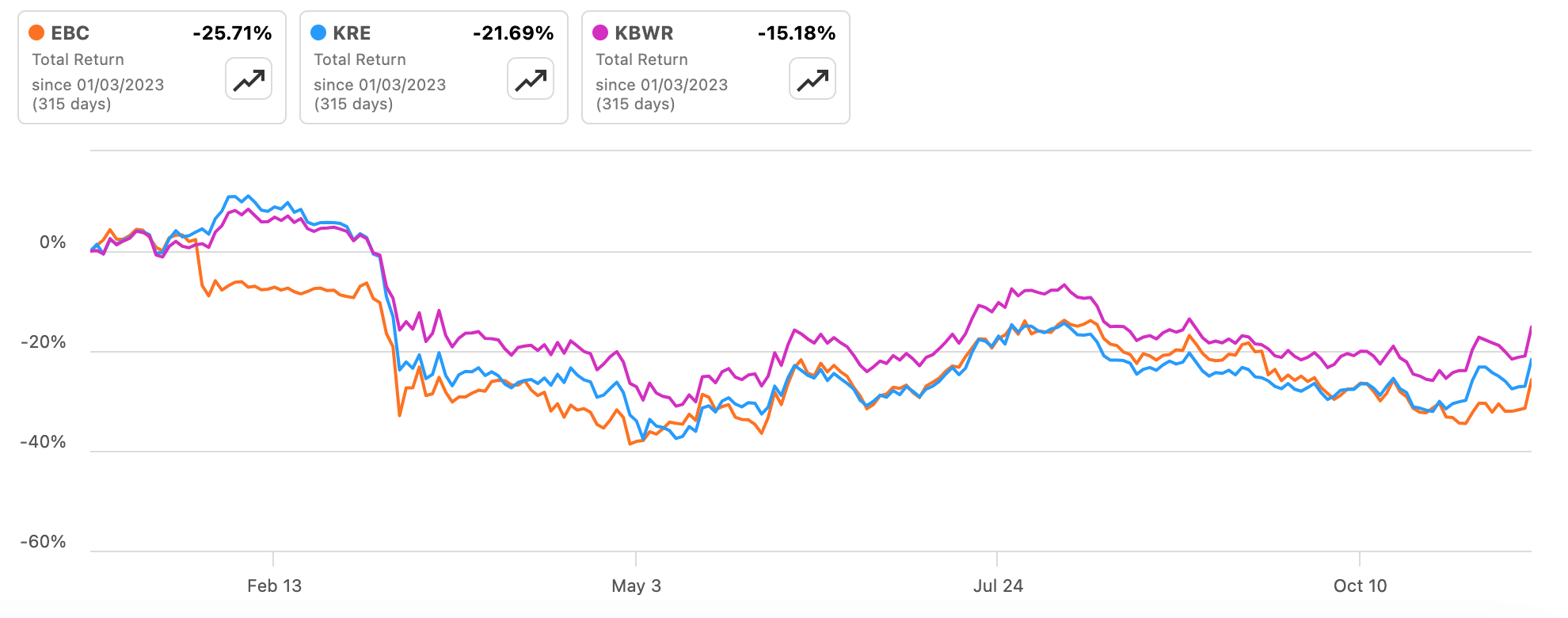

This has been a hard year for Greater Boston lender Eastern Bankshares ( EBC ). This is the holding company for Eastern Bank, one of the biggest lenders in the Greater Boston area with around $21 billion in assets. Like its peer group, Eastern has been put through the wringer recently on a combination of interest margin compression, concerns surrounding commercial real estate ("CRE") exposure and unrealized losses on its investment securities and swaps. Despite a nice bounce off the recent inflation report, shares of the bank have fallen by around 25% year-to-date with dividends, underperforming peers to varying degrees depending on which index you use.

{kind=link}

Source: Seeking Alpha

Regular readers will know I like smaller banks with solid core deposit franchises, like recently covered BancFirst ( BANF ) and First Hawaiian ( FHB ). Many of these names also come with strong track records on underwriting versus the larger regional or big money center banks. In what is a tough industry for earning decent returns, those avenues are two of not many ways to achieve this. While I think Eastern falls into this camp, there's no doubt it has struggled recently, with the bank buffeted by just about all the major headwinds facing the wider industry right now. I would like the stock cheaper than its current tangible book value multiple, but with some of its headwinds easing and the bank looking like a possible future M&A target these shares hold some longer-term appeal.

As mentioned in the prior paragraph, I like banks with sound core deposit franchises. Eastern looks like it falls into this bucket. It held around $10 billion in very cheap non-interest and interest-bearing accounts as of Q3, enough to fund almost half of its assets. They were costing the bank just 25bps annualized last quarter, with NIB balances alone totaling around $5.25 billion. Cumulative cycle-to-date deposit beta looks to have been around 25% on total balances as of Q3, which suggests to me that its deposits are indeed reasonably sticky.

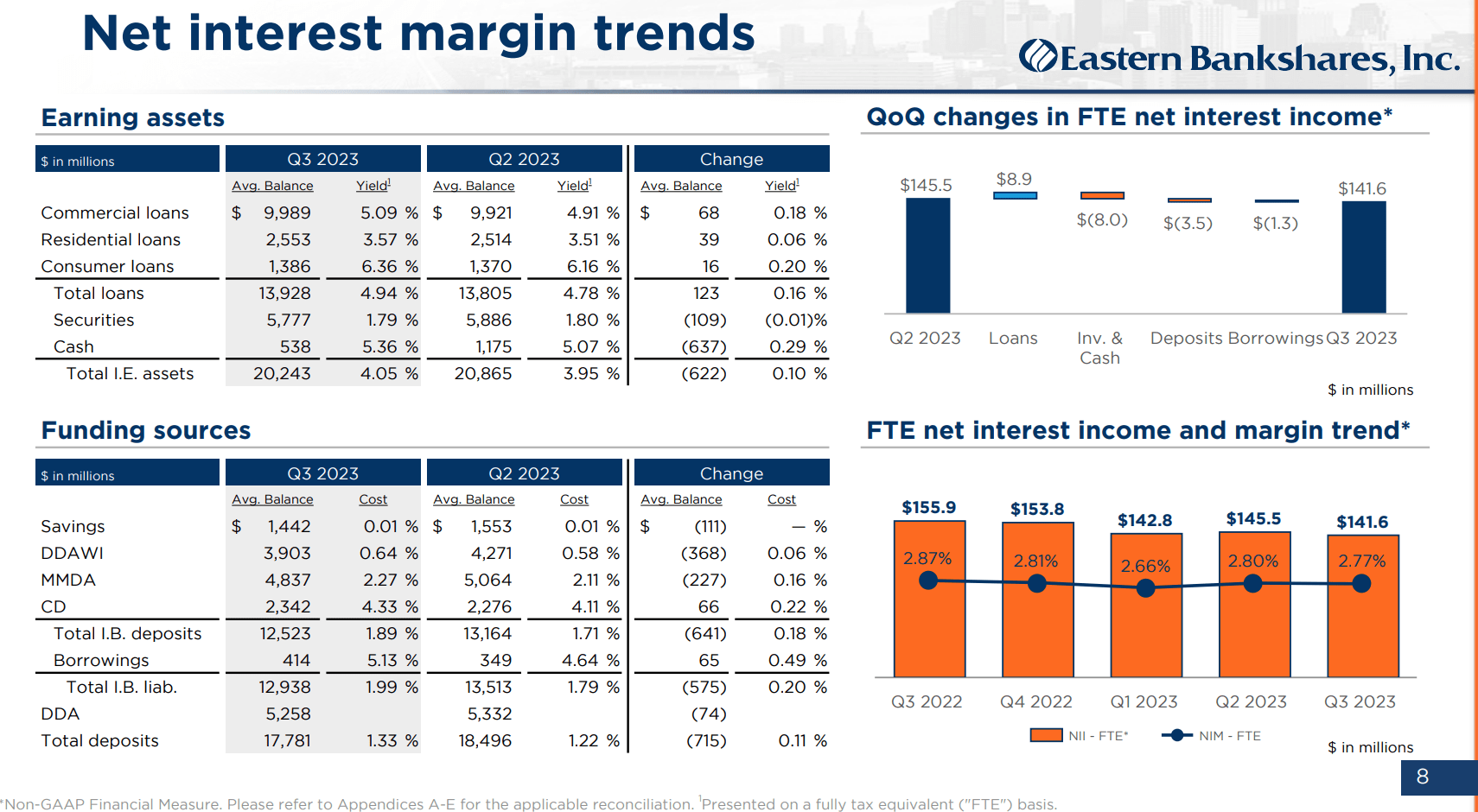

Like most other banks, Eastern has been grappling with NIM compression. Not helping matters was its decision to fix a significant portion of its variable rate loans back in 2022 at around 3% via swaps. This was understandable as many banks were eager to lock in higher interest rates after years of being stuck at ultra-low levels. While Eastern was far from alone in doing this, in hindsight this has obviously been an additional drag. The bank's net interest margin was 277bps in Q3, down around 10bps from the year-ago period but relatively stable on a sequential basis.

{kind=link}

Source: Eastern Bankshares Q3 2023 Results Presentation

The good news is that the pace of rate hikes has slowed to a pause, with the most recent inflation data lending further weight to the view that the Fed is now done. Indeed, it could even point to sooner-than-expected rate cuts. Eastern's liabilities reprice faster than its assets, so falling rates might actually lead to a rise in net interest income. It might also alleviate funding costs pressures for the industry in general, which is partly why regional bank stocks were among the market leaders following the report.

One other point I would note with respect to this is that Eastern recently sold its insurance brokering business. Now, this has been an industry-wide trend over the years and Eastern follows numerous other regional/community banks in doing so. I have mixed views about this. Insurance brokering is a nice source of non-interest income and is commission-based, with commissions tied to premiums. Said differently, insurance agencies don't take on underwriting risk, which makes this business line a nice source of stable cash flows. Why have banks been sellers then? The rationale is typically that their insurance brokering operations don't command the valuations they deserve from the market since they are overshadowed by their bread-and-butter banking businesses. While I am not sold on the merits of that point, it is moot now given the sale has occurred. The key point to take away is that Eastern's earnings will be even more dependent on net interest income going forward, which is something to bear in mind in light of what was outlined above.

There have been other issues weighing on the bank. For one, tangible book value per share ("TBVPS") has fallen significantly due to large losses in its AOCI line. This is linked to the unrealized losses on its available-for-sale securities and the cash flow hedges mentioned above. This would resolve on its own over time, all else equal, but the market's reaction to cooling inflation will help. Tangible common equity stands at around 8.50% of tangible assets (inclusive of unrealized HTM losses), which is around average and not a major source of concern for me.

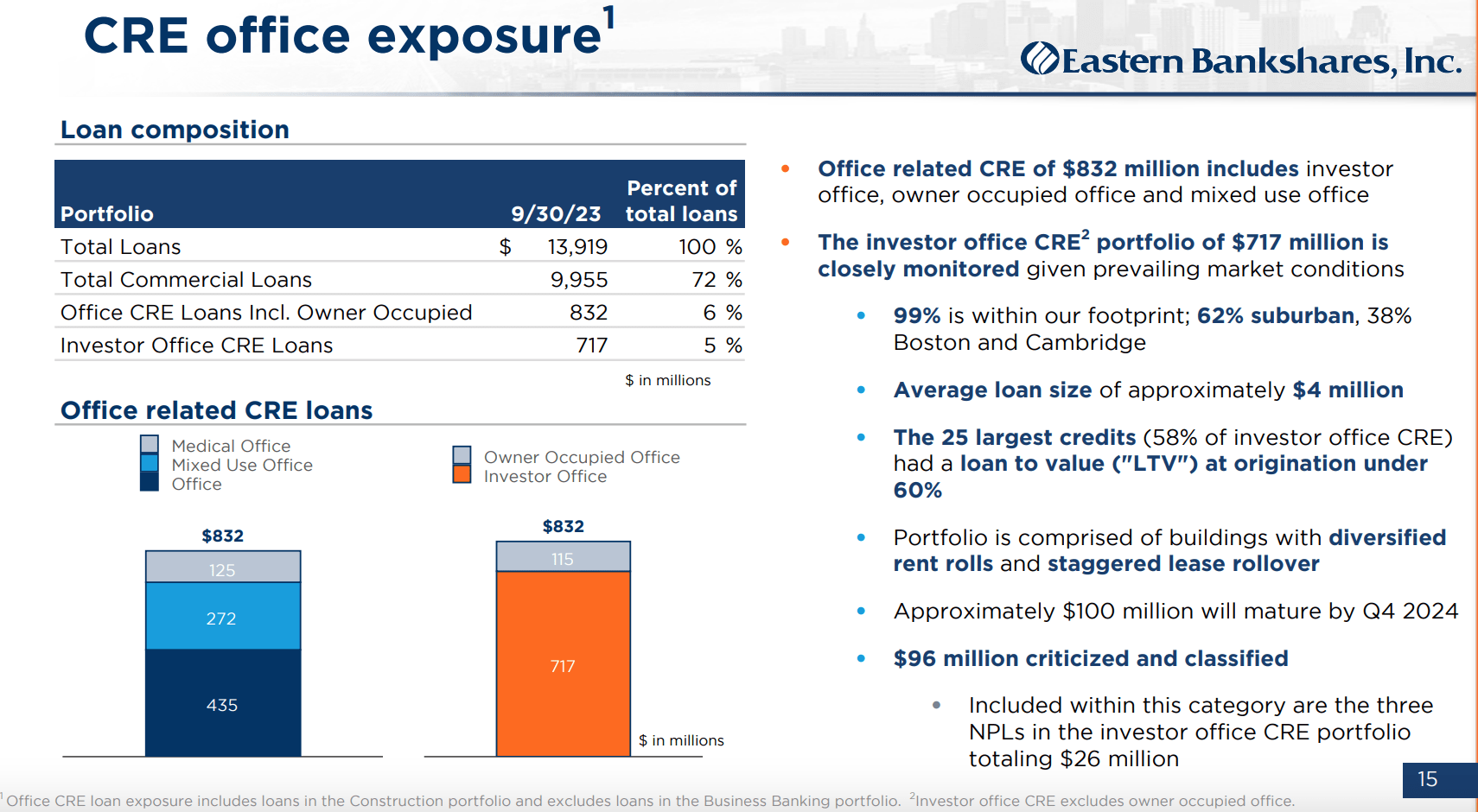

The other issue is credit quality, particularly in the commercial real estate ("CRE") space. CRE is a very large portion of Eastern's loan book, accounting for almost 40% of Q3 gross lending balances. Narrowing that down to non-owner occupied CRE still leaves us at 30% of gross loans, equivalent to around 2.5x TCE. One aspect of CRE lending that has the market spooked is the so-called "maturity wall", which could even hit previously stodgier areas of the CRE market like multifamily. On top of that, areas like office have been facing additional underlying cash flow strains due to external factors like work-from-home trends. Now, office obviously encompasses a very wide range of assets. What seems to be dragging the space down in particular is downtown properties in major cities that are currently reporting very weak occupancy levels. The nightmare scenario for owners would be a combination of low occupancy levels, weak/negative release spreads, sharply higher refinancing costs and falling property values.

{kind=link}

Source: Eastern Bankshares Q3 2023 Results Presentation

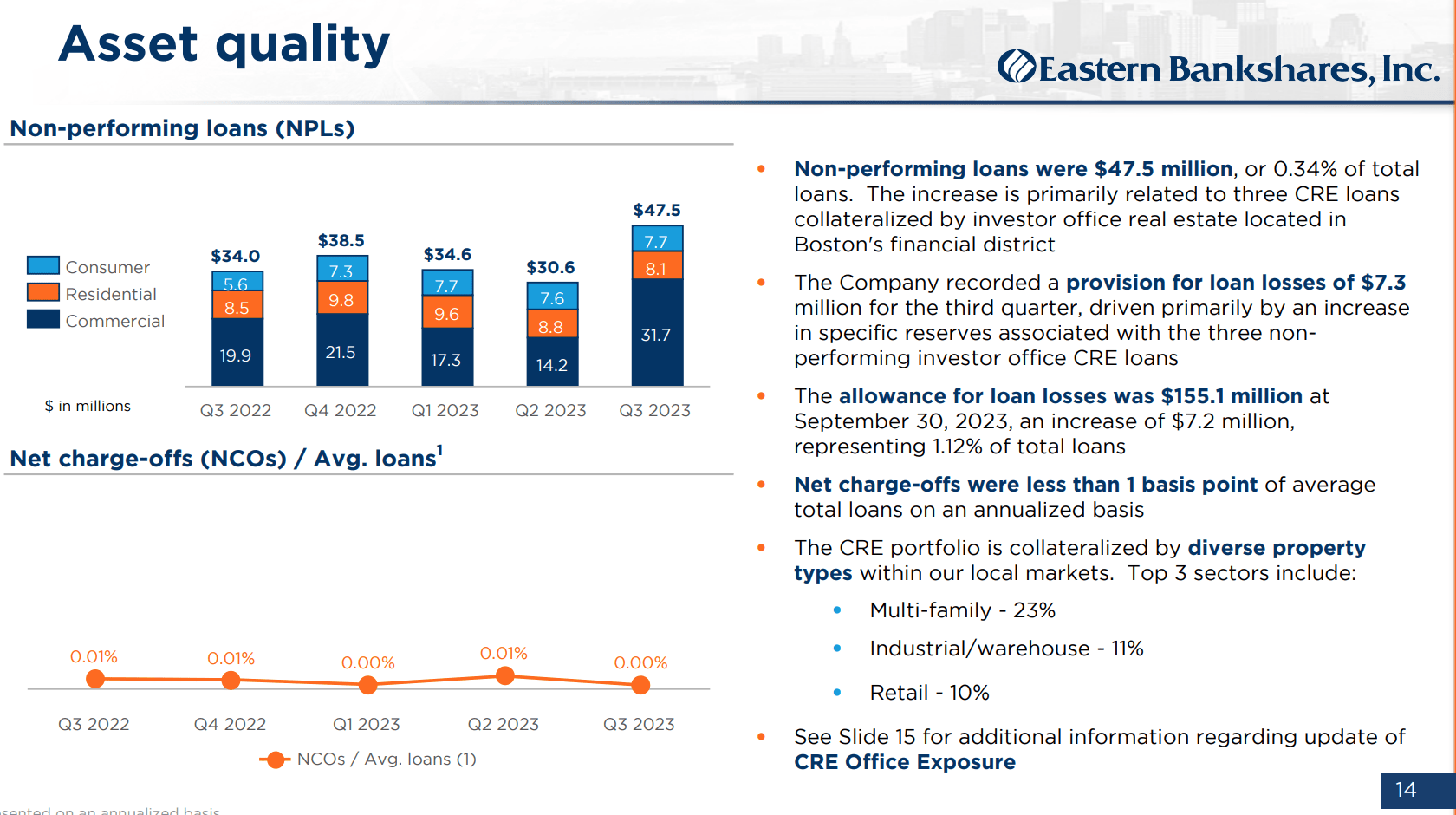

Eastern has around $720 million in investor office CRE, which is around 5% of total loans (~0.4x TCE). I would note that Q3 provisioning expenses of $7.3 million were largely driven by specific reserves against investor office loans in the Boston financial district. Non-performing loans remain very modest and charge-offs are still practically negligible; there is good reason to assume the bank is a prudent underwriter, but this is obviously something to monitor closely.

{kind=link}

Source: Eastern Bankshares Q3 2023 Results Presentation

With all that said, I do think Eastern stock has some longer-term appeal at its current $12.47 quote. This works out to a little over 1.2x TBVPS, leaving the stock around fair value given the bank earned an ~11% underlying ROTCE in Q3. Headwinds to net interest income should start to ease off at this point given the Fed looks like it's done hiking plus very modest loan growth. On a slightly longer-term horizon, Eastern's concentrated geographic footprint, deposit franchise and size marks it out as a pretty obvious M&A target. I admit that this is not a near-term play as the bank is involved in some M&A of its own right now as the acquirer , picking up Cambridge Bancorp ( CATC ) in an all-stock deal that will increase its assets by around 25%. Still, Eastern looks like a clear target for a larger regional bank further down the line, and while these shares could certainly go lower in the near term, I think investors with a slightly longer horizon can do well from here.

For further details see:

Eastern Bankshares: Headwinds Starting To Ease