EBC - Eastern Bankshares: Low Diversification Of Loan Portfolio But Steady NIM

2023-08-10 14:38:31 ET

Summary

- Eastern Bankshares has seen a major rally of over 40% after a 45% collapse earlier in the year.

- The net interest margin has improved but still lags behind similar banks.

- The bank has high exposure to commercial loans, which raises concerns about its performance in a recession.

The operating environment for banks is far from easy in 2023, but Eastern Bankshares ( EBC ) remains afloat. After collapsing 45% from January to May 2023, there has been a major rally of more than 40% in recent months.

The adversity may not have ended, but according to Q2 2023 , the situation remains stable.

Net interest margin and non-interest income

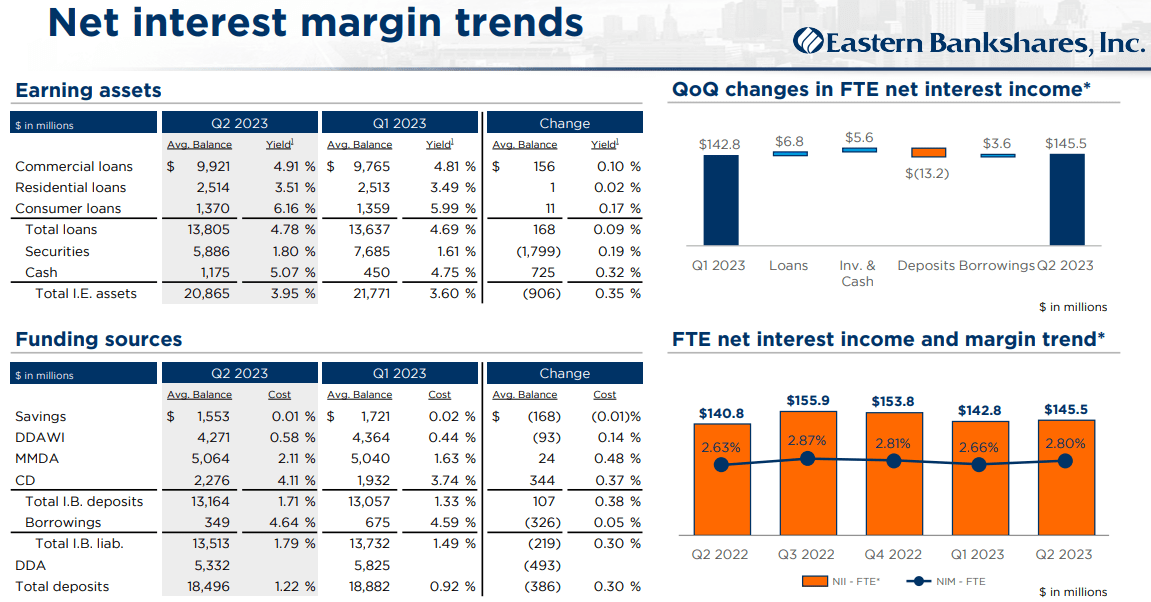

The first aspect of the earnings report I want to cover is the net interest margin, as Eastern Bankshares managed to improve it by 14 basis points over the previous quarter and 17 basis points over Q2 2022.

{kind=link}

Currently, the net interest margin is 2.80%, 37 basis points lower than the average of banks with similar market capitalization. Not an exciting result.

{kind=link}

However, I find its consistency over the past 12 months to be a positive aspect, as there are many banks whose net interest margin has been revised significantly downward over the past three quarters. In this case, a balance has been found between the yield on assets and the cost of liabilities, and it is likely to continue in the future since the guidance for NIM 2023 is between 270-280 basis points.

The yield on total interest-earning assets increased by 35 basis points from the previous quarter, reaching 3.95%. At the same time, the cost of total interest-bearing liabilities increased by 30 basis points to 1.79%.

{kind=link}

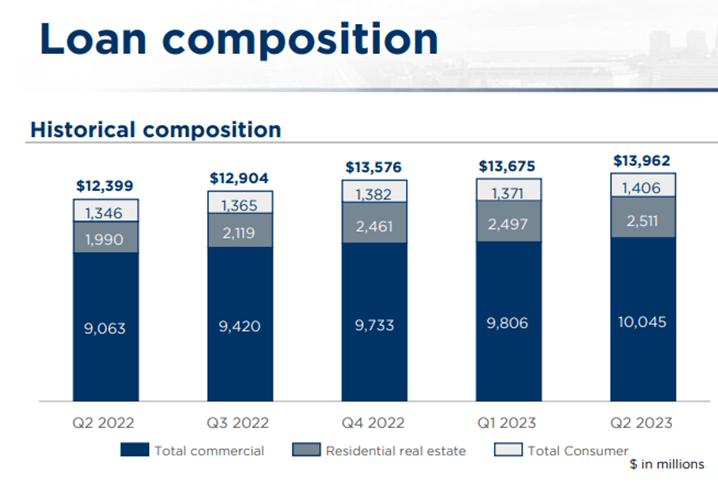

Fueling the improvement in the net interest margin was the loan portfolio, up $287 million from the previous quarter and yielding 9 basis points more. Here the biggest problem lies in the composition of this portfolio, since as much as 72 percent is represented by commercial loans. Such exposure creates many doubts about the performance of Eastern Bankshares in a recession and may partially explain why the current Price/Book Value is only 0.93x. But there is more.

CFO Jim Fitzgerald expects that, in the second half of 2023, the commercial segment will be the one with the most opportunity for growth, so in a few months the exposure could be even higher.

We have no non-performing loans in our investor office portfolio and our overall commercial real estate portfolio is performing very, very well. We expect commercial loan growth to slow in the second half of the year to the low single-digits and for mortgage and consumer loans to have a little no growth in the second half of the year.

For those who are pessimistic about the future performance of the U.S. economy, Eastern Bankshares is probably an unsuitable choice, as commercial loans are typically the most fragile in a recession. In any case, for now, there are no signs of weakness as NPLs remain very low.

Eastern Bankshares Q2 2023

Paradoxically, even though the Fed Funds Rate has skyrocketed, among the last five quarters, Q2 2023 is the best in terms of NPLs.

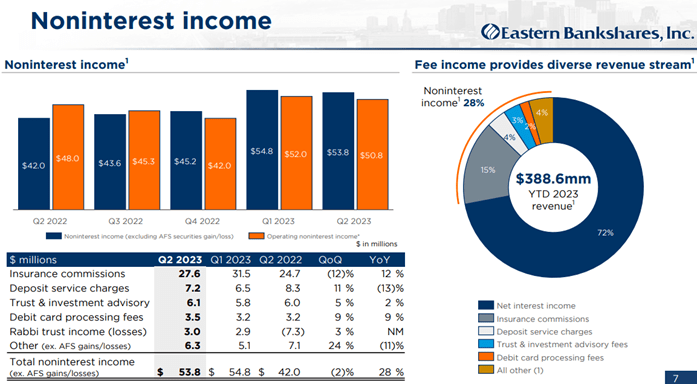

Finally, let's take a look at non-interest income.

{kind=link}

This segment is responsible for 28% of total revenues, and Q2 2023 saw a 28% increase over the same quarter last year. Much of this revenue comes from insurance commissions, which account for just over half of non-interest income.

In the first half of 2023 that segment generated operating revenues of $102.80 million, but the guidance for the full 2023 is between $175-$180 million: basically a weaker H2 than H1 is expected. The CFO attributed this deterioration mainly to the insurance line, which is typically more profitable at the beginning of the year and then fades until Q4. This is a sort of seasonal trend that has manifested itself before.

Deposits and liquidity

As we saw earlier, total interest-earning assets have a yield of only 3.95%, but this is not a concern since the funds raised by Eastern Bankshares are very cheap.

Eastern Bankshares Q2 2023

Certainly, the cost of deposits has increased quarter by quarter, but this is a minimal growth when compared to the Fed Funds Rate, currently 5.25-5.50%. This is in my opinion the greatest strength of this bank, as it is able to fund itself at lower rates than its competitors.

Moreover, from April to June, the cost of total interest-bearing liabilities seems to have settled at 1.80% or slightly less. In any case, it is still too early to speak of a trend reversal, as management believes that the migration from low-cost to higher-cost deposits is still an ongoing trend. The Fed may keep rates high for longer, and this could fuel deposit competition.

{kind=link}

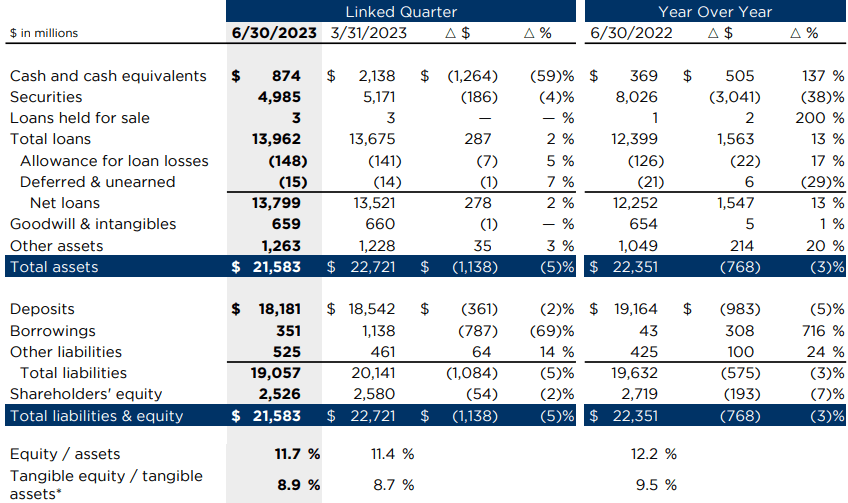

As for liquidity, it currently stands at $874 million, down $1.26 billion from last quarter. According to the CFO's words , the issue of liquidity assumes primary importance, especially after the bank failures at the beginning of the year. It is expected to decline slightly in the coming months but will remain high to provide some financial flexibility.

I would expect that to come down a little bit although, we are prioritizing balance sheet liquidity. I think coming through the bank failures that was obvious that it's important. So we expect it to come down a little bit, but we would still hold higher levels of cash than we did say a year ago.

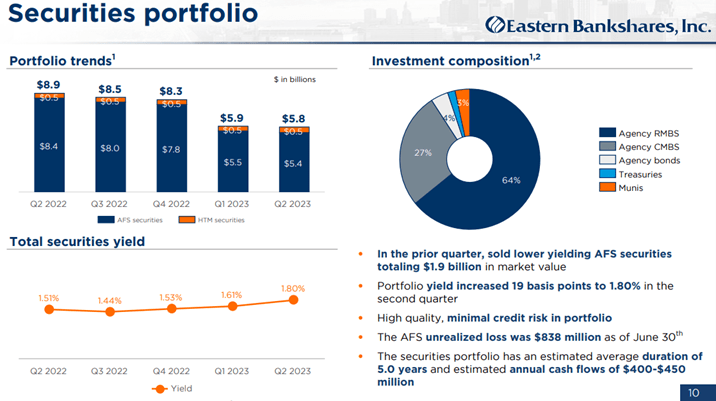

To put more weight on liquidity, at least for the next few quarters, the investment portfolio will be put on the back burner. This maneuver was already clear in the previous quarter when 25% of the securities were sold for a total value of $1.90 billion. The problem is that these securities had significant unrealized losses that upon sale became effective: we are talking about a non-operating after-tax loss of about $280 million. In short, in order to have more liquidity, Eastern Bankshares preferred to sacrifice hundreds of millions of dollars.

Unrealized losses booked in AOCI are still $838 million, about one-third of equity.

{kind=link}

After this sharp rebalancing maneuver, it is clear that there will be no new investments in securities and therefore this portfolio is bound to gradually shrink: As of today, it manages to generate cash flows between $400-$450 million per year and the average duration of securities is five years.

Conclusion

Overall, I rate this Q2 2023 quite positive, as the net interest margin remained constant and the cost of deposits did not increase too much. Concerns still remain about the huge exposure to commercial loans, as well as the choice to materialize the unrealized losses of AFS securities.

I personally would not buy this bank because I prefer banks with a more diversified loan portfolio, but at the current price I do not think it is overvalued as its Price/Book Value is only 0.93x. Certainly, for a bank with such a concentrated loan portfolio, an even lower value would be preferable, possibly 0.80x according to my degree of risk aversion. One thing is certain: It is clear that, in the past few months, the market has undervalued Eastern Bankshares too much, pushing it to $10 per share: now it is trading at $14 per share and is still far from the peak of $22 per share.

For further details see:

Eastern Bankshares: Low Diversification Of Loan Portfolio But Steady NIM