EMN - Eastman Chemical: Sales Volumes Need To Stabilize

2023-09-18 18:03:38 ET

Summary

- Eastman Chemical Company's Q2 earnings were not good, with declining sales volumes and increased debt.

- Weak demand and inventory de-stocking are expected to continue.

- The company's dividend growth rate may slow.

- The stock may have more downside as economic risks multiply.

I placed a hold rating on Eastman Chemical Company ( EMN ) in July, stating that the company was not out of the woods, indicating more uncertainty. The stock has dropped 3.6% since July, compared to the S&P 500 Index ( SP500 ) 0.08% drop. Since the article, the company has released its Q2 earnings , which were not good. The company’s revenue continued to decline, although the pace of decline should slow down in the coming quarters. The company’s debt has increased, and its dividend growth rate may slow in the coming years. I had added to my holdings in the company when it dropped below $80, yielding 4%. I have decided to pause after analyzing the Q2 earnings.

Although the company showed q/q improvement in gross and operating profits in its June 2023 quarter, the economy looks challenging. The stock may have more downside as economic risks multiply across the globe. New and existing investors may be better off waiting for the price to drop below $75. The stock’s 52-week low is $69.91. Given the uncertainties facing the company, it was the right call to slap a hold rating on this stock in July and continue that rating now.

Sales volumes continue declining

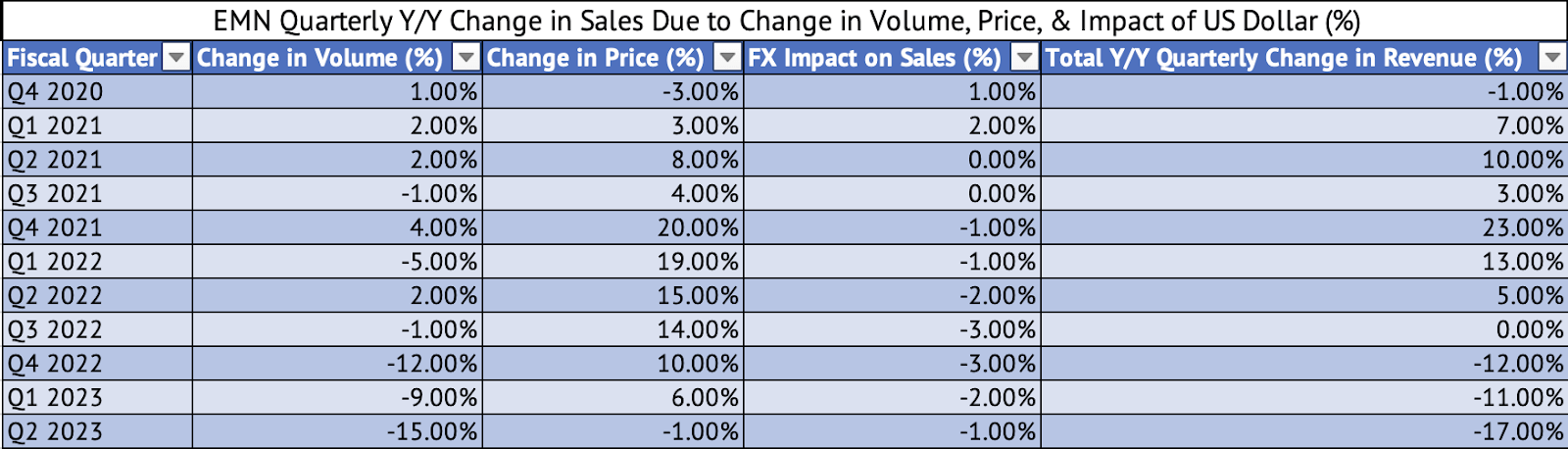

Eastman Chemical continues to see weak demand, which may last the rest of the year. Inventory de-stocking continued across its customer base in Q2 2023 . Its sales have declined at a double-digit pace over the last three quarters, and its pricing power has faded. Overall sales volumes declined by 15% y/y in Q2 2023. When accounting for lower prices and the impact of a strong dollar, revenue dropped by 17% (Exhibit 1) . Gross profits dropped by nearly 15% and operating profits by 27% y/y in Q2, not a good sign. The silver lining is that the gross profits improved sequentially Q/Q from $544 million in March 2023 to $584 million in June 2023. The company’s operating income improved from $294 million to $342 million during the quarters.

Exhibit 1:

Eastman Chemical Y/Y Sales Volume Growth (Eastman Chemical Investor Presentation)

{kind=link}

Resilient operating cash flows

The company’s operating cash flows have been resilient despite declining sales. It generated $1.12 billion in operating cash flows over the past four quarters and spent $777 million on capital expenditures during the same period. The company paid $373 million in dividend payments over the past four quarters. Cap Ex and dividend payments consumed the company’s operating cash flows over the past four quarters. The company’s trailing twelve-month EBITDA was $1.58 billion. That puts the debt/EBITDA ratio at 3.4x, a high number, especially if the global economy enters a recession.

Given the demands on the company’s operating cash flows, it is no wonder that the company’s total debt increased over the past two quarters. The company’s long-term debt went from $4.02 billion in December 2022 to $4.6 billion as of June 2023. The total debt stands at $5.5 billion

Recession worries linger

The company noted that de-stocking would slow in the coming quarters. Consumers have held up well in the U.S. and Asia in the face of high inflation and interest rates. But, the U.S. may be entering a prolonged slow growth era in the long term and a recession in the short term. With rising oil prices, there are renewed fears of inflation running higher than the Fed’s 2% target for much longer. The construction sector is already in a recession, and the strikes at the Big 3 automakers in Detroit add to the economic uncertainty. Many borrowers have stretched their budget with $ 1,000 monthly payments on their car loans. At those levels of monthly payments, many Americans will be left with limited or no discretionary spending power, further impeding economic growth. Also, the Federal Government may endure a shutdown due to the ongoing budget battle in the U.S. Congress. Let’s not forget that 43 million Americans will face renewed financial pressure due to the resumption of student debt repayments.

It has a good dividend yield at current prices but looks fully valued

The stock yields an impressive 4% due to the recent performance of the stock. The dividend payout of 47% is a tad high, given the company's state. The company has grown its dividend at a 7% CAGR over the past five years. However, the company may struggle to increase its dividend over the next couple of years due to the pressure on its free cash flow and debt levels. The company continues to spend money on share buybacks. Since its operating cash flows are used in capital expenditure and dividend payments, it borrows money to fund its buybacks.

In 2021 and 2022, the company spent $1 billion annually buying back shares. Over twelve months, that company has spent $300 million on buybacks. The company carried $410 million in cash and short-term investments at the end of Q2 2023, a drop from $494 million at the end of 2022. Companies must have a strong balance sheet in the face of economic uncertainty. The addition to the company’s debt load and its reduction in cash should be a concern for investors, albeit not a big one at this time, but if sales deteriorate further, it could spell more trouble.

The stock looks fully valued based on a forward EV/EBITDA multiple basis, trading at 8.7x, compared to its five-year average of 8.5x. The sector median EV/EBITDA multiple is 7.9x.

Eastman Chemical’s dividend may have to grow at a low-mid-single-digit pace over the next couple of years. Pessimistically, it may be stuck at current levels for a while. But a current 4% yield is suitable for long-term investors if it grows upwards of 5% when the economy recovers. The company may slow its share buybacks drastically in the coming quarters as it searches for more free cash flow. Every analyst covering the stock has lowered their EPS estimates for Q3 over the past ninety days.

Although I own Eastman Chemical, it may have been prudent to wait, given the economic headwinds and the increasing prospect of the U.S. economy slowing down further. I have paused my purchases and await signs of stabilizing sales volumes, revenue, and profits. I will watch the balance sheet to ensure the company does not add more debt in the coming quarters. Due to these reasons, I continue to rate Eastman Chemical a hold.

For further details see:

Eastman Chemical: Sales Volumes Need To Stabilize