KODK - Eastman Kodak: Q1 2023 Was Excellent But Risk Remains High

2023-07-12 09:00:00 ET

Summary

- Eastman Kodak had a recent 50%+ outperformance since my last review.

- Despite this outperformance, KODK's overall performance remains mostly flat.

- The article aims to explore whether there's a valid reason for this outperformance related to valuation or forecastable factors.

Dear readers/followers,

In this article, I intend to revisit Eastman Kodak ( KODK ) and give you my view on the recent 50%+ outperformance that the company has delivered since I reviewed it last. We saw a very quick trajectory upward in a matter of days and weeks, which has resulted in the following RoR since my last article with a "Hold" rating.

Seeking Alpha KODK (Seeking Alpha)

I remain one of the very few authors, and for the past year or so almost the only contributor that follows Kodak to any degree. Despite this recent bout of outperformance, the company is still mostly flat since my first article. And the more important thing here, as I see it, is to discover whether there is any sort of good reason for this recent bout of outperformance that could be related to valuation or something we can forecast.

So let's look at that, and see if the company still has ways to go.

Kodak - A risky play, no matter how you view it

Any company can become interesting at the right price - what matters is what you pay for what you're getting. However, Kodak definitely becomes tricky at the levels of valuation that we see here.

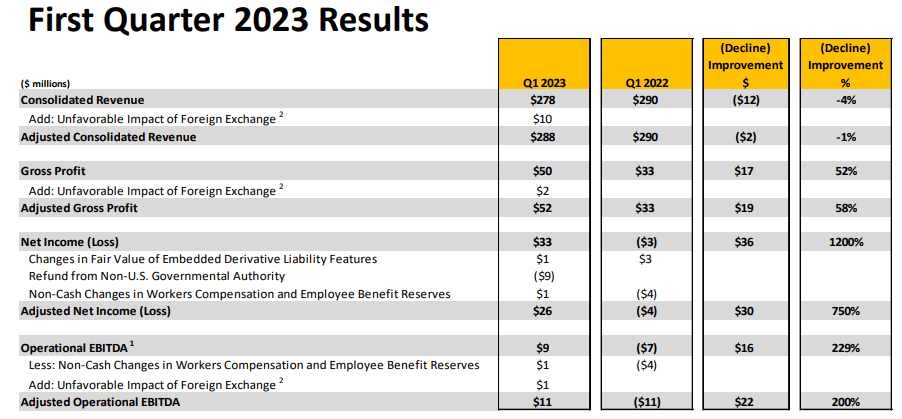

We do have company results - we have Q1 2023 that was reported in May of 2023. The company, during this, tried to continue to build momentum, increasing its overall revenues and improving its margins on gross, operating, and net margin levels in what in the company's own words is a "very challenging business environment".

However, it's fair to say that the company has made some progress over the past 4 years. This does not equate to KODK being a good investment in the timeframe, but it's worth acknowledging that the company's margins and specifics are far better today than it was a few years back.

Key pushes from the company come from investing in advanced materials and chemicals. KODK is moving towards EVs, specifically EV battery coating substrates and energy storage as well as light-blocking fabric. The company expects to see revenue from these growth businesses in this or next year. The company also invested in infrastructure upgrades, for increased Salesforce and SAP implementation, increasing efficiency company-wide.

At the same time, the company's core remaining business - meaning digital print and the like - is still going well. The launch of the recent PROSPER 520 series and the 7000 Turbo Press continue to show sales, as does the company's KODACHROME inks, which is the gold standard for color in the segment. A liken that comes to mind is an artist I'm aware of who didn't switch to digital medium when everything went digital in about 2006-2007 - instead sticking to his Watercolor and traditional renderings. Now, because he was quite literally one of the few left who did, and also could do efficiently what he did traditionally when certain clients started to once again see value in such renderings, he found himself in an almost-monopoly sort of situation until his competition had caught back up.

{kind=link}

My point is, being the last company or player in a market can be a very appealing thing if you know what you're doing. While a lot of criticism can be levied at KODK for how things have been going the past 10 years, I do believe the company has extensive expertise in key areas - namely the printing business, and their dominance here in certain areas is nothing to underestimate. The fact that other fundamental characteristics make this company to my mind, uninvestable regardless of this, is just an addition or a problem related to this.

But with quarterly revenues now above $275M despite the overall impacts and issues, the company is showing remarkable resilience in a difficult period - especially considering at constant FX, the company is down around 1% only. Gross profit meanwhile, is increasing, and not by an insignificant amount with a 52% increase.

KODK also managed to generate cash as before - though this fell significantly compared to the YoY period.

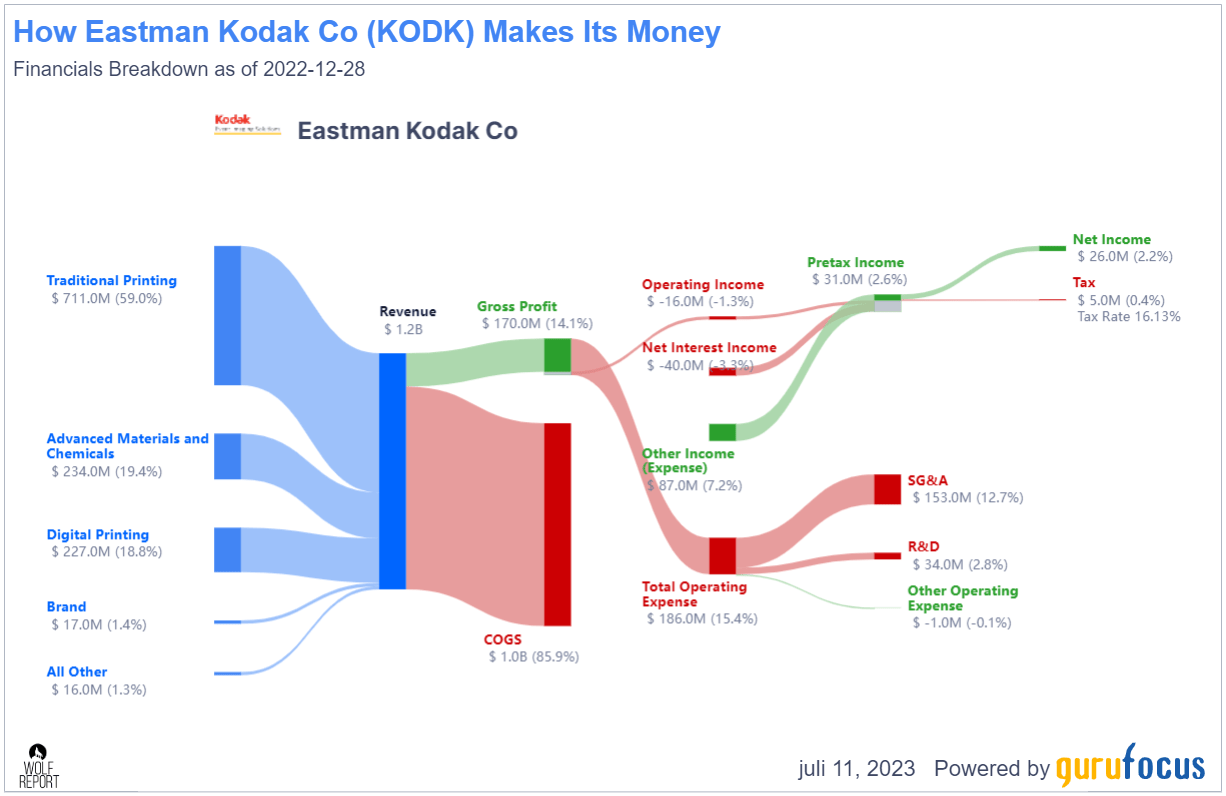

The key with KODK though isn't the quarterly results as they come in - it's the larger picture. This includes the launch of new innovative products in accordance with KODK's long-term strategic plans. The company has delivered some of these targets, with stabilization of the balance sheet now done, and continued operating efficiencies being realized. The company is also starting to really bring its capital to bear on investments, set to improve and really transform its earnings profile, which currently looks something like this in terms of revenue going to net profit.

{kind=link}

To say that the company has its work cut out for it would be an understatement. The COGS here are absolutely massive, and until KODK gets that under control and starts to really bring efficiencies to bear, I'll be hesitant to go into this investment regardless of the appeal that could be theorized.

However, the picture I want to share with you in this article is that things are clearly improving.

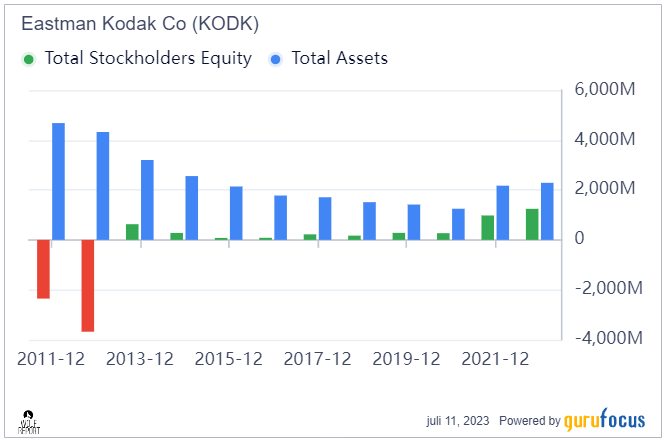

I'm talking about the fact that debt seems to have peaked or at least come to a manageable level. Revenue has been stable going on several years now, and the company is actually managing net profit and EBITDA. The company's previously bottoming ROIC net of WACC is now recovering - albeit slowly, and the reorganization and reduction in debt has done, historically, a very impressive thing to the SE portion of the company's assets, which are not only recovering but can be said to be "healthy" here.

{kind=link}

The company does manage a non-trivial set of sales across the world, with a very nice split geographically of 40/35/19 for US/EU-ME/APAC. Its sales mix is still over 50% traditional printing - but we're likely to see that mix change going forward, and when it does, that's when we're likely to see non-trivial amounts of margin improvements for the company.

The argument can even be made that I waited too long to get into KODK. As long as the company doesn't see any notable impacts or downturns in its near-term earnings, it's conceivable that things continue to climb from here or at the very least remain stable. However, as a value investor that's not something I'm prepared to hang my hat upon.

Nothing changes the fact that KODK is junk-rated, with a long, long way to go at CCC+. It has no yield and hasn't had that for a very long time. We don't have analysts that are willing to really estimate where things are going for Kodak - and I understand why, given the size and volatility of the business. The company is worth less than half a billion in market cap alone.

However, when summarizing Q1 2023, I do want to give you the picture that KODK had a good quarter during a very troubled macro. I also want to clearly state that I see improvement in the company's investments turning into improvements in key areas in its finances and profitability. A company is much like an organism. Healthiness or unhealthiness can be spotted in a myriad of different ways, usually well before the broader market becomes aware of it compared to analysts or value investors. What I am saying here is that the underlying signs are showing to the health of KODK improving - slowly - and I believe this to be the reason for the recent move-up. As long as the company's financial and profitability-related health keeps improving, I see no reason for this not to continue.

But that does not mean the risk isn't outsized compared to other companies - so let's look at the valuation for Kodak.

Kodak - The risk is high regardless of quarterly successes

So, if you invested in KODK and made that 50% RoR, that was a good gamble - and I do mean gamble here, because any company like this is mostly a gamble to me.

The encouraging sign is that the company's appeal that I wrote about tin my last article has gone from being momentary, to starting to show improvements over a period of over 8 months at this point.

Remember, KODK can't really be compared to other companies as such, due to size, risk and what they do, giving them peer multiples would be unfair not only to KODK, but to those peers it's being compared to.

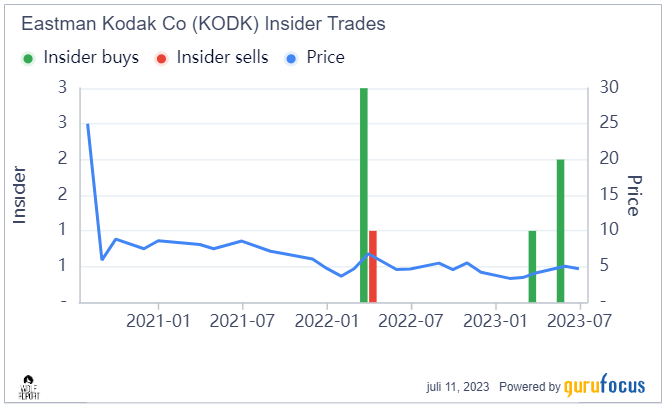

Also, remember that we actually have some activity both on the insider and on company "BUY" fronts. That activity continues in June of this year. Not only have we seen some insider buying activity both in 2022 and 2023. However, there was a significant selling spike on the institutional investors 1-2 months ago, which I interpret as some of those harvesting double-digit profits - not a bad strategy, all things considered. Still, here is the insider activity data for the past few months included.

{kind=link}

All in all, the signs are more encouraging than discouraging - but we also have KODK at a 50% higher level than in my last article. Based on Graham number valuation and Tangible Book Value, we can see valuations up to $12/share making sense for this company. I would not go even close to this. Based on conservative EBITDA estimates on the basis of historical results, I wouldn't go higher than $3.5-$4/share, and even at that point, KODK remains a company with CCC+ and no real heavy-conviction forecasts. The numbers I give you here are extremely speculative, because the company is still in the middle of a turnaround. It's a gamble to invest in the company at this point.

It's much less of a gamble than say, investing in Wheels Up (UP), a company that actually warranted a very rare "SELL" rating from me. I don't often do "SELL" ratings if you follow my work. KODK is safer than UP - because it has earnings, it earns GAAP and net profit, and that isn't going away. It's doing good business in good segments - and I can see the company, conceivably, turning around at some point.

However, at $6/share or above, I am still unwilling to put my money on the table or turn my capital over to the company. There are better alternatives for me, better companies, to do so with.

Because of that, here is my updated KODK thesis.

Thesis

My thesis for Kodak is the following:

- Kodak is an impressive business - if we looked at it in 1995. Today, it's a company with a mix of remaining legacy assets and segment ideas that it aims to expand. It's shown some decent progress on this expansion - but I would wait until we see even clearer signals of this.

- The signals are starting to appear, which means I'm taking closer looks at KODK and expecting continued improvements that hopefully take the company from a CCC+ to any sort of B-rating.

- I believe the company can be bought once any sort of turnaround and clarity is present here - and once we're looking at some sort of BB-rating.

- Until then, the company is a "HOLD" if you believe in it and own it, otherwise, I'd avoid or "SELL" Kodak.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( Italicized )

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Yes - to be clear - the company fulfills none of my current investment criteria.

For further details see:

Eastman Kodak: Q1 2023 Was Excellent, But Risk Remains High