KODK - Eastman Kodak: Still A 'Zero'

Summary

- I was surprised when a reader contacted me with regards to Eastman Kodak and my article on the business, given what I wrote - however, I'm happy to look again.

- Eastman Kodak is a storied and unfortunate company in a very difficult position - and one that I wouldn't envy them to be in. The theoretical and potential value is there.

- But there is a lot of uncertainty. After a 38%+ drop, the question is - is there value here?

- No - there isn't. Learn why you should stay away from this company.

Dear Readers/Followers,

A reader asked me to take a second look at Kodak ( KODK ). Why? Well, the company dropped 38%+ since I wrote my first piece. This can, of course, indicate some sort of value being present here because that's a big drop.

Eastman Kodak Article (KODK IR)

But let's see if there's any sort of improvement or any argument to be made as to why Kodak would suddenly represent an interesting or appealing buy in this market, and for whom.

Revisiting Kodak

So, remember - Kodak has a very strong legacy and a history that few other companies can compare with. It is the remnants of a 110+-year-old company that once held dominion over an area that was thought to never disappear - as these things usually are. I'm sure manufacturers of horse carriages and saddles thought the same when cars came.

Me, I'm old enough to remember the shift here - not with horses, but cameras. I had Polaroids, and when I was 10-14, I still used an analog camera. My first digital camera was a grainy horror show that had to be used with a cable the size of a computer power cable today, and it was several years before it became anything close to usable, as I see it.

Still, I'm old enough to recall when things went south, and when Kodak failed to adapt to the changing market. While we cannot "blame" Kodak for all of its failures, the company certainly could have adapted much better than it actually did. It tried to stay relevant through patents, creating digital cameras, developing tech, and digital printing in an attempt to generate revenues.

After Chapter 11 back in 2012 and the subsequent carve-ups in 2013 and the selling off of over half a billion worth of patents to businesses like Apple ( AAPL ), Google ( GOOG ) (GOOGL), Facebook ( META ), Microsoft ( MSFT ), and others, what remains is the corporate equivalent of a nearly-picked clean carcass.

Now, this is not necessarily a bad thing. If you've ever been to a butcher's shop, you know that sometimes the remnants before everything else is thrown away/shipped off can be some pretty nice pieces. In the case of Kodak, the proverbial remnants are the segments of Traditional Printing, Digital Printing, Advanced Materials, and Chemicals/Brands.

Things like printing plates, and digital services for end users in legacy printing formats. The one thing these segments seem to have if not in common, at least related is that they're mostly influenced by the current volatile state of the market in terms of raw materials, input cost inflation, and global supply chain challenges. They're not the easiest to work with.

Kodak also does advanced materials/chemicals, including still photographic film (industrial) in order to print circuit boards, specialty chemicals for the pharma industry, solvent recovery, and motion picture film. Now, this is a more interesting segment , especially with its PROSPER business lines and components.

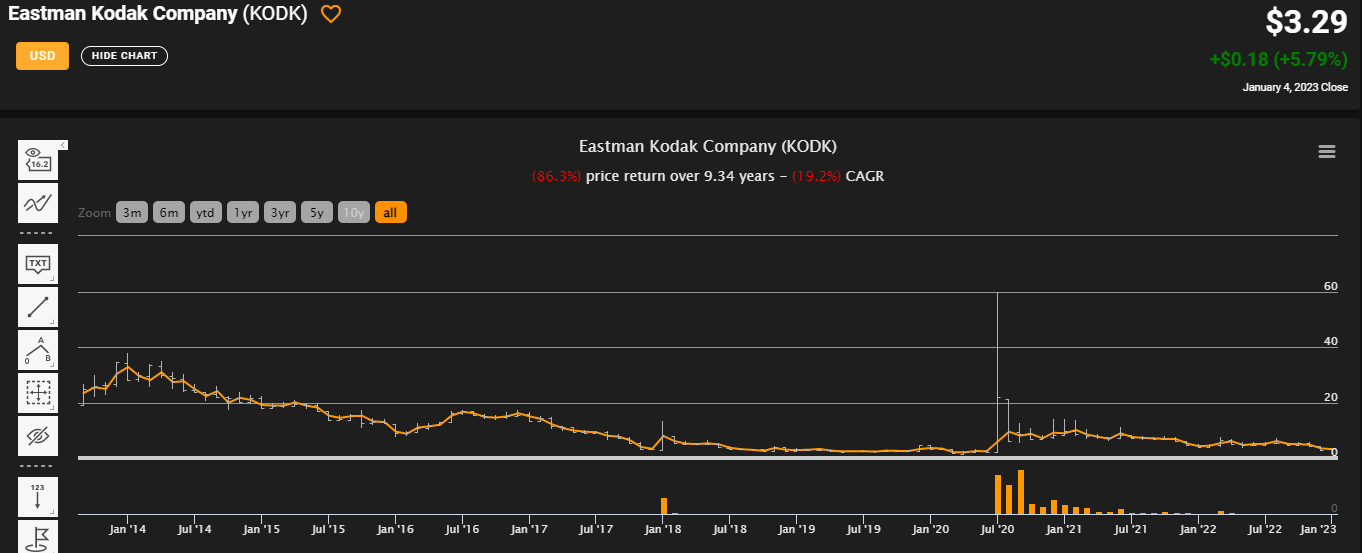

Kodak's share price has now dropped to $3.29/share as of the latest check. It also means the company now has an unimpressive 86.3% negative RoR over the past 9.5 years or negative 19.2% per year. It's a tale of value destruction, even if there have been times, such as in 2020 when you could have made money by investing in Kodak at the "right time".

{kind=link}

For 2021, the company had revenues of above $1.1B, which came to a gross profit of $164M and operating income of $54M, meaning a margin of 4.7%. After interest expenses and other things, this came to a net income of $24M, the first time since 2019 that the company could show off positive bottom line profits.

The company's fundamentals are shot. CCC+ means that Kodak is the only company below a B that I cover (unless you count the companies that don't have a credit rating, but to me having CCC+ is almost worse than having none at all).

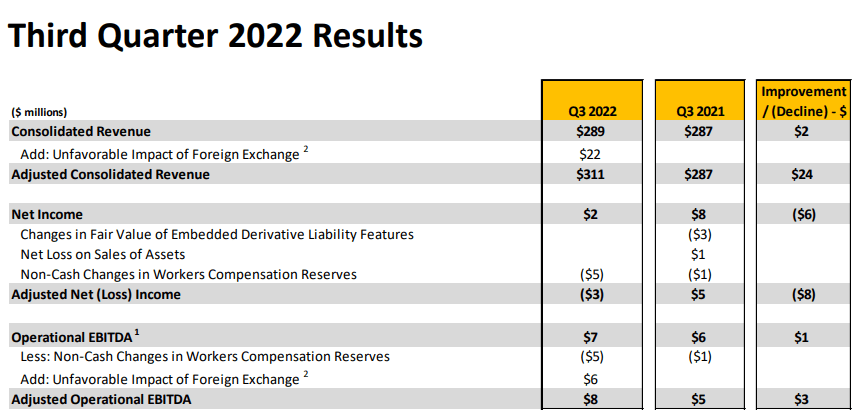

3Q22 has come and gone in November. The company continued to see top-line growth of about 1% and even higher if we exclude FX impact. Kodak focuses on what positives it can find - and one positive is that this marks the sixth consecutive quarter of revenue growth.

However, top-line is just that - top-line. The company's gross profit levels remained flat, and the company drew $50M from a term loan agreement due to its investment in Wildcat Discovery Technologies, a company that's developing a supposed EV super-cell, adding to its chemicals/materials portfolio here.

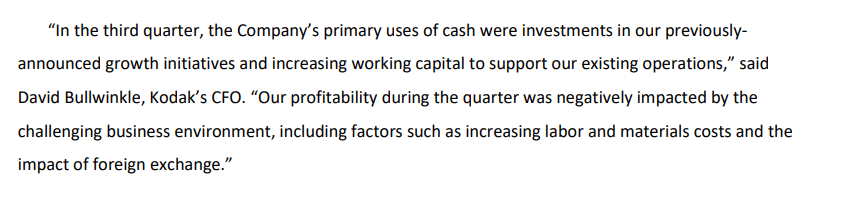

The company's challenges remain. In their own words:

{kind=link}

The company's strategy still is to focus on its core competencies in legacy print, materials and chemicals while transitioning toward revenue growth areas. It's growing digital technologies through its line of PROSPER products, which include the world's fastest inkjet press and the Ultra 520 digital press.

This means that the company now provides customers offset-like printing capabilities while no longer requiring traditional plates, which eliminates both Co2 and supply chain/manufacturing risks. This is a positive.

However, as we can see from revenue down to adjusted FCF/EBITDA, that's still a long way from going anywhere impressive, with an adjusted operational EBITDA margin of 2.7%.

{kind=link}

And for the YTD period, results are worse, with that EBITDA down nearly half on an adjusted basis despite volume improvements, mostly due to increased investments.

Those investments remain the focal point of Kodak. until the company finds ways to generate revenues, I believe that this is where we're going to be - Kodak basically hanging on by a thread. This is confirmed, as I see it, by management's own discussion.

{kind=link}

So, while 3Q22 saw some improvements in the top line, I view Kodak as a company in a "holding pattern", and one of the worst holdings patterns out there because it's a barely profitable business at this point.

If and once the company does find revenue generators - which it currently tries to invest in on a relatively continual basis - that may change, which in turn would of course turn around the share price and drive valuation - but until I can see clearly that this is the case from a P&L perspective, I wouldn't put money into what I see as a barely-profitable business.

Still, Kodak is better than most supposed "tech growth" out there today, because it actually generates positive cash flow and net income for 2021 and probably for this year as well.

Let's look at valuation.

Eastman Kodak Valuation

There's a reason why this company is one I still view as a "zero", and it's related to the near-zero in profit and earnings that it manages to eke out from its revenues.

The company's EPS multiples and anything profit-related is completely out of whack. It can be objectively said that the company is "cheaper" now than it was before because the share price is obviously cheaper and multiples are, again, obviously improved. However, we have no forecasts, no real workable multiples to calculate anything consistent with, and no real forecast accuracy on a historical basis.

When it comes to Kodak, I find myself with no choice other than working with my own assumptions. Based on management's guidance and what's been happening for the past few quarters in terms of profitability and revenue growth, I would argue that we can use a positive forecast, assuming a growth rate of 4-7%.

This is due to , even if we assume this growth rate, and a WACC range that's wide between the current-considered WACC of 27% (Source: GuruFocus ) and higher, we still get an implied share price per share that's well below $4/share. If our calculations give us such results when we use such very positive numbers to work of, you can imagine what sort of valuation we would get if we look at how the company is actually growing its earnings over time.

The issue is, in part, the massive volatility to the share price. Beta plays a role here. In addition, the company's equity weighting remains very high (though lower now), and WACC depends mostly on the overall cost of capital. A high beta results in a high cost of capital. While the beta is down from highs of 6x back in 2020-2021, and down from my latest article as well, we're still at beta of 4.21x.

If we assume growth rates of 8-10%, we get implied share price levels that would tell us the current price is "fair" for what the company is, but you should understand without me needing to break it down why we can't use those sorts of positive growth rates in a serious manner - it's highly unlikely that they'll come to pass.

There is no real situation where I would view Eastman Kodak as a "BUY" at this time. There's no price target that I'm willing to give at this time, which is very, very rare for me. Every company does have a value, but at this time I consider the specifics to uncertain to really pinpoint it - and fundamentals being in the toilet isn't helping things any.

Instead, my focus lies on my previous thesis, which was the following and still is the same at this time.

As before, there are no analysts or street targets to consider for this company.

Thesis

My thesis for Kodak is the following:

- Kodak is an impressive business - if we looked at it in 1995. Today, it's a company with a mix of remaining legacy assets and segment ideas that it aims to expand. Until it does, its fundamentals, including some very basic things like gross margin (less than 14%), imply the company lacks and there are issues here.

- I believe the company can be bought once any sort of turnaround and clarity is present here - and once we're looking at some sort of BB-rating.

- Until then, the company is a "HOLD" if you believe in it and own it; otherwise, I'd avoid or "SELL" Kodak.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Kodak is neither qualitative, nor fundamentally safe. It doesn't have a dividend it's not cheap and it doesn't have a realistic upside. As such, it fulfills none of my criteria.

Stay away from this one.

For further details see:

Eastman Kodak: Still A 'Zero'