ECAT - ECAT: Saba Trying To Shake Things Up

2023-06-07 15:38:53 ET

Summary

- Saba Capital has submitted a notice of intent to nominate four independent trustee candidates for BlackRock ESG Capital Allocation Trust's board and present five advisory proposals at the annual meeting.

- The activist shareholder aims to address the underperformance and significant discount to NAV of the closed-end fund (CEF).

- We believe Saba Capital's involvement is positive for the CEF's shareholders, as it has a history of creating value by closing gaps between fund assets and share values.

Thesis

We wrote an article regarding BlackRock ESG Capital Allocation Trust ( ECAT ) in March here , where we highlighted how the fund sported a significant discount to NAV and was using enormous amounts of return of capital ('ROC') in order to pay its dividend yield. The article did not go unnoticed, and one of the activist shareholders in ECAT moved forward in trying to shake things up at ECAT:

On March 22, 2023, Saba Capital Master Fund, Ltd., a private fund advised by Saba Capital Management, L.P., submitted to BlackRock ESG Capital Allocation Trust a notice of intent informing the Company of its intention to nominate a slate of 4 independent trustee candidates, Ravi Bhasin, Ilya Gurevich, Richard Thiemann, and Emmanuel Werthenschlag, for election to the Board at the Company's 2023 annual meeting of shareholders. Saba Capital Management also notified the Company of its intent to present 5 advisory proposals at the annual meeting asking the Board to (1) give shareholders the right to amend the Company's bylaws, (2) declassify the Board so that all trustees are elected on an annual basis, (3) adopt a plurality voting standard in contested elections, (4) eliminate a control share provision in its organizational documents that strips certain voting rights from shareholders owning 10% or more of the Company's stock, and (5) conduct quarterly tender offers for a minimum of 10% of the outstanding common stock shares of the Company, if the stock's trading discount to net asset value exceeded 10% in the previous quarter.

We have highlighted before the beneficial results that Saba has brought CEF shareholders via several articles:

- We covered ClearBridge Energy MLP Total Return Fund Inc ( CTR ) and Saba's impact here .

- We covered here Saba's success in closing the discount for the Center Coast Brookfield MLP & Energy Infrastructure Fund ( CEN ).

We believe regular shareholders always benefit from activist shareholders, because they usually end up closing some of the discounts to NAV that exist for structural reasons. At the end of the day, asset managers need to justify their performance and fees, and retail investors do not always have the firepower to engage large corporates.

The underperformance observed in ECAT since issuance and its discount to NAV have brought about Saba's actions:

The CEF's discount is off the lows recorded at the end of last year (which were close to -20%), but are still very wide for an asset manager such as BlackRock. Good funds from this issuer usually trade flat to NAV or at premiums.

BlackRock however did not move forward with any of the Saba recommendations, which has prompted the following letter from the activist fund to its fellow shareholders:

{kind=link}

Why are activist corporate actions justified?

In our opinion, activist shareholders' actions are justified because asset managers have a fiduciary duty towards shareholders and are paid management fees in order to perform. CEFs are very particular structures, but ultimately they are vehicles where value can be created when they trade at large discounts by simply liquidating all assets.

If ECAT would decide today to liquidate all its assets, then shareholders would realize an instant 11.5% gain. You do not need the market to move, equities to gain or rates to go lower. You just need a structure to unwind. Successful large managers have CEFs that trade flat to NAV or at premiums. BlackRock itself is a platform that tries to help its CEFs with share repurchases when discounts widen towards -10%.

Is ECAT going to liquidate? Most likely not. The main reason is represented by the fees the asset manager is clipping on the large $1.6 billion AUM the fund is running. The fund will likely turn around once a new bull market starts, but we would have expected more from the asset manager when the discount hit -20% to net asset value.

Saba's history with BlackRock

This corporate action is not Saba's first dance with BlackRock. The fund has engaged the asset manager before on a different CEF, namely the BlackRock Credit Allocation Income Trust ( BTZ ):

Blackrock Credit Allocation Income Trust v. Saba Capital Master Fund, Ltd., No. 297, 2019 (Jan. 13, 2020) (Valihura, J.)

01.13.2020

In this decision, the Delaware Supreme Court reversed the Delaware Court of Chancery's holding that a stockholder of two Delaware statutory trusts was excused from complying with the deadline for submitting requested supplemental information under the trusts' advance notice bylaws. Although recognizing that the requested supplemental information was overly broad to some degree, the Court held that the stockholder failed to timely respond to the trusts in any manner and therefore should not be excused from complying with the clear and unambiguous deadline.

Blackrock Credit Allocation Income Trust and Blackrock New York Municipal Bond Trust (collectively, the "Trusts") each had advance notice bylaws requiring the provision of certain information in order for stockholder-nominated trustees to be eligible for election. The advance notice bylaws granted the respective board of trustees the right to reasonably request certain subsequent information regarding such nominees. The deadline to respond to any such request was five business days.

In connection with the Trusts' upcoming annual meetings, Saba Capital Master Fund, Ltd. ("Saba"), a stockholder of both Trusts, delivered nomination notices in accordance with the advance notice bylaws. The Trusts subsequently requested supplemental information from Saba in the form of extensive questionnaires. Saba did not respond to either Trust prior to the expiration of the five-business-day deadline.

Saba is not shy about trying to shake things up when they think fund managers can optimize structural issues to increase shareholder returns. We can guarantee none of this would happen if ECAT was performing and posting large positive annual total returns.

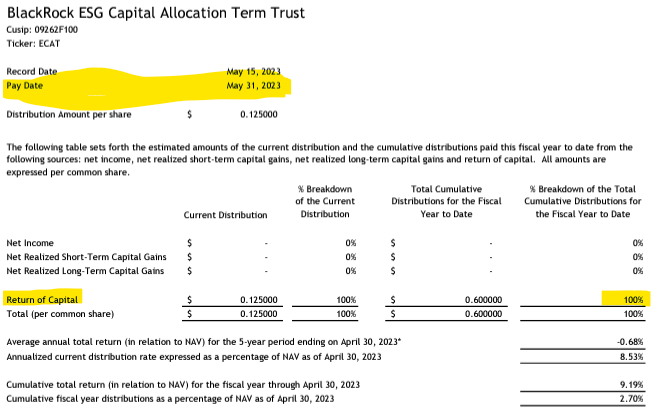

Current Distribution Composition

ECAT is still running very high ROC figures as per its latest Section 19a notice:

{kind=link}

Again, the equity component in ECAT is underperforming, with only the fixed income sleeve providing a stream of cash flows that can be used to pay the CEF's distribution.

Conclusion

ECAT is a multi-asset closed-end fund from BlackRock. The CEF IPO-ed at the top of the market in the fall of 2021. The vehicle had a very large drawdown in 2022, and has been trading at very large discounts to net asset value due to its poor fundamental performance. Its current distribution of 9.5% is not supported, with very large ROC figures utilized to cover it (100% ROC as of the May Section 19 notice).

Saba Capital is an activist shareholder which has taken a position in the fund and is trying to change the fund's trustees and force the CEF to start share repurchases. The fund is well known in the CEF space for trying to close arbitrage gaps such as this one. Ultimately, ECAT is a structure holding assets which are valued 11.5% above the market price of the ECAT shares.

We think ECAT's issues will be fixed once a new structural bull market starts, but the fund manager needs to take some additional actions to fix the current state of affairs. Saba's involvement with ECAT is very positive for the CEF's shareholders because they have a known, proven fund trying to create value by closing the gap between the fund's assets values versus its shares.

For further details see:

ECAT: Saba Trying To Shake Things Up