ECCX - ECC.PR.D: The Riskiest Slice Of The Eagle Point CEF Capital Structure

2023-11-20 10:13:24 ET

Summary

- Eagle Point Credit Company Inc. is a fixed-income CEF with a primary objective of generating high current income from CLO equity.

- The CEF's liability structure includes a mix of unsecured notes and preferred equity, with the Series D preferred stock being the riskiest slice.

- The Series D preferred stock has a perpetual maturity date, was issued at the top of the market, and is classified as equity rather than 'Liabilities' on the balance sheet.

- The CEF used the Series D proceeds to retire some of its senior unsecured notes, namely 50% of the Series 2028 Notes.

Thesis

Eagle Point Credit Company Inc. (ECC) is a fixed income CEF. The vehicle's primary investment objective is to generate high current income, with a secondary objective of generating capital appreciation. The fund invests in CLO equity tranches and sports a 28% leverage ratio obtained via debt and preferred equity issuance.

In this article, we are going to look at the CEF's capital structure and determine which slice is the riskiest one, while at the same time quantifying the downside in an adverse scenario.

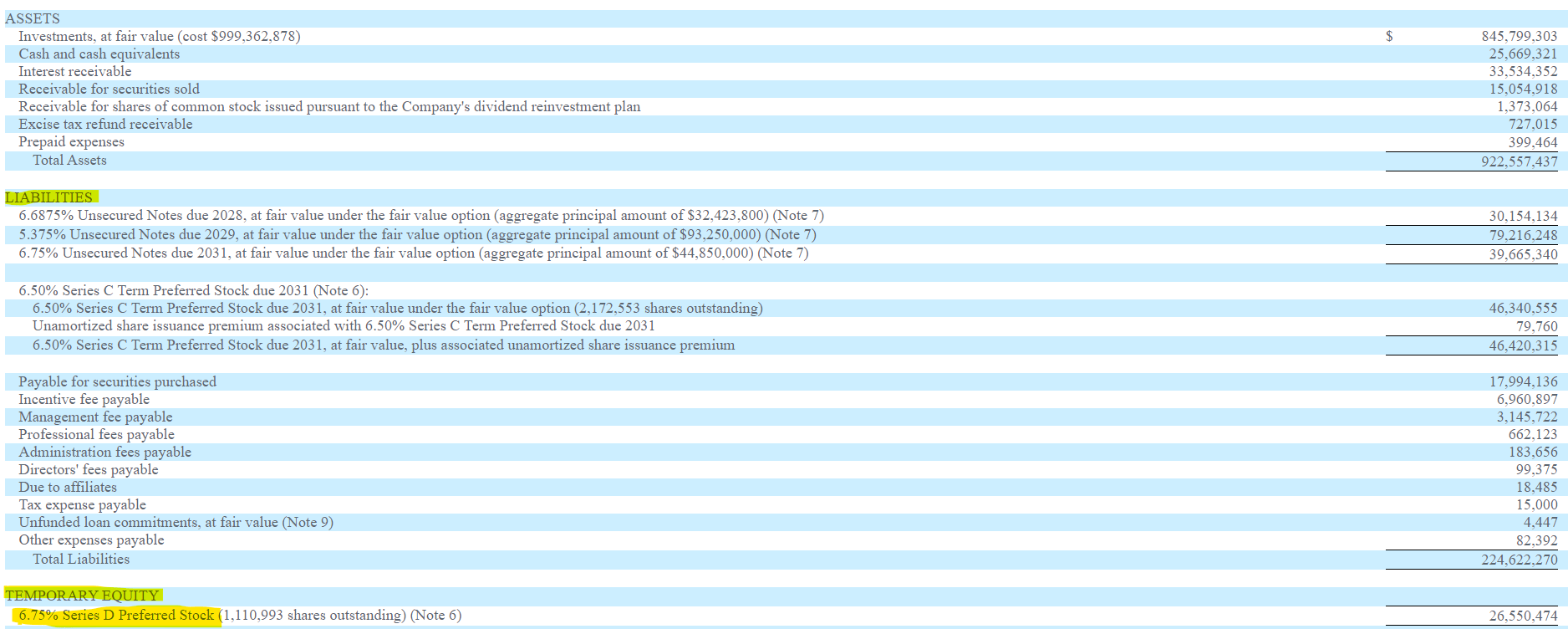

Liability structure

The CEF obtains its leverage via a mix of unsecured notes and preferred equity:

Capital Structure (Annual Report)

{kind=link}

We can see from the above table obtained from the fund's Annual Report that the fund has two outstanding series of preferred equity and three tranches of notes with mixed maturities.

It is important to note that only the latest issuance, namely the Series D Preferred Stock, does not have a defined maturity date. That is extremely important from both a pricing/valuation perspective as well as from an accounting one.

Firstly, from a valuation standpoint defined maturities matter. Whether issued in the form of a note or preferred equity, a defined maturity date provides for a set date when your principal is going to be returned, thus bringing the concept of yield to maturity in the mix:

Yield to maturity is the total rate of return that will have been earned by a bond when it makes all interest payments and repays the original principal.

As you will notice from the above definition, the concept of yield to maturity only exists when the original principal outlay is repaid back at the set maturity date. Otherwise, there is no yield to maturity for preferred perpetuals, only a theoretical one based on an assumed maturity date. In general preferred bonds/equities that are perpetual get comped based on current yield:

Perpetual Pricing (analystprep.com)

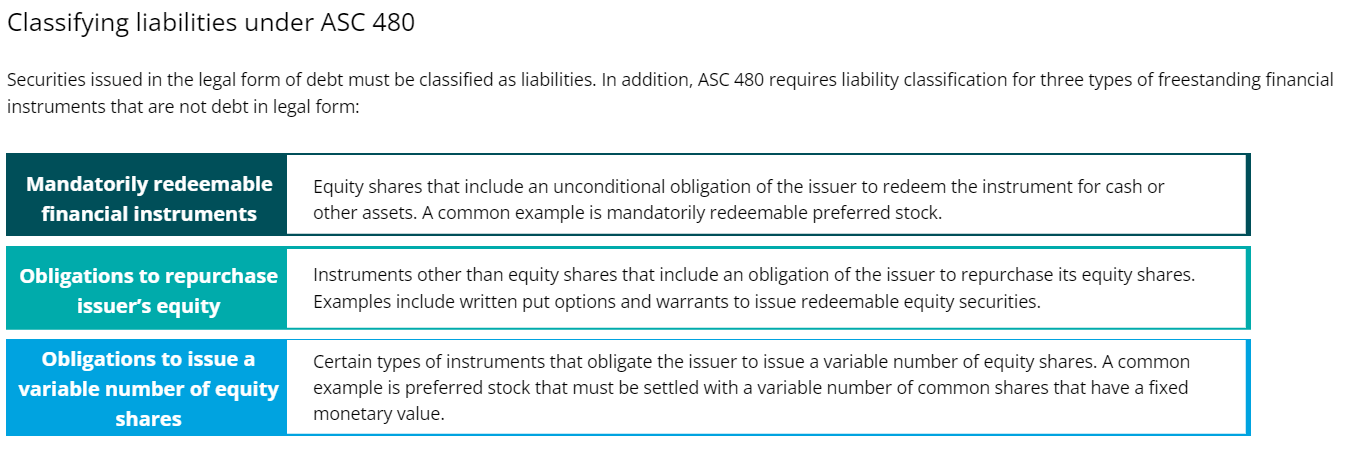

Secondly, equally important, is the accounting classification aspect for term maturities versus perpetuals. Preferred equity originated with companies due to their favorable accounting treatment where they were classified as equity rather than liabilities. This accounting classification allowed for the reporting of lower debt ratios (think Debt/EBITDA), which made institutions less risky in the eyes of investors.

The same concept applies to this CEF, with the company classifying the notes and Series C preferred equity as 'Liabilities', while the Series D is equity:

{kind=link}

Looking at the CEF's balance sheet above, an investor might ask themselves why is the Series C categorized as a liability, while the Series D preferred equity is recorded as equity. It all comes down to accounting standards:

{kind=link}

As per Deloitte, even preferred stocks that contain an unconditional obligation of the issuer to redeem the instrument for cash, are considered liabilities rather than equity. This is done to ensure a company does not simply circumvent debt covenants by issuing preferred equity with a term maturity. In our CEF's case the Series D does not have an unconditional obligation to be redeemed, and thus is classified as equity.

Why did the CEF issue the Series D? Smart liquidity management is the answer.

The CEF issued the Series D shares at the end of 2021, at the top of the market, and smartly utilized the proceeds to retire existing debt. On February 14, 2022, the CEF redeemed the total principal amount of the Series 2027 Notes and 50% or $32.4 million of the aggregate principal amount of the issued and outstanding Series 2028 Notes (ECCX).

By retiring fixed-term debt and replacing it with perpetual equity, the CEF was able to significantly extend its maturity profile. To that end, the fund has no financing maturities prior to April 2028. The weighted average maturity of the current outstanding financing stands at 6.7 years, and the weighted average cost of capital was only 6.18% as of June 30, 2023.

Why is the Series D the riskiest slice of the capital structure

Duration is the answer. As we can see from the CEF's liability structure, all notes have a defined maturity date, with the last liability to maturity being the Series C preferred equity. Series D was issued with a perpetual maturity date and furthermore issued at the top of the market in November 2021. The CEF will not get the chance any time soon to benefit from the 2021 zero rates environment, and it might also find it very hard from a cost perspective to place perpetual stock in the future.

To that end, we believe the Series D in effect will not be redeemed in the next 10 years, with the suspicion that it might actually never be. The cost of funds is very low for such an issuance and we see a difficult funding time ahead for the markets which would preclude attractive pricing for even term funding.

A perpetual maturity translates into a very high duration figure. Duration can make a significant dent in pricing during times of distress.

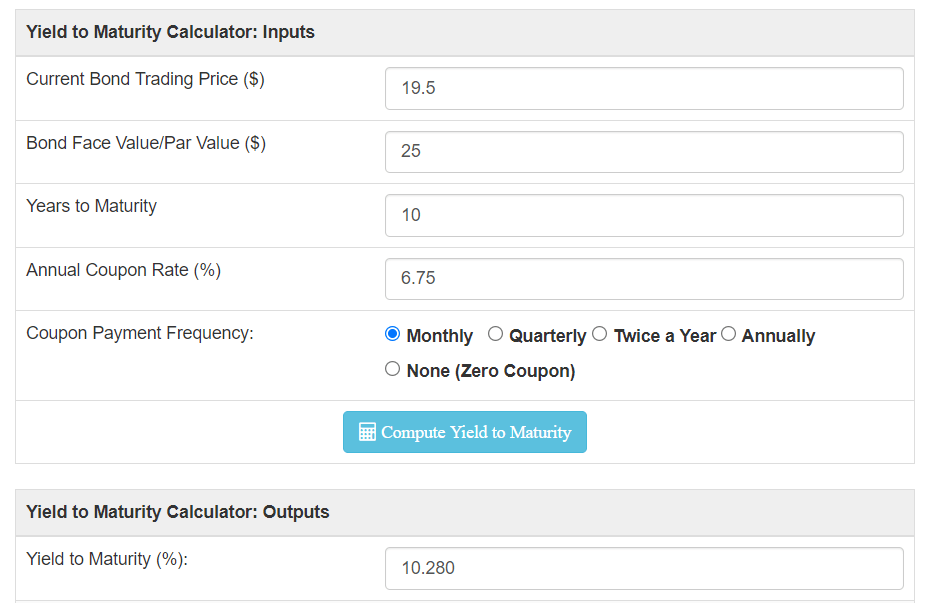

How low can the price go?

Let us have a look at the current pricing and then stress test this security. ( ECC.PR.D ) is perpetual, but let us assume a 10-year maturity date so that we can use bond math here. It is currently trading at $19.5, which gives us an implied yield to maturity to a theoretical 10-year date of roughly 10.2%:

{kind=link}

So using bond math and a ten-year treasury yield of 4.5%, the security is trading at treasuries plus 5.7%.

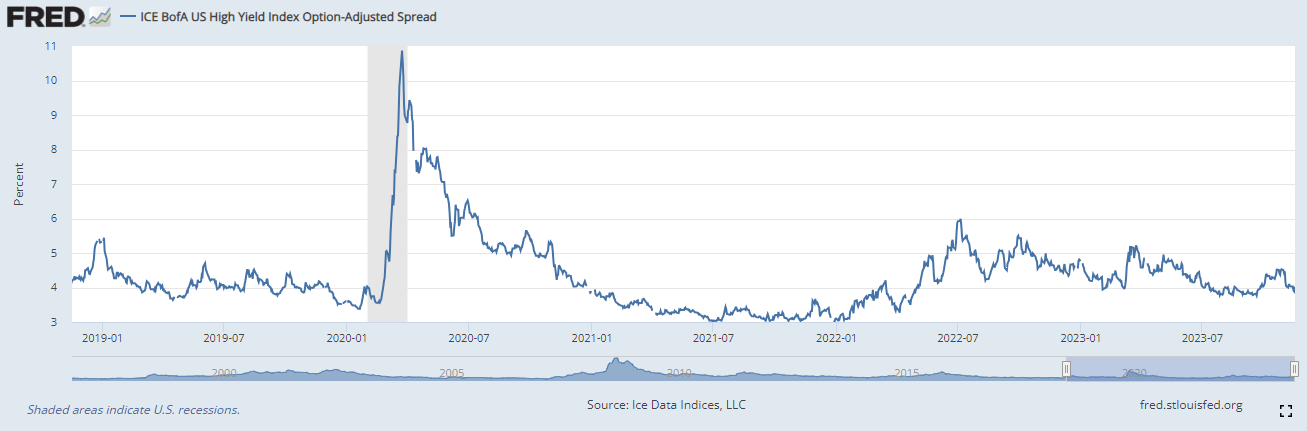

Following past scenarios, let us assume a stress case where credit spreads move up by 50%. This scenario tallies up with historical data:

{kind=link}

If we look at the ICE BofA US High Yield Index OAS Spread, we can see it is currently trading at 400 bps but was as wide as 600 bps during last year's market sell-off. This time around though we believe a significant market sell-off will be accompanied by the Fed cutting rates, therefore we will also lower the risk-free rate for our stress test by 100 bps. So the new hurdle rate will be (4.5% - 1%) + (5.7% + 5.7% x 0.5).

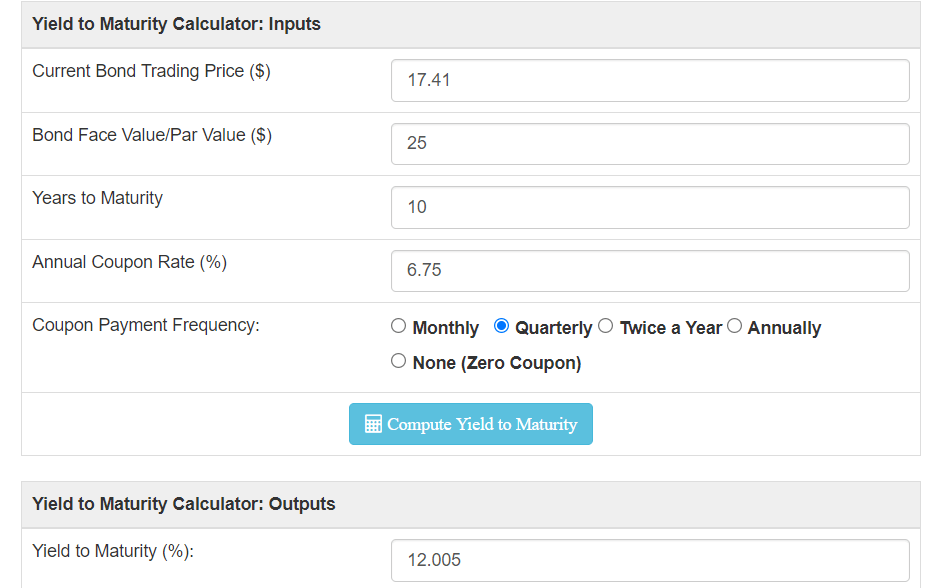

The above math translates into a yield to maturity of 12%:

{kind=link}

Applying this stress scenario to the security gives us a pricing of $17.4 per share, or roughly -11% lower from here.

Conclusion

ECC is a CLO equity closed-end fund. The vehicle sports a 28% leverage ratio achieved via bonds and preferred equity. The CEF issued its Series D preferred stock at the height of the market in November 2021, and achieved a very attractive cost of funds of only 6.75% at the time, with a perpetual maturity date. ECC.PR.D represents the longest duration slice of the capital structure, and in our opinion will represent a permanent funding instrument (i.e. it will never actually be called).

We believe the markets will experience another risk-off event next year, mainly driven by credit spreads. In such a scenario ECC.PR.D will see a price move of roughly -11% from here. A retail investor is best served to consider the Series 2028 Notes from the ECC capital structure, notes which have a debenture feature, a 5-year duration (defined maturity date), and an attractive spread over similar duration treasuries.

For further details see:

ECC.PR.D: The Riskiest Slice Of The Eagle Point CEF Capital Structure