GCV - ECF And GCV: Divergence Playing Out Revisiting This Idea

2023-04-13 13:21:52 ET

Summary

- In 2022, we highlighted how ECF was "a clear choice" over GCV.

- This has been playing out, and it could have more to go.

- However, with GCV's higher distribution yield, it could support its current valuation better.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on April 12th, 2023.

Last year we highlighted an opportunity for investors to consider : Ellsworth Growth and Income Fund ( ECF ) over Gabelli Convertible & Income Securities Fund ( GCV ). This was based on a significant difference in valuations between these two similar closed-end funds. In fact, each of these funds is under the Gabelli umbrella of funds with the same managers. ECF simply doesn't have Mario Gabelli listed, but Thomas and James Dinsmore run both of these funds.

We quickly followed up on how this idea was playing out in December when reviewing ECF. At that time, the trade was going in the right direction, but it wasn't to the degree that we could declare victory yet. Now, due to moves in 2023 so far, this trade has really begun to shift in the direction we felt it would play out. So I felt it was appropriate to do another quick follow-up. At this point, the valuation differences are still quite stark, but it isn't such "a clear choice" due to various factors.

The Basics

ECF

- 1-Year Z-score: -1.13

- Discount: 14.51%

- Distribution Yield: 6.35%

- Expense Ratio: 0.74%

- Leverage: 29.52%

- Managed Assets: $186.3 million

- Structure: Perpetual

ECF's objective is quite simple "... providing income and the potential for capital appreciation; which objectives the Fund considers to be relatively equal, over the long term, due to the nature of the securities in which it invests." They attempt to achieve this by simply "primarily investing in convertible securities and common stocks.

When including leverage expenses, the total expense ratio comes to 1.16%.

GCV

- 1-Year Z-score: -2.16

- Premium: 3.81%

- Distribution Yield: 11.01%

- Expense Ratio: 2.25%

- Leverage: 15.79%

- Managed Assets: $95.611 million

- Structure: Perpetual

GCV's investment objective is to "seek a high level of total return on its assets." They will attempt to achieve that objective by a "disciplined approach to investing in convertible securities and other debt or equity securities that are periodically expected to accrue or generate income." They also mention that their "goal is to generate consistently positive inflation-adjusted returns."

The fund's total expense ratio, when including leverage, comes to 3.23%. That gives us a fairly wide difference in expense ratios that can help make ECF's job easier to provide better returns going forward.

Leverage Update

Leverage in both of these funds means risks and potential rewards are both amplified. GCV carries much less leverage at this time. Towards the end of 2022 , they had a Series E that was "put back to the Fund."

On December 1, 2022, 337,600 shares of Series E were put back to the Fund at their liquidation preference of $100 per share plus accrued and unpaid dividends.

They then issued a Series G preferred at a 5.2% rate. ECF has its publicly traded 5.25% Series A ( ECF.PA ) and 4.40% Series B. These were high-cost leverage sources a year ago, but after rates have been ramped up significantly through 2022, these are now quite competitive to even being cheap. Most funds could not borrow at 4.40% if it wasn't locked in previously in this current environment. This fixed-rate leverage is, at least relatively speaking, to other CEFs and, in my opinion, a positive for these funds.

Final Verdict

Since that public article was posted on July 17th, 2022, we can clearly see that ECF was the dominant performer during this period. This trade actually began to work out almost immediately before becoming more mixed toward the last quarter of 2022. So far, in 2023, the divergence between the two funds has been quite dramatic.

Admittedly, neither fund provided exceptional results during this period, but it again highlights why valuations can be so important for CEFs.

Ycharts

Of course, the main point of ECF being a clear choice was that the valuation differences between the two. The difference was so wide that it was the more probable outcome going forward between these funds.

Ycharts

Not only was the difference between the two funds significant, but GCV's own valuation compared to its longer-term historical range was well outside of its usual range.

Ycharts

Conversely, ECF was still trading at a wider-than-usual discount. Although they experienced their own run-up in valuation through 2020 and 2021, this reversed early for them in 2022.

Ycharts

The reason that is going forward, we might not see such a drastic performance difference is for a couple of reasons.

First, we saw above that GCV is coming much closer to its longer-term average. While ECF is still below its longer-term average, the current environment probably isn't conducive to discount contraction unless we start getting some more clarity going forward.

The second point that I believe going forward the trade might not be so drastic in ECF's favor would be simply due to GCV's higher distribution yield.

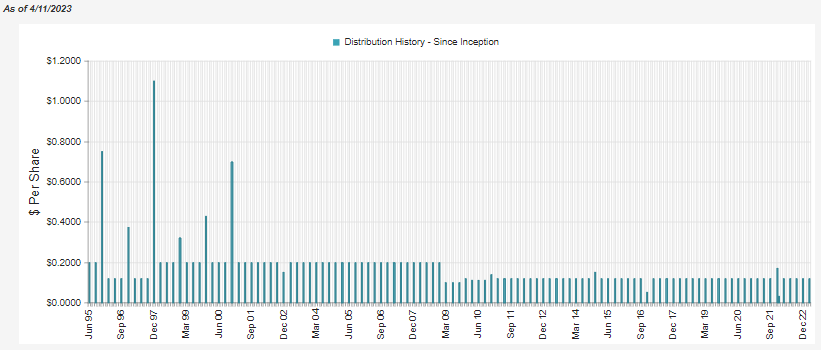

ECF's current distribution rate comes in at 6.35%, with a NAV rate of 5.43%, and it pays quarterly. The year-end specials we see in the chart below are because the fund has a managed 5% minimum distribution plan. That means some years, they pay out less than 5% and need to top it off at year-end. This is also a minimum; in some years, it will be well above this level. Still, it's paid at the year-end. Some investors prefer higher payouts throughout the year rather than a lump sum at the end.

{kind=link}

For GCV, we see a distribution rate of 11.01% and a NAV rate of 11.43%. They also pay quarterly. While that might not be sustainable during the current environment, it generally means little for the valuation of the fund as investors bid up double-digit yields, regardless. The only time it becomes dangerous to funds with higher yields is when they cut; then, valuations can dive if funds are trading at premiums. GCV hasn't historically been quick to cut, only happening a couple of times in its history.

{kind=link}

Historically, ECF has been the better performer in the long run.

Ycharts

This brings up another way to measure if a fund is covering its distribution. That is checking the annualized performance figures, the quick and dirty way to see if it's being covered. ECF's performance since inception , going back to 1986 at the end of 2022, was 7.86% on a NAV basis, suggesting they've been able to cover their regular payout.

GCV likewise has a long history after being incepted in July of 1989. Since that time through the end of 2022 , they've provided a 6.31% total NAV return. Any of the standard time periods show a return less than the fund's distribution rate. Thus, suggesting that they haven't been able to earn their distribution.

That doesn't mean that they couldn't start achieving this going forward. Common sense would suggest that an 11%+ return required to cover the payout plus their expense ratio would be fairly improbable though. However, that's also after a year where GCV experienced a 26.75% decline for 2022. ECF declined 27.59%, for some context.

Conclusion

ECF has been the better performer compared to GCV, as we thought would happen when the valuations diverged significantly. Today, the valuation difference isn't as drastic, which would suggest that most of this trade has played out. GCV has a higher distribution rate and it has historically traded at higher valuations which could provide support at the current level. At the same time, I still wouldn't be one to swap my ECF for GCV shares just yet. ECF remains an attractive discounted fund with a modest but decent yield.

For further details see:

ECF And GCV: Divergence Playing Out, Revisiting This Idea