MAXR - EchoStar: Includes Catalysts For An Upside

2023-03-29 04:14:49 ET

Summary

- EchoStar operates a satellite-based ISP and provides communications services.

- It is facing tough competition from Starlink for the ISP business.

- The change in revenue mix whereby higher revenues are being derived from enterprises compared to individual subscribers (consumer business) is positive.

- I identify two catalysts for an upside, namely the launch of Jupiter 3 and a potential satellite-to-device deal.

- Conversely, any delay could spell volatility for SATS stock.

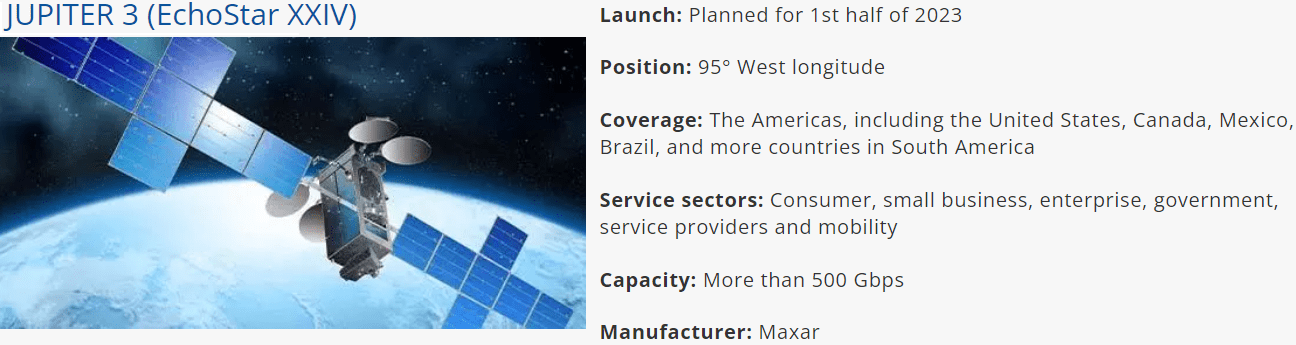

The first half of 2023 should be eventful for EchoStar Corporation ( SATS ) as its upcoming EchoStar XXIV satellite, also known as Jupiter 3 system, will be ready. Given its potential to more than double the internet speed provided by HughesNet , the company's ISP (internet service provider) over the Americas (North and South America), a successful launch should favorably impact the share price.

Now, at $17.46, the stock is roughly at the same level as when the Jupiter 3 news update was released on November 22 last year. Subsequent to that announcement, as shown in the chart below, the share price even went to the $20 level, before coming down.

Thus, my objective is to elaborate on the catalysts which can trigger an upside as well as assess whether in case things do not proceed according to plan, the stock makes for a long-term buy and hold. For this purpose, it is important to highlight some of the major developments shaping the satellite communication industry, including competition.

Reorientation as a Result of Higher Costs

To start with, just as for any sector of the economy, telecommunications has been impacted by rising costs. First, there have been Covid-led supply chain issues which have pushed up the prices of components like electronics and semiconductors, which have in turn increased the cost of radio antennae that an MNO or mobile network provider would install on top of one of American Tower's (NASDAQ: AMT ) masts.

Second, with higher wage inflation, the expenses incurred by MNOs like T-Mobile (NASDAQ: TMUS ) have gone up. This has prompted the service provider to partner with Elon Musk’s Starlink (STRLK), with the idea being to provide satellite-based basic message services, especially for remote and rural areas where traditional antennae-based mobile connectivity is prohibitively expensive.

This cost factor explains the interest in transporting data through satellites instead of terrestrial mobile cellular networks as I had elaborated in a previous thesis , illustrated by Apple’s (AAPL) launch of the satellite-to-device (in this case the iPhone 14) in partnership with Globalstar ( GSAT ). Samsung (SSNLF) has also followed suit.

Now, HughesNet which faces competition not only from Starlink but also from Viasat ( VSAT ) provides services to subscribers like you and me as part of its consumer business and also caters to enterprise requirements. Here, competition with Starlink for satellite-based ISP has been particularly tough as Musk also owns SpaceX ( SPACE ) whose Falcon rockets regularly transport payloads into space.

Additionally, according to Approved Modems , Starlink’s download and upload speeds are 50-200 Mbps and 20-50 Mbps respectively whereas, for HughesNet, it is less, at 25 Mbps (for download) and 3 Mbps (for upload). Moreover, Starlink is gaining popularity as its connectivity is sufficient for working, streaming, and even playing online for certain games. Here, it differentiates itself by using a large number of LEO or low earth orbit satellites compared to GEO (Geostationary Stationary Orbit) technology used by EchoStar and Viasat.

{kind=link}

This is the reason deploying Jupiter 3 (as pictured above) is primordial, as it will deliver over 500 Gbps of high-throughput capacity. This is more than double the throughput of 200 Gbps provided by the current Jupiter 2 launched in December 2016.

Sluggish Growth due to Competition, but Profitable

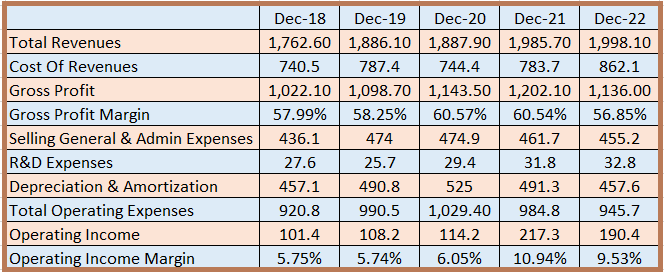

Disposing of older technology, EchoStar's revenue growth was sluggish or only 0.62% for the fiscal year 2022 when compared to 21 as pictured below. However, this is a profitable company, both in terms of gross profit and operating income margins.

{kind=link}

Detailing further, in addition to Hughes, EchoStar has the Satellite Services business segment, where it competes against the likes of Intelsat S.A., SES S.A., Telesat, and Eutelsat. Despite this competition, revenues increased by $2.9 million for 2022 thanks to this industry being one where providers benefits from long-term contracts as the switching costs are high for customers.

Coming back to Hughes, competition is tough for ISP, but, there are also other dynamics at play here other than mere internet speed. For example, in rural areas for people deprived of fiber, cellular, or ADSL connectivity, satellite internet is a boon which means that all service providers have an opportunity to gain market share. Also, not all providers cover the entire earth in the same way, signifying that the quality and strength vary considerably.

Pursuing further, while it faces tough competition for the consumer business, the company is focused on the enterprise one which grew in the fourth quarter with the company bagging $195 million of new orders in 2022, or an increase of 41% compared to last year. These orders are mostly coming from countries in Latin America.

The attractiveness of enterprise orders is that they are recognized over several years, which helps to create a more stable revenue stream, allows for revenue diversification but more importantly, entails the use of relatively less sales and marketing expenses. Thus, the adjusted EBITDA in Q4 was $164 million, or an increase of 3% from last year, also helped by continued focus on managing costs. Focusing on the corporate world also provides for better cash generation through utilizing relatively less capital investment.

In addition, the company should receive compensation pertaining to past production delays from Maxar ( MAXR ) the manufacturer of the satellite covering positioning of the satellite into orbit amounting to $14.5 million once launched and performance later on ($44 million+interests). This will be implemented through relief on future payments for a total contract value of $445 million when the satellite was ordered in 2017.

Noteworthily, the 2023 launch in fact constitutes a delay of about two years, as the previous launch was scheduled for 2021. Also, according to Via Satellite , the satellite provider sees low risks that delivery is effected after June 2023. Consequently, I consider this lowered risk factor for valuing purposes.

Valuations, Opportunities and Catalysts for Upside

Now, one of the reasons for the stock's downside was that it was downgraded from a price target of $57 to $27 on November 9 by analysts on basis that there was no catalyst for the next 6 to 12 months, which would fall in the May-November 2023 period. Now, with a delay looking less likely, there could be a surge to the $21 resistance level as per the introductory chart in case Jupiter 3 is ready.

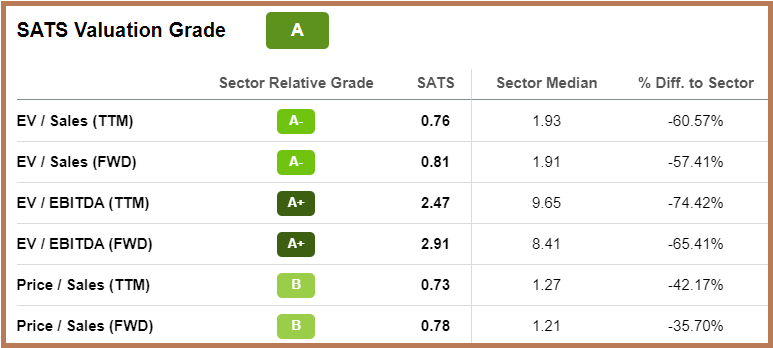

To further justify my optimism, the valuation grade is "A". Considering the trailing price-to-sales metric of 0.73x which is undervalued compared to the IT sector by over 40% and just assuming a 20% upside, I have a target of $20.9 (17.43 x 1.2).

{kind=link}

Also, while waiting for additional capacity to be added and cash for operations to increase, the company is managing costs with Capex reduced from $438.3 million in 2021 to $325.9 million in 2022. This has helped to increase free cash flow (levered) from $87.5 million to $134.5 million during this period.

Then, there is also the S-band frequency, which represents a significant area of opportunities.

In this case, EchoStar will launch a global S-Band network with 28 satellites in LEO as part of an agreement with Astro Digital, a designer and manufacturer. The ultimate aim is to be a stronger player in IoT or Internet of Things, a network service for connecting devices on earth in a low-cost and secured fashion so that companies can monitor assets across vast distances. The project may cost around $100 million to $200 million and possibly materialize next year .

Then, there are also opportunities in the satellite-to-device market as I touched upon earlier, where a smartphone comes packaged with satellite linkage. In this respect, according to EchoStar's CEO, this is an area of "fundamental opportunity" where the ultimate aim is to use a mobile phone in the same way as a ground-based network. This will take a few years' time, but, in the meantime, similarly to the T-Mobile-Starlink partnership, the company has already tested messaging-based service from satellite to device with related commercial offerings being planned for the near future.

Now, with the direct satellite-to-device market expected to be valued at around $93.1 billion between 2021 and 2031, do expect any related announcement to impact favorably on the stock.

Conclusion

Therefore, I have identified at least two catalysts that can trigger an upside, with the most probable one being the placement of Jupiter 3 into orbit. Now, as to whether it is the right time to buy, the stock is at an RSI of around 34 which is well below 50 and is therefore not overbought.

However, any further delay may induce volatility in the stock price, and it could drop further, to the $15.48 support level last reached in September 2022 in case HughesNet loses market share to Starlink as a result of not being able to add capacity.

Still, the price target of $21 is modest and remains below the average of $24 which analysts expect. Furthermore, for those holding the stock, it is comforting to know that EchoStar has $1.68 billion of cash, a debt to equity of 45.86%, and that the management is stringent on managing costs. Finally, I like the change in revenue mix with more sales derived from enterprises compared to individual subscribers together with the fact that the satellite operator is being compensated by the supplier.

For further details see:

EchoStar: Includes Catalysts For An Upside