EC - Ecopetrol: A Beneficiary Of Rising Oil Prices Macro Risks Still Apparent

2023-10-20 14:41:09 ET

Summary

- Global oil prices remain high amid geopolitical tensions, offering risks and opportunities for Energy sector stocks and dividend investors.

- I am upgrading Ecopetrol from sell to hold due to its decent operating performance and stabilizing earnings.

- The company faces risks from debt, volatile oil prices, and political instability in South America.

- I outline key price levels to watch on the chart ahead of Q3 earnings due out next month.

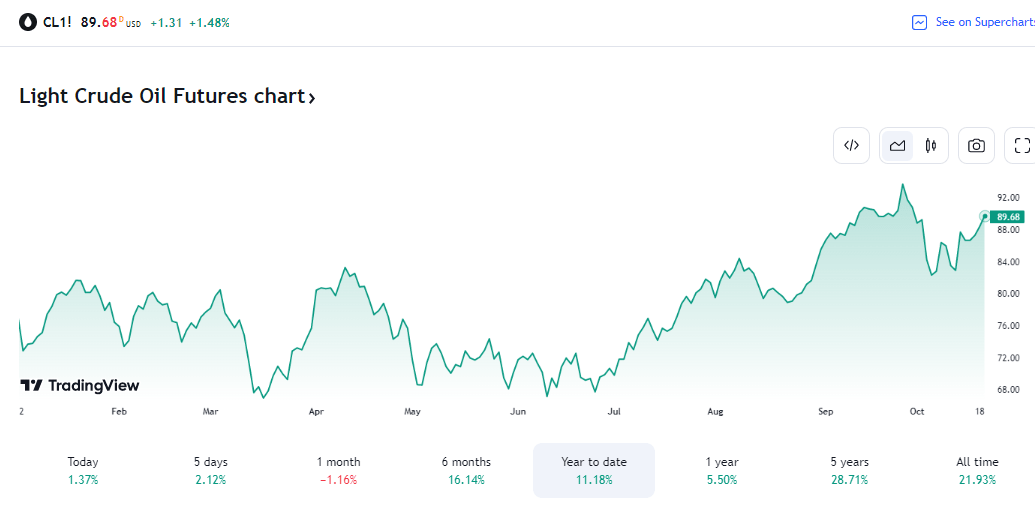

Global oil prices remain on edge amid heightened geopolitical tensions. The price of a barrel of light sweet crude is near $90 while Brent oil is even higher. The move comes as gasoline crack spreads dip, but large oil & gas companies still profit from such lofty oil prices. International energy firms, however, also face currency risks for US investors.

Amid these uncertainties, I am upgrading Ecopetrol ( EC ) from a sell to a hold.

WTI Rises To Near 2023 Highs

{kind=link}

Ecopetrol operates as an integrated energy company, and it operates through four segments: Exploration and Production; Transport and Logistics; Refining, Petrochemical, and Biofuels; and Electric Power Transmission and Toll Roads Concessions. Ecopetrol has a growing renewables business. It has operations located in the center, south, east, and north of Colombia, as well as outside of its home country. The Republic of Colombia is the majority shareholder with a participation of 88.49%, according to the company website. The firm weathered political uncertainty well during the middle of last year, helping shares to outperform the broad international equity market.

The Bogota-based $25 billion market cap Integrated Oil and Gas industry company within the Energy sector trades at a low 4.4 trailing 12-month GAAP price-to-earnings ratio and pays a high 26.9% forward dividend yield. Ahead of earnings due out next month, shares trade with a moderate implied volatility percentage of 37%.

Back in August, EC reported a mixed quarter. Average daily oil production tallied 728,000 barrels per day, a 3.3% increase from the same quarter a year earlier. The growth was attributed to robust performance in key fields, including Cano Sur and the Permian in the US. All told, the company recorded revenues of COP34.3 trillion, EBITDA of COP14.6 trillion, and net income of COP4.1 trillion, about in line with what the management team was expecting. Ecopetrol’s gross debt to EBITDA ratio stood at 1.6x, better than its 2.1 target, but its level of debt remains a key risk along with volatile oil and gas prices in South America, though favorable news came in October when Columbia announced it intends to pay $2 billion to Ecopetrol to support energy price stability.

Any company owned largely by a sovereign entity often features a depressed valuation when that state is in a politically volatile region. As such, EC’s low 5.5% forward non-GAAP P/E makes sense. Moreover, the Energy sector’s valuation is notably below that of the broader market, though recently rising oil prices are undoubtedly a boon to the oil & gas space. EC boasts strong margins, but it also carries a significant amount of debt when backing out the cash, so higher interest rates hurt the firm.

With free cash flow per share near the flat line due to heavy capex (executing COP12.3 trillion in organic investments during the first half of 2023), the firm must be careful with how it deploys capital in today’s tighter credit conditions. Dividends , meanwhile, have increased since April of last year given the strong run in the oil markets – don't expect consistent payouts from Ecopetrol, however.

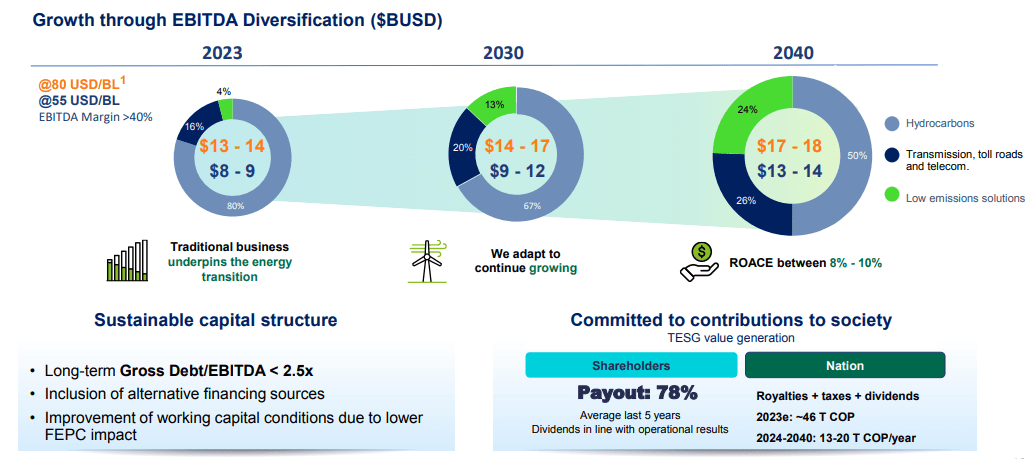

Investor Presentation: EBITDA growth and greater diversification

{kind=link}

On valuation , the consensus EPS estimate shows, 2023 per-share profits summing to $2.23 this year. Out-year EPS expectations are then seen dipping closer to $2 while top-line figures stagnate.

EC: Annual Earnings Per Share Seen Dipping To Near $2

Seeking Alpha

If we assume normalized EPS of $2.14 and apply a 6x multiple, then shares appear about fairly valued today. I assert that a significant margin of safety, or valuation discount, must be applied given EC’s ownership structure and the volatile area in which it is headquartered. While there are many attractive metrics seen below, I would like to see improved free cash flow to support the high dividend payments – the firm is ambitious with its Q3 2023 FCF target, per the most recent quarterly report presentation .

EC: Compelling Valuation Metrics

Seeking Alpha

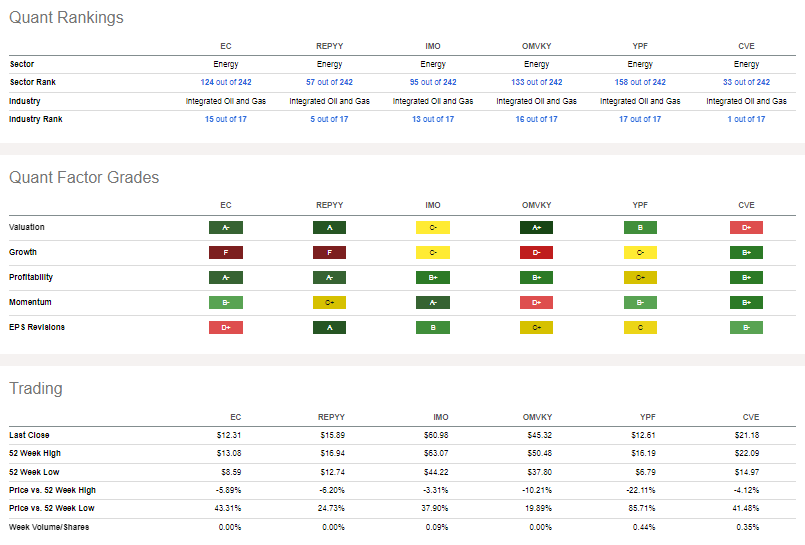

Compared to its peers , EC features a solid valuation, though comparable firms also have modest valuation ratios. Growth with Ecopetrol is weak, as noted earlier, though the firm is consistently profitable with very strong share-price momentum (which I will detail later). EPS revisions have been to the bad side, but oil above $90 should warrant some refreshed upward earnings revisions as we approach the earnings date.

Competitor Analysis

{kind=link}

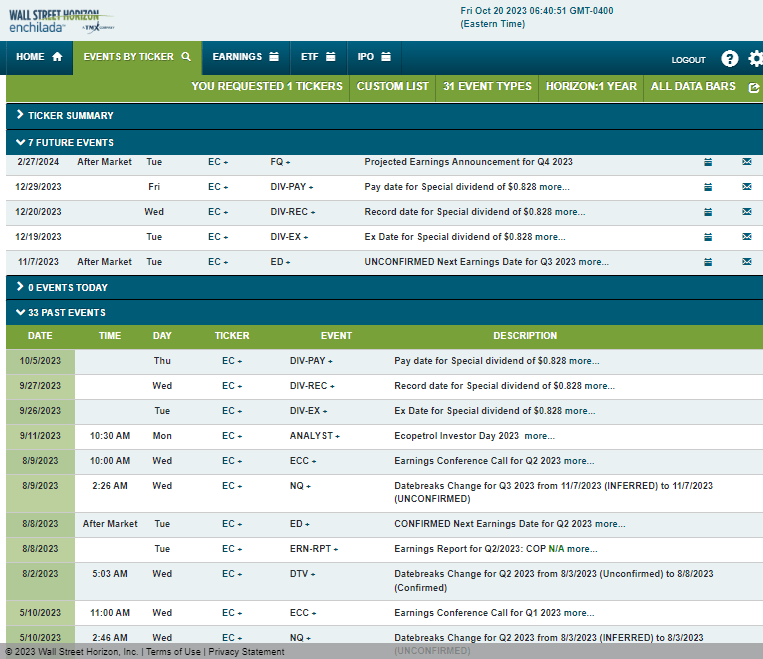

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q3 2023 earnings date of Tuesday, November 7, after the closing bell. Importantly, with this ultra-high-yielder, the next ex-dividend date is Tuesday, December 19.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

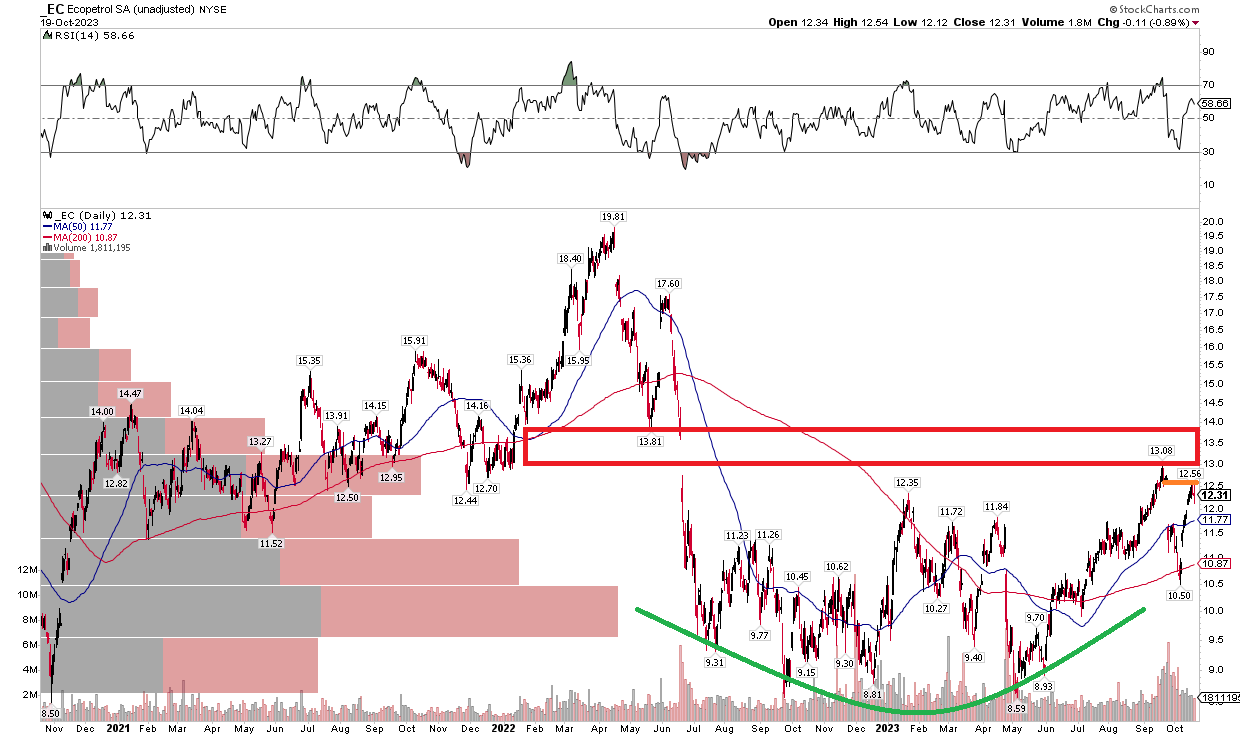

EC has been a winner in the last year. Shares are up more than 47% on a total return basis, outpacing the all-country world index by some 26 percentage points. With a significant portion of the total return coming via dividends, the technical piece of the analysis should be taken with a bit less confidence. Still, notice in the chart below that shares have approached a key resistance level in the $13 to $14 area – that is where the stock gapped down from in mid-2022 following the oil price plunge and political unrest in South America.

With a rising 200-day moving average, however, the bulls appear in control. Moreover, a bullish rounded bottom pattern was put in from July 2022 through this past quarter. I’d like to see the stock rise above $14, but I also see support in the $10.50 to $11 range (the October low and where the 200dma comes into play.

Overall, it’s a somewhat constructive chart, and relative strength (using total returns) is very impressive.

EC: Price-Only Chart Shows Some Resistance In Play, Rising 200dma

{kind=link}

The Bottom Line

I am upgrading EC from a sell to a hold. I was admittedly too skeptical about the stock last year, though I still see political risks, a significant debt burden, and broader macro/cyclical risks as in play.

For further details see:

Ecopetrol: A Beneficiary Of Rising Oil Prices, Macro Risks Still Apparent