EC - Ecopetrol Is A Steal At 3.3x Earnings With 22% Dividend Yield

Summary

- Colombian state-owned oil company Ecopetrol announced record profits and a dividend increase Tuesday.

- Shares have been trading near 52-week lows despite Ecopetrol's operational strength.

- It seems market participants thought Ecopetrol would cut its dividend. Instead, it gave shareholders another increase.

- Colombia has its risks, but Ecopetrol shares are discounted far more than is appropriate.

Colombian state-managed oil company Ecopetrol ( EC ) announced its Q4 and full-year 2022 results on Tuesday. And they were tremendous, with the company hitting records across the board. The company also hiked its dividend thanks to the company's increasing financial strength.

And yet, shares are way down from where they were trading in recent years:

This probably seems particularly strange given that Ecopetrol is an oil company. And, as you've probably heard, oil companies are earning far more money today than they were a few years ago. Many energy companies have already moved to new record high stock prices during this renewed upturn in the oil and gas sector. Yet here's Ecopetrol shares down sharply from where they were trading in past years.

As I'll argue below, this is a big mistake on the market's part, and investors willing to buy here will be amply rewarded both by the current 22% dividend yield and the sharply undervalued oil, energy, and infrastructure assets that Ecopetrol owns.

What Is Ecopetrol ?

Ecopetrol is the state-operated oil company of Colombia. The Colombian government owns 88% of the company , with the remaining 12% traded both in Colombia and on the New York Stock Exchange.

This ownership structure leads to an interesting alignment of interests. 88% of dividends paid by Ecopetrol go to the Colombian government to fund its obligations. As such, the state would prefer that Ecopetrol have as high a dividend as possible, all else being equal. This is important for reasons we'll get to in a minute. Meanwhile, the other 12% minority shareholders are along for the ride.

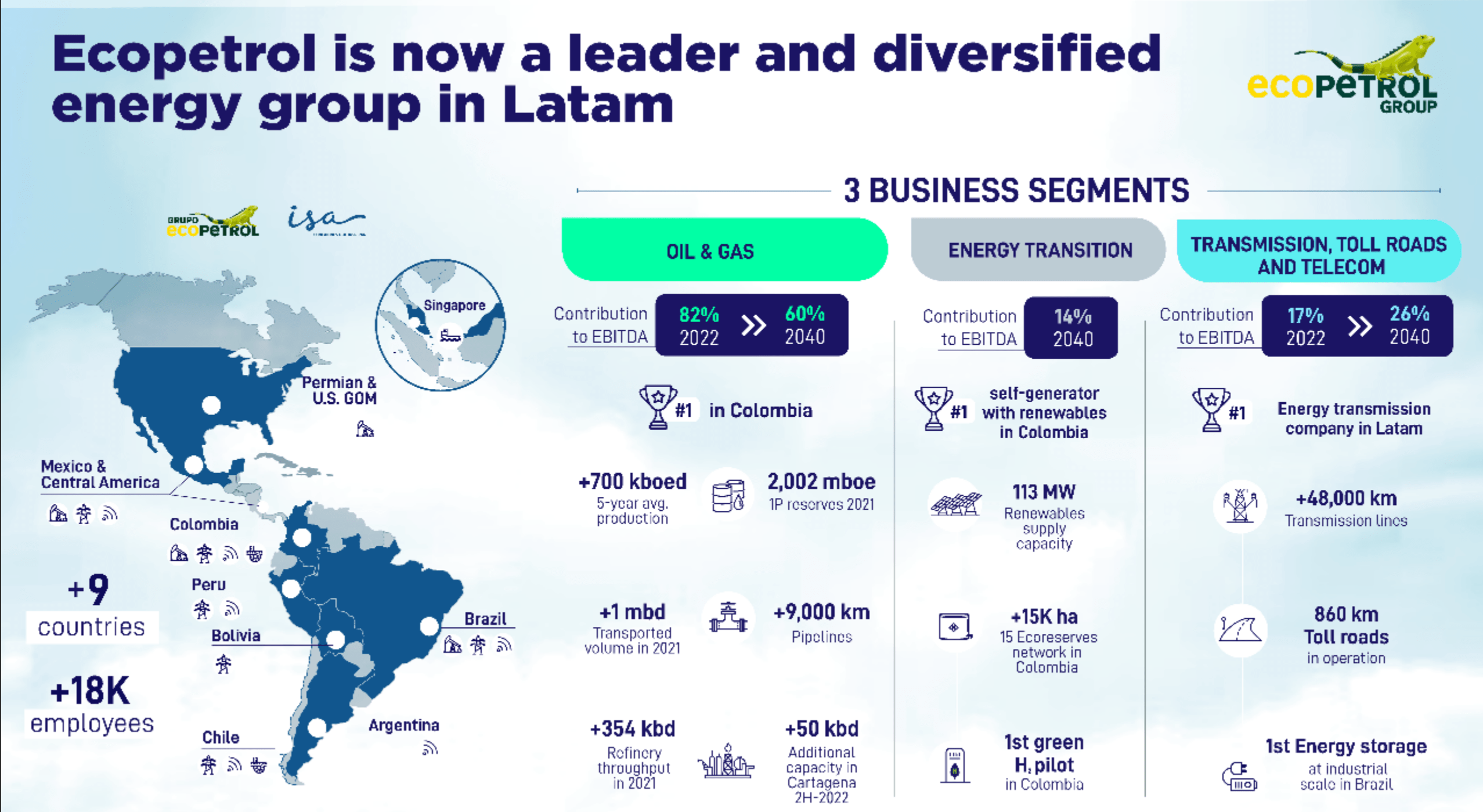

And what does Ecopetrol own, exactly? Quite a lot:

{kind=link}

It has assets spanning the Americas from the Southern Cone up to the Permian Basin.

That said, Ecopetrol remains an overwhelmingly Colombian business. It operates more than two-thirds of Colombian oil production, along with virtually all of the country's refining capacity. It has a big position in pipelines with more than 9,000 kilometers of them in total.

It has also diversified away from oil and gas. It is the #1 producer of renewable power in Colombia. I'd note that solar tends to make a lot better economic sense in countries on the equator with more intense direct sunlight, such as Colombia, as opposed to less tropical parts of the world.

In addition to renewables, Ecopetrol has invested heavily in infrastructure including nearly 50,000 kilometers of power transmission lines. It also owns 860 kilometers of toll roads along with various telecom assets and energy storage facilities.

In other words, there's a lot more to Ecopetrol than just oil sales, and it doesn't live and die by the daily fluctuations in the price of crude.

Why The Stock Is Badly Mispriced

So Ecopetrol has solid assets. In addition to its 700k barrel of oil equivalent production, there is also a large contribution from refining and midstream, along with growing operations in infrastructure and renewables.

As of Tuesday's close, Ecopetrol had a market cap of $23 billion. On Tuesday, it announced full year results. For FY '22, Ecopetrol earned 33.4 trillion Colombian Pesos ($6.9 billion). Earnings doubled year-over-year. Stop and think about the numbers for a second. For a $23 billion market cap, you can buy $7 billion in annual profits.

That's a P/E ratio of 3.3x.

Yes, I know there are a lot of cheap energy companies out there lately. But 3x earnings is quite the feat. Especially so when this is a large diversified operation rather than a boom/bust play relying on just production.

The issue, though, is of politics. Last year, Colombia elected a socialist president, Gustavo Petro. He will serve as president until 2026 and is not eligible for re-election as Colombia has a one-term limit for presidents.

Up until Petro, Colombia had consistently voted for conservative presidents during its modern era. The country had developed a reputation for pro-business policies and better-than-average governance when compared to Latin America as a whole.

However, the election of Petro has shaken up foreign investors' perception of the country. Petro campaigned on a message of making Colombia a leader in environmental aims, which runs contrary to some established industries such as mining and energy. And, some of Petro's cabinet picks, such as for mining, have been figures that take a negative view of many extractive resource activities.

This seemingly led to the idea that any and all businesses which have a carbon footprint were going to get crushed by the new government. And, indeed, I would avoid Colombian mining companies for the time being; the current government has taken a very negative view on that front.

However, Ecopetrol is the baby that got thrown out with the bathwater. For one thing, Ecopetrol has a huge array of businesses outside of upstream oil production. Assets such as the pipes, refining, electric grid, toll roads, and renewables all hold their value regardless of the government's view toward giving out new oil production licenses.

And there's the other matter, namely that the government owns 88% of Ecopetrol. Thus, if the government slows down Ecopetrol's ability to produce more oil, then it will reduce the amount of dividends it gets in turn from Ecopetrol. While the government has its idealistic vision for the country, it also has bills to pay, and Ecopetrol is one of the most reliable sources of cash for the treasury.

Long story short, if you are a private sector energy or mining company in Colombia, you're probably going to have a rough go of it until 2026 when there is the next round of elections. However, the state wants dividends and thus Ecopetrol gets to operate under special privilege.

To that point, you may have heard reports that Colombia's oil sector will be cutting its exploration budgets this year. Which is true, but somewhat misleading. Here's the full context from Reuters:

"Colombia’s leftist President Gustavo Petro has set his sights on weaning the Andean country from its dependency on oil exports, blocking new auctions for oil and gas blocks.

Exploration investments, including from state-owned Ecopetrol, more than doubled in 2022 versus the previous year to $1.29 billion, the ACP [Colombian Petroleum Association] said, citing soaring oil prices and a better regulatory environment.

Total exploration investment is forecast to fall just 4% in 2023 to $1.24 billion because Ecopetrol, Colombia’s largest producer, is increasing its investments, the ACP told journalists.

However, the private sector is expected to cut its own exploration investments to between $650 million and $700 million this year - a 33% cut versus 2022 - partly due to a less favorable fiscal environment, the ACP said."

The pertinent fact is that while the private sector is slashing investment 33%, Ecopetrol is actually increasing its investments in oil exploration and development this year. When a government has an anti-resources posture, it's generally much wiser to stick with the government-influenced producers rather than owning the private sector players.

In any case, Ecopetrol is reporting record profits and will be boosting its spending this year to deliver even more production into the favorable market conditions.

So why, again, is EC stock still near multi-year lows?

The Dividend Factor

The Petro government hasn't meaningfully affected Ecopetrol's operations. Profits are up sharply and the company is investing more to continue the positive trajectory in 2023. So what might the skeptics be holding onto at this point?

The final bearish talking point was that the dividend might get slashed. Ecopetrol paid $2.26 per ADR in dividends in 2022. Based on Tuesday's closing price of $11.09, Ecopetrol had a trailing dividend yield of 20.4%.

But, that was under the prior right-wing government. Perhaps the Petro government was going to crash the party and not allow Ecopetrol to pay such a large dividend in 2023. In theory, due to the government being left-wing or anti-business or something, maybe they would ask for the dividend to be reduced or so the thinking went.

The thing is, this never made much sense. Recall from above that the Colombian government owns 88% of Ecopetrol's stock. Thus, 88% of Ecopetrol's dividend goes to the state treasury.

Regardless of all the anti-oil posturing, the Colombian government can use more cash receipts and thus is unlikely to adjust Ecopetrol's dividend policy. The company has long paid around 60% of its net income as dividends. As noted, the company made $7 billion in 2022 -- a record -- and thus should be expected to pay out north of $4 billion of that to shareholders this year.

Tuesday was the moment of truth, though. Would Ecopetrol come through with its usual large dividend?

Yes, the answer was yes it did.

Ecopetrol announced that it will be paying a 593 Colombian Peso dividend per share of Ecopetrol in Colombia for 2023. The dividend will be paid in three parts with payments in April, September, and December.

Each U.S.-listed Ecopetrol ADR equals 20 Colombian shares. So the US ADR dividend will be (20*593) 11,860 Pesos each. The exchange rate is 4,810 as I'm writing this, which means the dividend this year will be 11,860/4,810 or $2.47 per share.

On Tuesday's closing price, that's a 22.3% current dividend yield. That's a pretty fat reward for taking political risk.

And with Tuesday's dividend announcement, that should eliminate the last bearish talking point around Ecopetrol.

President Petro has been in power long enough to have made serious changes if he so wished. Instead, his oil tax reform policy barely affected Ecopetrol's profitability at all, as Tuesday's results showed. Ecopetrol is still drilling for oil despite the anti-fossil fuel rhetoric. Profits are up. And the company just boosted its dividend from $2.26 last year to $2.47 this year.

At this rate, investors will get most of their capital back just over the next few years thanks to the outsized dividends. And remember Ecopetrol was a $24 stock in 2018 and a $60 stock back in 2013 the last time crude oil prices were as high as they are now. Ecopetrol is still trading at a fire sale price even as most other oil equities have rebounded sharply from their pandemic lows.

Given the bad political optics, we won't see Ecopetrol shares trading at new highs anytime soon.

But it wouldn't be too shocking if the stock doubled off this low point. At $22, shares would be going for a 6.6x P/E and an 11% dividend yield. That seems like a reasonable price and yield to account for Colombian political risk. But at $11, the odds are dramatically in favor of the bulls. The dividend announcement was the last piece of the puzzle, and it just snapped into place on Tuesday.

For further details see:

Ecopetrol Is A Steal At 3.3x Earnings With 22% Dividend Yield