EC - Ecopetrol: Oil Stock For Adventurous Dividend Seekers

2023-10-27 10:16:09 ET

Summary

- Ecopetrol is an excellent alternative to US oil majors. The company owns assets in the Caribbean and Pacific shelf.

- Since the oil crash in March 2020, the company has recovered its profitability while maintaining balanced leverage. EC pays dividends with solid yield, too.

- Companies extracting fossil fuels in the Latin American region will become more attractive to investors. The continent has been the most peaceful for over a century, with zero interstate wars.

- Ecopetrol distributes dividends with a respectable yield of 7.85% while maintaining EV/EBITDA at 3.3. Given both indicators, it is one of the top five enterprises in the region.

Introduction

One of South America's primary oil majors is Ecopetrol (EC). The company has robust finances, growing profitability, and an expanding reserve base. It pays dividends with generous yields and is cheap using percentile ranking and EV/EBITDA vs dividend yield.

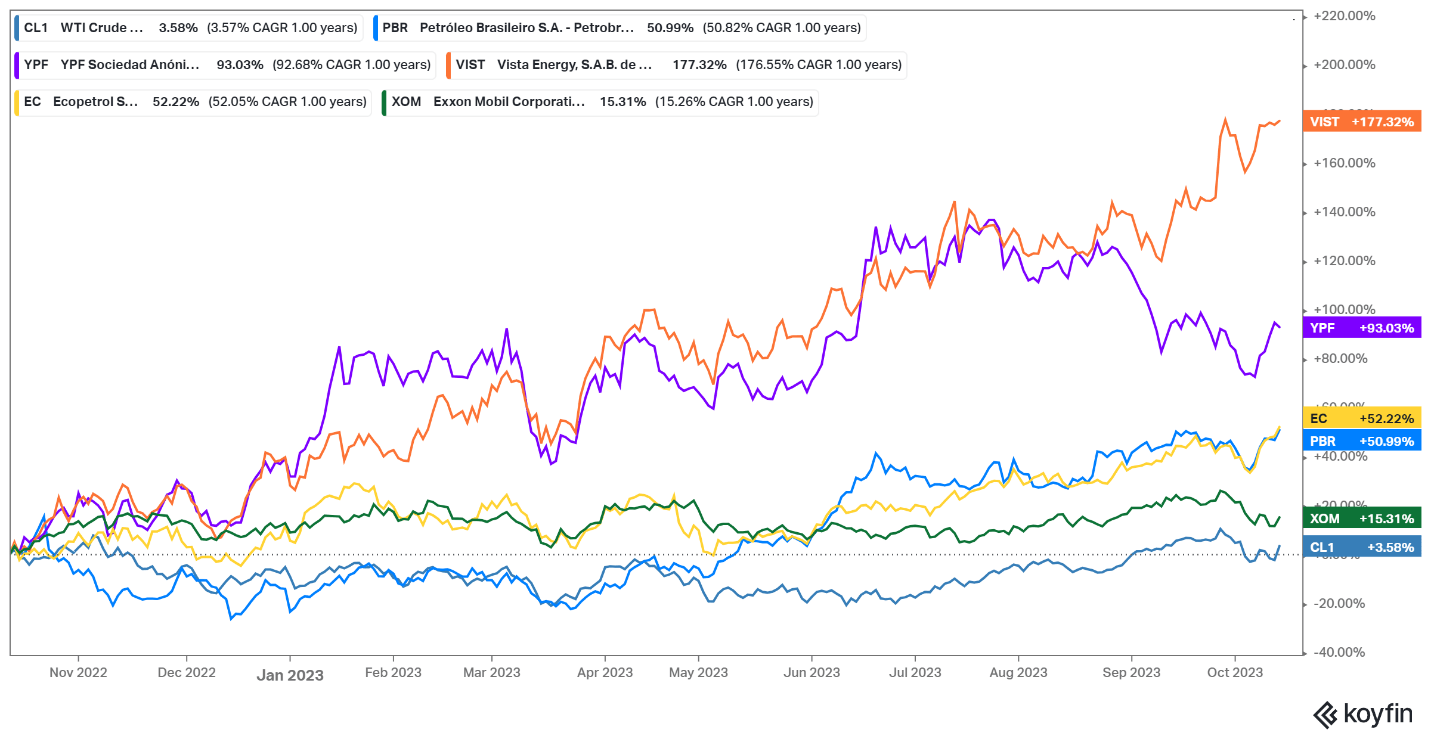

The most prominent players in South America are Petrobras (PBR), YPF (YPF), Vista Energy (VIST), and Ecopetrol. The chart below compares their share's performance against WTI and Exxon Mobile (XOM).

{kind=link}

The Latin American companies have achieved impressive returns led by VIST and YPF with triple-digit ROI. PBR and EC follow with a respectable 50% ROI. The laggard is XOM. It's worth mentioning that the WTI price moved by 3.58% YoY while South American oil and gas producers gained exceptional returns.

In two years, I expect the crude price to reach new highs above $150/barrel due to growing global disorder, declining production in the US shale basins, and lack of investments in new projects. US administration consumed SPR (strategic petroleum reserve) and partially lifted the sanctions on Venezuela as safety valves to maintain crude prices below $100/barrel. However, they cannot suppress the price in the long term. Investing in integrated companies such as EC is a great way to play that thesis while collecting dividends with solid yields.

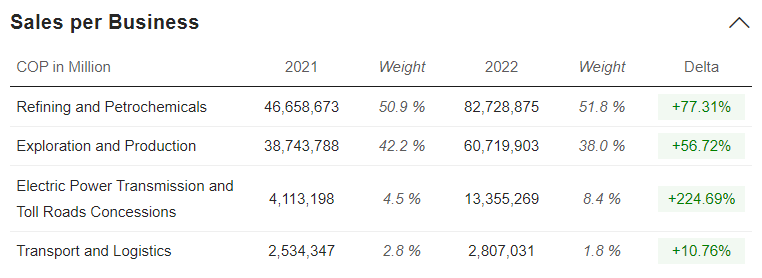

What does the company do?

Ecopetrol S.A. operations are spread across exploration and production, refined products and petrochemicals, renewable energy and biofuels, electric power transmission, and toll road concessions.

{kind=link}

Ecopetrol had over 9,127 kilometers of crude oil and multipurpose pipelines as of December 31, 2022. Additionally, it manufactures and markets masterbatches, polypropylene resins, and compounds and sells industrial and specialized management services.

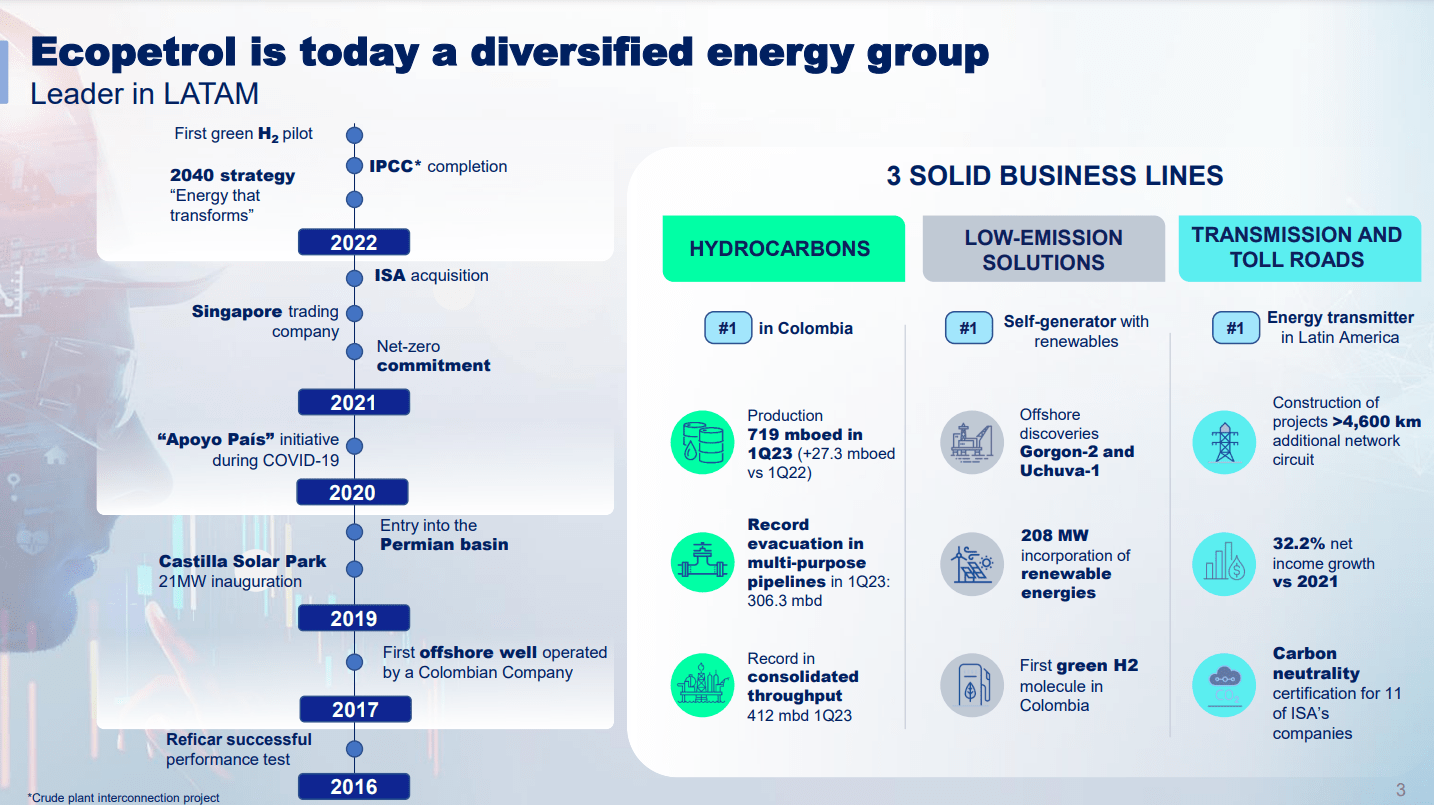

The company conducts business in South America, Asia, Central America, the Caribbean, Europe, and Colombia. The chart below from the last EC presentation details the three main pillars of Ecopetrol operations.

{kind=link}

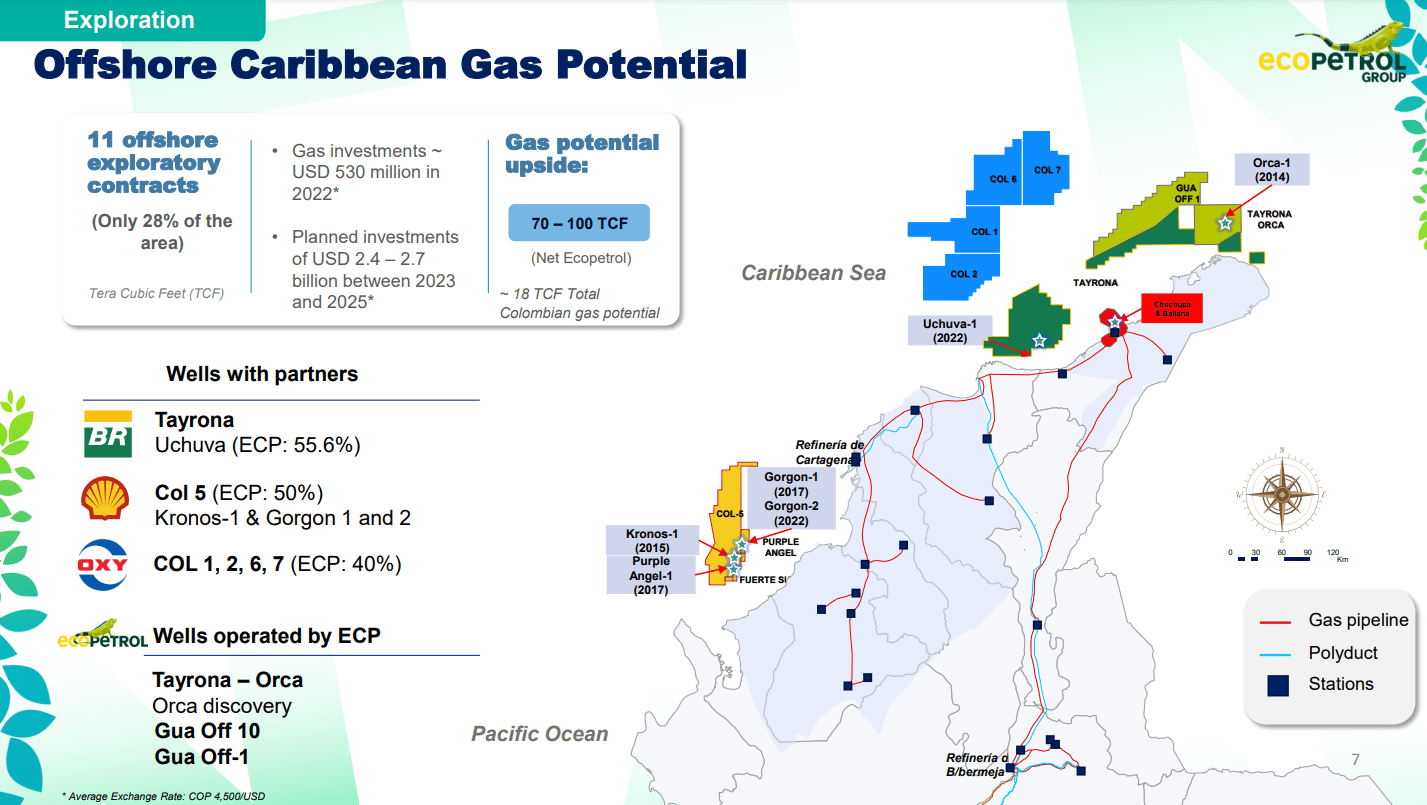

Colombia has exposure on the two sides of the Panama Canal: the Caribbean Sea and the Pacific Ocean. The former is vital for fossil fuel discoveries because it shares borders with Venezuela, the global leader in oil reserves. On the other hand, the Pacific shelf of the country carries significant potential, too.

The map below shows the Caribbean basin's colossal exploration potential .

{kind=link}

The blue squares indicate assets developed with Occidental Petroleum. EC has a 40% interest in the project. Gorgon 2 (yellow blocks) is one of the most significant discoveries on the Columbian shelf. EC owns 50%, and Shell will develop the project. Gorgon 2 is a deep-water discovery and is considered the largest in Colombia. Another notable asset is Uchuva (green blocks), created with Petrobras. Those discoveries illustrate Colombian oil and gas deep-water potential.

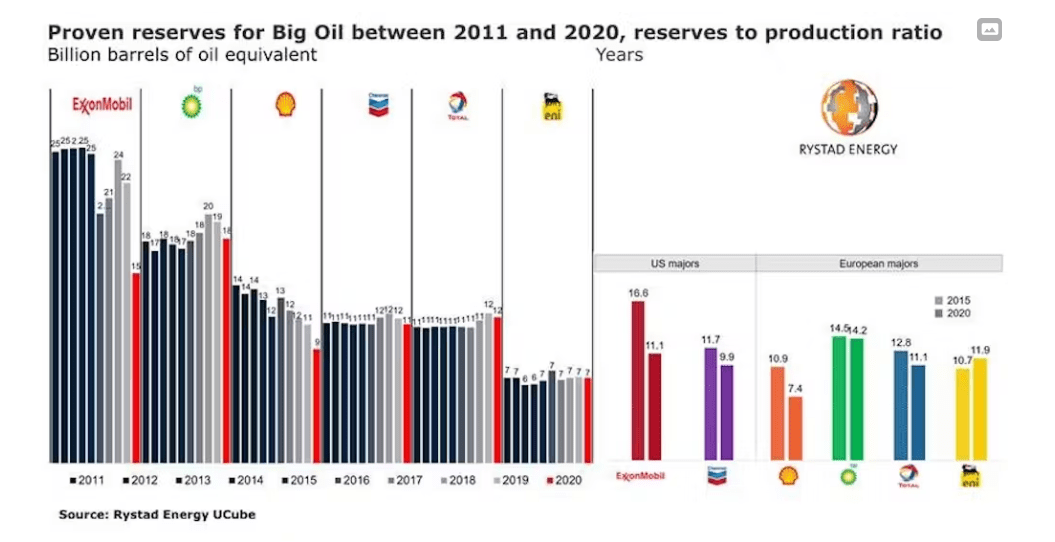

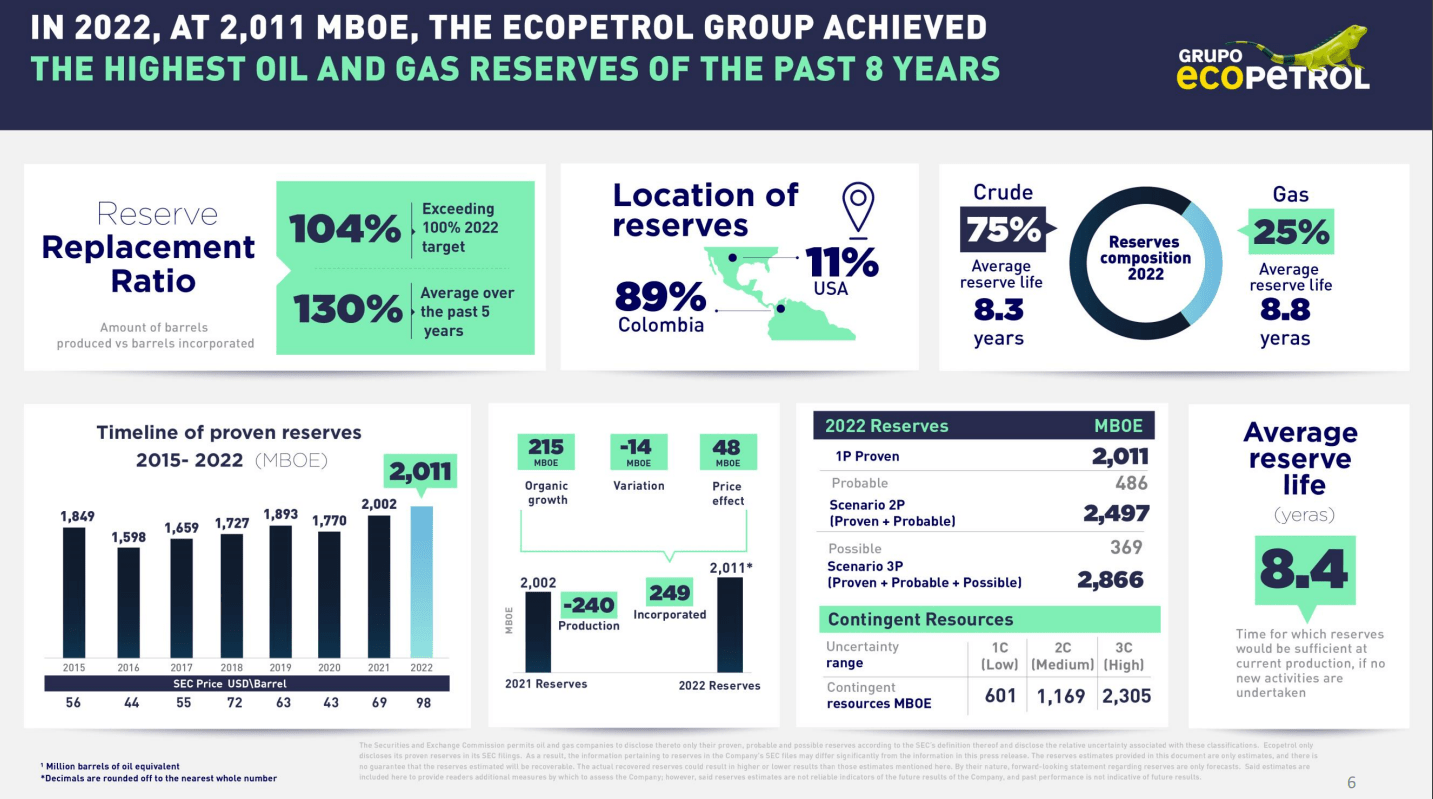

Replacing its reserves faster than depleting them is a matter of survival for any extractive business. EC maintains a solid replacement ratio of 130% over five years. The proven reserves have grown constantly since 2016, though the reserve-to-production ratio is 8.4 years. Petrobras has 12.2 years for comparison.

The reserve-to-production ratio has declined in the last few years among all majors. The chart below from Rystad Energy shows the downward trend in US and European oil majors.

{kind=link}

Considering the potential for another significant deepwater discovery, I expect EC reserves to grow, improving the reserve-to-production ratio.

The chart below gives details on EC assets.

{kind=link}

Balance sheet and profitability

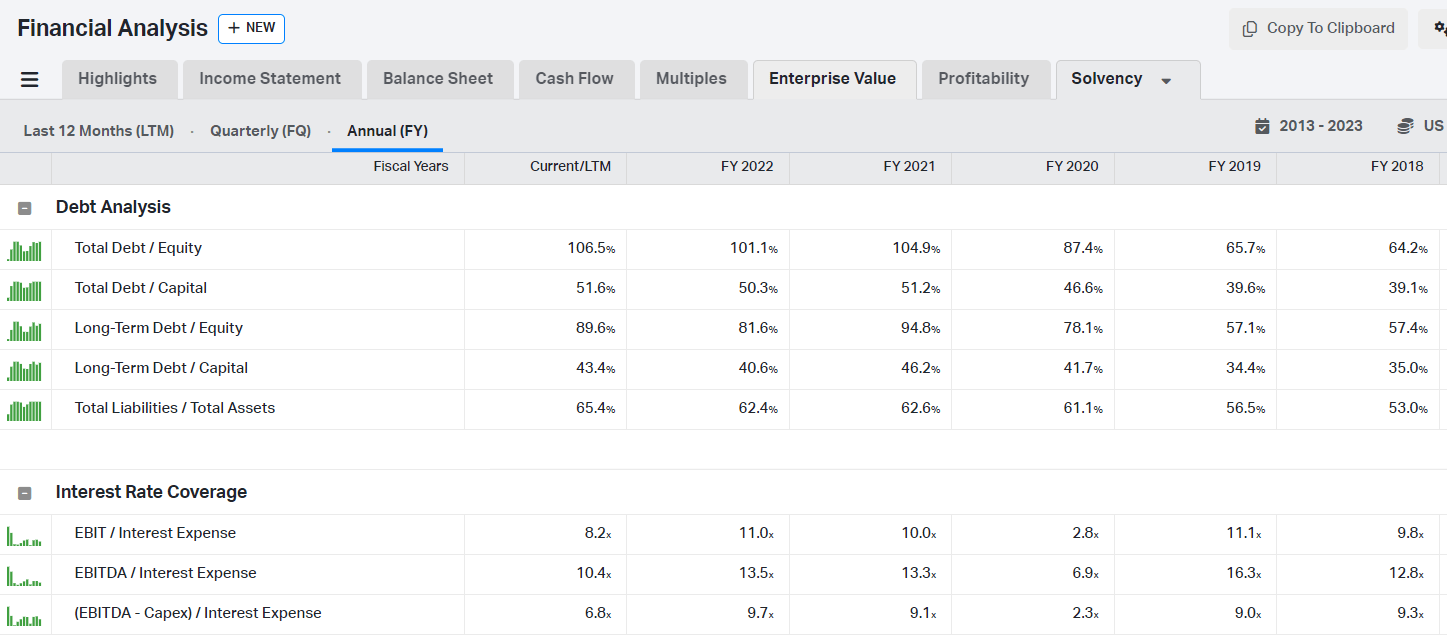

The oil majors have improved their balance sheets since the 2020 crash. Although EC did not significantly cut its liabilities, the company maintains moderate debt levels. The table below shows the company`s debt/equity multiples and interest rate coverage.

{kind=link}

Total Debt/Equity at 106.5% is far from overleveraged. The excellent interest rate coverage provides EC with a significant buffer against declining oil prices and liquidity issues.

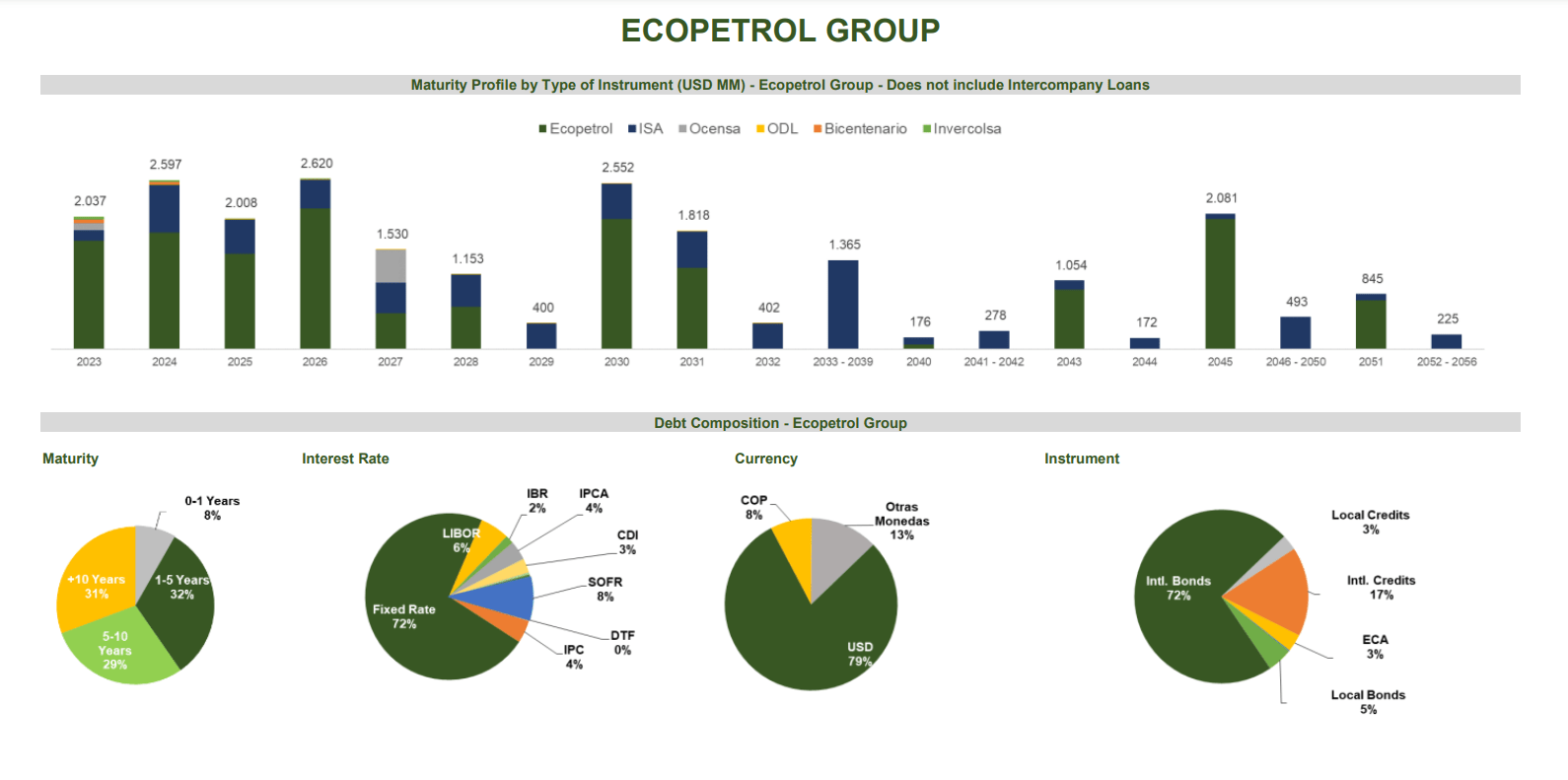

The company holds $2.7 billion of cash reserves, while the current portion of its long-term debt is $3.89 billion. Ecopetrol's total debt is $25.89 billion. The table below from EC debt preview shows the company's debt profile.

{kind=link}

The top part of the chart gives the maturity dates and the amount of debt. 72% of the company`s debt has a fixed interest rate between 4-9%. International corporate bonds comprise 72% of Ecopetrol's debt. The maturities are well diversified across durations. In the coming four years, the company must repay $9.12 billion: $2.07 billion in 2023, $2.59 billion in 2024, $2.02 billion in 2025, and $2.62 billion in 2026.

The company has enough cash on hand to cover the current portion of the debt. Besides that, it realized $4.46 billion in free cash flow ((TTM)). Even at the current oil prices, Ecopetrol generates excess cash flows sufficient to cover its debt obligations.

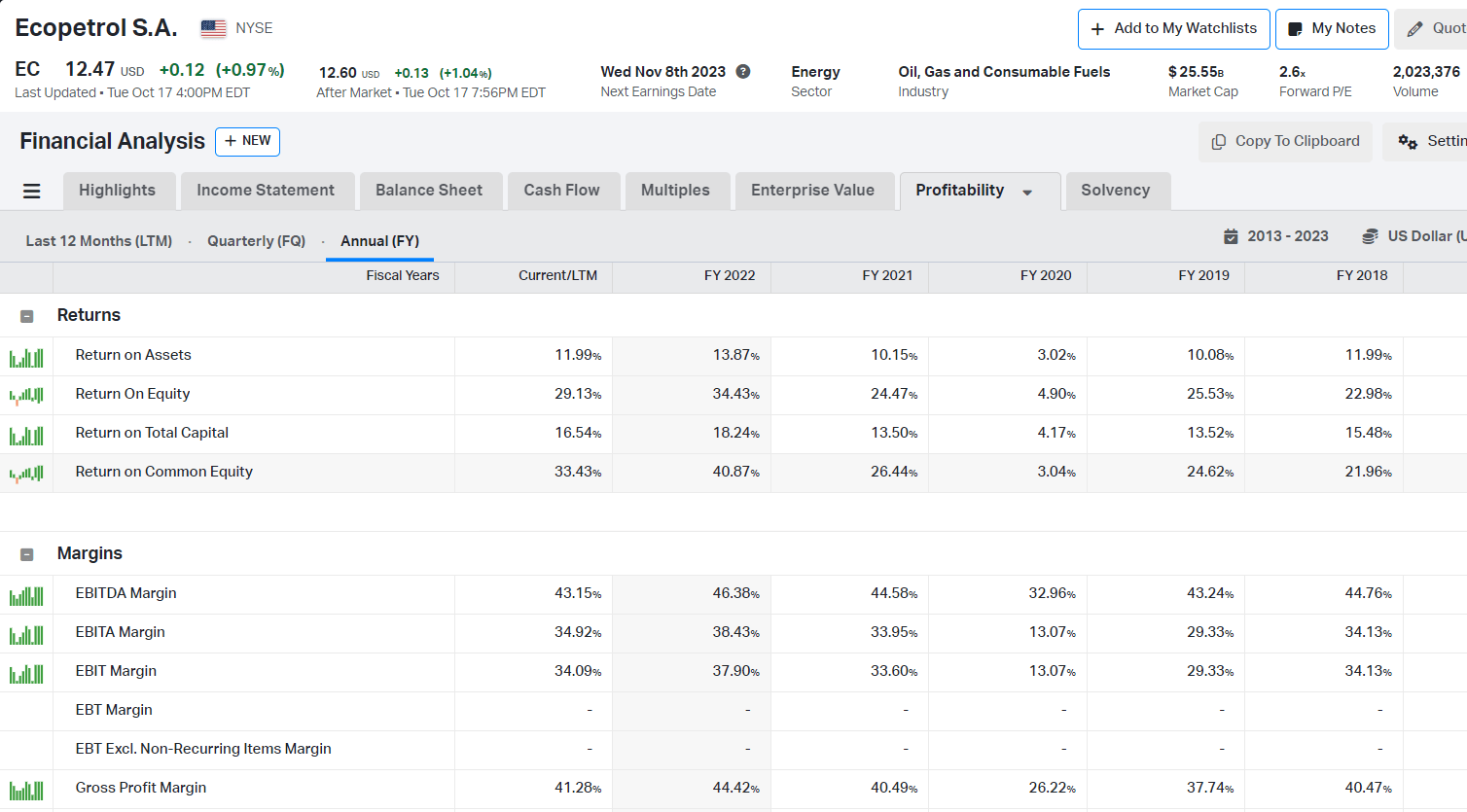

The company's profitability remains stable, as seen in the graph below. Even in 2020, a challenging year globally, the company had positive returns.

{kind=link}

Since then, the EBITDA margin has remained above 40%, and the Return on Total Capital is above 12%.

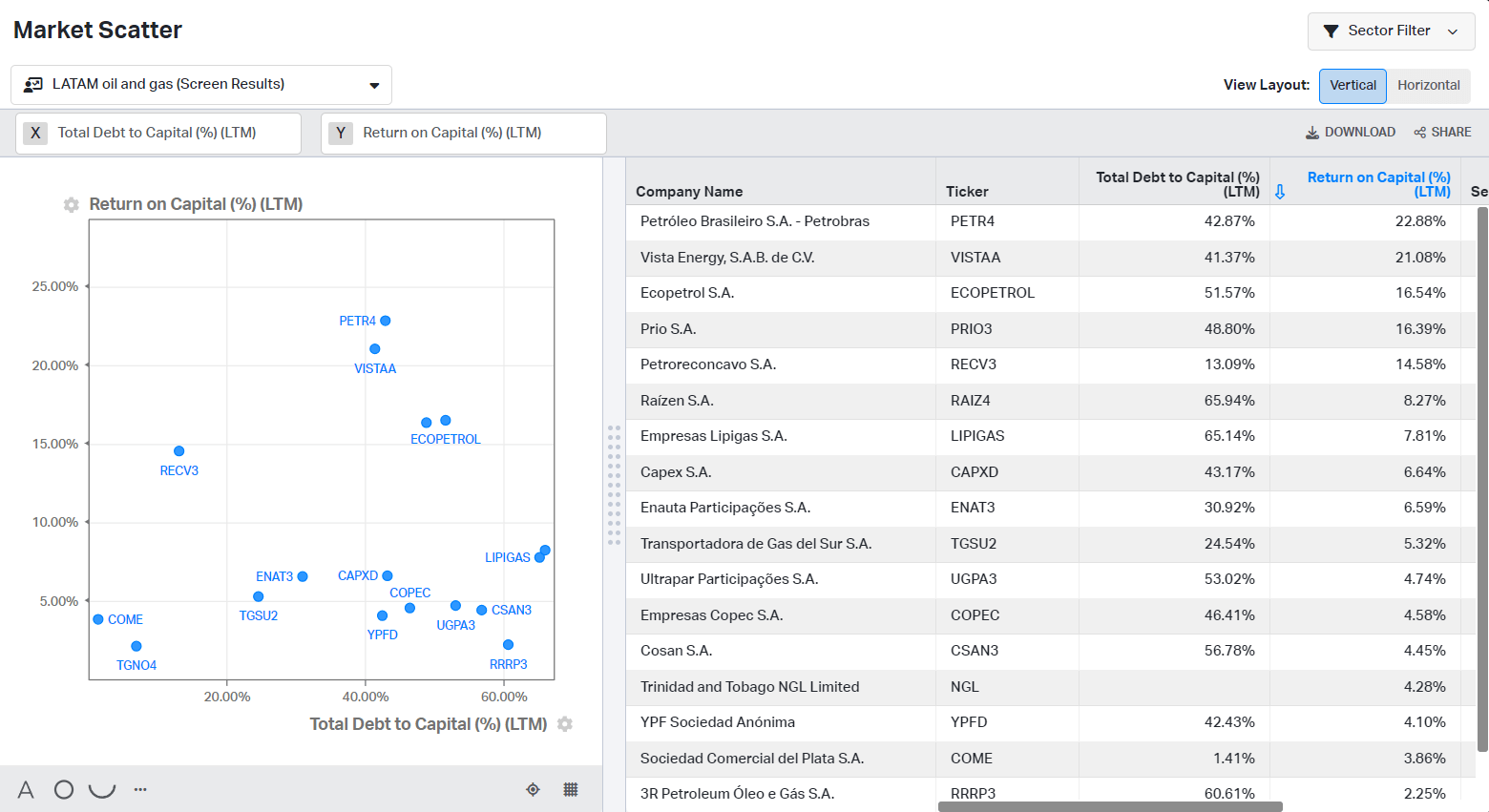

The graph below shows the Total Debt to Capital axis and the Y axis of Return on Capital. The blue dots represent oil and gas producers from South America.

{kind=link}

EC is third next to Petrobras and Vista Energy, with ROIC at 16.54% and debt-to-capital level at 51.57%. The company achieves strong returns without being over-leveraged.

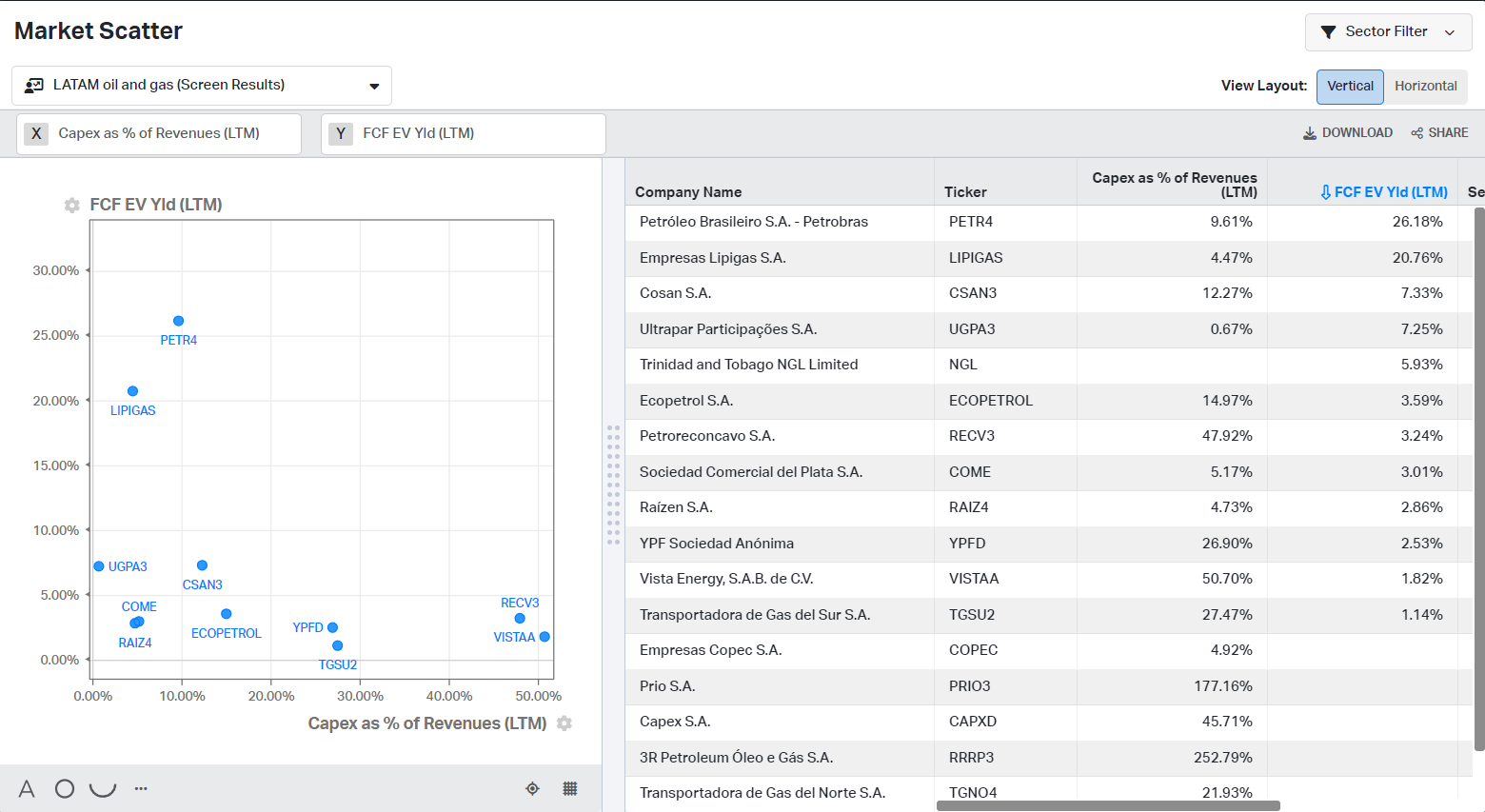

Similarly, I analyze FCF% and CAPEX as % of Revenue.

{kind=link}

EC realized a 3.57% FCF yield and 14.97% CAPEX as a percentage of Revenue. Petrobras again leads the group with a 36.18% FCF yield but 9.61% capital investments to revenue. Looking at the big picture, EC is a strong performer in the top percentile of South American oil and gas producers. The same could be said about the leverage; the company maintains a safe level of debt.

Valuation

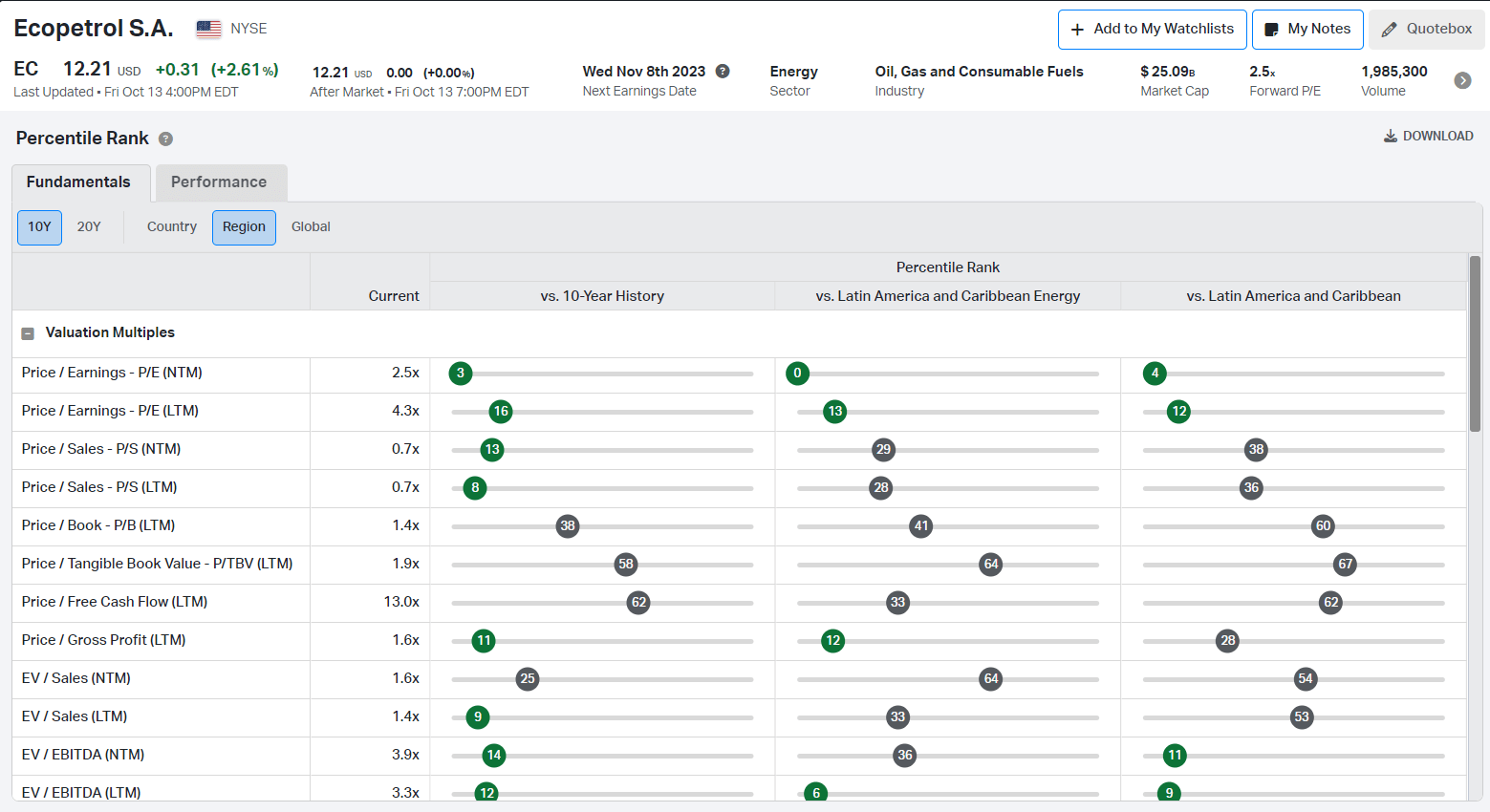

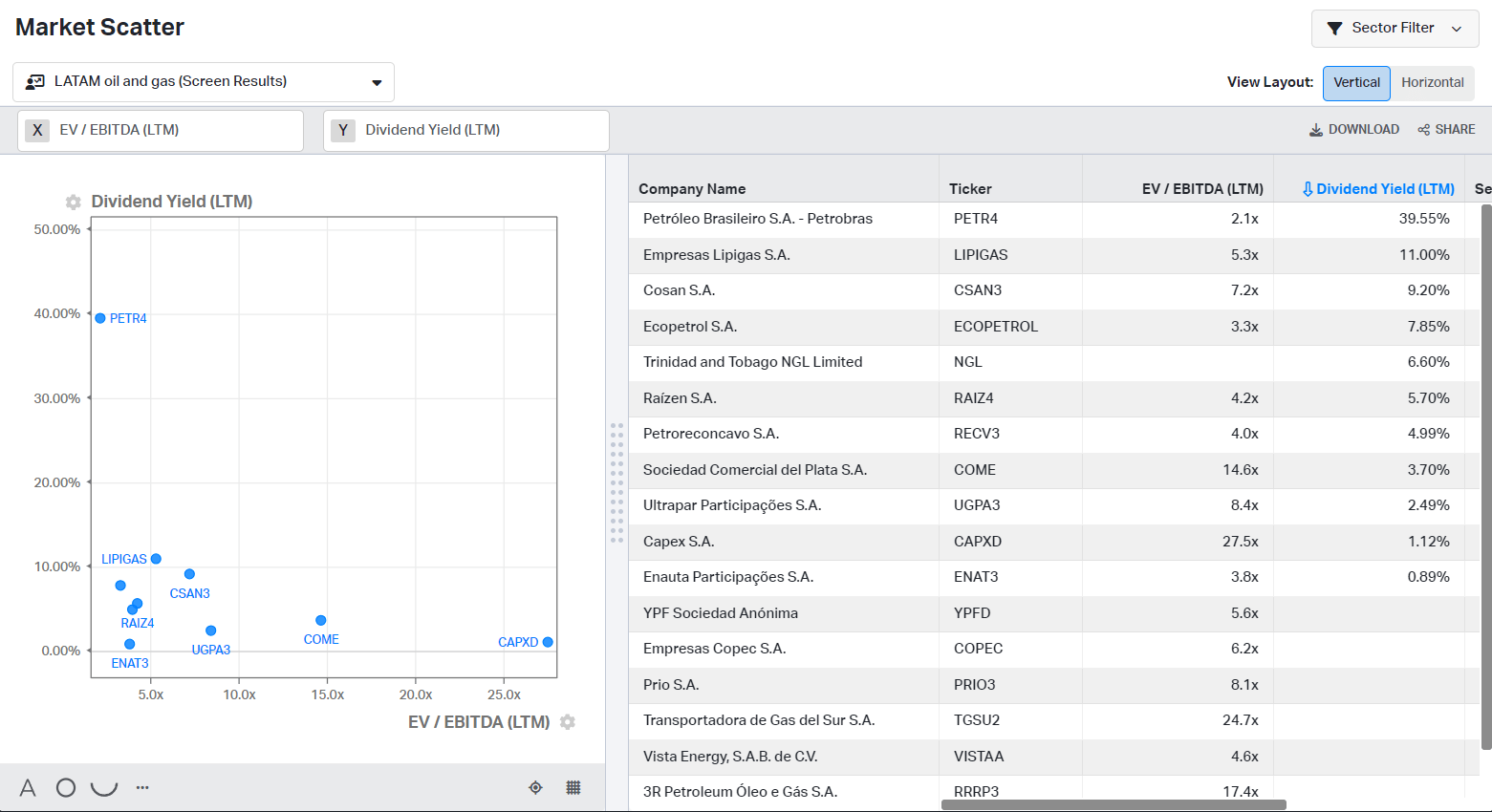

I use comparative valuation to estimate Ecopetrol's standing. I prefer EV/Sales and EV/EBITDA multiples. The chart below compares EC multiples with the company`s ten-year average and South American oil and gas industry figures.

{kind=link}

EV/Sales ((NTM)) is lower than 36% of the energy companies in South America while is significantly lower (75%) than Ecopetrol`s ten-year average. Based on EV/EBITDA ((NTM)) the company is even cheaper than 64% of its regional peers and its ten-year average.

Ecopetrol distributes dividends with a respectable yield of 7.85% while maintaining EV/EBITDA at 3.3. Given both indicators, it is one of the top five enterprises in the region.

{kind=link}

Based on the data discussed, the company is still cheap. Great company and reasonable price is not enough. The missing element is the timing.

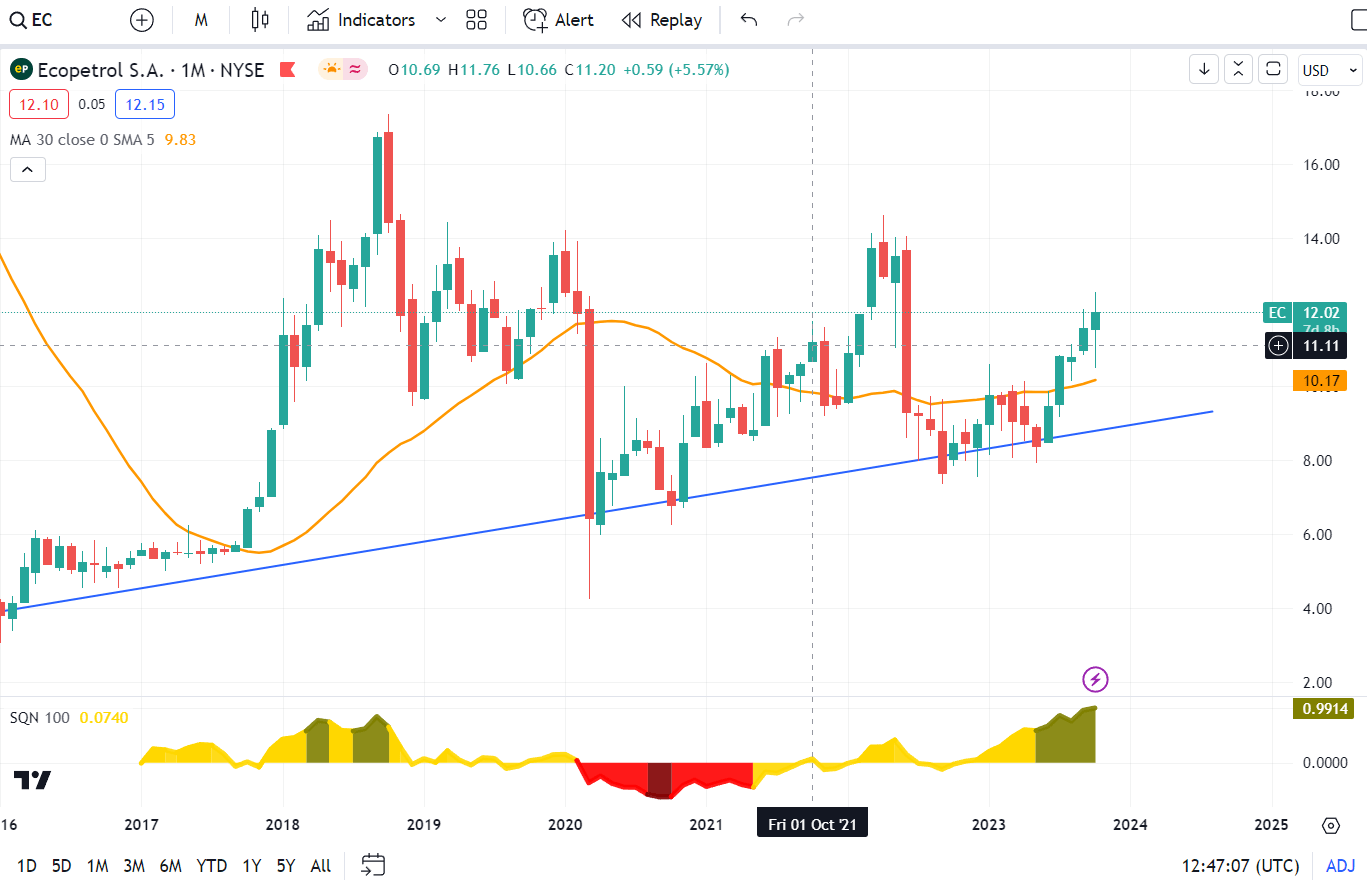

Price Action

Ecopetrol price action offers an excellent entry point. The SQN indicator is in a bull quiet regime, while the price is above the 30 monthly moving average ((MMA)) and rebounded from a notable support level.

{kind=link}

The markets peak in a bull volatile regime, while entries in the bull quote (green) and neutral (yellow) the odds are skewed in investors' favor. That does not mean a zero-fail rate of the SQN signals; SQN is a tool that increases signal reliability when combined with other analytical methods (macro, fundamental, narrative).

I want to point out something about the trendlines, too. The steeper the line, the less reliable it is as support/resistance. Steep trendlines tend to morph into other chart patterns while giving a lot of false breakout signals. The lowest signal fail rate holds multiyear horizontal trendlines. The blue line is not steep and has been notable support for eight years. Simply put, it could be a credible tool to assess the price action.

The price is above 30MMA, increasing the risk-reward ratio. Putting all together, EC price action affirms my thesis and provides an entry point with asymmetric risk reward.

Risks

Crude oil is the true blood of the economy. Its price depends not only on economic fluctuations but also on geopolitical tensions. The turmoil in the Middle East is another confirmation.

The turmoil in Europe and the Levant benefited South American oil companies. It will push investors and consumers to seek safer alternatives to Middle East oil, such as South America. The former produces more than 30.7 million barrels daily while the latter less than 7.8 million. If 5% of Middle East productions move to South America, the demand in the region will increase by 20%.

Companies extracting fossil fuels in the Latin American region will become more attractive to investors. The continent has been the most peaceful for over a century, with zero interstate hot wars. On the other hand, there have been countless interstate conflicts in Africa, the Middle East, and Eastern Europe (Caucasus region included) for the last 30 years.

Operating in a peaceful region is crucial for complex endeavors such as mining and oil/gas extractions. Those industries depend heavily on global logistics for spare parts, personnel, and shipping. The internal troubles inherent to the region, such as corruption, inequality, and inflation, are less adverse than geopolitical tensions for natural resource companies.

A global recession might affect oil demand, but there will be a brief demand squeeze. Commodities such as copper are more sensitive to economic cycles. Copper demand rises considerably in a growing economy and declines in poor economic conditions. Oil demand shows a higher degree of indifference during economic recessions. Oil prices suffer abrupt declines yet quickly recover.

As with every commodity, oil prices are dictated by the CAPEX cycle in the long term. So, it affects the supply. While demand projections are daunting, the supply depends on relativity known variables like costs and time to develop a new project. Of course, they vary, but ultimately, they rely on three inputs: capital, resources, and labor.

The most prominent risk is the Government of Columbia, which owns 88% of the company and is the largest shareholder. Colombia is one of the countries in the region with the best economic metrics , such as growing foreign direct investments, government debt to GDP at 55%, and total private debt to GDP at 106%. The incumbent president is the left-wing Gustavo Petro. His election is part of the "pink tide" in the continent that started with Chavez in Venezuela and has spread to different degrees in the region. Almost all incumbent presidents in South America are from left-wing parties. Besides, we have positive examples of Brazilian President Lula's pragmatic economic policies. Gustavo Petro tries to emulate Lula`s approach.

Lifting the sanctions on Venezuela's oil will act as a safety valve and suppress the oil prices in the short term. However, I believe this will have a temporary effect. The fundamentals are lined up for a long-term bull run in crude.

Investors takeaways

Oil and Gas stocks can potentially become the new darlings of the investors. They distribute dividends, offer asymmetry, and benefit from geopolitical turmoil. Ecopetrol is an alternative to the usual suspects Occidental, Shell, BP, and Conoco. The company has the advantage of operating in Colombia. The conflict in the Middle East will push the global oil demand, especially in safer regions such as South America.

Since the oil crash in March 2020, the company has recovered its profitability while maintaining adequate leverage. The company has enough cash on hand to cover the current portion of the debt. Besides that, it realized $4.46 billion in free cash flow ((TTM)). Even at the current oil prices, Ecopetrol generates excess cash flows sufficient to cover its debt obligations. The company distributes dividends with a respectable yield of 7.85 % while maintaining EV/EBITDA at 3.3. Given both indicators, it is one of South America's top five oil companies. Ecopetrol is a solid oil company for adventurous dividend seekers deserving a buy rating.

For further details see:

Ecopetrol: Oil Stock For Adventurous Dividend Seekers