EC - Ecopetrol: Still My Top Pick For Oil Stock

2024-01-18 20:08:28 ET

Summary

- The Middle East crisis has multidimensional consequences, affecting supply chains, oil production, and transport. EC operates in Latin America, the region with the lowest geopolitical risk and abundant oil reserves.

- EC issued $1.85 billion in bonds at the beginning of the year. The bonds have an 8.45% yield and will mature in 2036.

- The company pays dividends with impressive yields while maintaining a payout ratio below 30%.

- EC trades at low multiples compared to its local competitors (except PBR) and Global Energy stocks. The price is on the verge of breaking above significant resistance.

Introduction

One of my favorite oil stocks is Ecopetrol ( EC ). Today is my follow-up digging into the company's 3Q23 results and geopolitical tailwinds for Latin American oil producers. EC scored record figures in its last quarter across all segments. EC refinanced its 2025 notes with new bonds issued with 20236 maturities. The company has lower margins than its major competitor in the region, Petrobras ( PBR ). However, EC pays dividends with impressive yields while maintaining a payout ratio below 30%.

The world moves toward disorder and fragmentation. The events from the last few days confirm this view. The Middle East crisis has multidimensional consequences, affecting supply chains, oil production, and transport. EC operates in Latin America, the region with the lowest geopolitical risk and abundant oil reserves.

EC trades at low multiples compared to its local competitors (except PBR) and Global Energy stocks. The price is on the verge of breaking above significant resistance. I have been long EC for more than 12 months. A confirmed breakout is a signal to add more size. However, for the newcomers, the present stock price provides an opportunity to start building a position. I give EC a strong buy rating.

3Q23 overview

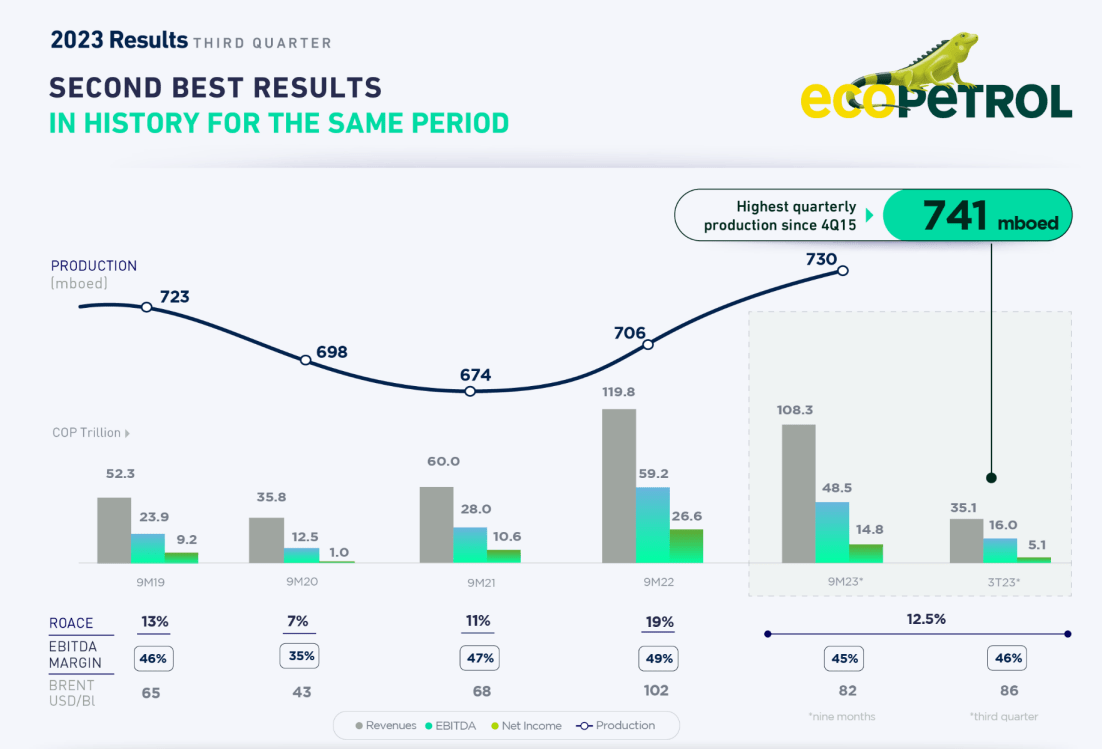

The third quarter of last year was the second-best in the company`s history. The chart below from the 3Q23 presentation shows some highlights.

{kind=link}

In 3Q23, EC had a record-high CAPEX at COP 19.2 trillion for 9M23. 3Q232 revenue reached COP 35.1 trillion, net income COP 5.1 trillion, and EBITDA COP 16 trillion. EC achieved substantial EBITDA margin at 46% and 12.5% ROACE. EC achieved 741 mboed average production per day in 3Q23. The production growth was observed across all assets: Cano Sur and Rubiales in Colombia and Permian Basin operations. In 3Q23, EC transported 1,127 mbd, or 52 mbd higher, compared to 3Q22. EC refining segment delivered 410 mpd and a gross margin of $20.6/Bl. This figure is one of the highest in the company’s history. In 3Q22, EC delivered 395 mpd and a gross margin of $20.3/Bl.

{kind=link}

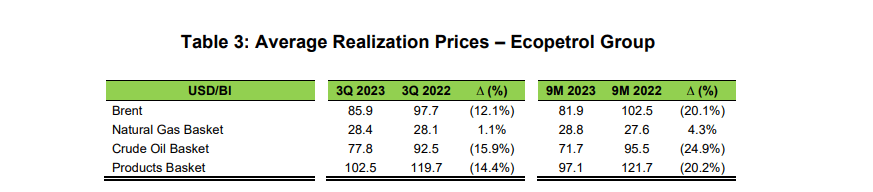

3Q23 EC realized a lower oil basket price, decreasing from $92.5/Bl to $77.8/Bl compared to 3Q22. However, compared to the 2Q23, realization prices have improved due to constrained oil supply from Canada and higher oil quality compared to Mexican Gulf competitors. The refined product's price dropped from $119.7/Bl in 3Q22 to $102.5/Bl in 3Q23. The main reason is the decreasing Brent price and diesel and jet fuel prices . Nat gas basket price improved by 1.0% YoY.

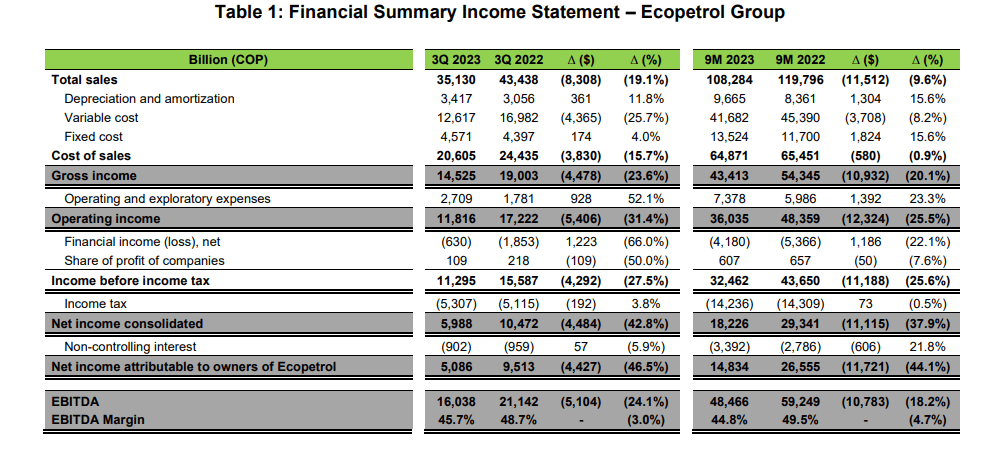

YoY cost of sales declined by 15.7% and by 0.9% QoQ. The factors reducing the expenses were as follows: lower purchase price, improved exchange rate, higher purchase volumes, and erratic inventories.

Fixed costs grew by 4% YoY in 3Q23. Besides that, they increased by 15.6% in 9M23 vs. 9M22. Inflationary pressure was the primary driver behind increased fixed costs. Higher labor costs, higher maintenance costs, and higher input materials costs drove the increase.

EC revenues in 3Q23 declined by 19.1% YoY. The primary reason was the lower realized price of crude oil and petrol products due to a lower Brent benchmark price. Besides that, the middle distillates vs Brent spread shrunk, resulting in lower margins. COP vs. USD rate decline additionally shrunk the profits by COP 0.4 trillion. Cartagena Refinery's increased output partially offset the impact of those mentioned above.

{kind=link}

Colombian sales decreased by 3% YoY. The decline was across all segments: gasoline demand dropped due to higher prices and available inventories; gas sales shrunk due to lower demand from the industrial sector. International sales, which account for 54% of the company`s revenue, grew by 2.6% YoY. The primary driver was higher product exports, increasing by 21.5% YoY. Cartagena refinery was the main contributor to achieving higher capacity than 2Q23. Nat gas sales increased by 55% due to a successful exploratory campaign in the Permian Basin. Oil exports to Asia dropped and partially offset the increased profits.

2024 budget

On December 1, 2023, EC announced its investment budget of COP23-27 trillion following the company`s “Transforming Energy strategy”. Investments in E&P are planned at COP19 trillion, accounting for more than 50% of the planned investments. The goal is to achieve production levels of 725-735,000 boed, figures close to 3Q23 record figures. The focus is to expand the reserve base. The company will drill 360 development wells, 74% in Colombia and 26% in the Permian Basin. EC plans to drill 15 exploration wells in Colombia and the Caribbean basin.

Refining investments account for 7% of the total CAPEX. Cartagena and Barracabermeja refineries are expected to deliver 420-430 mpd, 10-20 mpd higher compared to 3Q23 results. The mid-stream segment accounts for 5% of investments. The focus is improving the integrity and reliability of the transportation infrastructure. The expected rate is above 1,000 mbd, in line with the last quarter's figures.

EC projects a 38% EBITDA margin and 9% ROACE at a $75/Bl Brent price. This means the company remains profitable at lower Brent prices. I am bullish on oil and expect Brent to fluctuate between $85-$100/Bl in the next 12 months. This means the EC will have another strong year. EC trades at low multiples compared even to Latin American oil producers. A solid 1Q24 and 2Q24 performance would attract more investors and push EC's valuation multiples higher.

EC financials

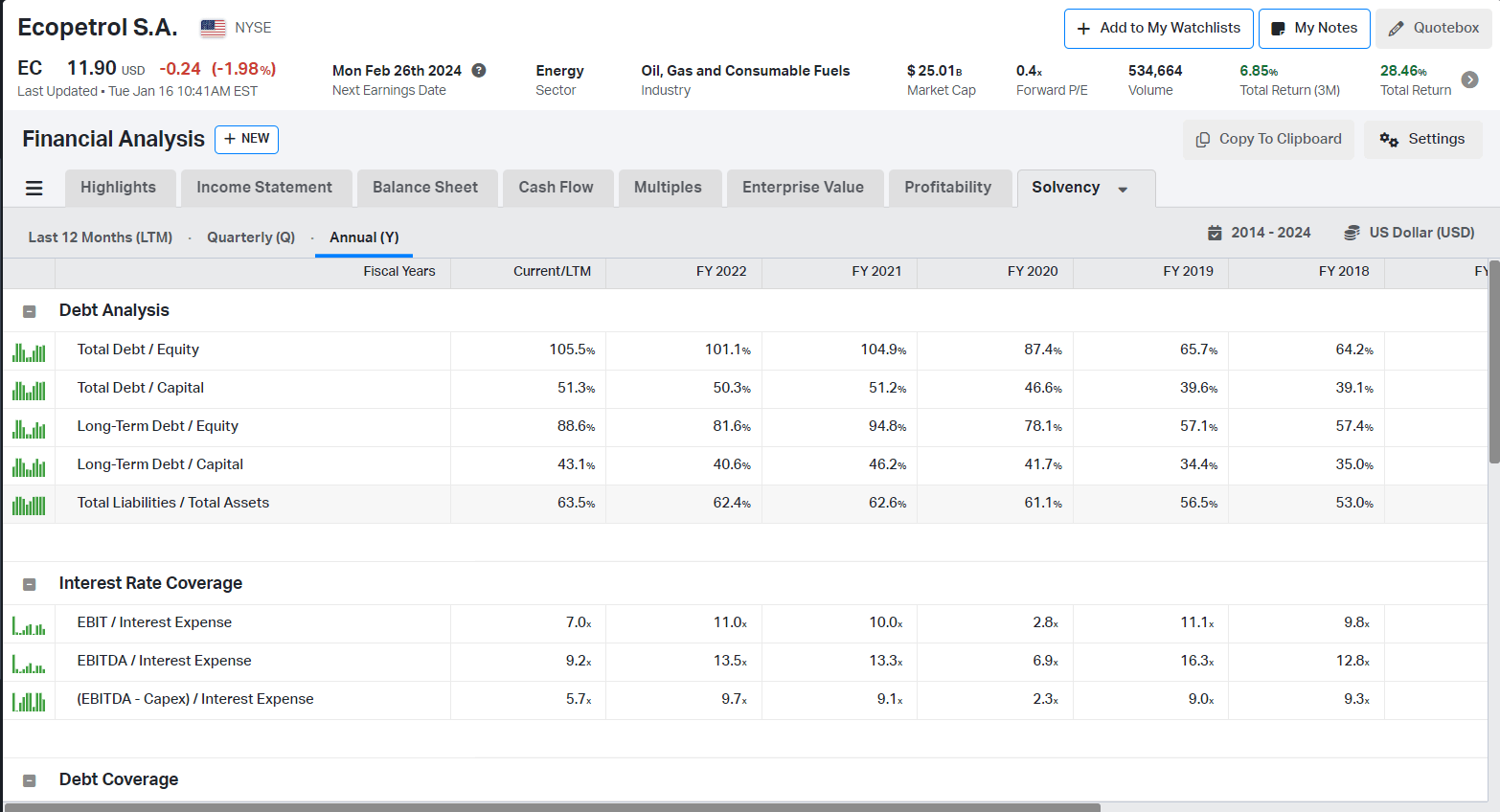

EC has an adequate balance sheet with $3.3 billion cash, $26.9 billion long-term debt, and $22.3 billion total debt. The table below shows how the company`s solvency and liquidity developed over the last five years.

{kind=link}

Over the years, EC has not increased its leverage but has not reduced its debts. EC is profitable at the current oil prices, resulting in ample liquidity far exceeding net interest expenses ($1.26 B). EC realized $11.7 billion operating income LTM and $5.08 billion operating cash flow LTM. EC issued $1.85 billion in bonds at the beginning of the year. The bonds have an 8.45% yield and will mature in 2036. The proceeds will repurchase $1.2 billion of outstanding notes in 2025.

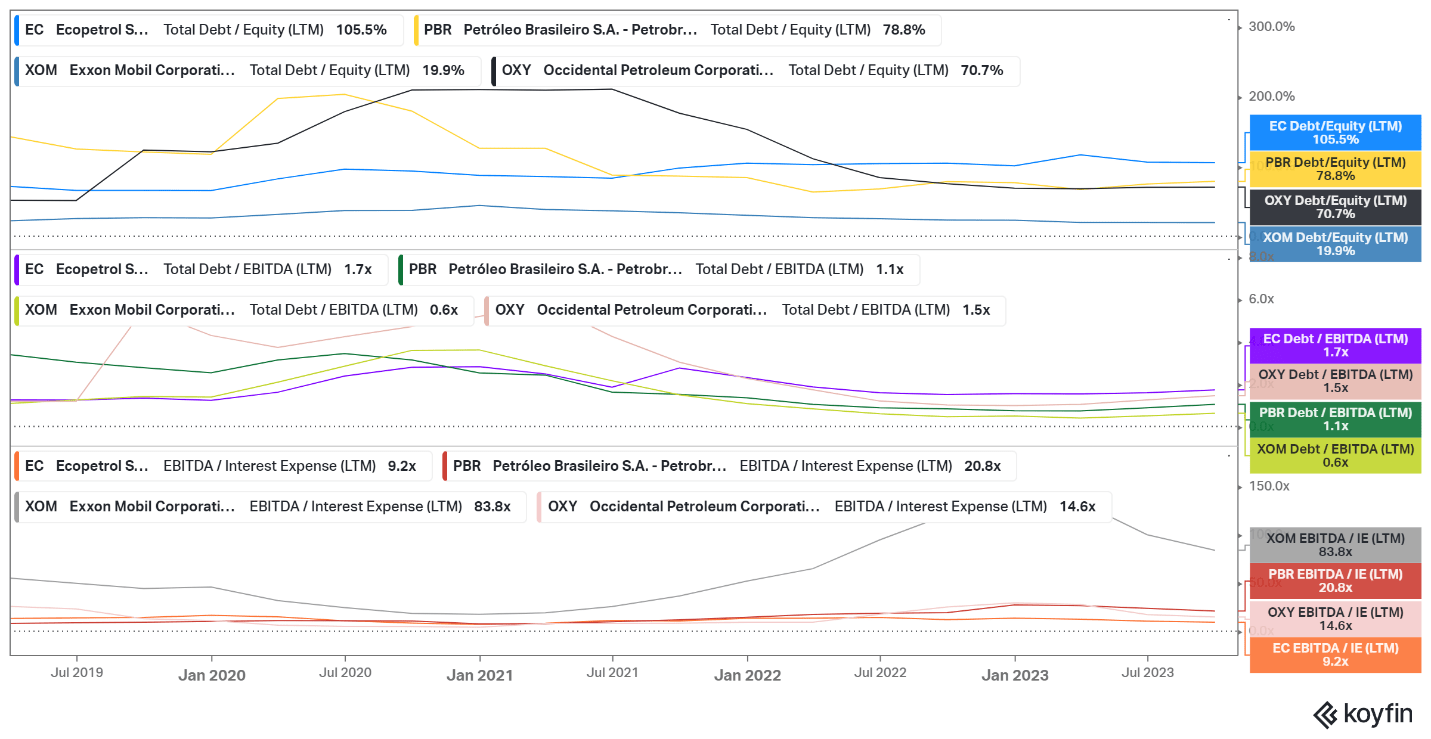

The table below compares EC with Petrobras, Occidental ( OXY ), and Exxon ( XOM ).

{kind=link}

EC scores poorly compared to its peers, with 1.7 Total Debt to EBITDA, 105% Total debt to equity, and 9.2 EBITDA to Interest expenses. PBR and OXY reduced their debt levels significantly since 2020. Despite that, I am still satisfied with EC's solvency. In the long term, I would appreciate management's effort in improving the company`s capital structure.

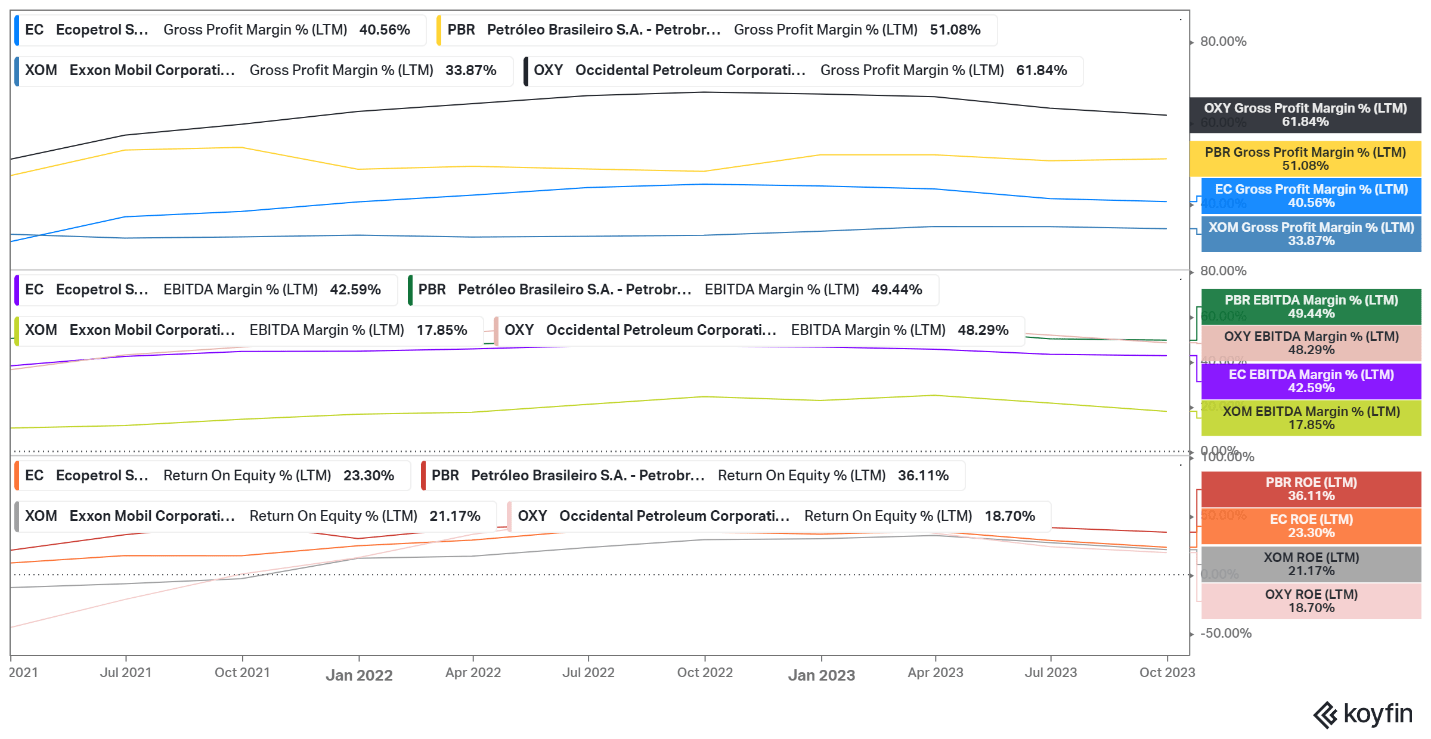

Looking at profitability, EC performs well; however, it is not the best in the sample group. EC delivers 40% gross margin, 42% EBITDA margin, and 23.3% ROE.

{kind=link}

OXY scores the highest gross margin. PBR holds the pole position with an EBITDA Margin and 36.1% ROE.

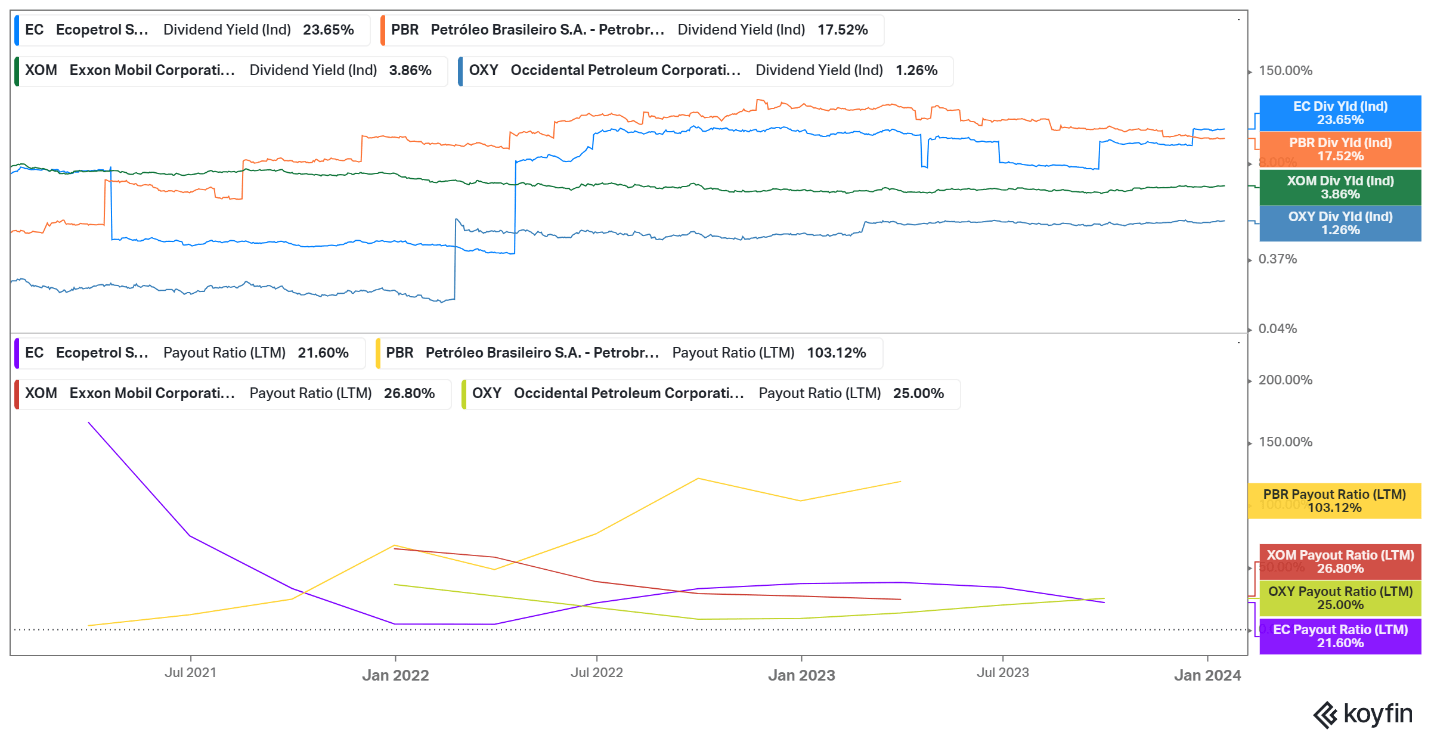

Now, we move to my favorite part: dividends.

{kind=link}

EC combines the highest yield (indicated 23.6%) and lowest payout ratio (21%). PBR maintains a 103% payout ratio.

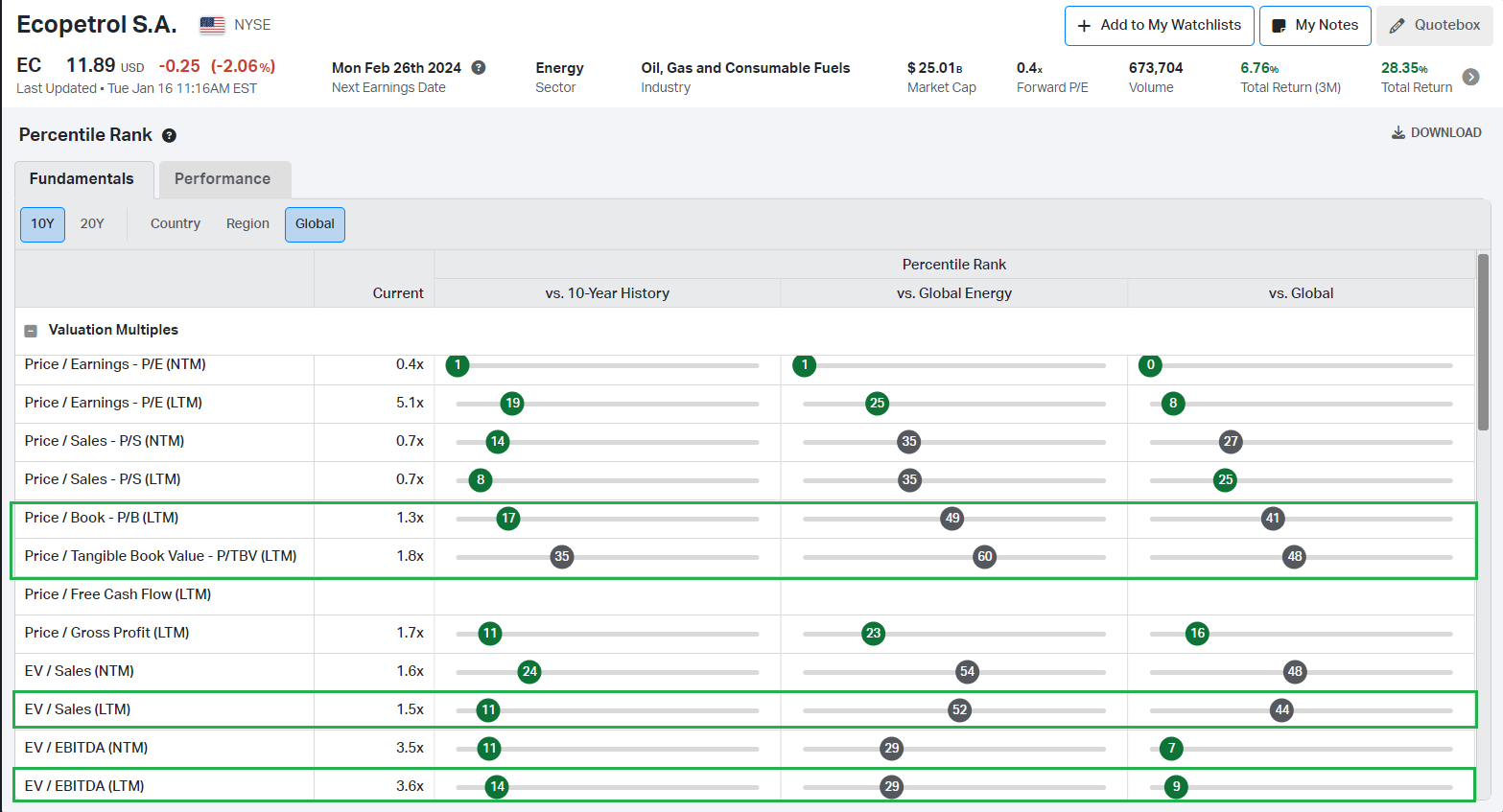

Valuation and price action

The Colombian stock market is one of the most undervalued equity markets globally. EC is a prime example of that. It trades in the bottom percentiles vs 10Y history, Global Energy, and Global Equity.

{kind=link}

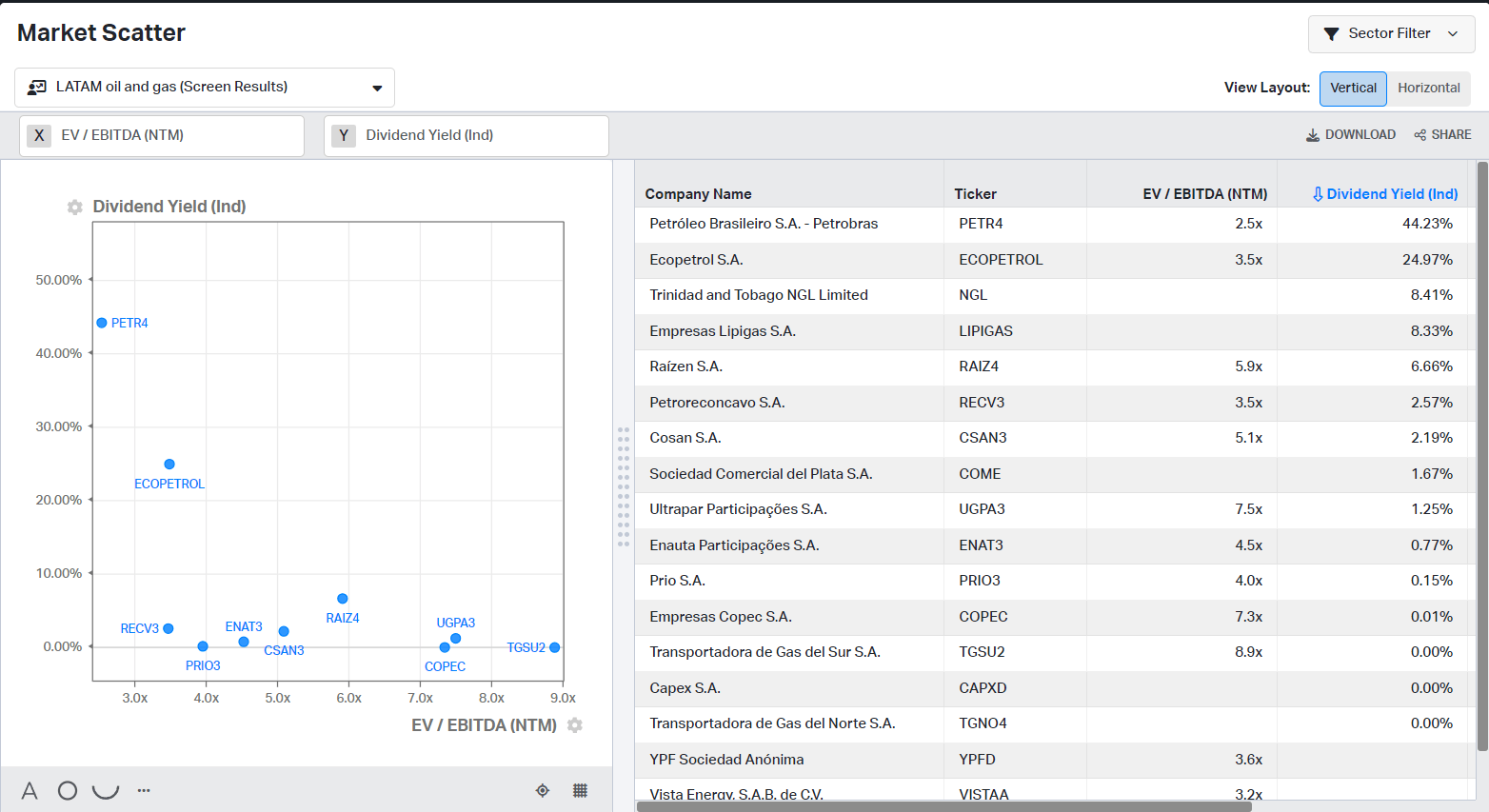

It is impressive how low EV/Sales and EV/EBITDA are. Adding excellent dividends, EC offers a lot of value for its price. The chart below compares Latin American oil and gas companies based on dividend yield and EV/EBITDA.

{kind=link}

EC trades at 3.5 EV/EBITDA NTM while providing dividends with a 24.9% yield (indicated). Given the chart above, PBR offers more value with 2.5 EV/EBITDA and 44.23 % yield. However, EC has a lower payout ratio.

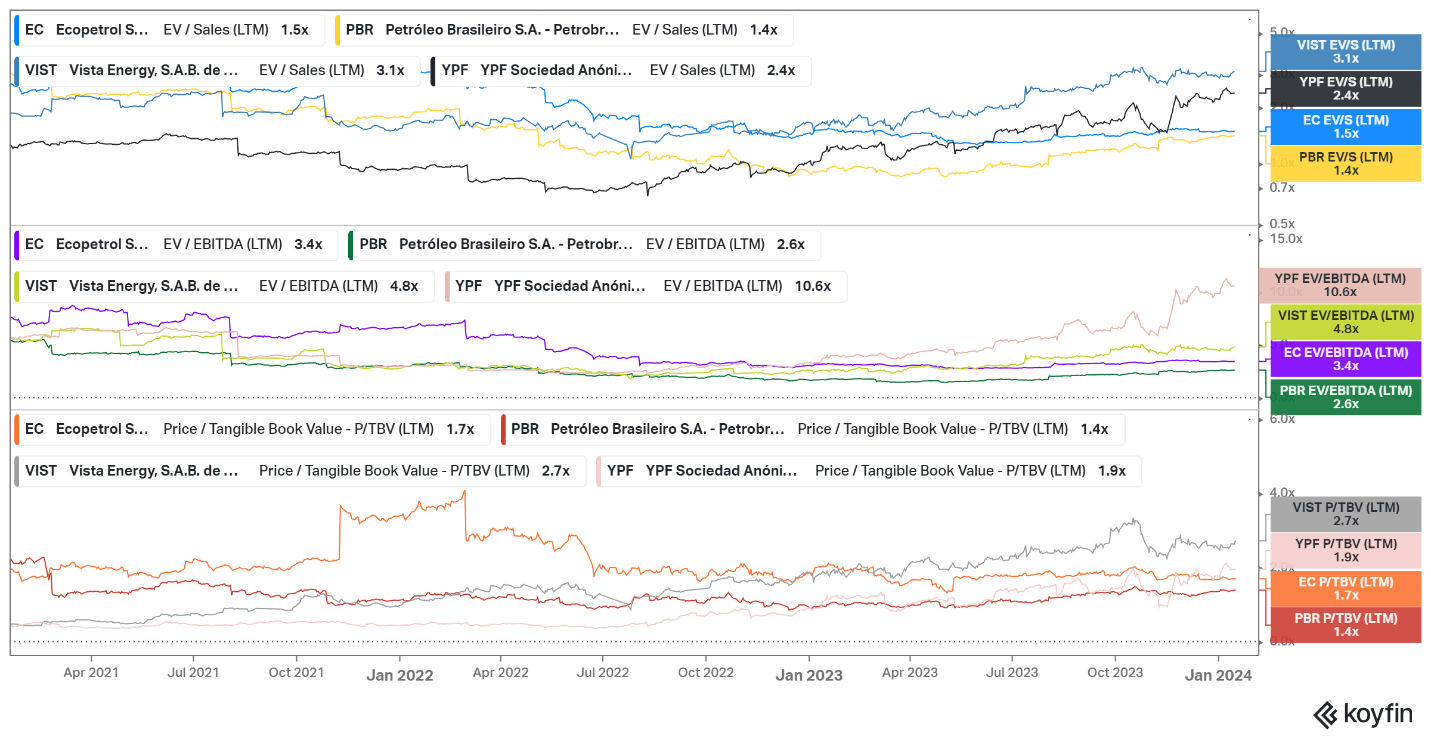

The next step is LATAM energy stocks based on EV/Sales, EV/EBITDA, and P/TBV. I picked PBR, Vista Energy ( VIST ), and YPF Anonima ( YPF ).

{kind=link}

YPF and VIST are Argentinean companies. PBR, YPF, and EC have one thing in common. Their largest shareholder is the government. YPF is the most popular because of the Petersen case . It is the most significant litigation case against Argentina. The court has ordered Argentina to pay the plaintiffs $16 billion in compensation.

Argentinean president Javier Milei shared his intention to privatize YPF. His election win and plans boosted YPF's price. However, compared to PBR and EC, YPF has less to offer. It does not pay dividends and trades at higher multiples. I am a dividend connoisseur, and having PBR and EC in my portfolio is a must. EC is undervalued compared to its global peers, past multiples, and dividend yields.

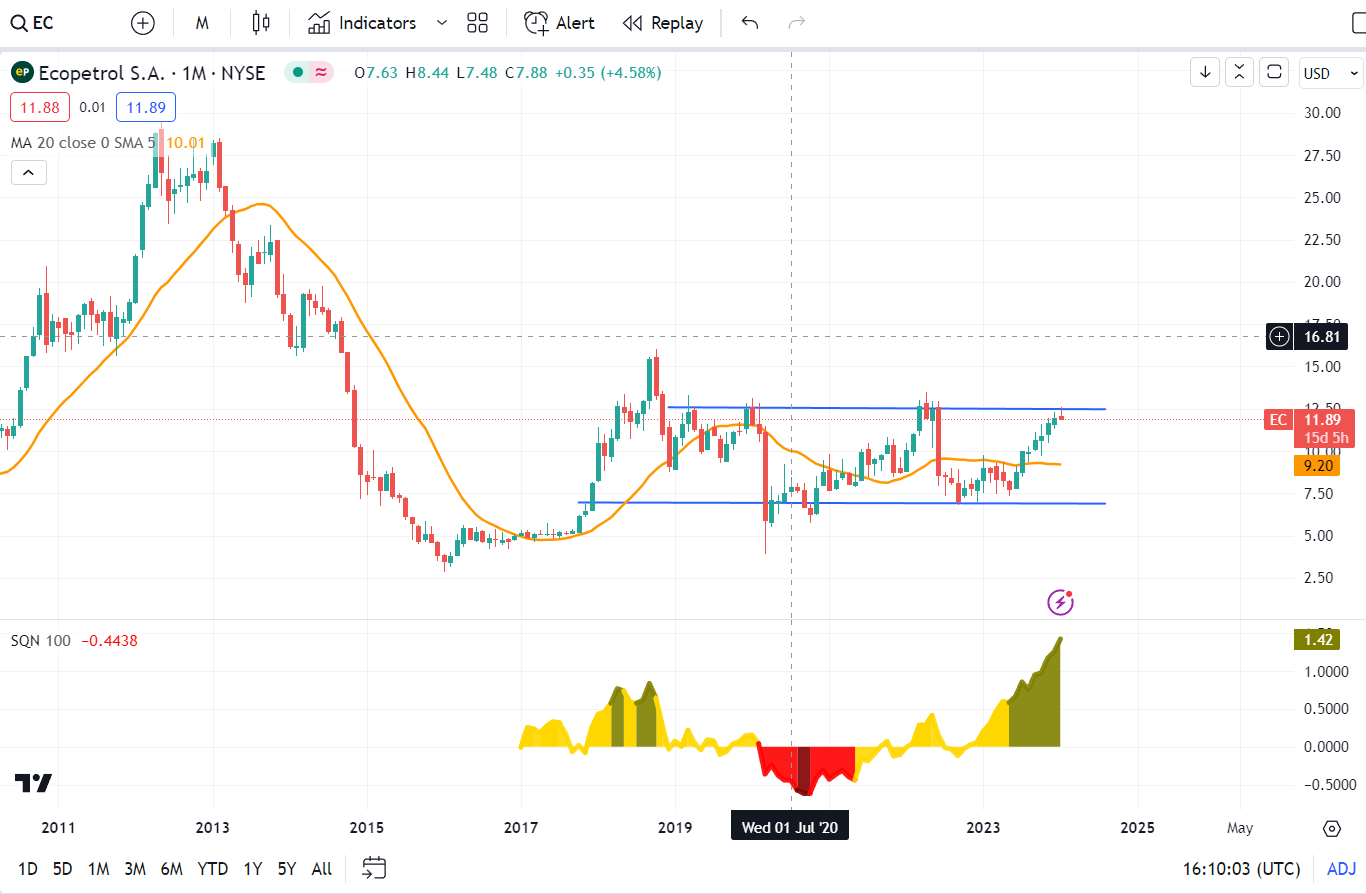

I mentioned the opportunity to start building a position in my previous article. My thesis remains intact, given the present price action.

{kind=link}

The price is close to a long-term resistance, defining the upper border of the rectangle. The horizontal trend lines are more reliable than their diagonal counterparts. The latter has the bad habit of morphing multiple times, giving false signals. A confirmed breakout on a horizontal trendline adds credibility to my thesis and serves as a signal to add more risk. Such is the case with the EC. I have been over 12 months; however, not all in. I will add more size once we have a breakout above the rectangle. The SQN indicator is in a bull-query regime, and the price is above 20 months' moving average ((MMA)). Simply put, I am stacking edges in my favor.

Some thoughts on geopolitics and Ecopetrol

Investing in emerging markets is a daunting task. It comes with high volatility and explicit uncertainty. The political risk brings both in abundance. The present Colombian president, Petro, is the first far-left leader of Colombia. He is a part of the pink tide that took over the continent in 2011. The next presidential election in Columbia is in 2025. I expect political shifts in the region. Milei`s win in Argentina and Nayib Bukele`s success in Salvador might ignite change to the right political spectrum.

The situation in the Middle East is getting worse day by day. The media ignores the profound effect of the attacks on the global supply chains and oil production and transport. Yesterday`s attack on the Iraqi city of Erbil from Iran means escalation. The missile aimed at the US consulate; however, it destroyed a residential building in the vicinity. Among the deceased is Peshraw Dizayee. He is a Kurdish billionaire involved in the oil business. His company, Falcon, provides services for the US government and US oil majors.

What does that mean for us? In my view, we trespassed the point of no return in the Middle East. The potential imminent scenarios lead to further escalation. Time will tell how bad it is and in what direction. The takeaway for me as an investor is to seek opportunities in oil-rich regions with lower geopolitical risk. Latin America comes to mind.

Investors Takeaway

Colombian equity is cheap even compared to Latin American markets. Colombian energy stocks are cheaper than their US counterparts, and EC is no exception. The company offers a lot for its price. However, before an EC rating, let`s point out the risks.

As discussed in the previous paragraphs, geopolitics is a tailwind for EC. Financially, the company is healthy, with liquidity covering its debts and capital investments. One more subtle risk is the refinancing of the debt. Most investors expect FED to lower the rates in 1Q24 or 2Q24. But the missing part from the puzzles is the creeping inflation. The supply chain disruptions have a lagging effect on consumer prices. I expect in February/March to see the first signs of inflationary pressures. This means rate cuts become questionable; hence, EC might refinance at higher rates. The company refinanced its 2025 notes.

I expect higher oil prices in the coming months. EC could use its excess cash to pay back its debt. Given a low payout ratio, the company will have spare firepower for debt payments while maintaining dividends with juicy yields. Declining oil prices is a significant risk. However, I am not expecting a significant oil price drop. The reason is simple: geopolitics.

3Q23 results confirmed my thesis: the company exceeds expectations, and betting on EC pays out. I have EC and plan to add more. I give EC a strong buy rating.

For further details see:

Ecopetrol: Still My Top Pick For Oil Stock