PRCT - EDAP: Reiterate Buy After Multiple Investment Updates

2023-07-14 16:23:57 ET

Summary

- EDAP TMS S.A. shares have pushed lower in H2 FY'23, presenting an opportunity to add on weakness.

- EDAP's Q1 revenues were up 13.8% YoY, with HIFU sales up around 40% YoY.

- On examination, sentiment and positioning remains bullish in the stock based on market and options-generated data.

- Net-net, reiterate buy at $15 price objective.

Investment updates

Following my publication in April on EDAP TMS S.A. ( EDAP ), shares have corrected ~16.5% to the downside, presenting an ample opportunity for those long of the stock to add to their positions on the weakness.

There have been several updates to the EDAP investment debate that I will run through here today. Chiefly, you need a gauge on the company's fundamental outlook, combined with the current sentiment in its stock, and valuations investors are asking to pay, and this report will cover each of these factors.

As a reminder, the buy thesis on EDAP is formed by:

- EDAP is building momentum around its High-Intensity Focused Ultrasound ("HIFU") business [check the previous publications for a deep dive into HIFU - you can see them here , here , and here ].

- Expansion of HIFU into potential applications for endometriosis.

- Growth estimates call for 20%+ at the top line for FY'23 on c.45% gross margin.

Net-net, following the positive investment updates discussed here, I am reiterating EDAP as a buy, maintaining the $15 price objective in situ.

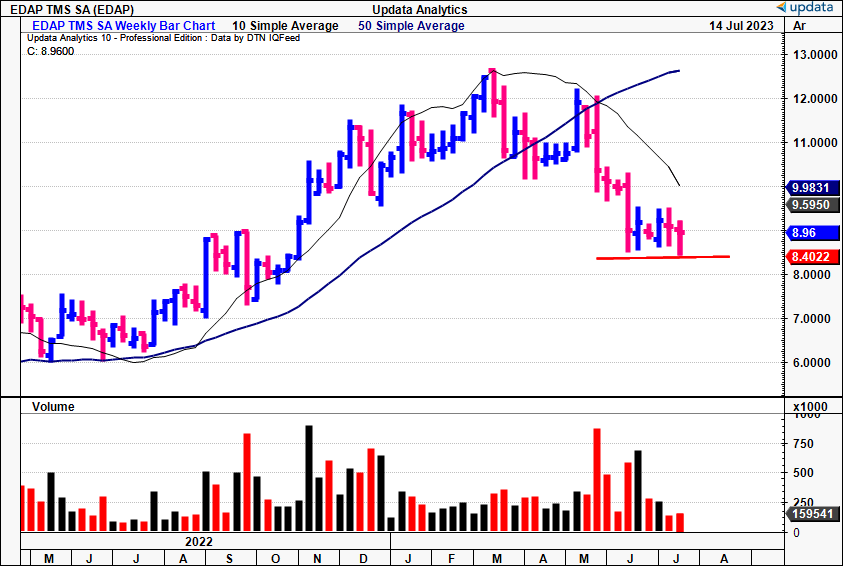

Figure 1. EDAP correction from May FY'23

{kind=link}

Changes to investment facts

Following its Q1 numbers back in May, and the subsequent market activity following, there are notable changes to the EDAP investment debate. You're looking at a revision in forecasts, changes in sentiment, asset factors, earnings power and valuation factors as the major crosscurrents feeding into the EDAP electricity grid.

1. Financials - ratcheting higher

EDAP's Q1 numbers reveal plenty about the full-year expectations of its financials. I'll run through the figures here and link this back to my own forecasts.

Starting with the quarter, EDAP clipped total revenue of €14.8mm, a growth of 13.8% YoY [note: EDAP reports in Euros, and I'll keep the same convention here so as to avoid confusion. At the time of writing, 1 EUR = USD 1.12] . Growth was underscored by performance across the entire portfolio:

- HIFU sales were up ~40% YoY to €5.3mm for the quarter. This stemmed from the placement of 6 Focal One units. The average sale price ("ASP") was therefore €0.883mm. In comparison, it moved 4 units in Q1 FY'22, so the cadence of placements is increasing, but ASP was down from €0.95mm.

- Similarly, the LITHO (Lithotripsy) business pulled in €2.8mm versus €2.2mm last year, 4 lithotripsy units sold during the quarter. This is 3 more on Q1 last year, adding to the momentum points above.

- Despite a slight decline in total revenue for its distribution arm -which amounted to €6.8mm vs. €7.0mm in the previous year- management is still bullish on long-term growth.

- Added to this, the company sold 8 ExactVu units during the quarter, following the ultrasound biopsy's approval in Japan earlier this year. As a reminder, it sold 9 in Q1 last year, so this isn't too far off the mark, and still a strong number in my estimation.

Moving down the P&L , it pulled the c.€15mm to 41% gross, with ~300bps of margin compression YoY resulting from the firm's investment in its U.S. markets, that are booked as expenses under cost of sales due to GAAP accounting rules. Quarterly OpEx pulled to €12.6mm, up more than 100% YoY.

I'd note that a good portion of this 'expenditure' was again investment in human capital and marketing efforts in the U.S. to drive sales there. Still, the operating loss was €6.6mm for the quarter. Alas, several adjustments must be made. My estimates for the investment component expensed for EDAP under GAAP convention are ~35% of total OpEx, bringing the adj. operating loss to ~€2mm. As a side note, Mauboussin (2022) found that treating ~30% of SG&A and other OpEx as investments is acceptable, therefore I am confident with this adjustment for EDAP.

2. Clinical trial updates

In addition to the financial momentum, EDAP has also made progress across several of its clinical programs this year.

For one, it recently announced positive clinical results from its Endo-HIFU-R1 Phase 2 study , that was investigating the safety and efficacy of therapeutic HIFU for the treatment of rectal endometriosis. On my analysis, safety and efficacy data held up well, with a particular focus on symptom reduction, improved quality of life, and a significant decrease in lesion volume within the endometriosis cohort of the study.

Two, at the 38th Annual Congress of the European Association of Urology, EDAP presented readouts from its large-scale, non-inferiority study comparing HIFU to radical prostatectomy as a first-line treatment for localized prostate cancer. For patients treated with HIFU compared to those who underwent radical prostatectomy, the study demonstrated:

- Favorable salvage treatment-free survival rates, and;

- Improved urinary incontinence and erectile function outcomes.

It's important to note that patients who undergo conventional forms of prostate surgery -like radical prostatectomy- leave patients with quite poor outcomes, especially with incontinence (both urinary and fecal), erectile dysfunction, and, ultimately, a poorer quality of life. In that vein, ANY procedure that produces the same treatment effects, albeit with improved patient outcomes, is a major medical breakthrough in this segment, without debate. This is a central point to my EDAP buy thesis, and, whilst there are competing names out there [think Profound Medical ( PROF ), and PROCEPT BioRobotics ( PRCT ), both names I've covered - see my coverage on each here and here, respectively], EDAP's HIFU theses are appealing to my investment cortex.

Three, as I covered in my April publication, EDAP obtained approval from Japan's Pharmaceutical and Medical Devices Agency ("PMDA") for commercializing its ExactVu line. ExactVu is a micro-ultrasound unit, that functions on a 29 MHz frequency and is used for prostate imaging and biopsy. This is a big feat- getting approval for any medical device in Japan isn't straight forward. For starters, it is all governmental factions that make approvals, unlike the FDA in the U.S. for example. It also faces additional scrutiny being a foreign-made device. Prostate cancer is the most prevalent cancer among Japanese men, with more than 100,000 cases diagnosed each year. Hence, EDAP has potential to penetrate this market and earn its share of revenues from treating patients in Japan and making a difference to their lives.

3. Sentiment and valuation

There have been 3 upward revisions to EDAP's revenue estimates by The Street over the past 3 months. Similarly, 1 downward revision has been made to balance the equation. Consensus now calls for 14% YoY growth in sales to €68.7mm, stretching up by 14% to €78mm in FY'24. I've revised my forecasts higher, too [see: Appendix 1], now calling for €74.7mm in FY'23 revenue (from €70mm prior) and €91mm in FY'24 (up from €84mm prior).

Looking to the options-generated data , calls expiring for August have the most concentrated demand at a strike of $12.50, with open interest extending to a strike depth of $20. This tells me investors -those with actual money at risk- are bullish on EDAP up until this mark. If you believe the market is a fair estimate of value, this data adds a heavily bullish weight to the risk-reward calculus.

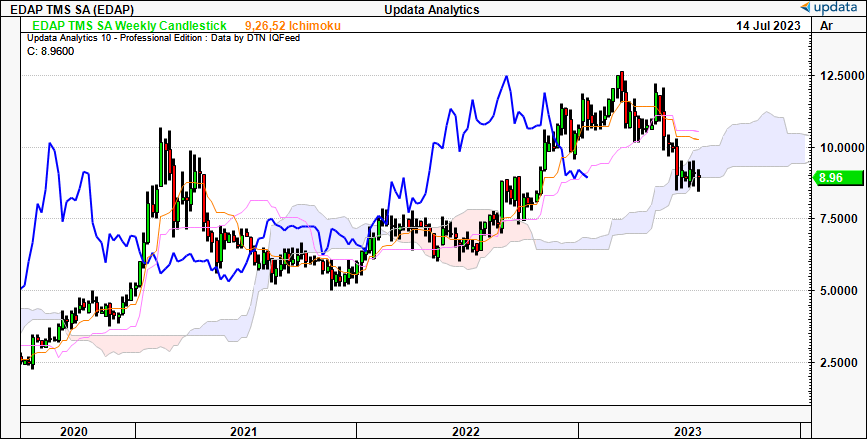

Finally, looking at trend indicators via the weekly cloud chart below, EDAP is currently testing the base of the cloud. This would be a crucial turning point for EDAP in trend-terms for me, and we'd need it to bounce from this level in order to stay within the longer-term trend. Most importantly, the lagging line (shown in blue) is still well above the cloud, suggesting we are still bullish on a directional bias. This also confirms my reiterated buy thesis.

Figure 2.

{kind=link}

EDAP trades at more than 4x forward sales, which, may be quite the premium, but also tells me investors are expecting a high growth period from the company. Added to this, the company trades at 4.5x book value - a clear indication it has added $4.50 in market value for every $1 in net asset value EDAP has clipped each period. This is telling. It shows the market places a high value on EDAP's assets (HIFU being the main one) and ties in with the bullish positioning in the stock described earlier. I would be happy paying 4x sales for 1) the numbers projected in my own analysis, 2) the market's viewpoints, and 3) the fundamental changes HIFU looks to make in treating prostate cancer. Last publication, I said I was looking for a price objective of $15 for EDAP, and I'll hold this in place after the latest updates. Hence, this also supports the buy call.

In short

EDAP continues ratcheting higher on a sales and valuation front. Each of these are conducive to a company growing in value as time rolls on. The HIFU segment, being the clear differentiator for EDAP, also continues building momentum. You see the company pushing up the cadence of new EDAP placements, along with steady numbers in its broad portfolio. As a result, investors, analysts, and all between, appear to be bullish on EDAP's prospects, in line with my own viewpoint. Not that consensus is needed - I often stay away from overcrowded trades - but there's more to think about here. EDAP has the potential, along with its competitors, to make a large medical change in the outcomes for prostate cancer survivors. In that vein, that EDAP continues pushing ahead fundamentally, backs up the company's underlying mission just fine in my eyes. Net-net, I am reiterating EDAP as a buy, looking for $15 per share over the coming 6-12 months.

Appendix 1. EDAP Forecasts, FY'23-25

{kind=link}

For further details see:

EDAP: Reiterate Buy After Multiple Investment Updates