NTCO - Edgewell Personal Care: Still A Healthy Prospect To Consider

2023-09-27 06:56:48 ET

Summary

- Edgewell Personal Care Company has experienced a 7.1% decline in its stock, despite being rated a 'buy' and offering upside potential.

- The company's fundamental data shows positive performance, with increased revenue, net income, and operating cash flow.

- Management expects organic revenue to climb by 3-5%, and earnings per share to be between $1.95 and $2.15, indicating positive growth prospects.

- Add in how cheap the stock looks and it's difficult to not be bullish on it.

There are all sorts of ways to make and lose money in the stock market. But if you are planning to be a value investor, you should be prepared to take a beating, sometimes for a while, before you can be right. One company that I wrote about earlier this year that I mentioned offered upside potential for investors is Edgewell Personal Care Company ( EPC ), a provider of personal care products such as razors, sun and skin care products, feminine care offerings, and more. Unfortunately, things have not been going exactly according to plan. While I rated the company a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future, the stock has actually generated downside of 7.1%. That compares to the 9% upside seen by the S&P 500 over the same window of time. Even with this pain, however, the stock does look attractively priced to me and, in the long run, I suspect that my bullish thesis will be proven correct.

A picky market

When I last wrote about Edgewell Personal Care Company in January of this year, I talked about how the firm had experienced some pressure on both its top and bottom lines leading up to that point. But between how bullish management was for the 2023 fiscal year and how cheap shares were, I could not help but rate it a 'buy'. Fast forward to today, and it may seem as though, judging from the market's reaction, the fundamentals might not be so great. But when you actually look at the fundamental data, you find a company that is thriving.

{kind=link}

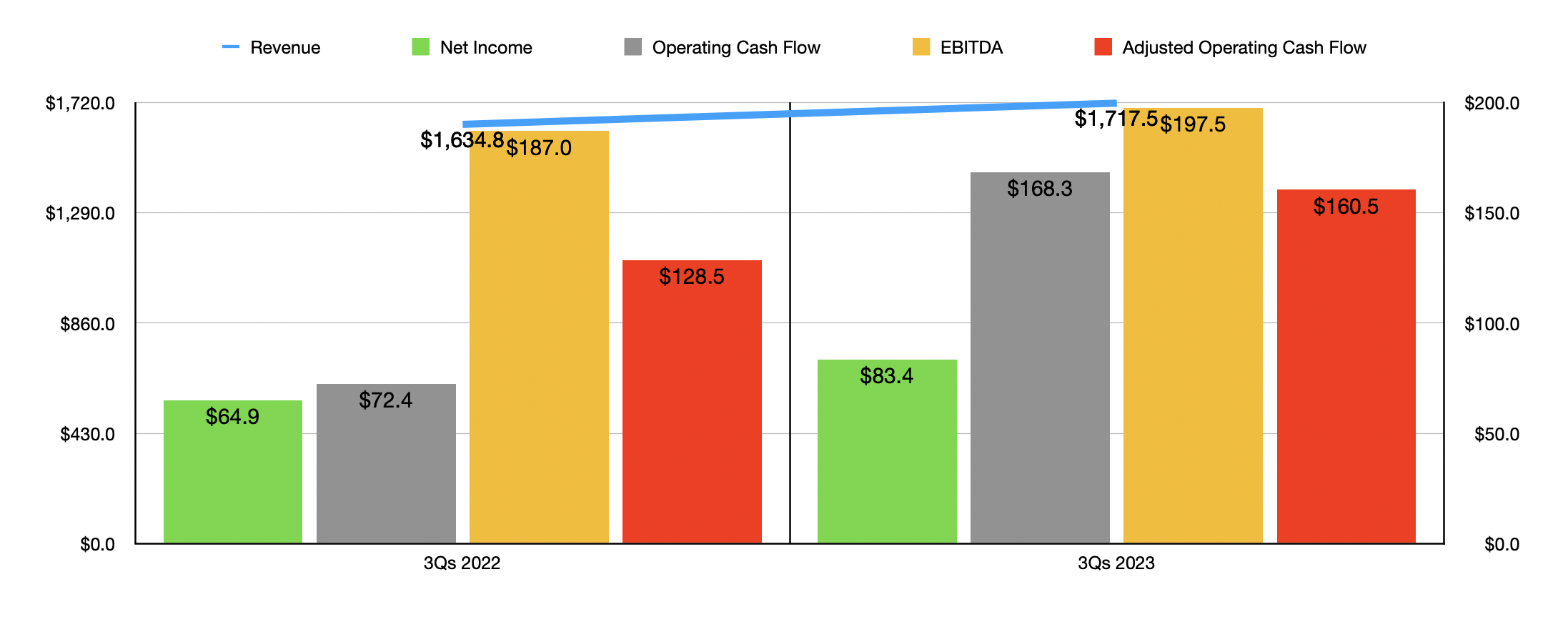

Consider, for starters, how the business performed during the first nine months of its 2023 fiscal year. Revenue for this time came in at $1.72 billion. That represents an increase of 5.1% over the $1.63 billion generated one year earlier. Sales would have been higher had it not been for a $33.7 million impact caused by foreign currency fluctuations. It is true that $12 million of this increase was attributable to its acquisition of Billie. All of the rest of the increase, $104.4 million in all, was driven by organic expansion, with management chalking this up to a 9.2% revenue growth in the international markets thanks to its sun care and wet shave products, and a 4.8% rise associated with its sun care and men's grooming and feminine care products throughout North America.

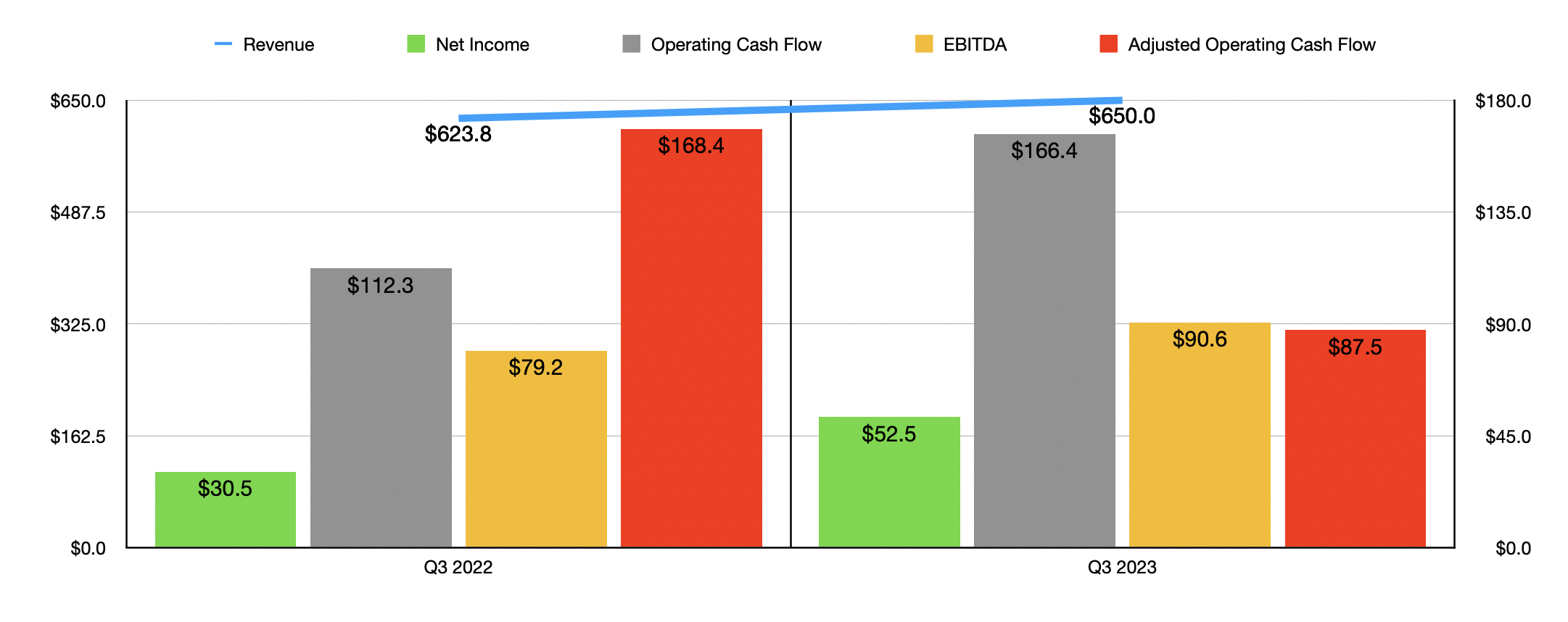

On the bottom line, the picture has been positive as well. Net income of $83.4 million beat out the $64.9 million generated in the first nine months of the 2022 fiscal year. Operating cash flow, meanwhile, skyrocketed from $72.4 million to $168.3 million. If we adjusted for changes in working capital, we would have gotten a rise from $128.5 million to $160.5 million. And finally, EBITDA for the company grew from $187 million to $197.5 million. For those worried more about the present day, I would say that any concerns are likely overblown. As you can see in the chart below, for the third quarter on its own, revenue, profits, and two of its three cash flow metrics, are all higher year over year.

{kind=link}

For the year as a whole, management has provided some guidance . They currently anticipate organic revenue climbing by between 3% and 5%, with total revenue coming in a bit lower than this at between 2% and 4%. Much of that disparity can be attributed to pain caused by foreign currency fluctuations. Even though we are dealing with a great deal of economic uncertainty, this kind of growth should be expected. If anything, it's a bit on the low side. I say this because, according to a report by McKinsey & Co., beauty retail sales are expected to grow by about 6% per annum from 2015 through 2027. This year, they should be around $460 billion globally, which would be 7.7% above the $427 billion generated in 2022. The North American market alone should expand by 7.1% from $85 billion to $91 billion.

Operationally speaking, Edgewell Personal Care Company focuses on what McKinsey would consider the hair care and skin care categories of the beauty space. The skin care space is expected to grow at a rapid pace in certain markets. In North America, for instance, it should grow by roughly 6% to $10.9 billion. The hair care market should grow even more by 7% to $7.2 billion. In places like China and elsewhere, growth is comparable to this or even greater.

On the bottom line, management expects earnings per share of between $1.95 and $2.15. This is actually up from prior guidance of between $1.80 and $2. On an adjusted basis, we are looking at earnings of between $2.30 and $2.50. At the midpoint, this would translate to profits of about $124.3 million. Management also said that EBITDA should now come in above the high end of its range. That range was between $320 million and $335 million. Because we don't know how much above management is forecasting, I have, for the purpose of this article, assumed that it will match the $335 million reading. No guidance was given when it came to cash flow. But a rough estimate that I conducted calls for it to come in at around $183 million.

{kind=link}

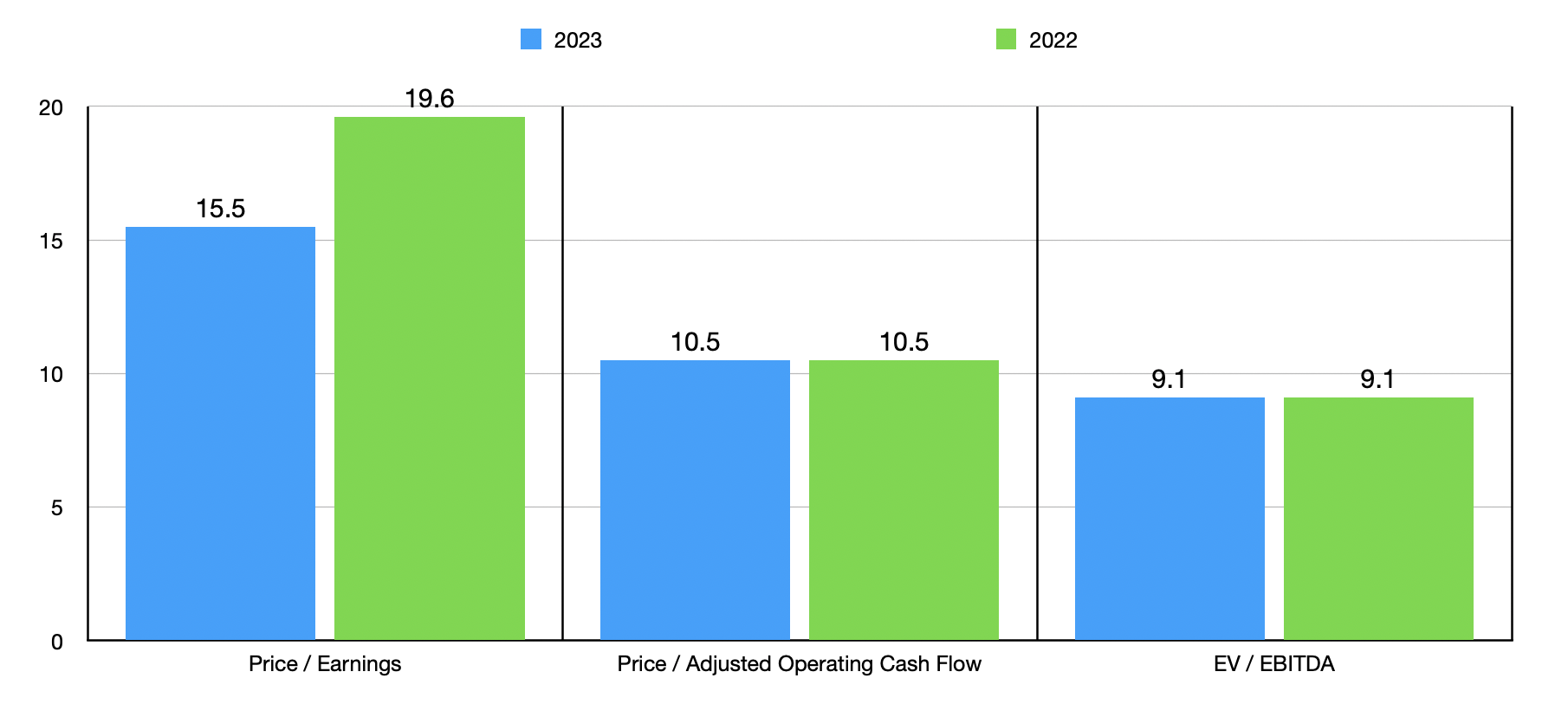

Using these figures, I was able to create the chart above. In it, you can see that the forward price to earnings multiple for the company is 15.5. That's down from the 19.6 reading that we get using data from last year. The forward price to adjusted operating cash flow multiple and the forward EV to EBITDA multiple, however, should both approximately match what the company saw in 2022. Those would be readings of 10.5 and 9.1, respectively. As part of my analysis, I then compared the company, I decided to compare it to five similar firms in the table below. Using both the price to earnings approach and the price to operating cash flow approach, I found that only one of the companies was cheaper than it. And when it comes to the EV to EBITDA approach, two of the five were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Edgewell Personal Care Company |

| 15.5 |

| 10.5 |

| 9.1 |

| e.l.f. Beauty ( ELF ) |

| 61.2 |

| 64.4 |

| 43.4 |

| Coty Inc. ( COTY ) |

| 20.6 |

| 16.5 |

| 10.4 |

| Inter Parfums ( IPAR ) |

| 29.5 |

| 28.9 |

| 17.0 |

| Olaplex Holdings ( OLPX ) |

| 11.3 |

| 6.9 |

| 6.8 |

| Natura & Co ( NTCO ) |

| N/A |

| 140.7 |

| 7.0 |

Takeaway

Even though the market has not treated Edgewell Personal Care Company and its shareholders very well recently, I believe that the broader picture for the business is positive. The industry it's in is growing at a nice clip and overall fundamental performance is robust. Add on top of this how cheap shares are, both on an absolute basis and relative to similar companies, and I still believe that a 'buy' rating is appropriate at this time.

For further details see:

Edgewell Personal Care: Still A Healthy Prospect To Consider