EIC - EDI: Emerging Markets Offer Opportunity For The Risk-Tolerant In High-Yield Fixed Income

Summary

- Emerging markets are showing signs of recovery, and fixed-income assets in hard-currency terms represent a rare buying opportunity due to mispricing.

- The performance of Stone Harbor Emerging Markets Total Income Fund has been sub-par until recently, but now offers a relatively low risk, high yield income investment opportunity.

- The outlook for EM debt for 2023 and beyond is encouraging and risk-tolerant investors seeking high yield income may wish to consider EDI now while the price is low.

When searching for high-yield income funds to generate passive income for retirement, most investors start with the past performance of a potential investment to attempt to discern patterns or price history that might indicate whether they feel it is a good investment for the future. It is basic human nature to believe that what happened in the recent past is likely to continue, or at least follow a similar pattern, in the near future. However, when it comes to investing choices there are a host of factors and macroeconomic conditions that can greatly influence the future behavior of a particular investment that may look nothing like what happened in the past.

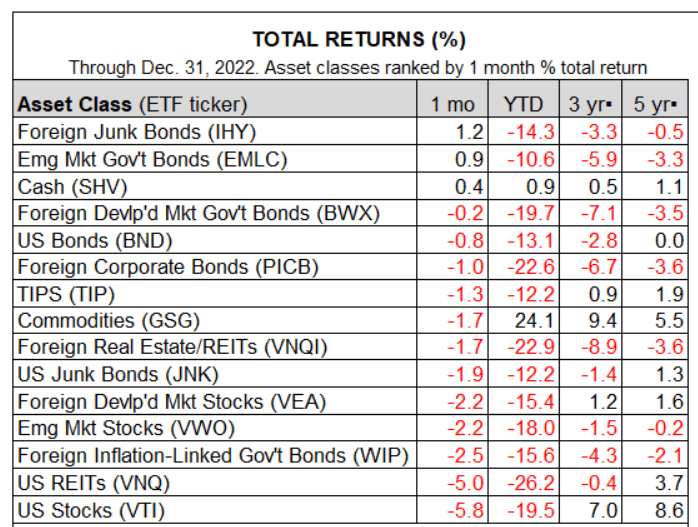

When looking at major asset class performance, it becomes evident that different asset classes perform differently over different periods of time. One of my fellow contributors on Seeking Alpha offers a review of major asset classes, and his chart from the December version clearly shows how emerging market ("EM") government bonds performed poorly over the past year, 3-year, and 5-year periods, but began to recover in December.

{kind=link}

Looking even farther back in time, emerging markets have underperformed developed markets for most of the past two decades. What this means for investors now is that opportunities in emerging markets represent some of the most mispriced asset classes that offer attractive valuations based on historical levels. According to this report from Lazard, emerging markets now represent an excellent long-term value given a global backdrop that is supportive of both fixed income and emerging markets.

It is difficult to imagine a more challenging backdrop for emerging markets debt than the one that unfolded over the course of 2022: Stubbornly high inflation, aggressive monetary tightening, slowing global growth, the war in Ukraine, and record investor outflows all contributed to one of the worst drawdowns ever for the asset class. However, we believe the outlook for 2023 is significantly better given the rare combination of elevated yields, attractive valuations, and a global backdrop that is more supportive of both fixed income and emerging markets.

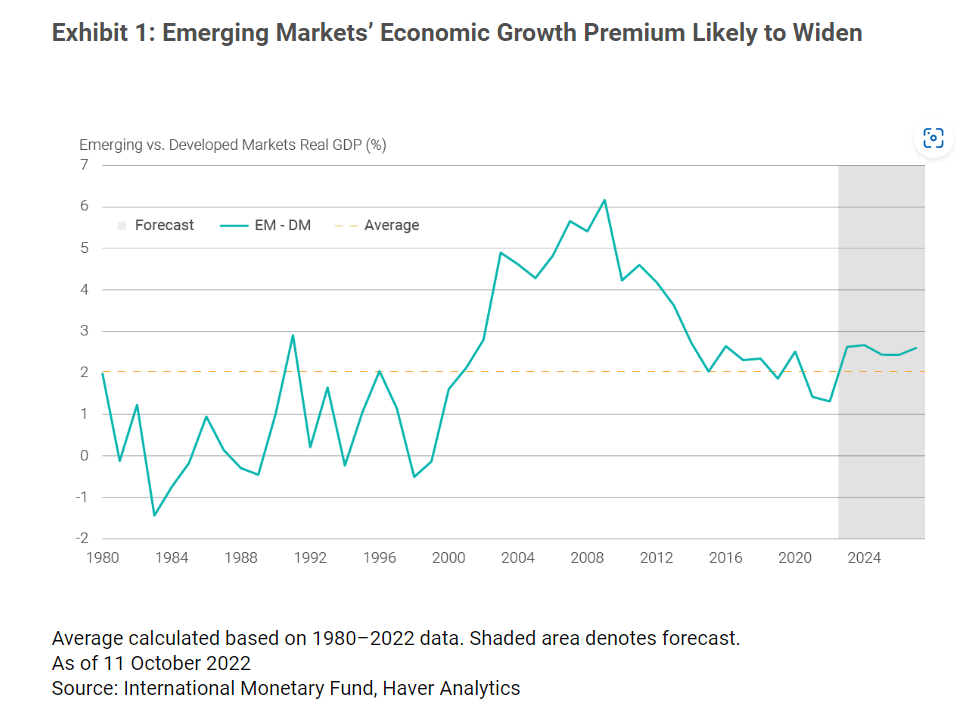

Furthermore, the growth premium in emerging markets relative to developed markets is increasing and is likely to continue to widen as inflation recedes, the strength of the U.S. dollar declines, and leading indices such as manufacturing purchase managers surveys point to growing economic opportunities in Latin America, Africa, and other developing economies.

{kind=link}

Furthermore, the opportunity in emerging market debt is even more salivating due to the equity-like returns (mid-teens) that are now possible over the next 12 months in both hard currency and local currency debt due to a confluence of factors including record-high bond yields that have not been seen since the Great Financial Crisis ("GFC").

In hard currency debt, the yield on the JPMorgan Emerging Markets Bond Index Global Diversified (JPM EMBI GD) now stands at around 8.5%, and notwithstanding the rally since mid-October, has not been higher since the Global Financial Crisis. The elevated yield is partly a reflection of the pain inflicted by rising US Treasury bond yields as the Federal Reserve raised interest rates throughout 2022 and partly due to spread widening from the tightening of financial conditions and broad-based risk aversion last year.

The Opportunity in EDI (and EDF)

One fund that I believe represents an excellent opportunity for income-oriented investors with a long-term view is the closed-end fund ("CEF") now called Stone Harbor Emerging Markets Total Income Fund ( EDI ). The EDI fund was taken over by Virtus, and the fund name was changed in April 2022 after Virtus acquired the assets from Stone Harbor. The other sibling fund that was acquired from Stone Harbor that also holds emerging market securities is the Virtus Stone Harbor Emerging Markets Income Fund ( EDF ). The two funds are very similar in many ways, with the primary difference being that EDF is a slightly larger fund with about $75M in net assets under management, or AUM, while EDI is a bit smaller with about $51M in net AUM. Both funds specialize in EM debt, although EDI may also hold some EM equity positions as well. Both funds offer very high yield distributions (both currently exceed 14%) and both trade at a premium to NAV.

For purposes of this article, I intend to focus the discussion on EDI, primarily because the current premium at the time I am writing this is about 7% for EDI, while EDF is trading at a premium exceeding 15%. The fund overview from the website states:

The Fund's primary investment objective is to maximize total return, which consists of income on its investments and capital appreciation. The Fund will normally invest at least 80% of its net assets (plus any borrowings made for investment purposes) in emerging markets debt.

EDI had an inception date of 10/25/2012 and pays a monthly dividend of $0.07, yielding 15.2% at the current market price of $5.52 as of 2/17/23, while NAV was $5.14, leading to the 7.4% premium. Total share count is just under 10 million shares with about $63 million in managed assets employing about 20% effective leverage as of 1/31/23.

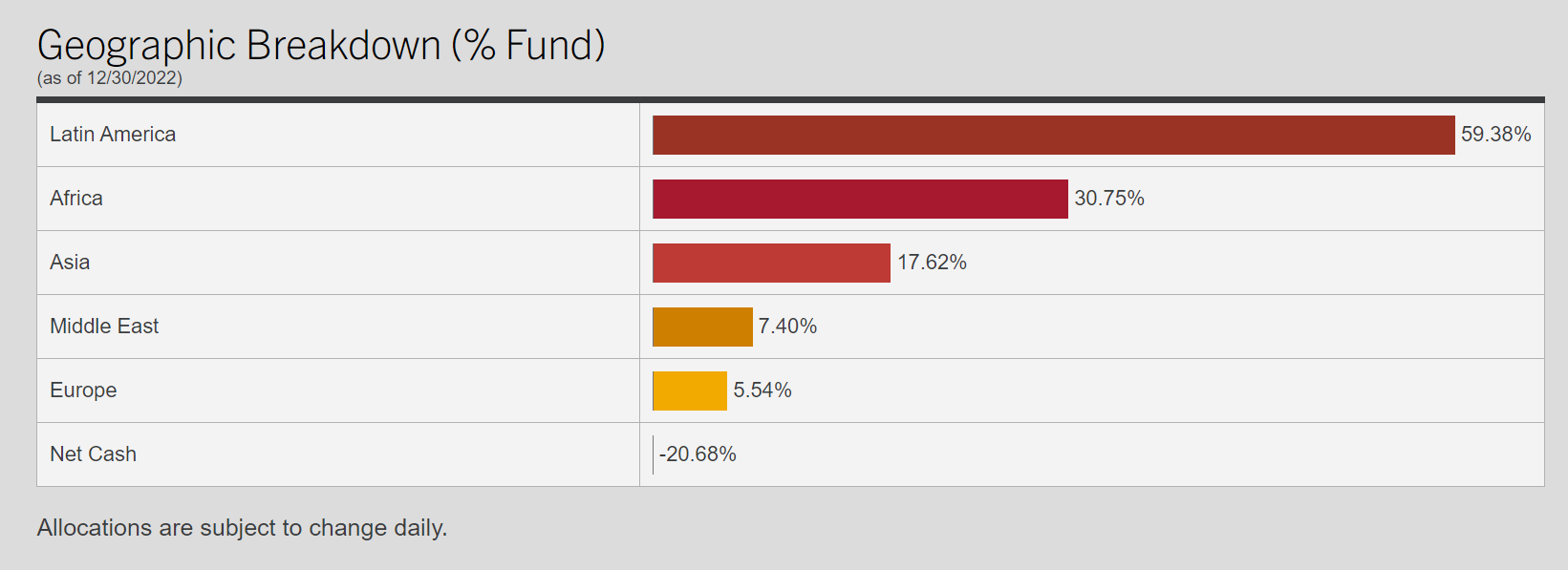

The current geographic breakdown of the fund shows a primary emphasis on Latin America, with nearly 60% of holdings from those countries. Africa is the second largest concentration with about 30%. Mexico holdings make up more than 20% of the fund, which is not surprising given the expectations for economic growth in Mexico from the manufacturing boom that is underway.

{kind=link}

The credit quality, not surprisingly, consists of BBB-rated and below credit ratings, which is not unusual for EM fixed income as illustrated on the fund fact sheet dated 12/30/22.

fund fact sheet

As mentioned above, hard currencies and local currencies in many emerging market countries are starting to rally in 2023 as the U.S. dollar shows signs of weakening. According to this article from Morgan Stanley, this trend is likely to continue for the foreseeable future, and EDI is well-positioned to take advantage of this opportunity.

Technicals started to recover in the last few months of 2022, but January saw a substantial shift in investor interest for the asset class. Both hard and local currency funds experienced notable inflows with $5.8 billion and $1.9 billion, respectively. All EMD risk factors produced positive performance during the month.

In the current EDI portfolio, the sector allocations show about 78% in sovereign hard currency, 26% in corporate hard currency, 15% in local hard currency, and -20% net cash (i.e., leverage). From the fund’s annual report dated November 30, 2022, the management commentary summarized the positive contributors to the fund during the year, which I also see as potential tailwinds heading into 2023:

The largest positive contributors to performance were sovereign and corporate debt of select commodity oil exporters, including Angola and Mexico. Other positive contributors to performance included hard currency sovereign debt exposure in Tunisia, corporate debt exposure in Jamaica, and local currency sovereign debt exposure in Mexico and Brazil.

Many of the negative contributors to fund performance in 2022 were related to impacts of the Russian invasion of Ukraine (including bond exposure to Russia, Ukraine, and Belarus), escalating inflation, rising interest rates by central banks, and hard currency sovereign debt exposure in several countries that struggled in 2022 including Pakistan, Ghana, and Ecuador.

Putting the past in the rear view mirror and looking ahead, I see more opportunities than downside given the apparent recovery in many emerging markets heading into 2023. With China reopening its economy and Mexico and other emerging markets experiencing growth rates generally exceeding those of more developed nations like the U.S., UK, and Europe, the future looks promising for EM debt investments to offer high yields with relatively less risk than what we have seen since the onset of Covid-19 in 2020.

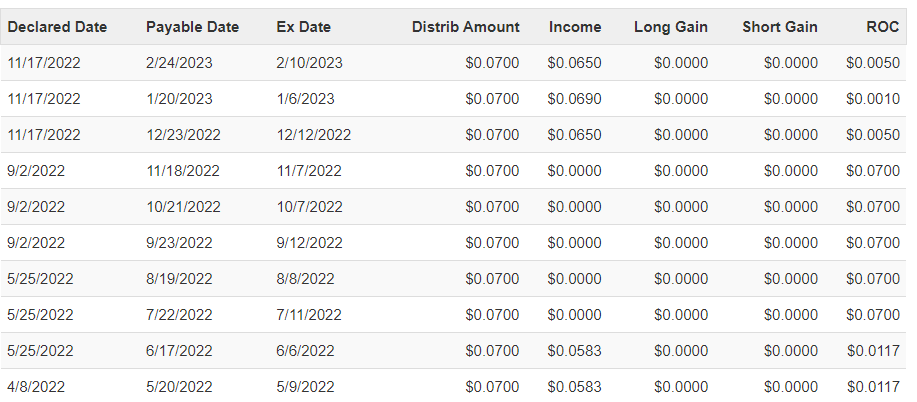

The outlook for EM foreign currency valuations is improving and sentiment appears to be shifting in favor of those countries as explained in the Morgan Stanley report . As the EDI fund makes adjustments to its portfolio holdings, the fund performance is showing signs of recovery, with the NAV starting to stabilize and trend upwards, while distributions consist of mostly income rather than ROC for the most recent three months as shown on CEFConnect (and verified by section 19a notices posted on the fund website).

{kind=link}

The performance of the EDI fund in 2022 was nothing to get excited about, and I would not have recommended the fund a year ago. A lot has changed in the past year though, and especially in the past few months. The combination of emerging market growth potential with very high yielding fixed income opportunities at low cost of entry offers a rare opportunity to initiate a position in the fund now to secure future passive income, along with other high yield income funds that I have recently reviewed.

Comparing EDI with Other High Yield Fixed Income Funds

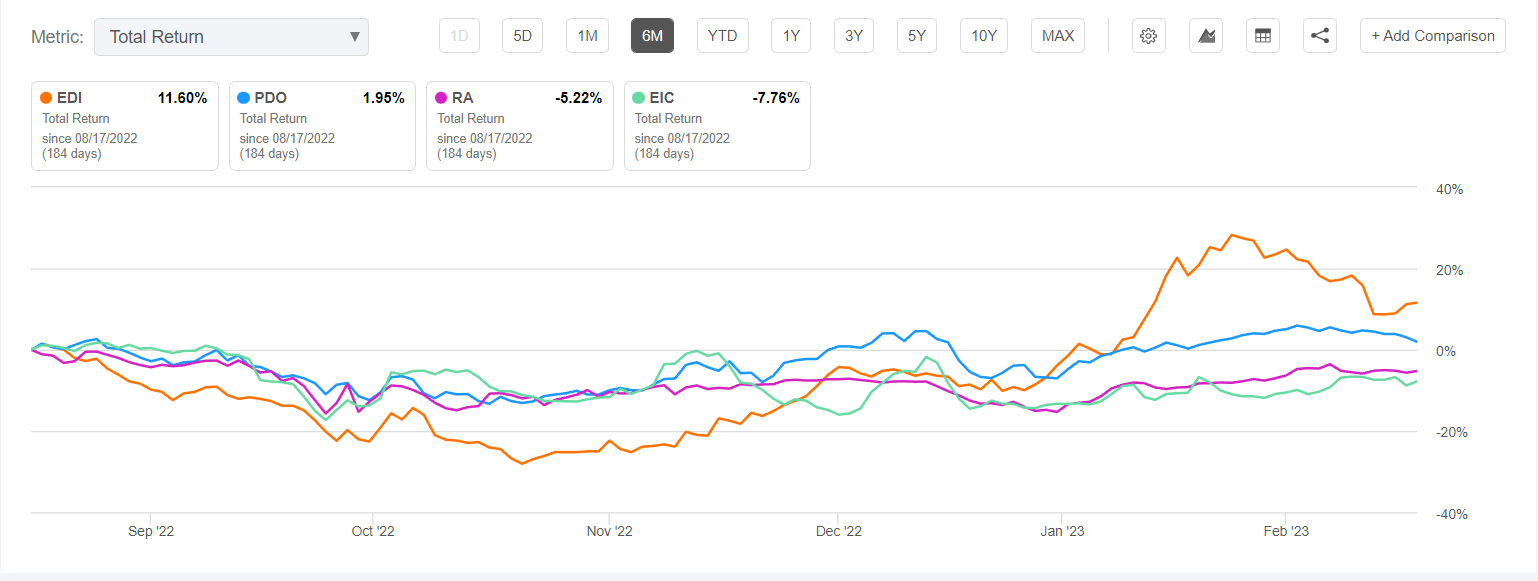

Out of curiosity, I took a quick look at some of the other high yield fixed income funds that I have recently reviewed and compared the total returns over the past 6 months with EDI. The chart below shows the 6-month total return for EDI compared to 3 other funds – Brookfield Real Assets Income ( RA ), PIMCO Dynamic Income Opportunities ( PDO ), and Eagle Point Income ( EIC ). The chart surprised me.

{kind=link}

This is not to say that you should sell your other high-yield income funds and jump into EDI. There are risks and tradeoffs, with each asset class and EDI definitely having its share of risks to consider. The fund adviser is new, with Virtus acquiring Stone Harbor, although some of the fund managers have been involved in managing the fund since its inception, including James E. Craige, CFA, who was co-founder of Stone Harbor. There are geopolitical risks, currency risks, and macroeconomic risks that are difficult to predict in these uncertain times that we live in.

On the other hand, there are indications that 2023 is starting out to be a bit more optimistic from the perspective of both fixed income and emerging markets. The EM debt asset class has been on the low end of the totem pole for quite some time and now is showing signs of recovery. I like the potential for EDI to outperform in the coming years as the global economy continues its post-pandemic recovery while offering mispriced values for selective holdings in emerging market economies that are realizing the benefits of a weaker U.S. dollar and slowing inflation.

I am cautiously optimistic on EDI as a long-term income holding and I believe that the distributions are now well-covered and should be a reliable source of high yield income in 2023 and beyond. I rate EDI a Buy at the current price and will be looking to add some shares to my own No Guts No Glory IRA portfolio .

For further details see:

EDI: Emerging Markets Offer Opportunity For The Risk-Tolerant In High-Yield Fixed Income